IBEX - IBEX Limited: No Buying Opportunity Right Now

2023-03-07 08:43:41 ET

Summary

- IBEX recently posted Q2 FY23 results. Their net income and net income margins fell significantly.

- They are overvalued compared to industry standards.

- Technical chart of IBEX is showing bearish signs.

- I assign a hold rating on IBEX stock.

IBEX Limited ( IBEX ) offers complete, technology-enabled customer lifecycle experience options both nationally and globally. Ibex Connect, part of their portfolio of goods and services, offers customer support, revenue generation, and other back-office outsourcing services using the CX model, which combines email, SMS, and other communication apps; ibex digital, a client acquisition strategy that combines platform and e-commerce technology solutions; and ibex CX, a client experience solution that provides exclusive software tools to track and control the customer experience for its clients. They serve banking and financial services, health tech wellness, retail and e-commerce, and travel and hospitality. They recently posted Q2 FY23 results . They saw an increase in revenues, but their net income fell significantly. I'll discuss its future growth potential and analyze its financial performance in this report. IBEX does not appear to be a good purchase right now, and I will explain why in this report. I give IBEX a hold rating.

Financial Analysis

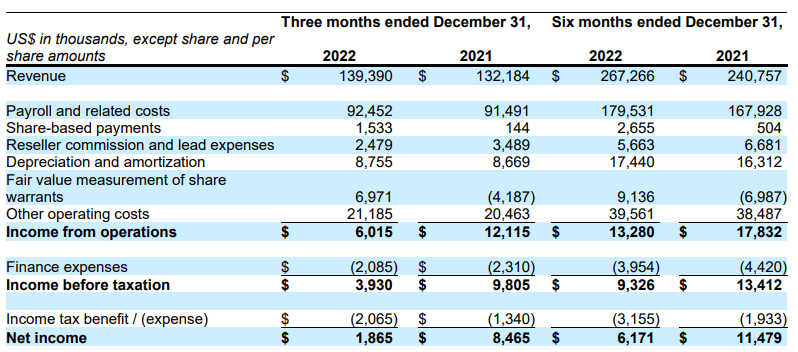

IBEX recently posted Q2 FY23 results . The revenue for Q2 FY23 was $139.4 million, a rise of 5.45% compared to Q2 FY22. The growth in revenue from BPO 2.0 clients, as well as increases in revenue from the retail and e-commerce, fintech, and health tech sectors, are, in my opinion, the main causes of the rise. In comparison to Q2 FY22, the revenue from BPO 2.0 clients increased by 16.9%, while the revenue from the retail and e-commerce sector increased to 26.9% from 22%, and the revenue from fintech and health tech increased to 27.9% from 22.3%.

{kind=link}

The net income for Q2 FY23 was $1.8 million, which was $8.4 million in Q2 FY22. I believe the decline in net income was brought on by the share warrants' being revalued, which was driven by the increase in stock price. The net profit margin in Q2 FY23 declined to 1.3%, which was 6.4% in Q2 FY22. Despite increased revenues, their net income and net income margins dropped significantly in Q2 FY23, which is a matter of concern.

Technical Analysis

{kind=link}

IBEX is trading at the level of $28. According to the daily chart, IBEX's stock has been consolidating between the band of $24 and $27.5 since November 2022. But lately, it broke out with a huge candle, which worries me because it has a huge wick. It demonstrates that selling pressure is still present, and we can observe that the stock dropped shortly after the breakout. The stock is now at a critical point; if it fails to maintain the level of $28, it could enter another period of consolidation and possibly decline by 15%. Because of the uncertainties, in my view, one should refrain from making any new entries into the stock.

Should One Invest In IBEX?

{kind=link}

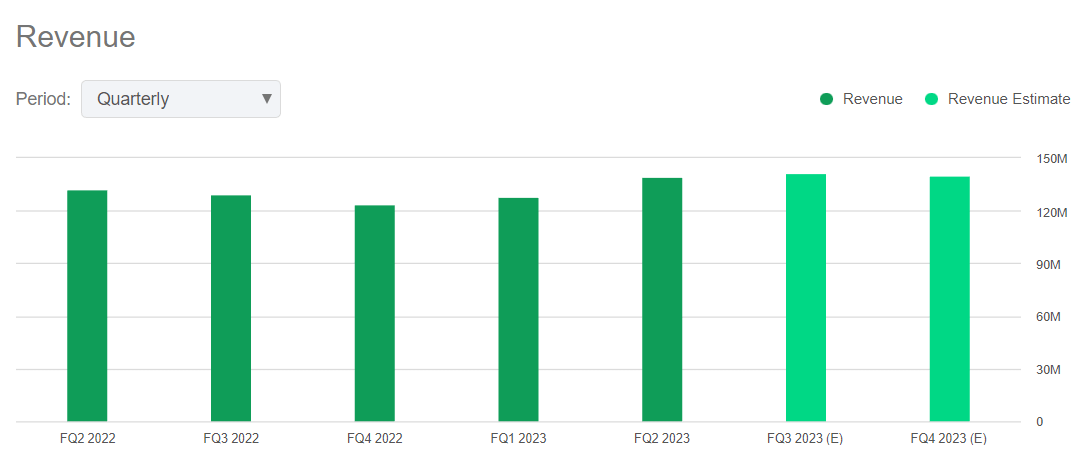

Their revenue grew by 9% in Q2 FY23 compared to Q1 FY23. But if we look at the revenue estimates, we can see that the management is expecting stagnant revenue growth in Q3 FY23. The estimated revenue of Q3 FY23 is around $141.6 million, which is just 1.5% higher than Q2 FY23 revenue. The Q4 FY23 revenue estimate also points to sluggish revenue growth. They did well in the fintech, health tech, retail, and e-commerce segments. However, compared to last year's quarter, the telecommunications vertical's quarterly revenue share fell to 16.7% from 17.3%. Technology's share of quarterly revenue fell to 8.7% from 15%. I think the loss of a legacy technology customer in Q4 FY22 was the cause of the decline. In addition, due to macroeconomic pressures experienced by one of its bigger clients, travel and transportation's share of quarterly revenue dropped to 11.4% from 15.2%. I think the business may experience issues in 2023 due to macroeconomic challenges like inflation, which could impede its revenue growth. In Q2 FY23, they also experienced a sharp decline in net income and net income margin, which is a matter of concern.

Now talking about its valuation. I will use two valuation metrics to judge its valuation. The first ratio is the PEG ratio which is the stock price-to-earnings ratio of a business divided by the earnings growth rate over a given period of time. They have a PEG ((TTM)) ratio of 1.65x compared to the sector ratio of 0.71x. It shows that it is overvalued. The second ratio is the Price / Book ratio. It is a metric used to compare a company's book value to its present market value. They have a Price / Book ((TTM)) ratio of 4.67x compared to the sector ratio of 3.02x. After looking at both ratios, I believe they are currently overvalued and may not have much room for growth.

Risk

Typically, statements of work are entered into with its clients-many of which are for two to five years-including the pricing of its solutions. Sometimes, they agree to set prices for this time frame with little to no sharing of inflation and exchange rate risks. Additionally, they are required by some of its contracts to provide its customers with productivity benefits, such as a decrease in handle time or a faster response time. They could experience an adverse effect on the company if they underestimate future wage inflation rates, unhedged currency exchange rates, or the productivity gains they can realize through a contract.

Bottom Line

They saw an increase in revenue in Q2 FY23, but the net income and net income margins fell significantly. The revenue guidance suggests that the management expects slow revenue growth in the coming quarters. In my opinion, they are overvalued, and the technical chart is showing bearish signs. Considering all these factors, I believe there is no buying opportunity right now in IBEX. Hence I rate IBEX as a hold.

For further details see:

IBEX Limited: No Buying Opportunity Right Now