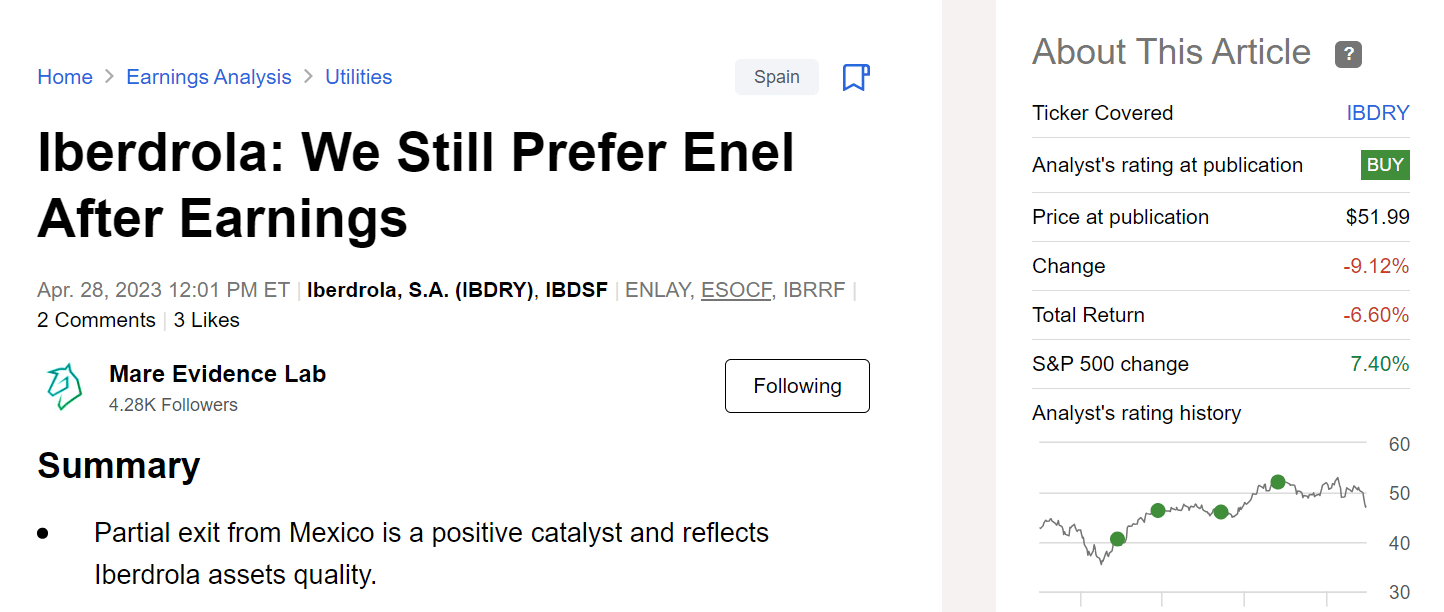

IBDSF - Iberdrola: Guidance Raised Again; Time To Re-Enter

2023-08-10 06:05:23 ET

Summary

- Iberdrola's Q2 financial results beat expectations, with a 21% increase in net income.

- The company (once again) raised its Fiscal Year 2023 guidance and is on track to achieve the strategic plan targets.

- Ongoing debt development with lower earnings volatility due to disinvestments is a plus to consider.

- Iberdrola offers upside potential in renewable energy expansion and downside protection on grid earnings. Our buy rating is then confirmed.

Our most devoted readers know we preferred Enel After Q1 Earnings vs. Iberdrola (IBDSF) (IBDRY). This was mainly due to a valuation discrepancy, and despite that, we had maintained a buy rating target on the Spanish integrated energy player. In our analysis, after comparing asset quality, we recognized that the differences between the Italian energy giant and Spain's Iberdrola were insignificant enough to account for a 60% valuation gap. Looking at the European utilities, we favor portfolios with capital-intensive renewable, onshore/solar assets and networks with high inflation protection, low regulatory risk, and long-term concessions. Although some differences highlight the superior quality of Iberdrola's acquisitions, these cannot justify the significant valuation discrepancy. Since our last update, we are not surprised to see Iberdrola's stock price, which declined by 10%, while Enel is up by 13%.

{kind=link}

Iberdrola: Mare Past Analysis

{kind=link}

Enel: Mare Past Analysis

Q2 results analysis

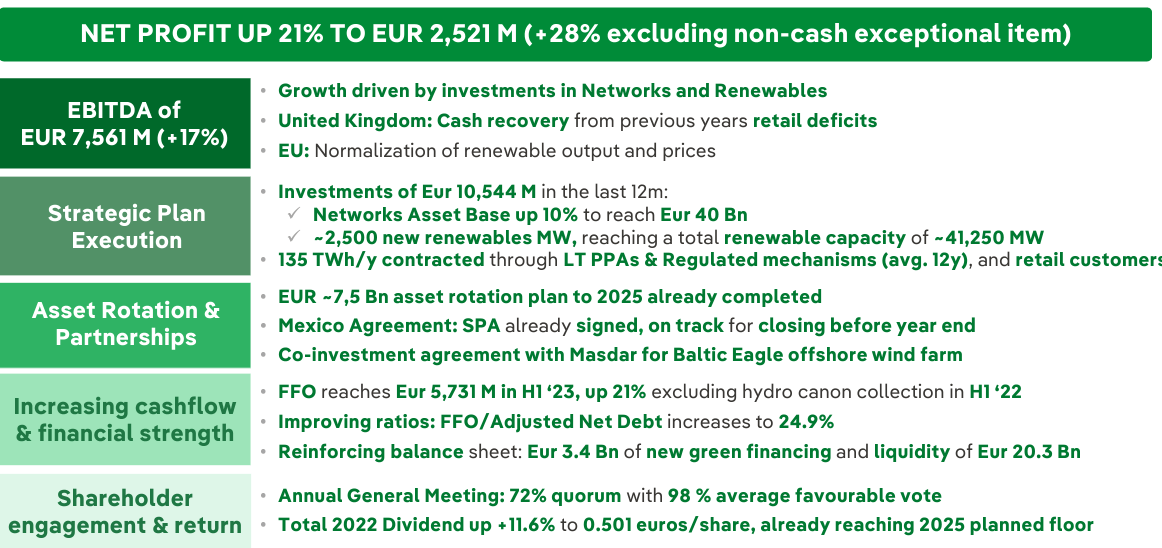

Even though Enel and Iberdrola stock prices diverged over the period, Iberdrola Q2 financial figures were broad-based beats. We are impressed by the H1 financial results, and the company raised (once again) its Fiscal Year 2023 guidance and is well on track to achieve 2025 financial targets. Iberdrola reported a stronger-than-expected Q2 number growth with a 21% positive net income trajectory (excluding one-off capital gain). After listening to the Q2 Q&A analyst call, management expects additional upside in H2. As already mentioned, this guidance upgrade has already happened twice this year. Iberdrola is now expecting a net income of high single-digit growth from low-mid single-digit growth. Before commenting on the Q2 results, Iberdrola 2025 strategic plan presented in November last year is ahead of schedule. In detail, 100% of the company's asset rotation is already completed, the 2025 dividend per share floor has already been achieved, and 100% of grid investment CAPEX is secured with approximately 70% of capacity under construction. Here at the Lab, Iberdrola might present a new plan with higher targets over the next five-year time horizon.

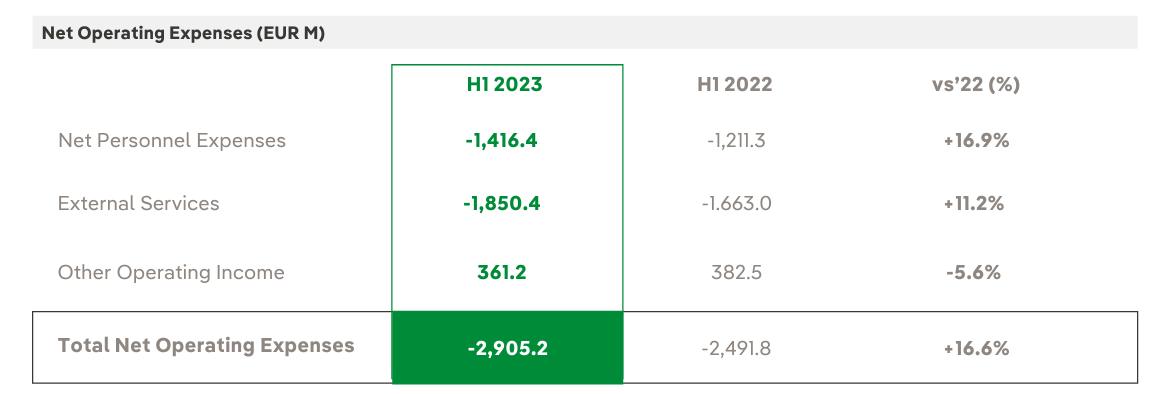

Starting with net income growth, Iberdrola achieved a plus 21% compared to last year's results. This positive outcome was recorded thanks to a hydro normalization in Spain and a margin recovery in the UK region. EBITDA grew to 7.5 billion, a plus of 17.3% compared to last year. The margin recovery (Fig 1) was supported by lower growth in operating expenses (Fig 3).

Iberdrola EBIT development (Source: Iberdrola Q2 results presentation -)

Fig 1

{kind=link}

Iberdrola lower op. expenses

Fig 2

Mare upside

- Iberdrola raised its H2 target thanks to the new grid rate in the US and Brazil. In addition, the company plans to install new renewable energy capacity and increase the renewable load factors;

- The company is now forecasting an important net debt reduction from disposals. Our guidance also incorporates a €200 million tax on revenues in Spain. This is due to the extra-profit tax related to higher energy prices. However, our numbers do not take into account any potential extraordinary positive results;

- Iberdrola has set a very attractive 2023 asset rotation. There is an expectation of >€6 billion to cash in by year-end. This is supported by the sale of 49% of Baltic Eagle announced in July. This offshore project was sold to Masdar at an implicit value of approximately €1.6 billion. In Q1, we already commented on the 2023 Mexican sale. This deal is expected to close by year-end with a significant capital gain;

- Iberdrola expects a favorable NM Supreme Court hearing in September related to the extra-profit tax;

- We are now forecasting (in line with the company's indication) a net debt of €42 billion by year-end. This significantly improved over the previous guidance set at €50 billion. And it is also in line with our supportive buy rating target of Enel. This is achieved with disposals and co-investments and already considers a CAPEX acceleration in H2. In total, here at the lab, we forecast a CAPEX of €11.5 billion in 2023;

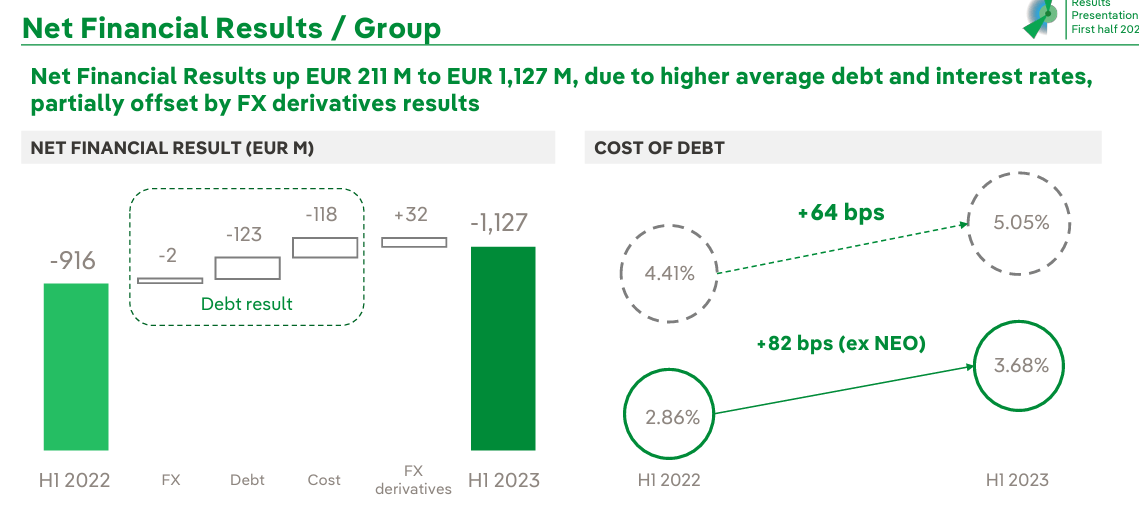

- In H1, the company increased its interest expenses, and now Iberdrola's cost of debt increased by 5.05%. As a reminder, 75% of the total company's financial obligation is 75% fixed (Fig 2);

- Our numbers do not incorporate an upside on the new Noor Midelt II power plant construction. Morocco's energy plans may prove to be a unique opportunity for Iberdrola. The group was pre-qualified in the tender offer for a 400 MW complex with a solar power plant and an ancillary energy store.

{kind=link}

Iberdrola Q2 Financials in a Snap

Fig 3

{kind=link}

Iberdrola net interest rate evolution

Fig 4

Conclusion and valuation

Here at the Lab, renewable energy sources can guarantee an average annual EBITDA growth rate of 15%-20% over the next ten years. The company's internal forecast supports this. Indeed, in the 2020-2025 time horizon, the company " will invest €75 billion to continue leading the energy transition and develop its growth strategy in countries with a solid credit rating and climate ambition; maximize operational efficiency and drive innovation in all its activities. " And this is also based on the Biden administration's IRA envisages $369 billion in subsidies for producing solar panels, wind turbines, batteries, and hydrogen technologies to reduce CO2 emissions by 40% by 2030. With the Inflation Reduction Act, Biden wants to anchor the US economic recovery despite inflation that remains high and a FED that is continuing to raise rates. Iberdrola has 20% exposure of its EBITDA to the US and will benefit from the ongoing energy revolution. The European Union is responding to the USA's IRA with the Green Deal Industrial Plan. This framework will likely foster the EU's energy transition, and combined with the REPowerEU Plan, and the EU will move away from fossil fuels. Here at the Lab, we believe that the US and EU political developments are favoring a multiple expansion scenario. In addition, many EU countries already set critical financial resources to support the energy revolution.

{kind=link}

Iberdrola offers an upside related to renewable energy expansion and downside protection on the grid earnings. We decided to maintain an unchanged multiple of 15x on the P/E level. After the Q2 results, our rolling forward 2024 EPS stands at €0.86, and we derive a valuation of €13 per share ($55.4 in ADR), confirming a long-standing buy. We are impressed by Iberdrola disposal's run rate, lower debt development, and its 2025 targets already achieved. Downside risks already include changes in remuneration on regulated utilities, fluctuation in commodities prices, higher interest rates, and volatility in exchange rates (USA, UK, and Latam derive 61% of the total Iberdrola's EBITDA).

For further details see:

Iberdrola: Guidance Raised, Again; Time To Re-Enter