ESOCF - Iberdrola: We Still Prefer Enel After Earnings

2023-04-28 12:01:21 ET

Summary

- Partial exit from Mexico is a positive catalyst and reflects Iberdrola assets quality.

- Iberdrola delivered a solid set of numbers with an EBITDA growth of almost 40%.

- We are reiterating our buy; however, Enel is trading at a lower P/E and a higher dividend yield.

Before commenting on Iberdrola's (IBDSF) (IBDRY) results, we would like to follow up an analysis started one year ago called ' We Still Prefer Enel '. In short, after having compared their respective asset quality, we believe that the differences between the Italian energy giant and the Spanish Iberdrola are not significant enough to account for the large valuation discrepancy which is currently existing between the two companies. In the context of rising rates and higher renewable investment demand, we prefer simplified strategies that focus on improving accounts and strengthening balance sheet numbers.

Comparing Southern European utilities, we favor portfolios with capital-intensive renewable assets as well as networks with high inflation protection, low regulatory risk, and long-term concessions. Although some differences highlight Iberdrola's assets' superior quality, these cannot justify the significant valuation difference with the Spanish company which trades at a premium P/E of 60% compared to Enel. Going deeper into the analysis, retail sales should guarantee robust profits thanks to commodity price drops and a more stable contracts presence. This should lead to an attractive free cash flow, especially for Enel (ENLAY). Enel's industrial plan, under the direction of the new CEO Flavio Cattaneo , will be in continuity with the previous one, in particular on the debt reduction target at €21 billion. At year's end, the continuous demand for renewable energies and investments in networks led to an estimated net debt/EBITDA ratio exceeding 3.5x for Iberdrola, while Enel's ratio is falling below 2.5 times.

This will improve Enel's balance sheet and will make its dividend payments more sustainable in our view. Therefore, Enel at a 7% yield is very much attractive, while Iberdrola's dividend at <4% is not so compelling. To our readers, we suggest having a look at our recent Enel publication titled We Double Down .

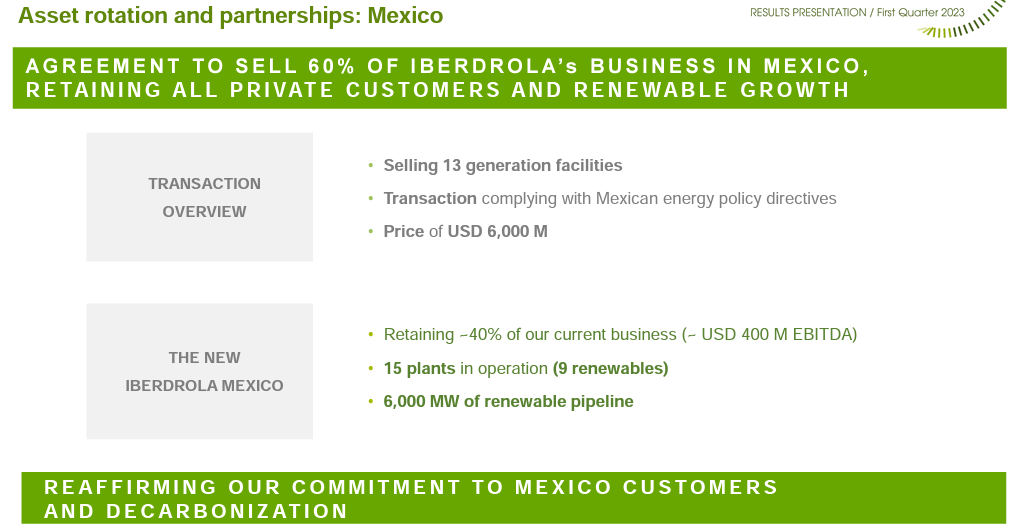

Mexico Deal

It was a good move to sell Iberdrola's Mexican business . The transaction is a positive catalyst for the company and implied an 11x EV/EBITDA multiple. The Mexican assets represent approximately 4% of Iberdrola's EV, but Mexico was a region of risk. In detail, the Spanish energy conglomerate is selling its 8.5GW of renewable concession capacity with a normalized EBITDA of circa $550 million. In the meantime, the company is retaining 2.4GW of private customers' assets, which contribute to $400 million in the company's EBITDA and have upside potential. The sales in Mexico will allow some capital to be invested in the US region as communicated in the 2022 strategic plan. On a balance sheet basis, this will decrease the Net Debt ratio by 50 basis points.

On an aggregate basis, well ahead of 2025, Iberdrola already disposed of 90% of its target assets . Here at the Lab, we assumed a €9.5bn capital gain over the period. This recent disposal will give Iberdrola more balance sheet strength to pursue new acquisitions. This was also emphasized during the call, management is opportunistic in 'A-rated' countries with both organic and M&A teams mentioned.

{kind=link}

Q1 Results

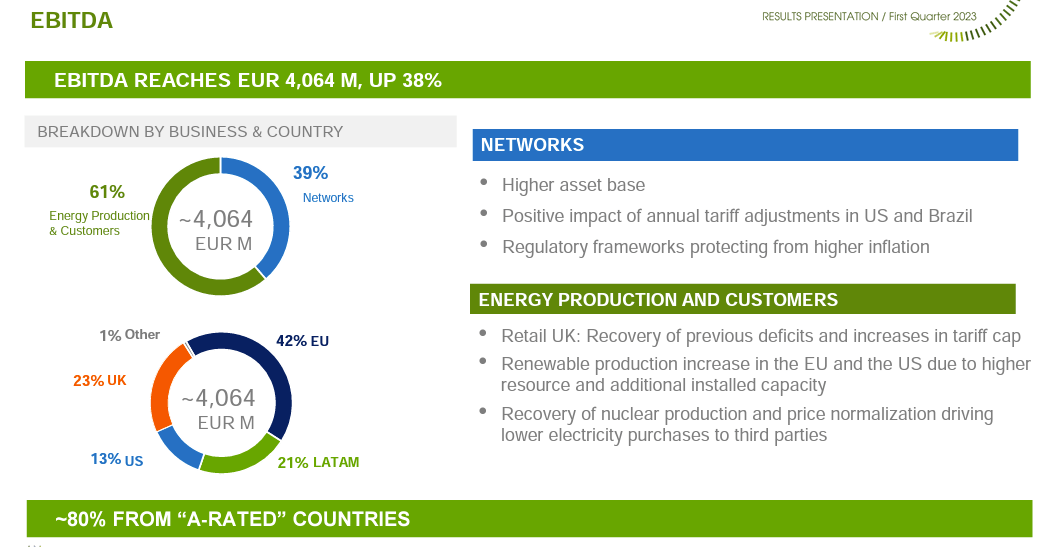

The company delivered a solid set of numbers with EBITDA at a record level of €4.1 billion signing an increase of 38%. This was supported by all the geographies. In detail, 80% of total EBITDA is coming from A-rated regions such as the U.S., the EU (including the UK), and Australia. There was also an increase in renewable output production from wind & solar compared to Q1 2022 and a normalization in retail markets. We should recall that interest expenses were €111 million higher vs Q1 2022 and were due to higher debt on BS as well as higher interest rates. Despite that, the company achieved a net income of €1.49 billion driven by new CAPEX investment and strong operating performance. Net profit development was also favored by the UK recovery of retail deficits.

{kind=link}

Conclusion and Valuation

Since our last update , Iberdrola delivered another 12% stock price appreciation and is approaching our target price. Continuing to value the Spanish energy giant with a 15x P/E, we still derive a buy rating of €13 per share ($55.4 in ADR) versus the current stock market price of €12 per share.

{kind=link}

Even if we are supportive of Iberdrola, the company raised 2023 organic CAPEX investments to €12 billion, and with less disposal (as mentioned 90% were delivered), we see more limited growth given its current leverage. We are continuing to be supportive of Iberdrola's long-term horizon, but we much prefer Enel's investment value proposition.

For further details see:

Iberdrola: We Still Prefer Enel After Earnings