CSIQ - Iberdrola: A Utility Giant With A Head Start In Renewables

Summary

- Iberdrola, S.A. is a utility giant and a leader in green energy production.

- The company expects to grow earnings by 10% per year as it capitalizes on the transition to sustainable energy production pushed by government around the world.

- Let me show you why Iberdrola, S.A. is a substantial part of my portfolio and why you should consider buying it, too.

Dear readers/followers,

In my recent article on Canadian Solar Inc. (CSIQ), I outlined the reasons why I like to have some exposure to renewable energy in my portfolio. Today I want to cover a renewable energy giant - Iberdrola, S.A. ( IBDRY ) and show you why I think it makes a good investment.

Note: The native shares of Iberdrola denominated in EUR trade on the Madrid exchange under the ticker IBE. As a European, these are the shares I prefer. For American investors, there is also an ADR denominated in USD.

Overview

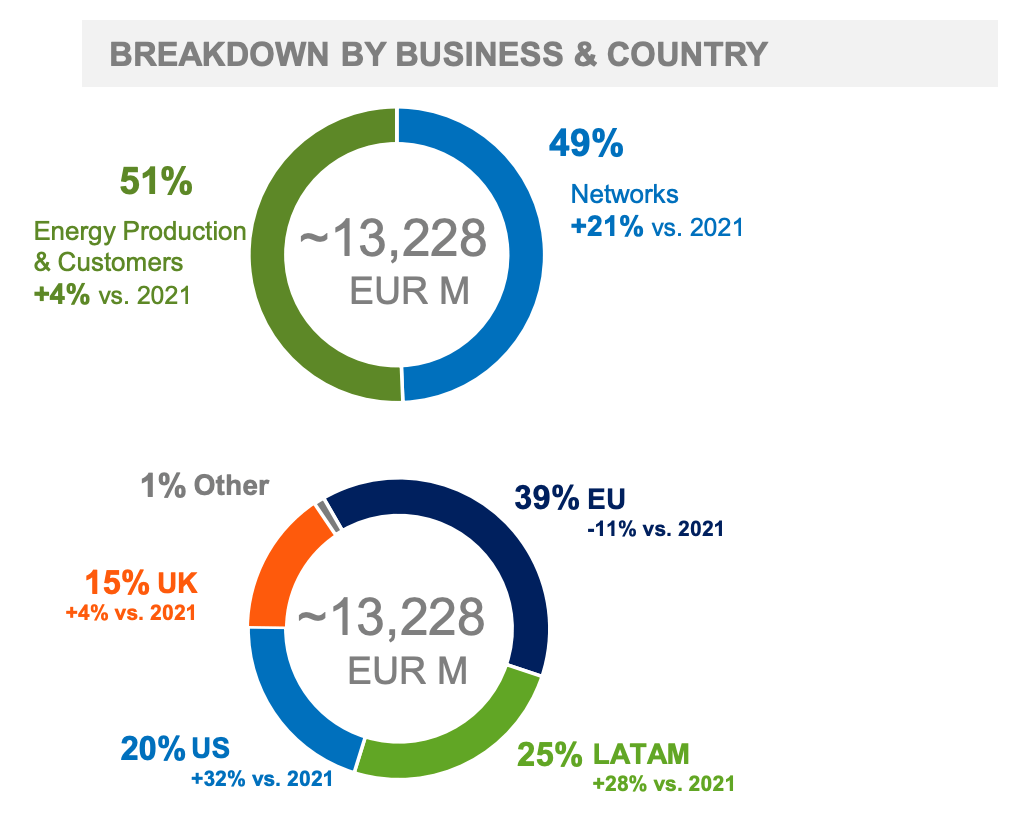

Iberdrola, S.A. is a Spanish-based utility company with global operations. It is one the largest and greenest fully-integrated electric utility companies in the world, with revenues of over EUR50 Billion and EUR13 Billion in EBITDA. The company operates in two primary segments - energy production and networks with revenues split equally between the two segments. In terms of geographical presence, the company is heavily present in Spain, Brazil, the UK, the USA, and Mexico, with the majority of revenue coming from their native Spanish market.

Iberdrola Investor Presentation

{kind=link}

In terms of energy production, I want to point that Iberdrola is very clean and a leader in renewables. They abandoned coal a few years ago, and the majority of their production comes from renewables (60%), followed by nuclear (20%) and natural gas (20%). Notably, the company is the second-largest producer of wind energy globally (after Danish Orsted), so it comes as no surprise that the majority of their installed capacity in renewables comes from onshore wind (51%), followed by Hydro at 24%.

The company is well-diversified, which allows it to balance volatile renewables with more stable traditional revenue streams such as nuclear and distribution networks. It also makes the company extremely well-positioned for the renewable future. Iberdrola is several years ahead of its peers in the transition to renewables, as 80% of their production already comes from zero emission sources with zero exposure to coal .

Iberdrola Investor Presentation

{kind=link}

The company's CAPEX plan is massive, as they continue to expand their renewables and networks. In 2022 alone, the company invested EUR 10.7 Billion (up 13% YoY) primarily into EU renewables and U.S. and Brazil Networks. The company also has 7.6 MW of renewables under construction, with expected delivery between 2023 and 2026. The majority (47%) of this new capacity will come from on-shore wind strengthening their almost unrivalled presence in the sector.

Financials

Iberdrola, S.A. reported their 2022 results in February. In short, the results slightly beat expectations and there were no real surprises. EBITDA (which is the key metric for the company) increased by 10% YoY to EUR13.2 Billion driven primarily by a positive performance in the networks segment in Brazil (due higher tariffs) and the U.S. (due to higher tariffs and a positive one-off in New York ). The New York one-off accounted for about 40% of the year-on-year growth in EBITDA, so even without it the growth was solid.

For 2023, management guides towards an 8-10% increase in earnings. Iberdrola, S.A. expects that the increase will be driven by a production increase in hydro and wind and new investments of over EUR10 Billion which will more than offset the increase in financial costs and the effect of a newly introduced revenue tax in Spain (1.2% of revenue in Spain). Looking beyond this year, the renewable space will likely continue to grow, as most governments in the West are pushing for sustainable energy production by introducing various new laws and regulations. The energy crisis in Europe will only speed up the transition.

Iberdrola Investor Presentation

{kind=link}

Regarding financing, the overall weighted average interest rate on their debt increased by 67 bps to 4.27% in 2022. This is not surprising given that rates are increasing worldwide. The increase for Iberdrola was primarily fueled by Brazilian rates on their BRL denominated loans. If we exclude Brazil, their cost of debt is only 10bps higher, despite an increase of over 150bps in reference rates.

Iberdrola Investor Presentation

{kind=link}

Debt on their balance sheet is BBB+ rated and spread over time, and their liquidity of EUR24 Billion, of which EUR6 Billion is in cash, is enough to cover over two years of financing needs. The majority of their debt is denominated in EUR (40%), followed by USD (27%), GBP (15%) and BRL (13%). The company's Adj. net debt/EBITDA is 3.3X.

Iberdrola Investor Presentation

{kind=link}

The company has set a dividend floor similar to that of its peers, as described in their 2022 annual report:

In the 2020-2025 Plan, Iberdrola established a minimum shareholder remuneration of EUR 0.40 per share for the years 2020-2022. In this regard, at the end of January 2023, Iberdrola paid a retribution for the 2022 financial year amounting to EUR 0.18 gross per share (+5.9% vs 2021). The support that Iberdrola shareholders continue to show to the Group's management is noteworthy, since almost 80% of them chose to receive the dividend in shares. In light of the results posted, at the next General Shareholders' Meeting, Iberdrola will propose a supplementary remuneration of EUR 0.31 gross per share, which will result in a total shareholder remuneration amounting to EUR 0.49 gross per share, against 2022 earnings, provided it is approved in the General Shareholders' Meeting.

At EUR 0.49 per share, the dividend yield stands at 4.6%, which is quite high considering the quality of the company and also the fact that the dividend is likely to grow by a high single-digit percentage over the next few years if management delivers on their guidance.

Valuation

Assuming a 2023 EPS of EUR 0.715 (up 10% from EUR 0.652 in 2022), Iberdrola is currently trading at a forward P/E of 15.8x, which is in line with its long-term historical average. The 15x P/E ratio is also what most analysts are using to value this company, and I think it's spot on.

On a P/BV basis, the company is currently trading at 1.70x and below Enel at 1.89x. Wolf report argues for a 2x price-to-book in his article. I think that's reasonable given the outlook and quality of Iberdrola's assets, and I certainly think that Iberdrola deserves at least the same (if not higher) multiple than Enel simply because it has a head-start of at least a few years in renewables.

Based on this, Iberdrola seems fairly valued at the current price of EUR 10.70 per share, and if management delivers on their guidance, the stock could reach a PT of EUR 12.70 by 2025.

With that said, let's have a look at what we can reasonably expect from the company going forward:

- 4.6% dividend yield (growing at 6-8% per year)

- 8-10% EPS growth for the next two to three years

- 0% annual return from multiple expansion as the company is fairly valued

- -> total return of 13.6% per year.

Remember how I generate alpha:

- Start with a thesis why a given industry/sector should outperform

- stay overweight in those sectors for as long as the thesis is valid

- look for companies with sound fundamentals that are either undervalued or fairly valued with exceptional growth prospects

- if a company becomes overvalued, trim the position and rotate into another stock/sector that is still undervalued

- if a company becomes increasingly undervalued and the thesis is still valid, add to the position

- generate alpha and repeat.

My total return then comes from the dividend yield, EPS growth and multiple expansion as the valuation normalizes over time. I always target a total return in excess of market returns (>8%) to generate alpha.

What things do I look for when selecting individual stocks to buy?

- strong and safe fundamentals

- good management teams with a track-record of caring about shareholders

- healthy EPS growth

- well-covered dividend

- discount relative to peers and/or historical fair multiples

- other catalysts.

Takeaway

Iberdrola, S.A. is very well-positioned to capitalize on the future of renewable energy. It is one of the largest and the greenest utility companies in the world, making Iberdrola, S.A. a very safe play for investors. This stock will not 10x your money, but it will pay you a 4.6% dividend that is essentially guaranteed and could return another 8-10% in price appreciation as the company grows their bottom line. I rate Iberdrola, S.A. as a " BUY " here at EUR 10.70 per share, and will continue to add to my existing position on any major dip. I think Iberdrola, S.A. is a great and safe company to buy and hold for 5-10% years as the world transitions to renewable energy.

For further details see:

Iberdrola: A Utility Giant With A Head Start In Renewables