JNK - IBHE 2025: 7% Yield With No Duration Risk

2024-01-01 00:42:25 ET

Summary

- iShares iBonds 2025 Term High Yield and Income ETF is a less risky high-yield bond fund that will terminate at the end of 2025.

- The fund follows the Bloomberg 2025 Term High Yield and Income Index and uses representative sampling to construct its portfolio.

- 7% yield with no duration risk is an interesting prospect, but we tell you why we are staying out.

High yield has been an appealing sector since late October of 2023. The combination of a benign Federal Reserve alongside the pricing for a perfect economic environment has got investors rushing in with wild abandon. We tend to exercise extreme caution where yield is concerned. This is because with high-yield seeking products where you can break an arm and a leg chasing that thrill. That risk management tends to pay off over the long run, though every rally, like the one we just had, makes investors believe that caution is for wimps. All that caution aside, there are certain products that are less risky than others and can still work out if bought at the right times. Let us look at one such yield from the Blackrock family called iShares iBonds 2025 Term High Yield and Income ETF ( IBHE ).

Fund Overview

IBHE is a term fund and will terminate at the end of 2025. That is now 24 months away and gives investors a rather different way of investing in the high-yield space. While other junk bond ETFs keep rolling their bonds to keep their weighted average maturity the same, not this one. It will terminate at the given time. There is actually an index that this fund follows called the Bloomberg 2025 Term High Yield and Income Index. IBHE was started in May 2019 when this fad first took off and now, we have self-terminating funds for many different years. The fund does not buy every single high-yield bond that matures in 2025 as that would create liquidity issues and they might overpay for some issues. Instead, it relies on what is known as "representative sampling", which means that about 80% of its portfolio will be comprised of securities from the index.

The fund rebalances on the last day of each month and the last one though will be done six months before the fund termination and that would be on June 30, 2025. At that point, we start coming out of high-yield bonds and start reinvesting the proceeds in cash equivalents. This would be Treasury bills in all likelihood but the fund has some discretion here and could go for whichever is the best high-yielding safe choice at the time. The key point is that you are essentially making a bet on high-yield bonds between now and June 2025 and then rapidly (about 16% a month) winding that risk to zero over the next 6 months.

IBHE Portfolio

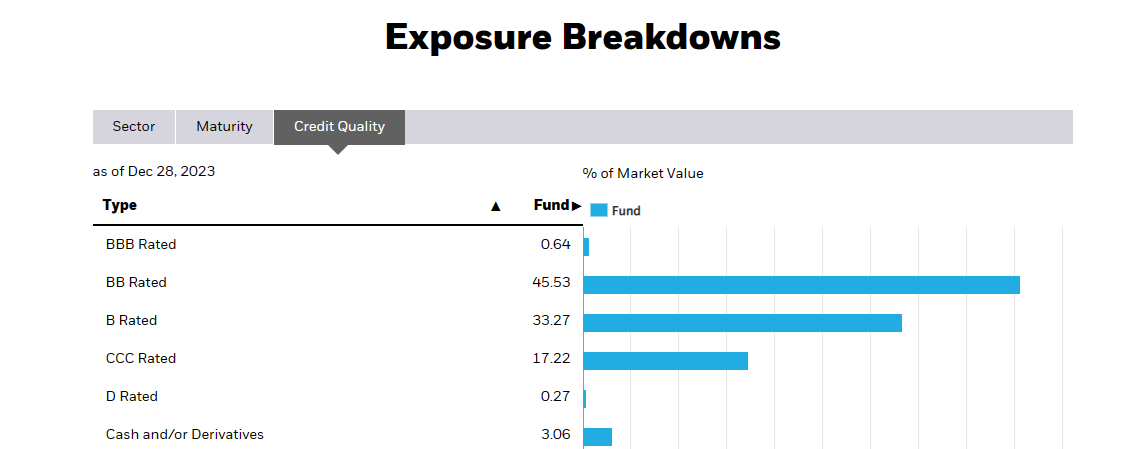

IBHE is still a "high-yield" bond fund, so you are not going to find anything that resembles ultra-quality over here. There is a smidge of BBB Most of the portfolio is rated within two rungs of the IG (investment grade) rating though, so you won't be buying companies near imminent bankruptcy.

{kind=link}

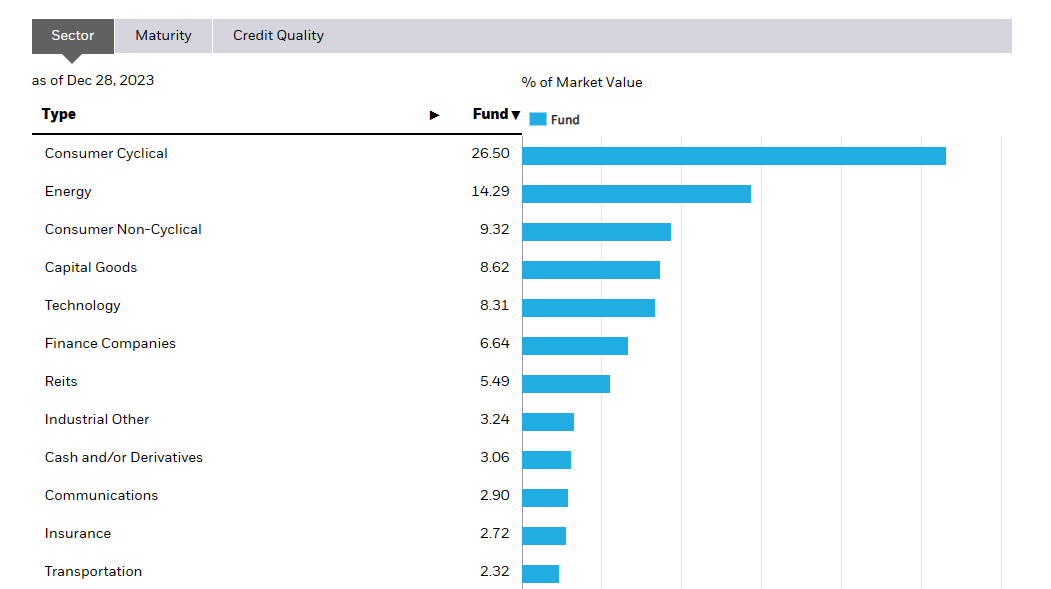

The fund is heavily exposed to consumer cyclicals, followed by energy and the non-cyclical sector.

{kind=link}

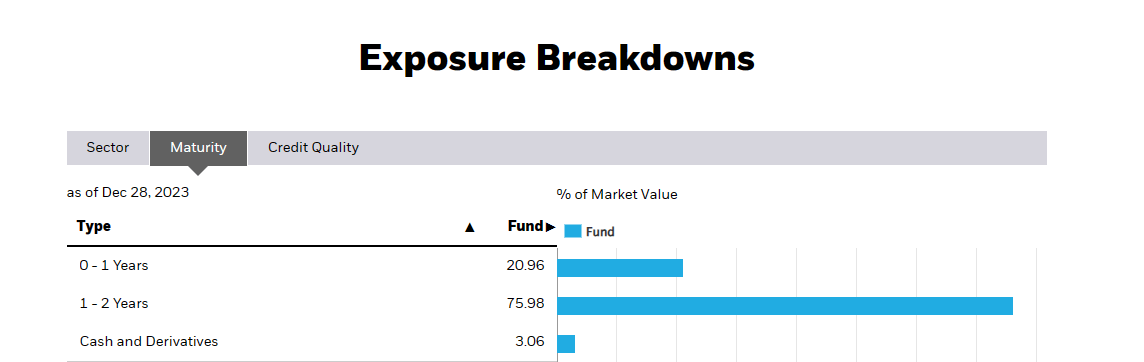

One of the key reasons for a fund like this is that you have the chance to take credit risk without the additional spice of duration risk. Most of the fund holdings mature between 1 and 2 years and that makes sense with the mandate it has.

{kind=link}

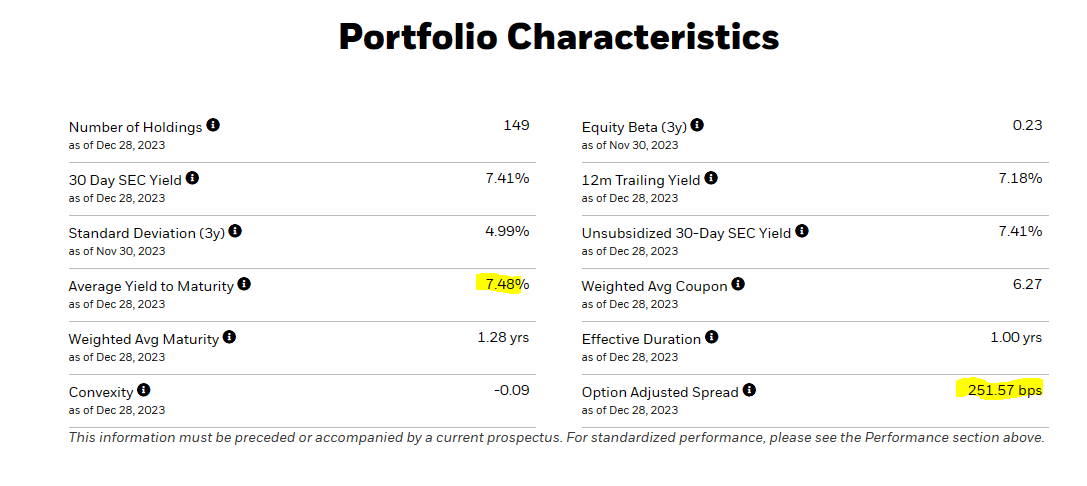

The weighted average maturity is 1.28 years. Key other figures here include the option-adjusted spread, which comes in at 251.57 basis points, and the average yield to maturity of 7.48%.

{kind=link}

For those unfamiliar with the option-adjusted spread concept, it shows the spread between the average yield of these bonds and the equivalent Treasury rate. This is also "adjusted" for bonds that might be called sooner than their maturity. A direct comparative would be a Treasury bond maturing in 1.28 years but you cannot find that on YCharts, so the 1-Year Treasury rate will have to do.

The 4.82% yield here is about 264 basis points away from the Yield to maturity of the fund's holdings (7.48%). If we had a 1.28-year Treasury rate, presumably, it would be 251.57 basis points away. from this.

Outlook & Verdict

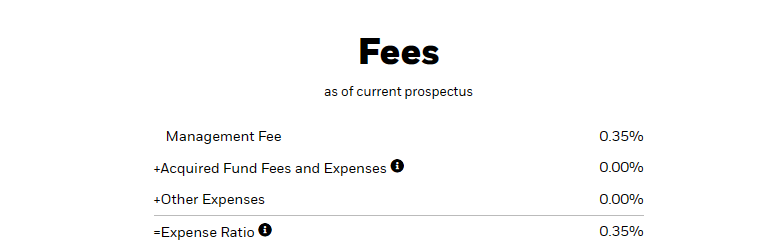

With a yield to maturity of 7.48% your returns will likely be that minus the fees, in the best case scenario.

{kind=link}

So you are aiming for about 7.13% here assuming everything goes right. The last distribution was 14.4 cents, which works to an annualized yield of about 7.48%. We think these distributions will stay stable for now and then head a bit lower to get to that 7.13% effective yield. We believe this is a bit low here, even for such a low-duration bond fund. We are not being prudish and we did give its sister fund a buy rating 6 months back . That was then and this is now. The credit spreads and the extremely close maturity of the fund, allowed us to get behind it. Currently, the market is pricing in 6 Fed rate cuts and we cannot envision that outside of an epic blow-up of a recession. In that case, a "high-yield" ETF is the last place you want to be. Yes, this is relatively better than SPDR® Bloomberg High Yield Bond ETF ( JNK ) and SPDR® Bloomberg Short Term High Yield Bond ETF ( SJNK ), but we focus on absolute returns and give two hoots about just losing less money. We are focusing on select opportunities that we identify for our subscribers, like this one we did recently for an 8.6% yield to maturity for a baby bond maturing in 8 months. There are also longer-term opportunities where we get 8% yields but with investment grade preferred shares . We are staying out of IBHE and rate it a hold. We might pick it up in a market meltdown (read has high-yield spread blowout) as it offers a good way to take credit risk without duration risk.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

IBHE 2025: 7% Yield With No Duration Risk