TASK - IBEX Limited: Competitive Position Amidst Market Uncertainties

2023-11-15 05:23:19 ET

Summary

- IBEX has achieved revenue and EBITDA growth of 7% and 17%, respectively, owing to industry tailwinds and a successful growth strategy.

- The company’s margins had been on an upward trajectory, although there has been limited progress in the last 5 years.

- We believe the business is facing tough competition in an unattractive industry, owing to its lack of competitive advantage.

- Illustrating this is IBEX’s financial performance relative to its peers, with below-average growth and margins. The company has struggled to keep pace.

- Although IBEX’s valuation may appear attractive, we think TaskUs is a better choice if investors are looking for exposure to tech-enabled outsourcing.

Investment thesis

Our current investment thesis is:

- IBEX Limited (IBEX) lacks a material competitive advantage that can propel the company into a leading financial position when it transitions toward maturity. Even in its growth phase, the company is underperforming and likely losing market share. Management is placing hopes on its AI innovations but we have yet to see if this will have any impact on the company's fortunes.

- This is not to say IBEX is a bad business, it is not. The issue is that we do not think IBEX is an attractive investment for long-term value. This industry is not very attractive as it is.

Company description

IBEX is a leading global customer engagement firm, providing innovative customer experience solutions to top-tier clients across various industries. With a focus on technology-driven outsourcing services, IBEX assists businesses in enhancing customer satisfaction and driving operational efficiency.

Share price

IBEX's share price performance has been mild, trading flat since 2021. Much of this period has been difficult, with economic conditions transitioning from the post-pandemic bump to an inflationary period with higher rates. Despite this, the market has performed well, although its recovery in 2023 was driven by a handful of technology firms.

Financial analysis

{kind=link}

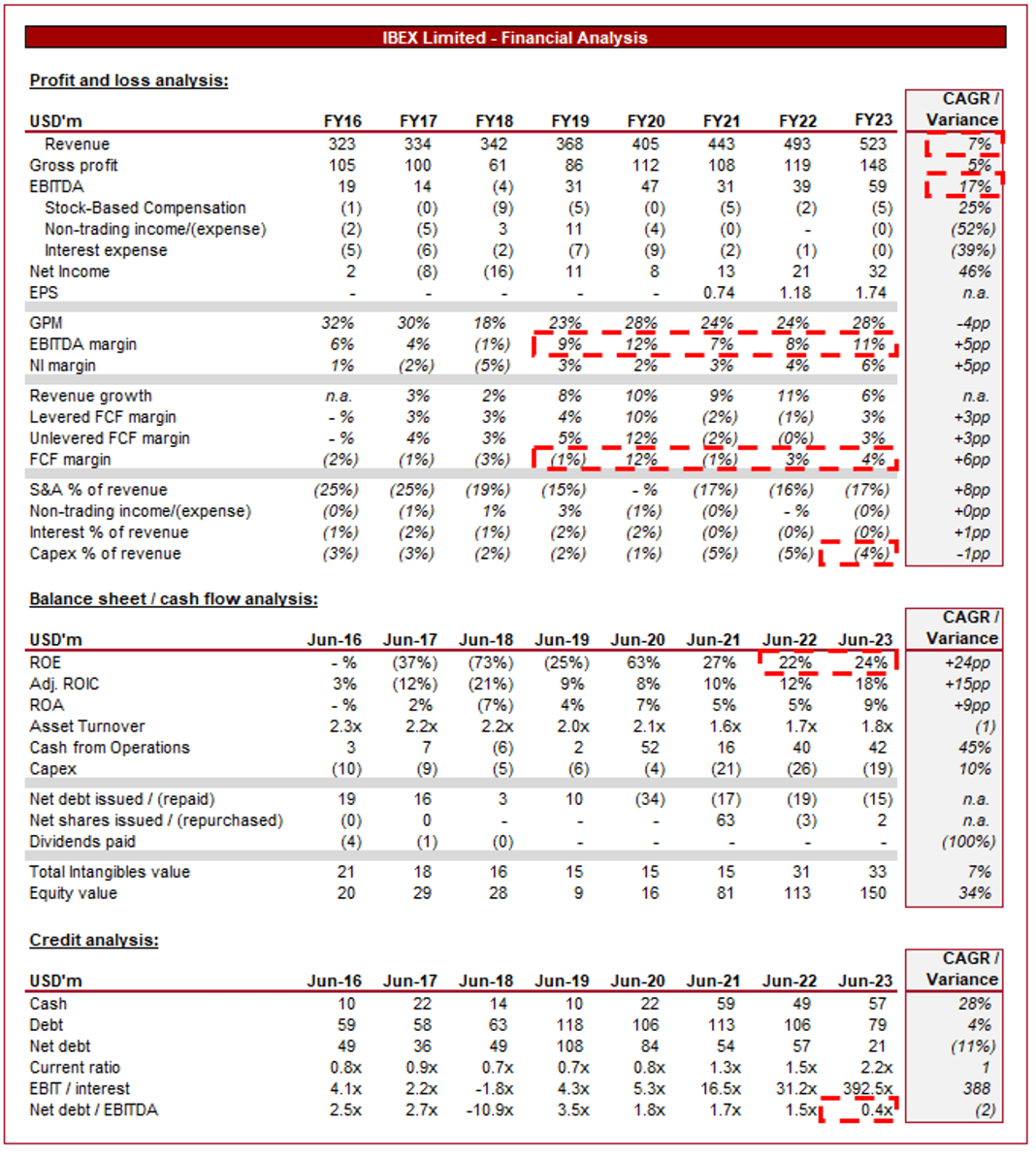

Presented above are IBEX's financial results.

Revenue & Commercial Factors

IBEX's revenue has grown at a CAGR of 7% during the last 7 years, with broadly consistent growth year-on-year, even during the peak of the pandemic. In conjunction with this, margins have sequentially improved, although lacked consistency in recent years.

Business Model

IBEX provides customer support across various channels, including phone, email, chat, social media, and more. This omni-channel approach has become critical as customers seek to interact with businesses through their preferred communication channels, leading to higher customer satisfaction and loyalty. IBEX offers customer support services in multiple languages. This multilingual capability allows them to serve diverse markets and cater to multinational clients.

IBEX also integrates advanced technologies such as AI, chatbots, analytics, and automation into its customer service solutions. This integration streamlines operations, enhances efficiency, and improves the overall customer experience. This has become glaringly obvious to businesses in the last decade, contributing to a rapid uptake of such services.

IBEX tailors its services to cater to specific industries, such as finance, healthcare, retail, and technology. This specialization allows them to develop deep domain expertise, understanding the unique challenges and needs of each sector (both from clients' and customers' perspectives). Industry-specific knowledge enhances the quality of its service and also its ability to convince potential new customers that it has the required expertise. IBEX's specialism is in Fintech, Retail & E-commerce, Telco, and Healthcare.

{kind=link}

IBEX's operations are designed to be highly scalable. It can rapidly adjust its workforce to accommodate fluctuating demand from clients. This allows IBEX to grow alongside its clients, fostering high retention.

Our view is that IBEX's business model is solid, although lacks any standout characteristics. We do not see anything that its peers materially lack, which is a concern when seeking to differentiate. Further, the company's heavy weighting toward Telco and Retail could be restrictive, given these are not fast-growing industries.

Further, a separate criticism of this industry, and IBEX's response in particular, is its heavy weighting toward labor usage. Simplistically, IBEX will always need x number of people to deliver y hours of services. The scope for economies of scale to reduce x relative to y is not currently present in our view. In FY17, each employee generated ~$21k of revenue, now they generate ~$17.5k. Gen AI appears to be the technology that may finally change this dynamic, but we must ask ourselves:

- Will people always need and desire human support in many instances?

- How different from a cost perspective will an AI-driven solution be? (Businesses have been using technology for years to deliver a service with reduced human interaction).

- When with the GenAI stack be powerful enough to materially deviate away from the current business model?

We feel the answers to these questions are not positive for IBEX. A day may come when the fundamental cost base of IBEX changes but we struggle to see it happening in the coming 5-10 years.

Competitive Landscape

The Customer Engagement Solution industry is forecast to grow exceptionally well in the coming decade, with a CAGR of 11% . This is expected to be driven by the continued digitalization of society, contributing to a change in information communication. Additionally, businesses are seeking to outsource a greater proportion of administrative tasks, as greater operational complexity has forced focus.

IBEX faces competition from companies such as Alorica, Teleperformance ( TLPFF ), Concentrix ( CNXC ), and TaskUs ( TASK ).

We consider the following to be key factors in the coming years:

- Technology Integration - Technology has the biggest potential to disrupt the industry. Although we are skeptical about the value proposition, the beauty of the industry is that it can change things overnight. IBEX must incrementally increase its investment in finding innovative solutions.

- Diversified Service Portfolio - Diversifying its service portfolio would allow IBEX to cater to various client needs, increasing its market appeal and revenue potential. We believe this is a trend that will occur in the coming years, as the scope for further support is high. An ability to achieve superior growth could come from providing a broad range of services in a package.

- Operational Efficiency - The inherent nature of the industry is to provide tangible operational efficiencies to clients. The scope for this is high and is only growing as operations become more complex. Operational efficiency reduces costs, improves profit margins, and so can command genuine value from clients.

- Adaptability and Flexibility - Being adaptable and flexible in responding to changing market demands and client needs will be critical in the coming years, as Management teams seek support. IBEX's ability to swiftly adjust strategies, services, and workforce size will enable it to capitalize on emerging opportunities and navigate challenges effectively.

Broadly, IBEX is positioned to benefit from the growth in the wider industry, although we reiterate that its lack of clear differentiation will make competition difficult to overcome. Its key scope to achieve differentiation is producing a superior AI stack.

Margins

{kind=link}

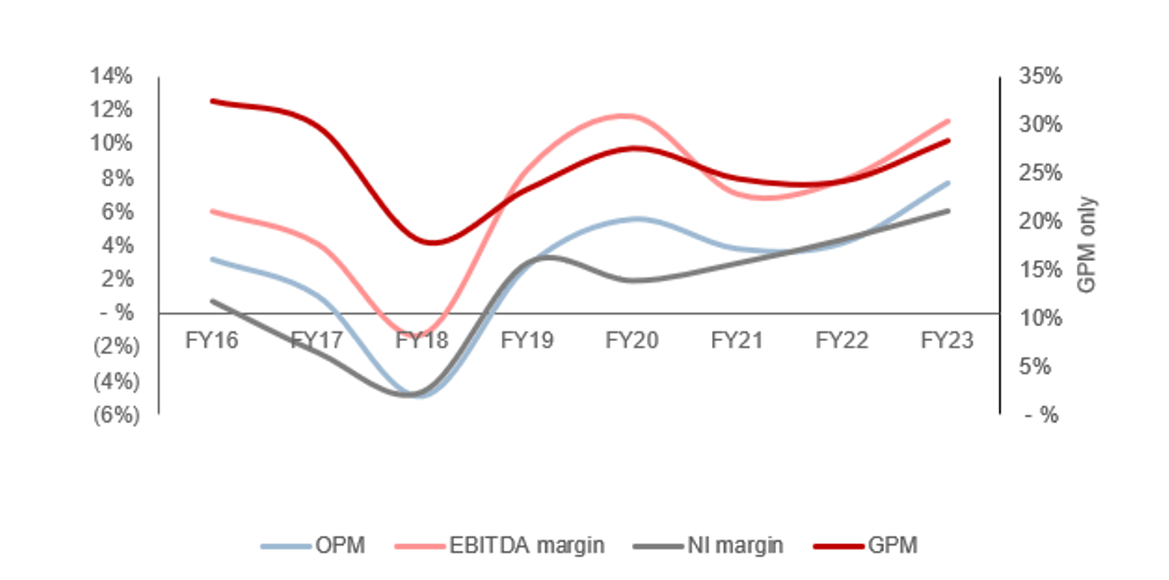

IBEX's margins have improved since its earlier period, although has struggled to develop further since FY20. We attribute this to market conditions, as demand has softened and inflationary pressures have impacted the company's cost basis. We suspect that as healthy demand returns, with greater scale, IBEX should achieve further margin improvement through operating cost leverage.

Quarterly results

IBEX's recent performance has slowed relative to its broader 3-year trajectory, with growth in its last four quarters being +5.5%, +1.9%, +1.0%, and (2.5)%. In conjunction with this, margins have been surprisingly rigid, with improvement in FY23 relative to FY22.

We attribute the slowdown to the current macroeconomic climate, with reduced spending at a corporate level in order to protect margins. With elevated inflation and interest rates, consumers are softening their spending to protect finances and businesses are seeing both demand decline and cost pressures rise.

Key takeaways from IBEX's most recent communications are:

- IBEX's growth has been achieved through new wins, with blue-chip clients in its strategic verticals. Existing growth has meaningfully softened in light of market conditions.

- Strategically, the company has made good progress in its key HealthTech and Retail & E-Commerce verticals, as well as expanding its geographic footprint and capacity utilization. These operational efforts have supported margin strength and offsetting reduced demand.

- Management believes this is the early stages of margin expansion, following the disruption in the pandemic/post-pandemic period. The view is that the scope for operating cost leverage and higher margin service delivery is high, particularly through transitioning to higher margin offshore regions.

- The company is progressing well in developing a market-leading AI-based solution, with Management extremely positive about its relative position to peers.

- Management has reiterated that the pipeline is strong, with sales funnel conversion improving. We are hesitant with this statement as Management is expecting FY24 revenue to be $525-$535m, representing low single-digit growth. This implies that the pipeline is not as strong as expected or customer retention will materially slip.

Balance sheet & Cash Flows

IBEX's balance sheet is relatively clean. The company does not materially utilize debt, allowing for cash flows to be reinvested to grow the company. Thus far, its FCF generation has not translated well from profitability, reflecting the substantial Capex requirements currently and inconsistent working capital management. We believe these minimal returns will continue in the medium term, as Management invests in growth. Beyond this point, its FCF margin could increase several percentage points, allowing for distributions to begin.

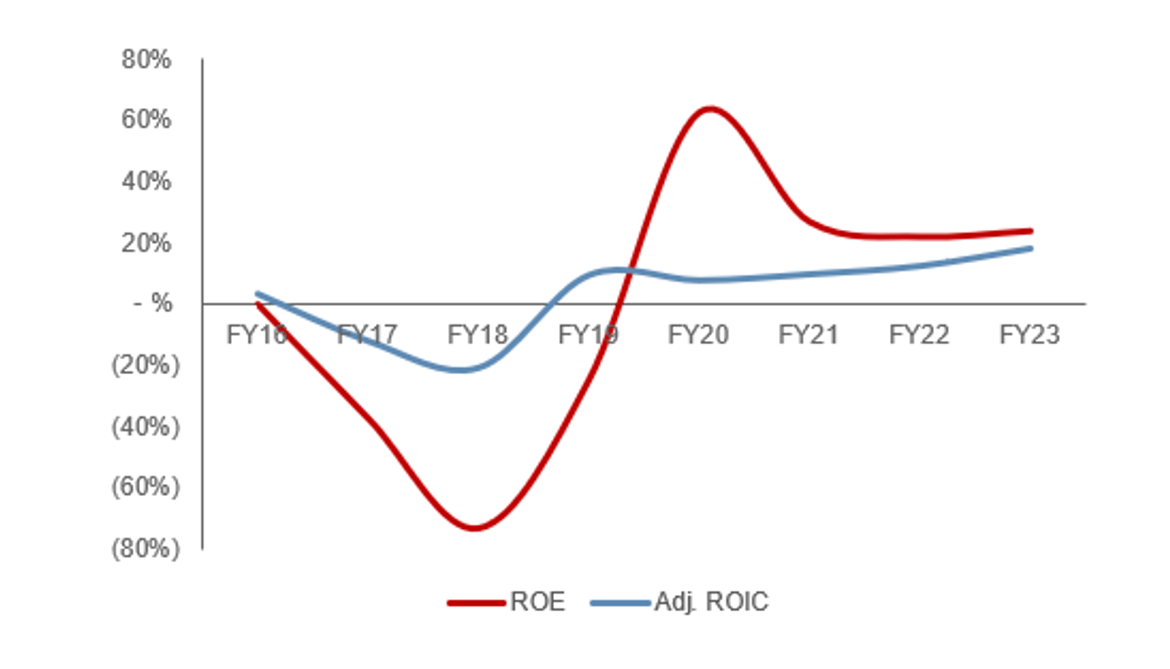

Despite the scope for margin improvement, IBEX's returns are already very impressive. The company currently has a ROE of 24%.

{kind=link}

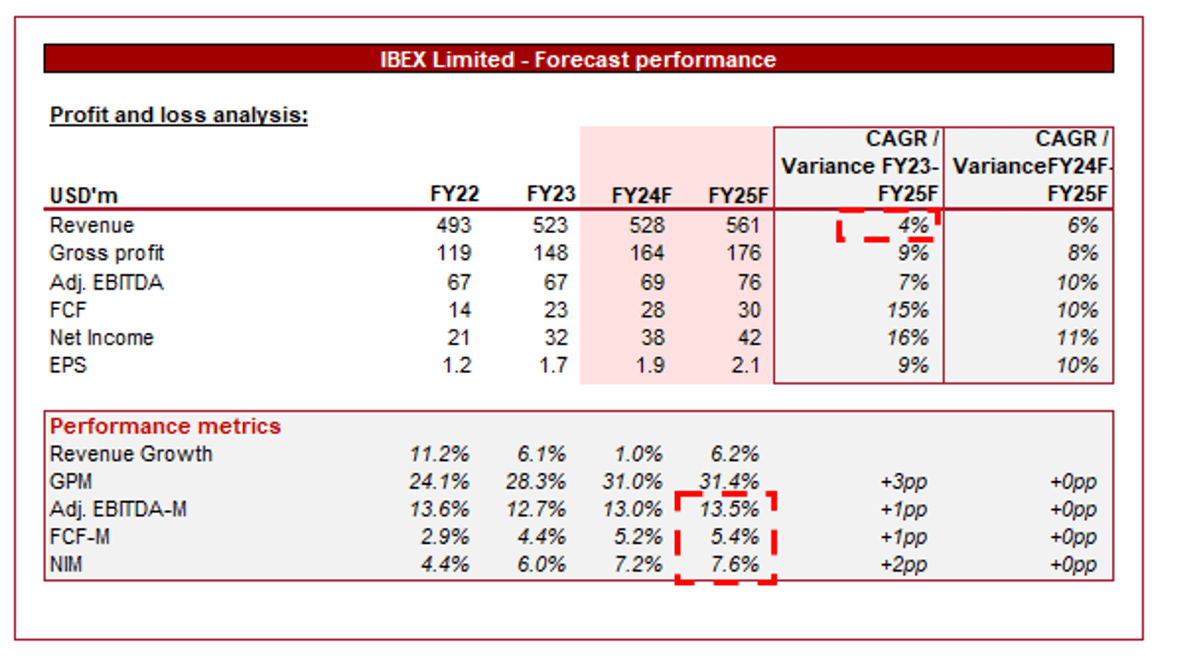

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 2 years.

Analysts are forecasting a reduction in the company's trajectory, with a CAGR of 4% into FY25F. In conjunction with this, margins are expected to remain broadly flat. We consider this outlook to be disappointing given the financial improvement achieved thus far, the industry forecasts, and the industry developments expected.

Our view is that technological integration and the globalization of an increasing proportion of operational capabilities should drive growth beyond this level, implying a degree of uncertainty from analysts around IBEX's capabilities.

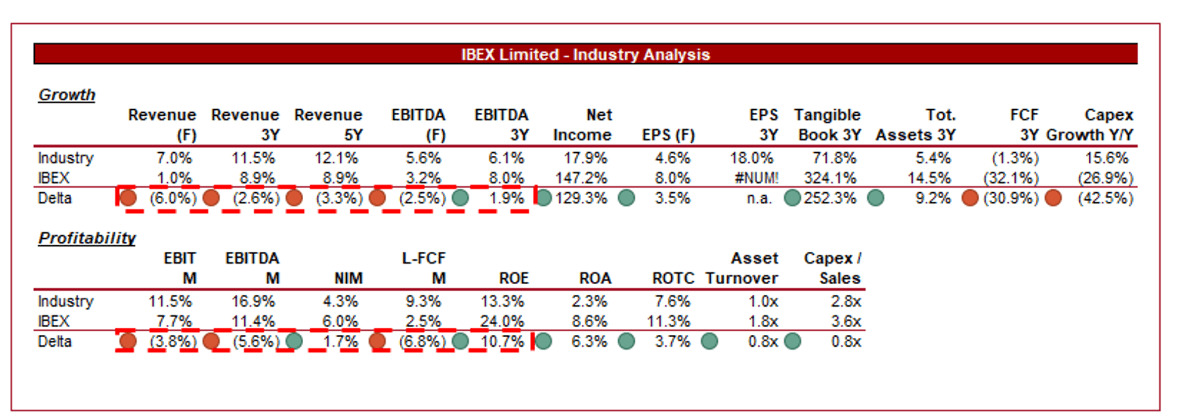

Industry analysis

Data Processing & Outsourced Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of IBEX's growth and profitability to the average of its industry, as defined by Seeking Alpha (18 companies).

IBEX's performance relative to its peers is disappointing. The company has seen below-average growth across the various time periods, with this underperformance expected to continue. This is likely a reflection of the quality of IBEX's services relative to its peers. This is particularly damning given that IBEX is one of the smallest businesses in the group and thus has a higher growth runway.

In conjunction with poor growth, IBEX also has below-average margins. This gap closes on a NIM and ROE basis, which is a respectable performance but the lack of margins is an inherent concern. With scale, IBEX is positioned to see appreciation but we do not see a clear route to above-average levels.

This industry is incredibly competitive and has unattractive qualities due to its labor-intensive nature with scale. Unfortunately for IBEX, it appears the company is not competitive enough relative to its leading peers, clearly lacking the final mile to be a market leader.

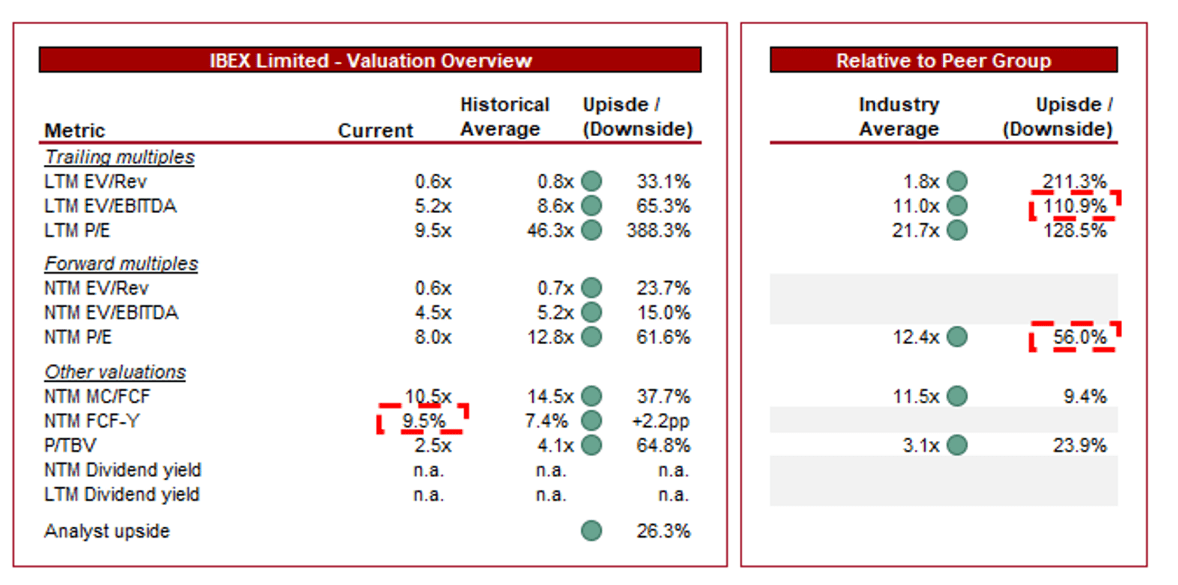

Valuation

{kind=link}

IBEX is currently trading at 5x LTM EBITDA and 5x NTM EBITDA. This is a discount to its (short) historical average.

IBEX is trading at a 111% discount to its peers on a LTM EBITDA basis and 56% on a NTM P/E basis. A discount to its peers is undeniably warranted, owing to the company's poor financial performance relative to this group and the lack of clear competitive advantage. It is making good developments in areas such as AI, but so is TaskUs as an example. We do not see anything unique with IBEX.

TaskUs (which we have also covered) is trading at a similar valuation on a NTM basis, while having better margins and a superior growth trajectory. Based on this, we struggle to rationalize IBEX's current valuation.

This said, it should be highlighted that IBEX is trading at a low valuation. This valuation implies a FCF yield of almost 10%. However, given investors are not seeing any of this cash as tangible distributions, we are not overly convinced.

Final thoughts

IBEX is a solid business that has achieved growth through a combination of industry tailwinds and the provision of a quality service. We struggle to see any key standout characteristics, however, which is likely the reason for its poor performance relative to its peers.

The industry is inherently a tough sell due to its labor-intensive nature, making the scope for accretive returns difficult. With the company trading at a similar valuation to TaskUs, we do not think it is attractively priced.

For further details see:

IBEX Limited: Competitive Position Amidst Market Uncertainties