CTSH - IBM Sold Off While The Market Rebounded But There Is An Opportunity

2023-04-18 09:00:00 ET

Summary

- I believe there is an opportunity in shares of IBM as they look 30-40% undervalued compared to different valuation metrics against their peers.

- IBM has shed its legacy businesses and isn't the same company it was as its focus has shifted to cloud and AI.

- While IBM may not grab headlines, it's changing with the times and still generating billions in profits and running a high-margin business.

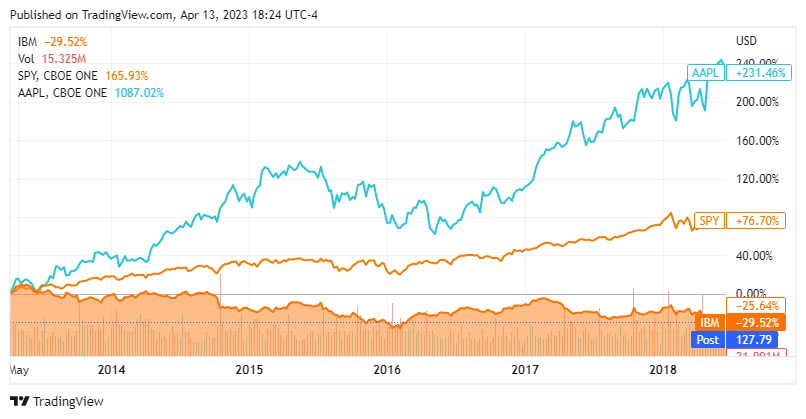

International Business Machines ( IBM ) can't seem to catch a break. Over the past decade, shares have declined -29.52%, and one of the only attractive aspects has been the dividend. In 2011, Berkshire Hathaway (BRK.A) ( BRK.B ) started a position in IBM, purchasing 64 million shares at $170 per share, and at the end of 2017, BRK.B owned more than 2 million shares of IBM. In May of 2018, Warren Buffett told CNBC's Becky Quick that he was almost certain that BRK.B had sold all its shares of IBM and indicated BRK.B had added another 75 million shares of Apple ( AAPL ) in the first quarter of 2018. BRK.B made the correct decision as IBM and AAPL have gone in different directions since then, as AAPL has generated significant returns while IBM has continued to decline. Investing isn't just numbers, as market perception and investor sentiment are critical for stocks to appreciate. I really don't know if there is anything that will get investors excited about IBM again, but there could be an underlying opportunity as IBM is operating a high-margin business leading to billions in EBITDA, net income, and FCF.

{kind=link}

IBM looks like a transformed company compared to the one Berkshire exited

In November of 2021, IBM completed the separation of its managed infrastructure services unit into a new public company. IBM stockholders received one share of Kyndryl common stock for every five shares of IBM common stock, while IBM retained 19.9 percent of the shares of Kyndryl common stock immediately following the separation. Throughout 2022, IBM disposed of its retained interest in Kyndryl and was left with its IBM Infrastructure, Consulting, and Software business.

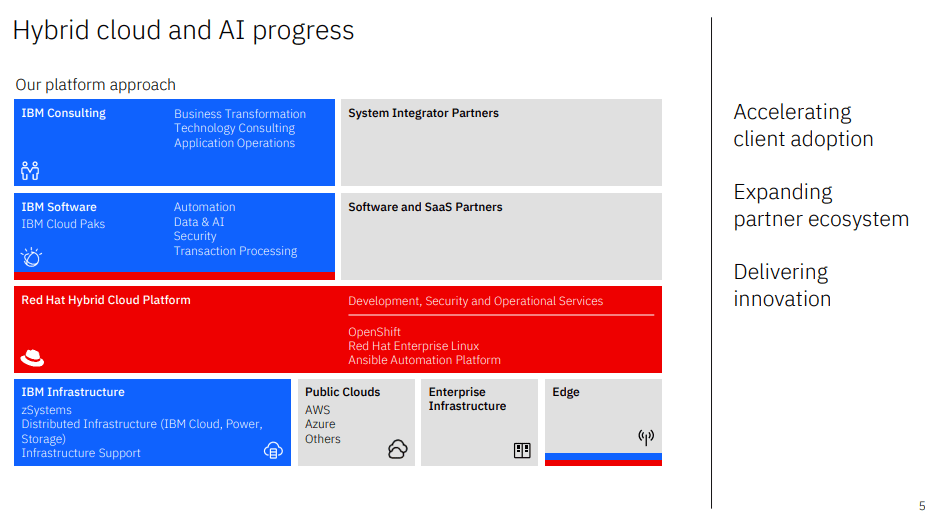

The new IBM is built around hybrid cloud and artificial intelligence ((AI)). Cloud computing has been one of the most transformative technologies as it's changed the technological landscape. AI is still in its infancy, as companies have barely scratched the surface of its capabilities and how it can revolutionize society. Arvind Krishna, who was IBM's former Cloud Chief, has been laying the groundwork for a digital future as he was a driving force behind the RedHat acquisition to serve as the foundation of IBM's hybrid cloud and AI business. IBM's digital transformation has succeeded, and IBM is running a high-margin business focused on the technologies of tomorrow, not yesterday.

{kind=link}

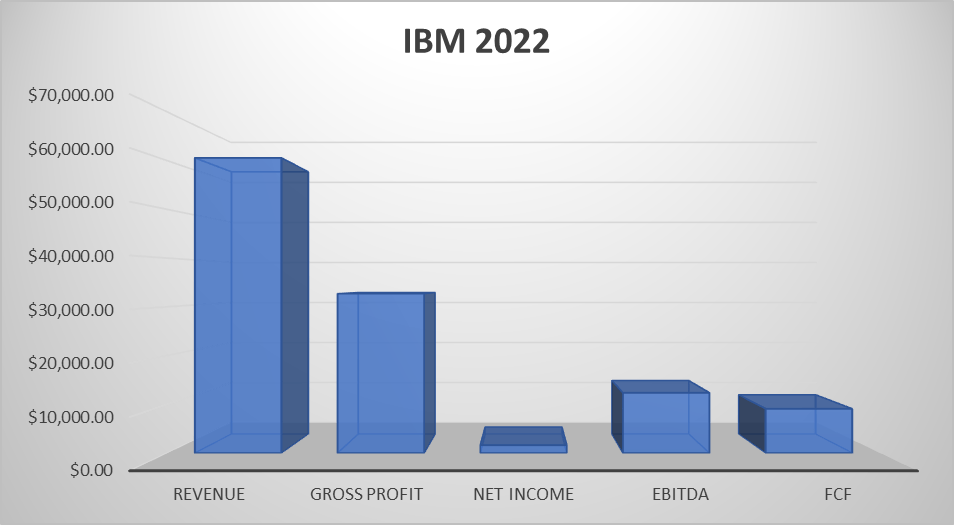

In 2022, IBM generated $60.53 billion in revenue, which comes after spinning off its legacy business. IBM is designing products and services to maximize the business value of hybrid cloud and AI for its clients, and the proof is in the numbers. IBM's software segment generated $25 billion in revenue and saw 12% YoY growth, while Infrastructure produced $15.3 billion in revenue with 14% growth, and consulting generated $19.1 billion in revenue with 15% YoY growth.

The market may be underestimating IBM as they are still an efficient powerhouse. IBM has focused on technologies that have a long roadmap of relevancy while operating at fantastic margins. In 2022, IBM produced $32.69 billion of gross profit, which was a 54% gross margin. This is well above Mr. Buffett's 40% level that he looks for in businesses to determine if they have established a moat. IBM delivered $12.37 billion of EBITDA in 2022, which was a 20.43% margin. Personally, my key measure of profitability is FCF for a number of reasons which I will explain when I look at IBM's valuation. IBM generated an FCF yield of 15.02% as they produced $9.09 billion of FCF in 2022. The bottom line profitability in net income was $1.64 billion, which is a 2.71% profit margin. On the surface, net income is drastically lower than IBM's 2022 EBITDA and FCF, so I looked at it on a quarterly basis to see why. In Q1, net income came in at $662 million, then in Q2, IBM produced $1.47 billion of net income. In Q3, IBM took a loss of -$3.21 billion, and in Q4, IBM produced $2.87 billion in net income. In Q3, IBM had a $1.3 billion income tax expense, and it looks like there was a write-off of $4.5 billion as -$4.5 billion showed up on the line item of EBT Incl Unusual Items. Due to these pieces of information, it makes sense why net income in 2022 is drastically different compared to EBITDA and FCF, and leads me to believe that IBM is still a profit center that investors are overlooking.

{kind=link}

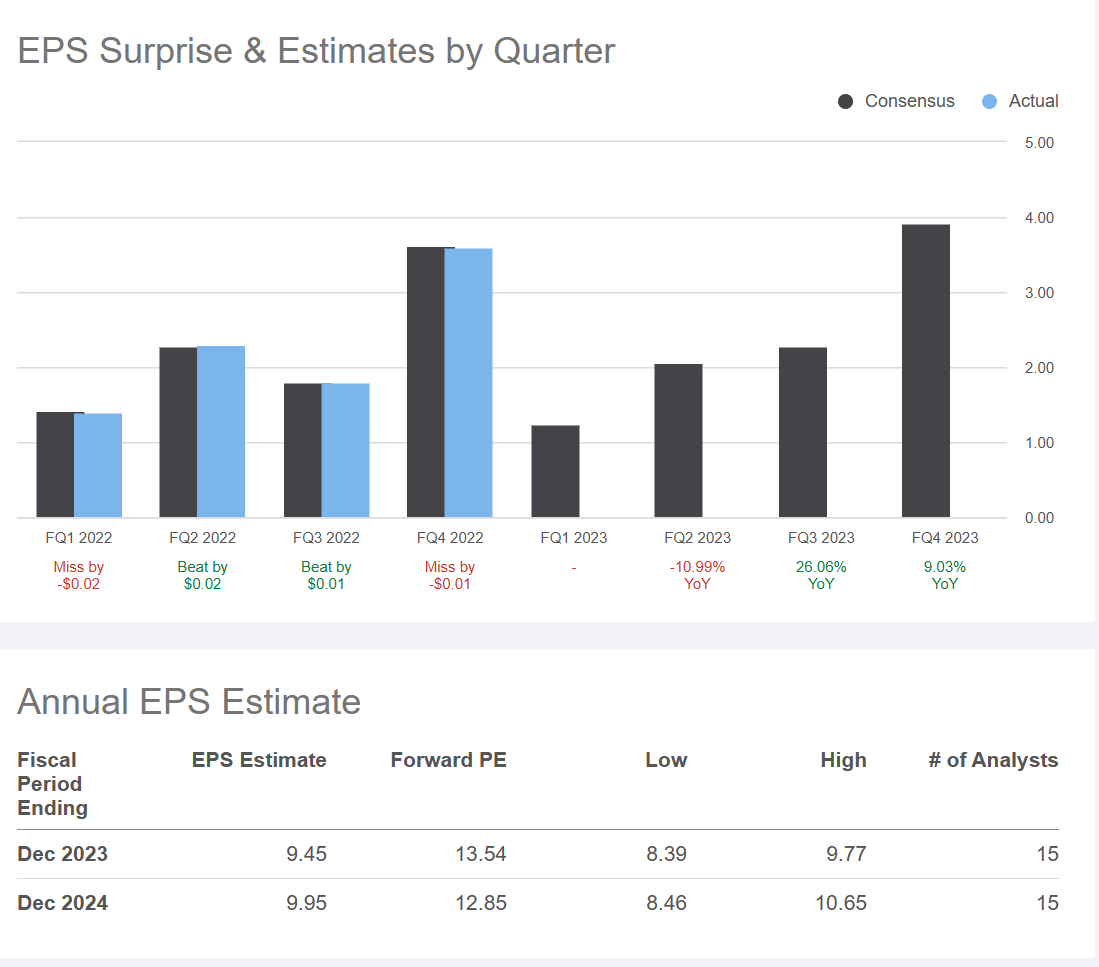

In 2022, IBM generated $9.12 of EPS. There are 15 analysts providing estimates for IBM, and the EPS consensus for 2023 is $9.45, and in 2024, EPS will reach $9.95. On the high end, IBM could reach $9.77 of EPS in 2023 and $10.65 in 2024. On the actual consensus, the analysts are projecting that IBM will increase its EPS by 3.62% YoY and then by another 5.29% YoY in 2024. This also doesn't account for IBM allocating capital to buybacks which could increase EPS further as earnings from operations are distributed across fewer shares.

{kind=link}

IBM looks undervalued on a valuation methodology compared to its peers

I am big on paying a great price for a company so I wanted to see how IBM is valued compared to its peers, which Seeking Alpha lists as:

There isn't a one size fits all approach to valuing companies, and different metrics are more important to different investors. My preference is to base my valuation model on FCF as the profitability measure because, unlike net income, it can't be manipulated through write-offs, write-downs, and other GAAP accounting practices. FCF is simply deducting capital expenditures from the cash generated from operating activities. How much cash a company generates from its operations is much harder to manipulate than net income because $1 of cash from ops should always equal $1 of cash from ops. To determine what I believe the fair market value is, I start with the total equity of a company. Total equity is simply total assets minus total liabilities. This is my baseline because if a company was to dissolve itself, theoretically, the total equity is what would be left for the shareholders to chop up among themselves after all liabilities are zeroed out. After the baseline for total equity is established, I look toward profitability. I can't predict what companies will do in the future, so I take the average price to FCF multiple that the largest companies in the market trade at, then assign that multiple to each company's FCF and add that figure to its total equity. This gives me a baseline valuation because I am taking the equity of the company and an average multiple on profits to determine its value. Then I look at the company's market cap and see if it's currently trading at a discount or premium to what Mr. Market has determined.

{kind=link}

After conducting my analysis, I was surprised at how IBM stacked up against its peers. IBM isn't an unprofitable company, and while it may not be a popular company, they produce real profits with growing estimates. IBM currently trades at a price to FCF of 12.82x compared to the peer group average of 18.8x. IBM produces the largest amount of cash from operations in its peer group, and generates more than double the average amount of FCF than its peers, as its FCF came in at $9.09 billion in 2022. When I use my methodology outlined above, IBM's total equity plus assigning the peer group average FCF multiple on IBM's FCF places my fair market value at $193.1 billion. IBM is currently trading at a -39.75% discount to this number. What's interesting is that IBM trades at a 13.47 P/E ratio, and the peer group average is 19.99. IBM is trading at a -32.60% discount to the peer group average P/E ratio, which is very close to the discount found using my fair market value methodology. Based on the numbers, I believe IBM is undervalued by -30% to -40%.

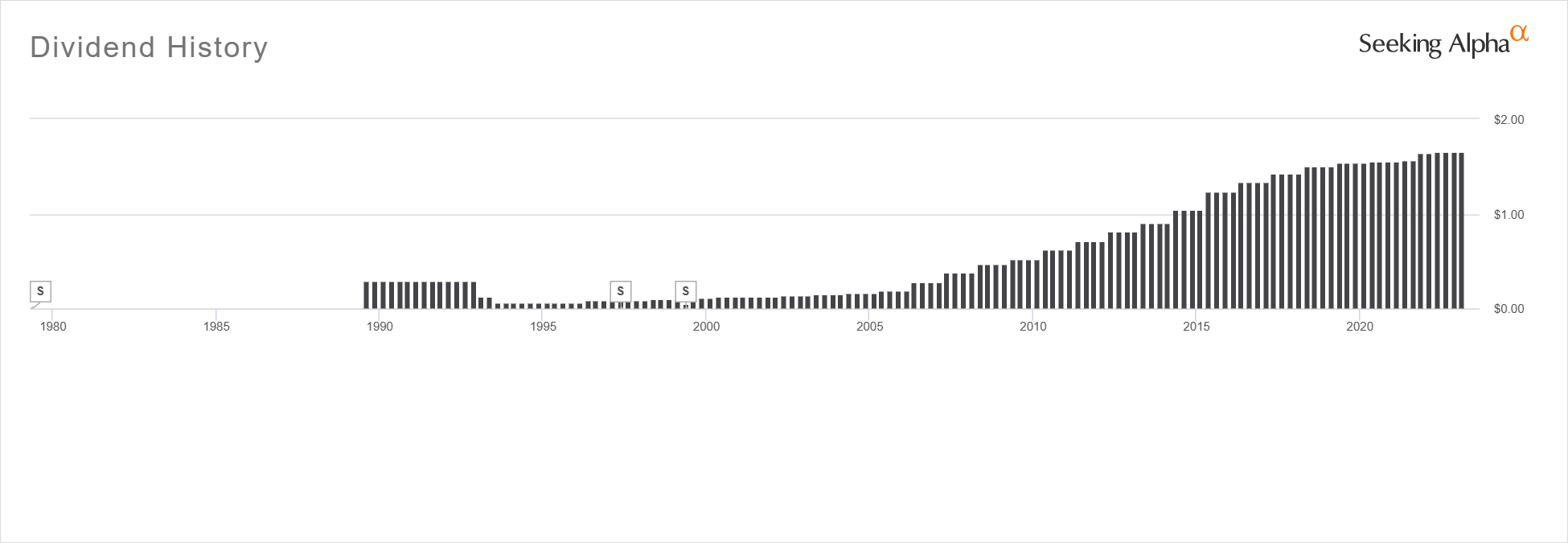

IBM is still paying a hefty dividend with a yield that exceeds 5%

IBM has provided shareholders with 23 consecutive years of dividend growth with a 5-year average growth rate of 2.86%. Today IBM is paying a dividend of $6.60 which is a 5.16% yield. There aren't many places where traditional companies such as IBM generates a yield that exceeds 5% with a track record of consecutive increases that spans over 2 decades. IBM also has a payout ratio of 72.26%, leaving a tremendous amount of room for increases in the future. The dividend is very interesting because as the Fed pivots and starts to reduce rates, CDs and T-bills won't be as attractive, and IBM could become a more sought-after income play. IBM's dividend has everything I look for as its track record for growth is stellar, the yield is strong, and there is significant room for future increases.

{kind=link}

Conclusion

IBM may not grab headlines, and it's certainly not as exciting as AAPL or AMZN, but that doesn't mean it's not undervalued. IBM has undergone a much-needed transformation, shedding its legacy businesses and focusing on the areas that will be growing profit centers for years to come. This isn't the same IBM that BRK.B sold, as its focus is on the future. IBM is operating a high-margin business that generates billions in profits while providing a dividend with a 5% yield. Based on how I look at companies compared to their peers, IBM looks undervalued by 30-40%, and I think this is a good entry point. Analysts are expecting earnings to increase, and at some point, its profitability should get more people excited about it. I think there is an opportunity for capital appreciation and capturing a strong dividend yield in IBM.

For further details see:

IBM Sold Off While The Market Rebounded, But There Is An Opportunity