IBDSF - Iberdrola: Supportive Q4 Reiterating Buy

Summary

- The Spanish energy conglomerate delivered a strong set of numbers.

- Cross-checking its CMD and despite an unfavorable energy situation, Iberdrola is delivering on its promises.

- DPS up versus consensus, financial targets in line, and solid balance sheet with an FFO/Net debt at 25.4%. Our buy is confirmed.

After having checked Enagás latest quarter , today Iberdrola ( IBDSF ) ( IBDRY ) just released its accounts. Here at the Lab, our internal team sees the 2022-25 strategic plan as credible, and the 2022 adverse political measures are now well priced in. Q4 was a positive confirmation of our analysis called 'Looking Forward To Iberdrola Capital Market Day'. We see the Spanish energy conglomerate as one of the more defensive global utility players with limited EU energy crisis exposure and a track record of successful investments in renewable energy infrastructures and networks far away from fossil fuel exposure that characterized Iberdrola in the past decade. As a reminder, our investment thesis was supported by 1) GEO diversification with new investments in developed countries rather than emerging markets, 2) the REPowerEU act upside, 3) an existing liquidation value of Iberdrola's portfolio across the globe, 4) immaterial exposure to Russian gas, 5) EBIT margin protection from inflation and 6) its total fixed rate debt. You can also check our previous publication on the company's performance in Q1 , Q2, and Q3 .

Why are we still confident?

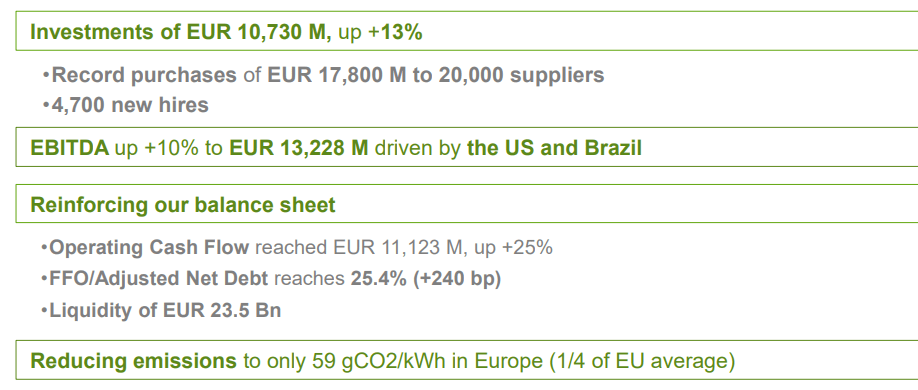

- Iberdrola's EBITDA increased by 10% to €13.2 billion thanks to the positive performances recorded in Brazil and the US that partially offset the slowdown in Mexico and Spain. Cross-checking Wall Street analyst assumption, 2022 accounts were slightly ahead, in detail, according to Reuters, EBITDA was forecasted at €13 billion (Fig 1);

- The Spanish player is continuing to invest in A-rated countries. Despite supply chain constraints, CAPEX investments reached €10.73 billion (in line with management indications);

- Key to note is the bad provision evolution which increased in abs value from -€369 million to -€470 million; however, compared to the 2021 numbers, there was a 3.1% decrease as % of turnover (Fig 3);

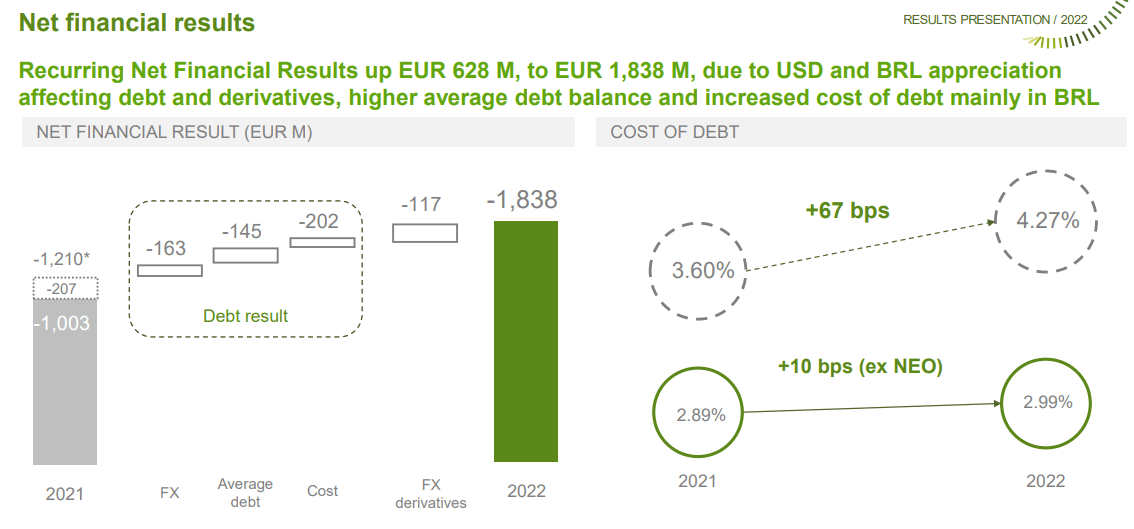

- Looking at the interest costs, at first sight, we note an increase of 67 basis points (to 4.27% from 3.60% ); however, if we exclude Brazil's development, interest expenses development just increased only by 10 basis points ( to 2.99% from 2.89%) (Fig 2);

- The above points support Iberdrola's operating leverage. Thus, net income reached 4.33 billion (again up by 12% vs 2021 end). The consensus was forecasting a profit of €4.09 billion (again another bear from the Spanish integrated player) (Fig 1);

- Again another support to our buy thesis came from the latest numbers on Iberdrola's debt. In 2022, the Group's balance sheet gained strength thanks to a plus 25% increase in operating cash flow. In addition, the company has a supportive liquid position at more than €25 billion (with more than €5.5 in cash & equivalents - Fig 4).

Iberdrola financials in a Snap

{kind=link}

Source: Iberdrola Q4 and FY results presentation (Fig 1)

Iberdrola int. exp. development

{kind=link}

(Fig 2)

Iberdrola bad provision evolution

(Fig 3)

Iberdrola cash liquidity

(Fig 4)

Conclusion and Valuation

So, the bottom line results were marginally ahead of consensus and in line with our supportive estimates. Iberdrola's balance sheet appears strong and the total dividend payment for 2022 was set at €0.49 per share (consensus was estimating €0.48 per share - Fig 5). What is key to emphasize is once again Iberdrola's debt obligation, in detail, adjusted net debt (including the hybrid bond) stood at €43.7 billion and is consistent with Iberdrola's Q3 financial guidance. The key Wall Street financial ratio is the FFO/Net debt which reached 25.4% and was well ahead of the 22.3% average forecast. Continuing to value Iberdrola with a 15x Price/Earnings ratio , we derive a target price of €13 per share with a dividend yield of 5.0% ($55.4 in ADR). In our best-case scenario, including Avangrid (profits were up by 25%) and Inflation Reduction Act development and also considering Iberdrola renewable pipeline, we see an upside of up to €17.5/share for Iberdrola ($70 in ADR).

For further details see:

Iberdrola: Supportive Q4, Reiterating Buy