IAG - Iamgold: Turnaround Thesis Remains Intact

2023-12-12 05:45:32 ET

Summary

- Iamgold reported mixed Q3 results, with a decline in production and higher operating costs, resulting in negative AISC margins.

- The company's Westwood mine showed improvement in production (albeit still at high costs), and Cote is 92% complete, paving the way to better margins in 2024.

- In this update, we'll dig into the Q3 results, recent developments, and whether the stock is offering enough of a margin of safety at current levels after its recent pullback.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) is finally over, and it was a mixed Q3 overall. This is because while some producers continued their track record of over-delivering on promises like Alamos Gold ( AGI ) and Calibre Mining ( CXBMF ), several others reported disappointing results with razor-thin all-in sustaining cost [AISC] margins. One name in the group of underperformers was Iamgold ( IAG ) with operations in Burkina Faso and Quebec, but the company is unique because it expects to pour its first gold from a top-5 gold mine by scale in Canada next year. In this update we'll dig into the Q3 results, recent developments, and whether the stock is offering enough of a margin of safety at current levels after its recent pullback.

{kind=link}

Q3 Production & Sales

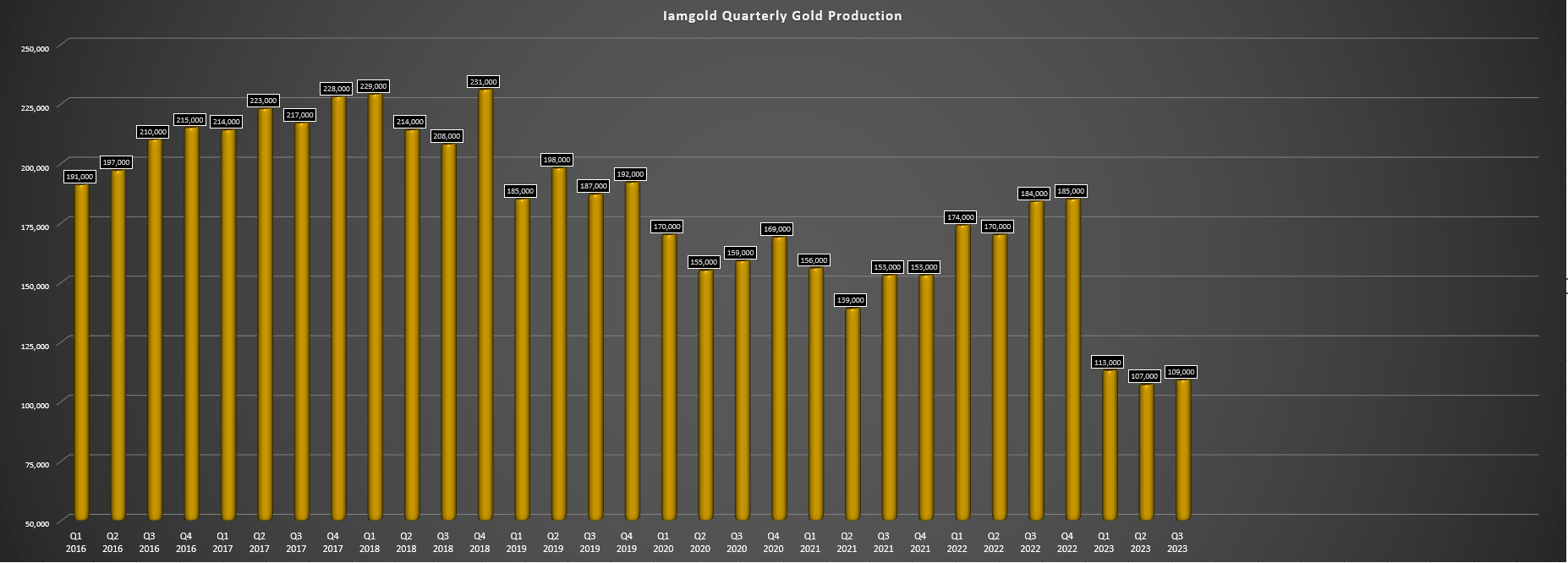

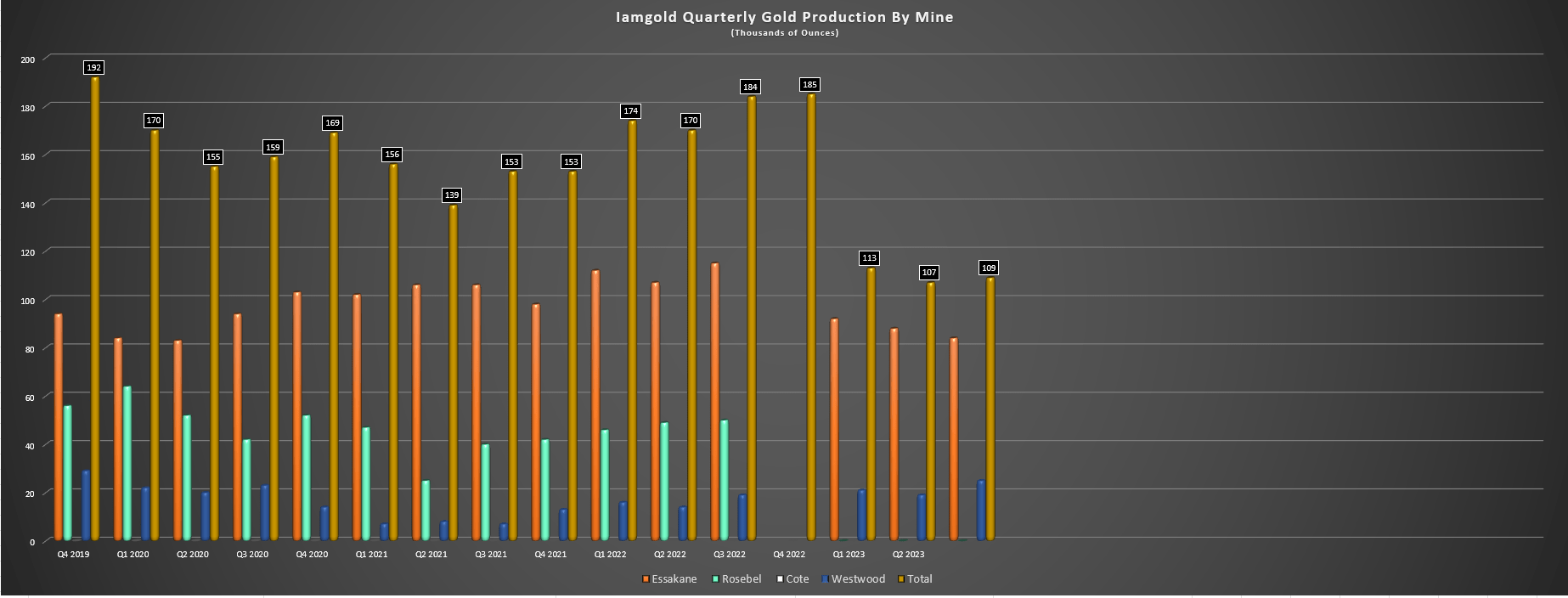

Iamgold released its Q3 results last month, reporting quarterly gold production of ~109,000 ounces, a 40% decline from the year-ago period. The significant decline in production was related to the sale of its Rosebel Mine, which contributed ~49,000 ounces during the year-ago period and lower grades and throughput at its Essakane Mine in Burkina Faso. On a positive note, Westwood made up for some of the shortfalls with higher underground tonnes mined at slightly higher grades as progress on rehabilitation work has continued, allowing for greater operational flexibility. Still, the 6,000-ounce increase in production (25,000 ounces vs. 19,000 ounces) wasn't nearly enough to make up for the ~30,000-ounce decline at its larger Essakane Mine.

Iamgold - Quarterly Gold Production - Company Filings, Author's Chart Iamgold Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

{kind=link}

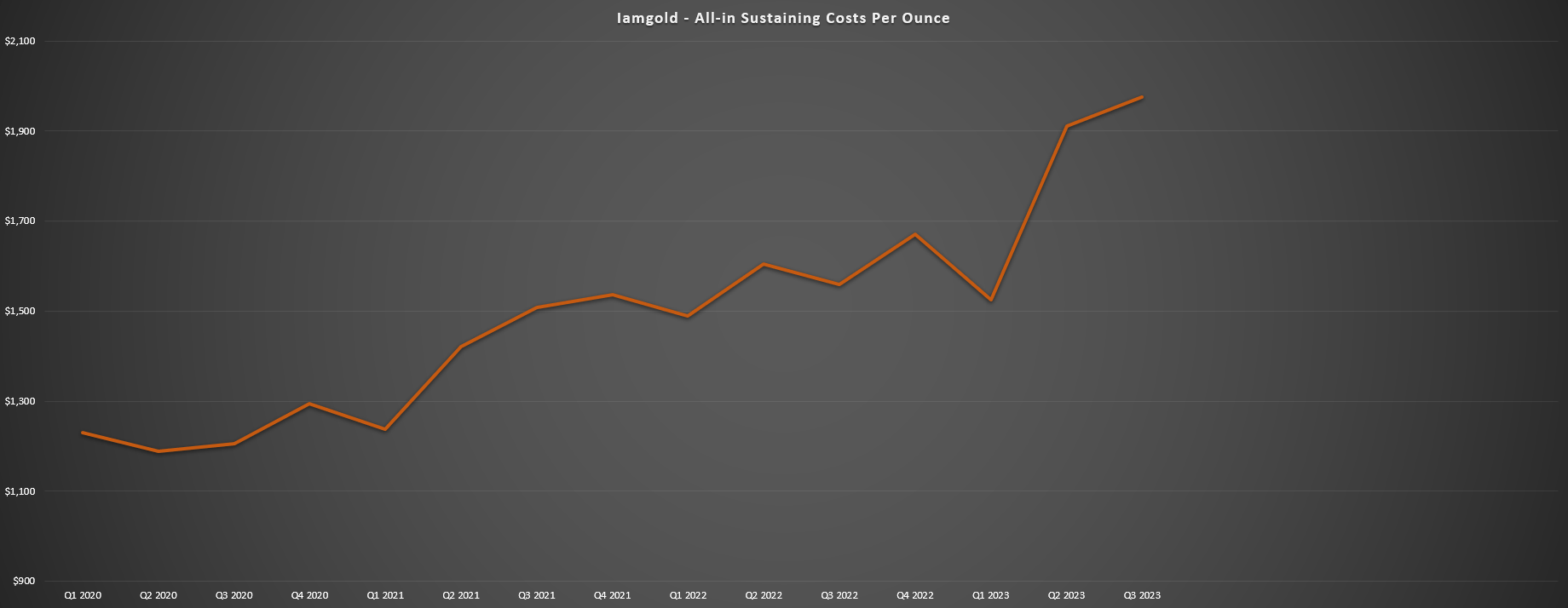

Digging into the results a little closer, Essakane processed ~2.91 million tonnes at an average grade of 1.10 grams per tonne of gold and 90% recovery rates, well below the ~2.98 million tonnes processed at 1.50 grams per tonne of gold in Q3 2022. The lower grades were related to mining in the upper benches of Phase 5 and reliance on low-grade stockpiles, and mining activity in August was impacted by fuel supply disruptions related to geopolitical issues and the worsening security situation. Not surprisingly, the lower gold sales, higher reliance on light fuel oil (more expansive than HFO) and higher landed fuel costs, transportation/camp costs, and labor costs led to much higher operating costs, with AISC coming in at $1,798/oz (Q3 2022: $1,248/oz). This has contributed to FY2023 cost guidance being updated to $1,787/oz vs. $1,662/oz previously.

As for Westwood, production came in 30% higher with similar throughput but at much higher grades (2.94 grams per tonne of gold vs. 2.23 grams per tonne of gold). The higher grades were driven by an increase in underground tonnes mined (~79,000 tonnes vs. ~61,000 ounces) and higher grades from satellite pits, with the benefit of higher grades from the Fayolle Pit that lies 30 kilometers from Westwood and positive grade reconciliation at Grand Duc. That said, costs still came in well above spot levels at $2,138/oz (albeit partially impacted by elevated sustaining capital), which was better than $2,208/oz reported last year but didn't do much for the company from a mine-site free cash flow standpoint even with the stronger gold price.

{kind=link}

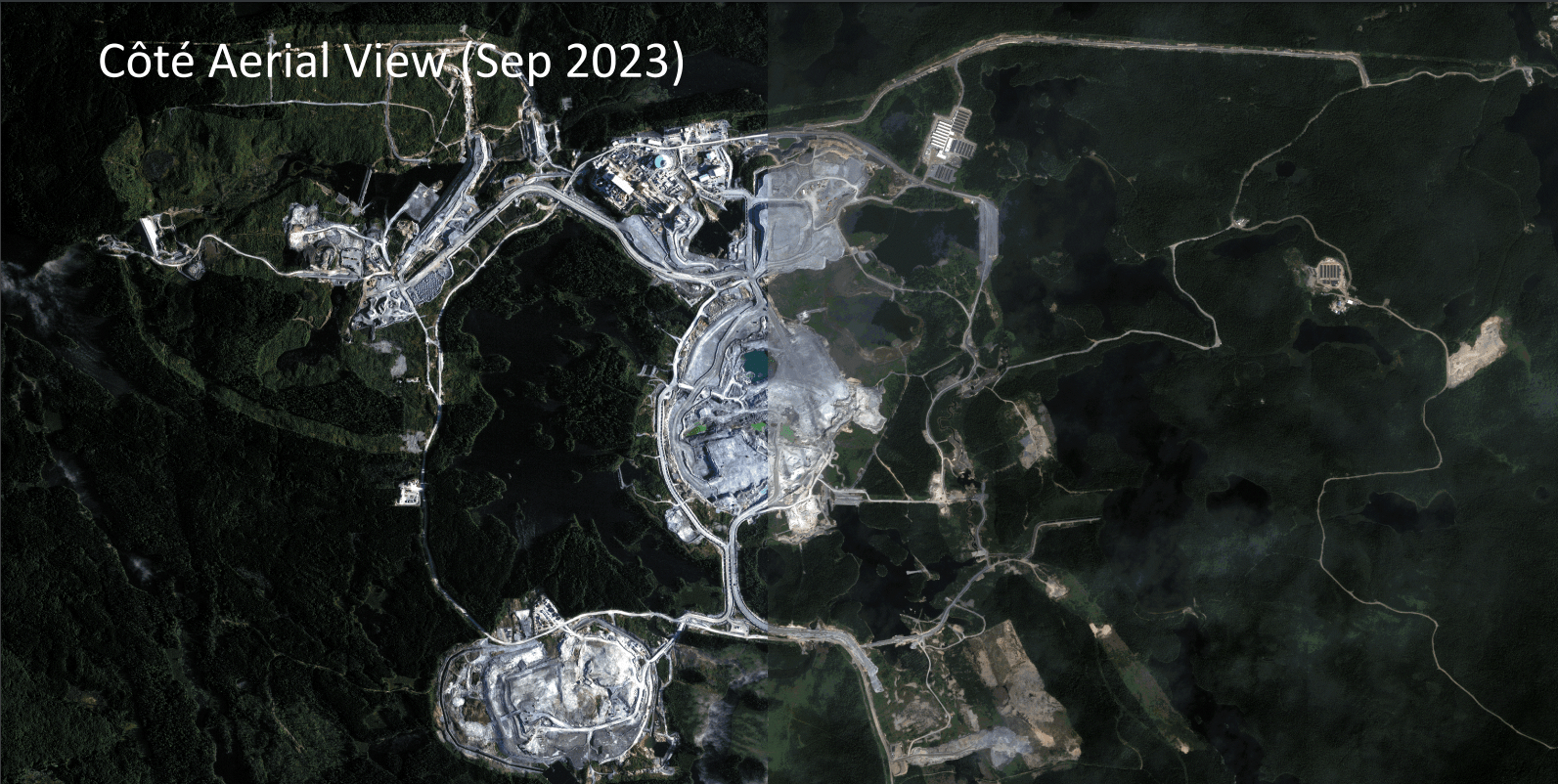

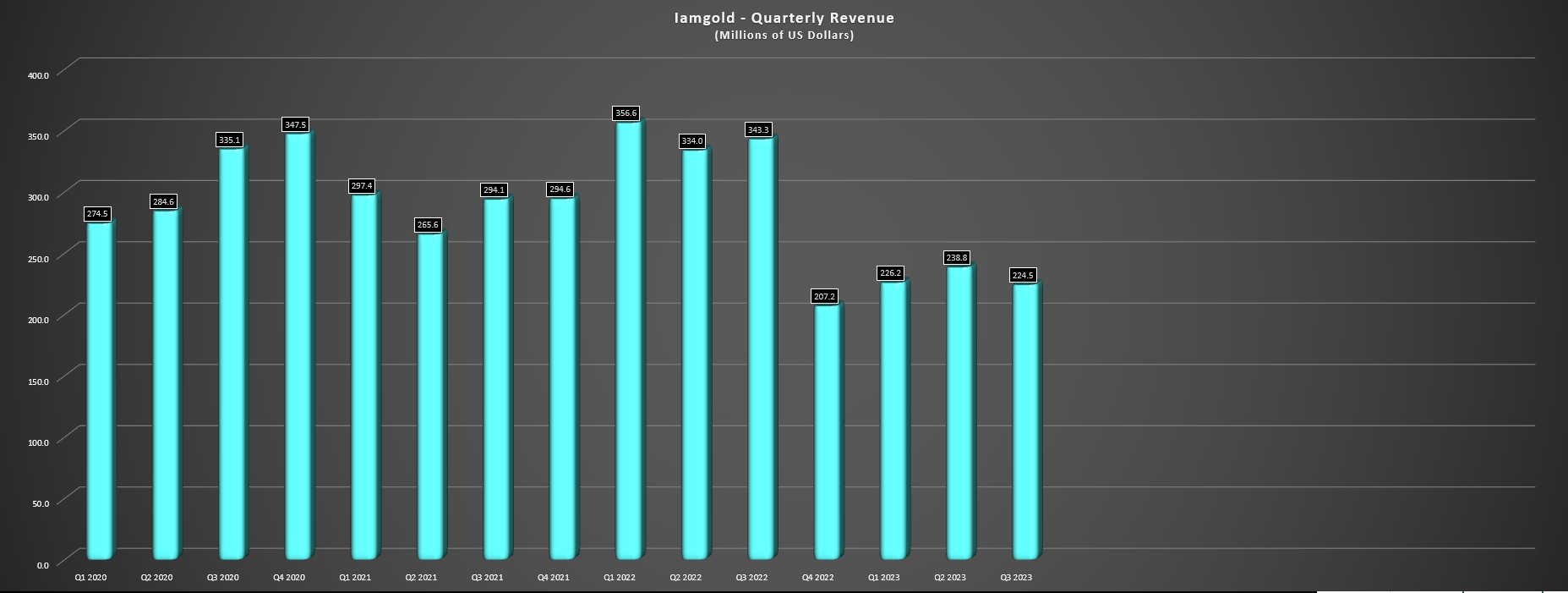

Finally, looking at the financial results, revenue plunged to $224.5 million despite the benefit of a higher average realized gold price ($1,937/oz vs. $1,690/oz), with the culprit being lower sales due to no contribution from Rosebel and lower output from Essakane. Meanwhile, operating cash flow sunk to $37.5 million (Q3 2022: $94.5 million), and mine site free cash flow came in at just $2.1 million, down from $64.9 million in the year-ago period. And after significant capital expenditures on its major growth project in Ontario (Cote Gold, where it has ~55.5% ownership), Iamgold exited the quarter with ~$550 million in cash and ~$480 million in net debt, but with the finish line in sight with ~$2.55 billion of a planned ~$2.97 billion spent at Cote (100% basis) and just ~$420 million remaining.

Costs & Margins

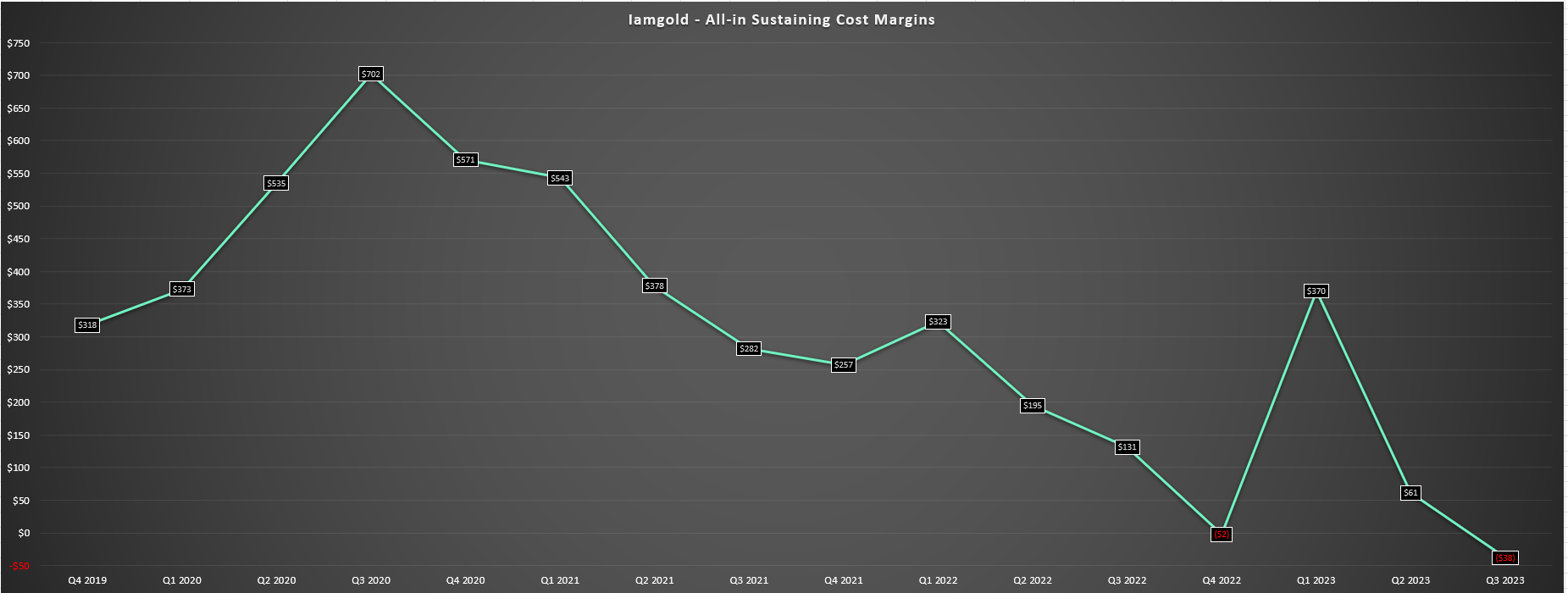

Moving over to costs and margins, the performance has continued to leave a lot to be desired, with company-wide all-in sustaining costs coming in at $1,975/oz, up over 25% year-over-year from already easy comparisons in Q3 2022 ($1,559/oz). The higher costs were related to increased power costs at Essakane and the worsening security situation that has contributed to higher costs plus, higher sustaining capital at Westwood, and fewer ounces sold at Essakane. Unfortunately, the year-to-date results haven't been much better, with AISC of $1,773/oz, which would imply another high-cost quarter in Q4 based on the new guidance range ($1,750/oz to $1,825/oz). The result of these higher costs was that AISC margins fell back into negative territory in Q3 2023, and were down sharply year-over-year despite a $247/oz increase in its average realized gold price.

Iamgold All-in Sustaining Costs - Company Filings, Author's Chart

{kind=link}

{kind=link}

On a positive note, Westwood looks to be turning around and may be able to bring costs below $1,850/oz next year. Meanwhile, Cote is ~92% complete and will be one of the top-5 largest gold mines in Canada by scale over its life of mine (~370,000 ounces) and similar to Agnico Eagle's Meliadine Mine in Nunavut. And with a cost profile of sub $900/oz in its first six years (elevated production years) even factoring in what have been sticky inflationary pressures, this will go a long way to improving Iamgold's AISC margins. That being said, 2024 will be a partial year for production, and it's important to note that after giving away additional ownership to Sumitomo, Iamgold is ~55.5% owner at Iamgold. Hence, although this is a ~480,000 ounce per annum asset from 2025 to 2029, Iamgold's share will be closer to ~265,000 ounces unless it buys back its reduced ownership.

Recent Developments

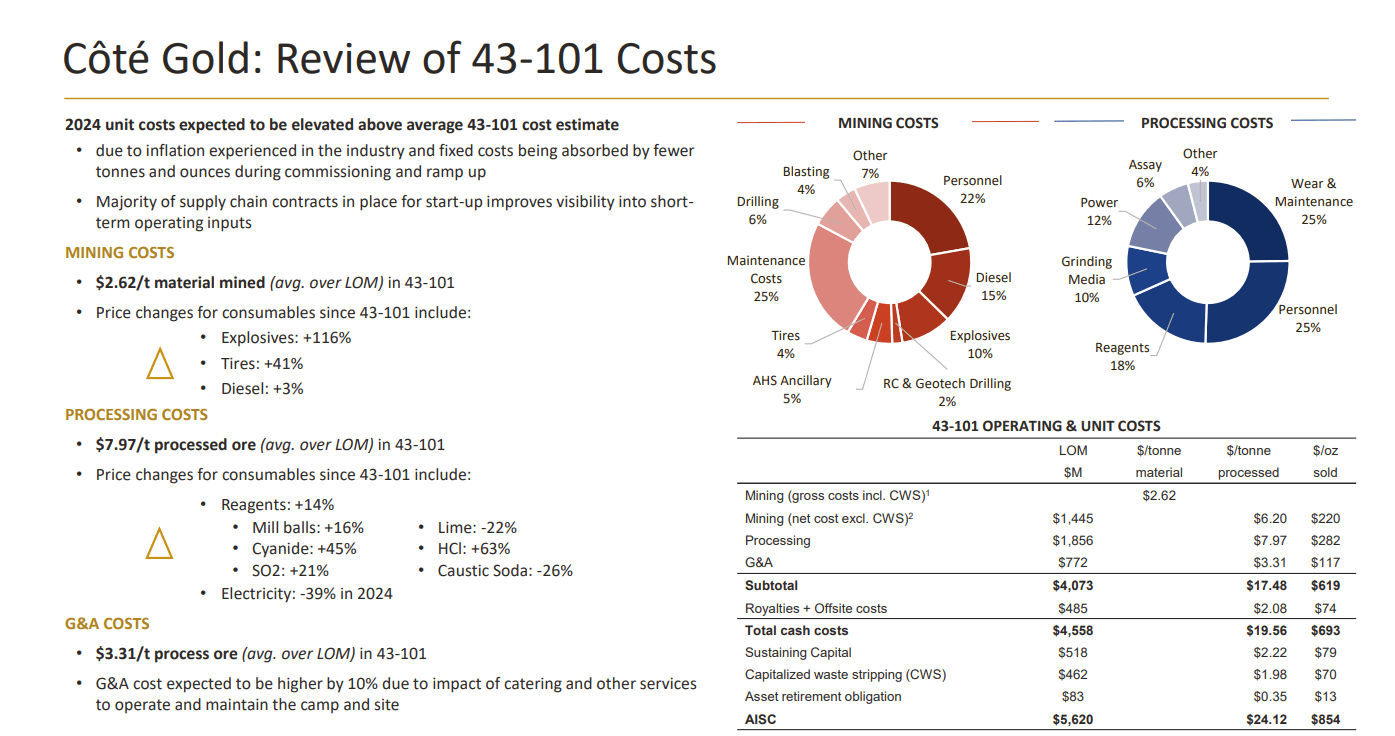

As for recent developments, they have been mixed, but have skewed positive overall. Starting with the negatives, Cote's estimated costs from its 2022 TR appear to be far too ambitious, with the estimate of $2.62/tonne on mining costs likely to be sharply higher with a 100%+ increase in explosives costs, 40% increase in tire costs and an increase in diesel costs since the 2022 TR was completed. Unfortunately, this same trend will apply to G&A costs and processing costs which were previously estimated at $7.97/tonne and $3.31/tonne, with the former impacted by increases in prices for ball mills, reagents, labor, and cyanide, with these making up over 50% of processing costs and offsetting lower electricity and lime prices. Therefore, the life-of-mine AISC of ~$850/oz is not likely to be realized, though this shouldn't be that surprising for those looking at other operations with a larger scale and similar grades like Detour Lake (70,000+ tonnes per day) that are struggling to keep AISC below $800/oz in North America.

{kind=link}

On a positive note, costs may be higher than previous estimates, but this mine has the scale, the technology (autonomous haulage), and the grades to overcome the inflationary pressures. Hence, this is not a case like Pure Gold Mining ( LRTNF ) at Madsen or Great Panther at Tucano where the sector-wide cost increases turned a low-margin operation into an operation that simply couldn't survive. In addition, even at ~$1,000/oz LOM AISC to be more conservative, this is a huge decline relative to the company's current AISC of ~$1,800/oz and will help Iamgold to bring costs back closer to the industry average. However, it's important to note that consolidated costs won't improve immediately, with costs likely to remain above $1,500/oz in FY2024 as the bulk of production still comes from its two current high-cost mines (Essakane/Westwood).

The final negative worth discussing is that the situation hasn't improved much at Essakane and we've seen a new royalty rate introduced to add insult to injury. As noted in its prepared remarks, royalties have increased to 6.5% (5.0% previously) on gold sold at prices between $1,700/oz to $2,000/oz and 7% (previously 5.0%) on gold sales above $2,000/oz. Meanwhile, Iamgold noted that terrorist related incidents continue to occur in country and in "the immediate region of the Essakane Mine" , which is creating a difficult situation from a supply chain standpoint and overall cost standpoint to get consumables and labor to site, and it and impacted fuel supply in Q3. In order to help reduce these issues, the company plans to expand its fuel storage capacity on site, with higher usage of HFO impacting Q3 costs. While this is disappointing, Essakane is not the future of the company and is a shorter-life asset, so while the outlook is not great (higher costs at lower production levels), it isn't like this is the future flagship operation.

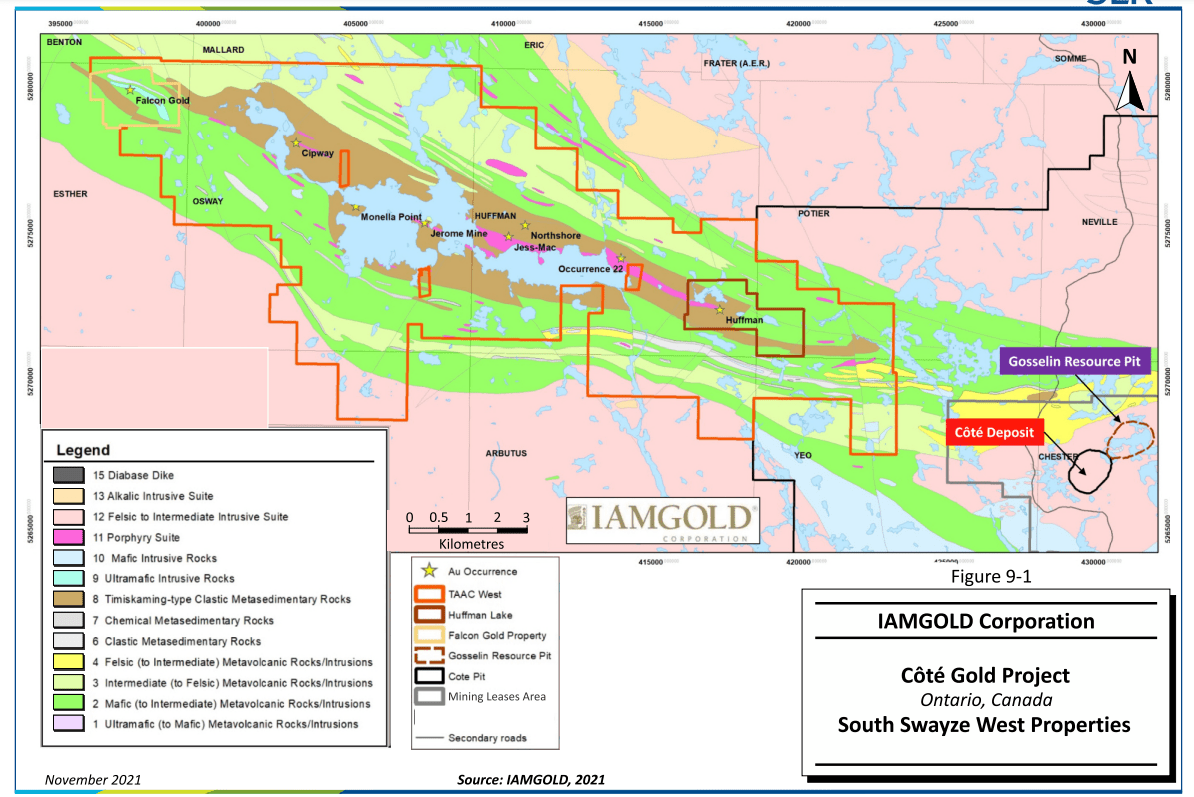

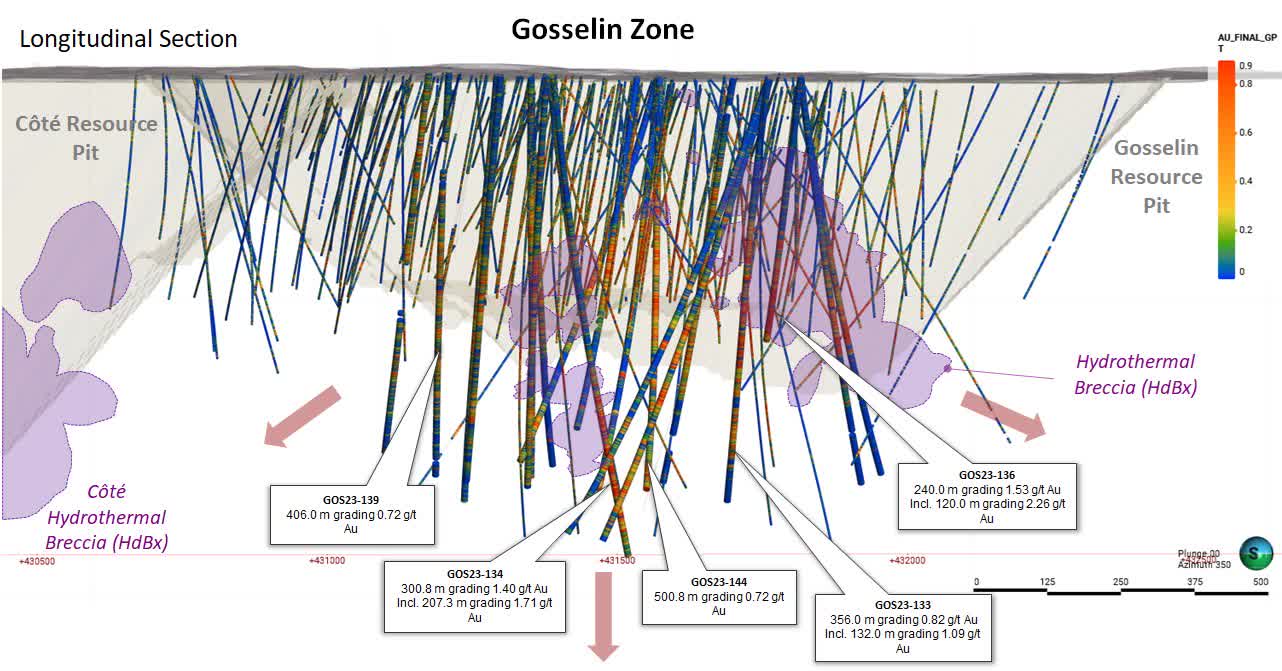

As for the positive, the company continues to report monster intercepts from Gosselin, which lies under a lake to the northeast of the massive Cote deposit (shown below). Iamgold noted that Gosselin is now "approaching similar dimensions" to the neighboring Cote deposit, suggesting that the total resource at Cote Gold could increase to over 20.0 million ounces. Therefore, the long-term outlook here is certainly positive (assuming necessary permits are received), with the potential to smooth out the production profile in later years (albeit with lower grades, but higher than stockpile grades) and extend the mine life at this massive Ontario mine.

{kind=link}

{kind=link}

Finally, Iamgold noted that its goal is to become an intermediate gold producer with a strong operating base in Canada and this was confirmed with its recent proposed acquisition of the remainder of the Nelligan Project near Chibougamaou in Quebec where there's a current 5.0+ million ounce resource base. Overall, I see this as a smart move to improve its pipeline after chopping it down with the sale of Rosebel and its Senegal assets, and like Kinross ( KGC ), a move to a primarily Americas-focused producer should help its multiples to increase longer term.

In the longer term, our goal remains that we want to become a low-cost, high-margin intermediate gold producer with a strong operating base in Canada. Financially, we will prioritize returning our 70% position in Cote with our partner, Sumitomo, as well as use our cash flows to optimize our balance sheet."

- Iamgold, Q3 2023 Conference Call

Valuation

Based on ~488 million fully diluted shares and a share price of US$2.30, Iamgold trades at a market cap of ~$1.12 billion and an enterprise value of ~$1.57 billion (included deferred consideration paid for Senegal assets after quarter-end). This leaves the stock trading at less than 0.75x P/NAV vs. an estimated net asset value of ~$1.55 billion, a reasonable valuation for a company set to bring a massive Tier-1 jurisdiction mine online in Q1 of next year. Meanwhile, Iamgold trades at one of the lower cash flow multiples in its peer group, hovering near 3.3x vs. cash flow per share estimates of $0.76. The low multiple can be partially attributed to its relatively high net debt vs. peers and its poor track record of production per share growth, plus its exposure to Burkina Faso which has lost investment attractiveness points with a worsening security situation and the recent increase in royalties.

{kind=link}

Using what I believe to be fair multiples of 0.95x P/NAV and 5.5x cash flow and a 65% weighting to P/NAV vs. P/CF, I see a fair value for Iamgold of US$3.40. This points to a 47% upside from current levels and a decent upside for this turnaround story, especially given that fair value would jump closer to US$3.55 if the gold price can average at least $2,000/oz next year. That said, I am looking for a minimum 40% discount to fair value to justify starting new positions, and this translates to an ideal buy zone of US$2.04 or lower. So, although Iamgold is getting closer to its buy zone and is finally nearing the finish line at Cote Gold, I continue to see more attractive bets elsewhere in the sector.

As for more interesting opportunities, Argonaut Gold ( ARNGF ) stands out among its peers. Not only is the stock the most hated that it's been arguably since its inception, but it's trading at ~1.4x FY2024 P/CF, ~0.40x P/NAV, and closer to ~0.30x P/NAV if the company can execute successfully on its Magino Expansion to push production rates to 17,500 to 20,000 tonnes per day post-2025. In fact, the current enterprise value of ~$440 million represents just a fraction of the Magino Expansion case NPV (5%) of ~$1.33 billion at 17,500 tonnes per day (low end of planned expansion), and this excludes its four other mines (three held for sale in Mexico, one in Nevada). Hence, with one of the cheapest multiples sector-wide and the stock hated, I see this as one of the more compelling reward/risk bets in the sector currently.

Summary

Iamgold had a tough Q3 and was one of the few companies to report negative AISC margins with all-in sustaining costs coming in just shy of $2,000/oz. Fortunately, Westwood should see better cost performance with more production stopes available, Cote is barely four months away from its first gold pour, and the company is set to see a meaningful decline in company-wide costs next year. However, I would still expect AISC to come in above $1,500/oz next year with a lengthy ramp-up to commercial production and with over 70% of ounces still coming from its high-cost mines. In addition, while FY2024 will be a better year, the real turnaround (~270,000 attributable ounces from Cote) won't arrive until 2025. In summary, while I see IAG as reasonably valued and a decent turnaround story, I would need a deeper pullback to get more interested in the stock.

For further details see:

Iamgold: Turnaround Thesis Remains Intact