IEP - Icahn Enterprises: Avoid And Consider CVR Energy Instead

2024-01-07 00:41:25 ET

Summary

- Carl Icahn holds a large stake in Icahn Enterprises LP, and directly or indirectly in two other companies, CVR Energy and CVR Partners.

- IEP cut its distribution in half in August 2023 and faced short attacks, leading to an SEC investigation.

- CVR Energy and CVR Partners, both MLPs, also offer high yield distributions and have performed better than IEP over the past 3 years.

- CVR Energy is poised to deliver outstanding total returns due to improving crack spreads, growth in renewable biodiesel capacity, and a recovery in fertilizer prices in 2024.

Some people get rich studying artificial intelligence. Me, I make money studying natural stupidity. -- Carl Icahn

If you follow the financial news at all you have probably heard of billionaire investor Carl Icahn . You may even know about him from his primary public investment vehicle, Icahn Enterprises LP (IEP), an industrial conglomerate that Icahn incorporated in 1987. From the company website:

Icahn Enterprises L.P. is a diversified holding company engaged in seven primary business segments: Investment, Energy, Automotive, Food Packaging, Real Estate, Home Fashion and Pharma. Icahn Enterprises L.P. is a Delaware master limited partnership.

Icahn currently holds a very large personal stake in the company as reported in December 2023 based on 13-F filings:

On December 27, 2023, a renowned activist investor, increased the holdings in Icahn Enterprises LP by adding 17,060,798 shares. This transaction impacted the portfolio by 2.34% and was executed at a price of $17 per share. Following this addition, the total shares held in IEP by Icahn amounted to 367,879,902, representing a significant 50.56% of the portfolio. The position in the company now stands at an impressive 85.98%, underscoring the confidence Icahn has in Icahn Enterprises LP.

Being an MLP, the IEP units offer investors a very high yield distribution (currently about 22% on a forward annual basis based on $1.00 paid quarterly) and issues a K-1 at tax time. One reason why the company (and Icahn) has been in the news lately is because IEP cut the distribution in half in August 2023.

{kind=link}

Another reason why IEP was in the news in 2023 was due to a short report issued by Hindenburg Research in May. Then an article was published in the NY Times in August that described the efforts of short sellers to attack IEP. Following those events, the SEC decided to investigate, further punishing the stock price.

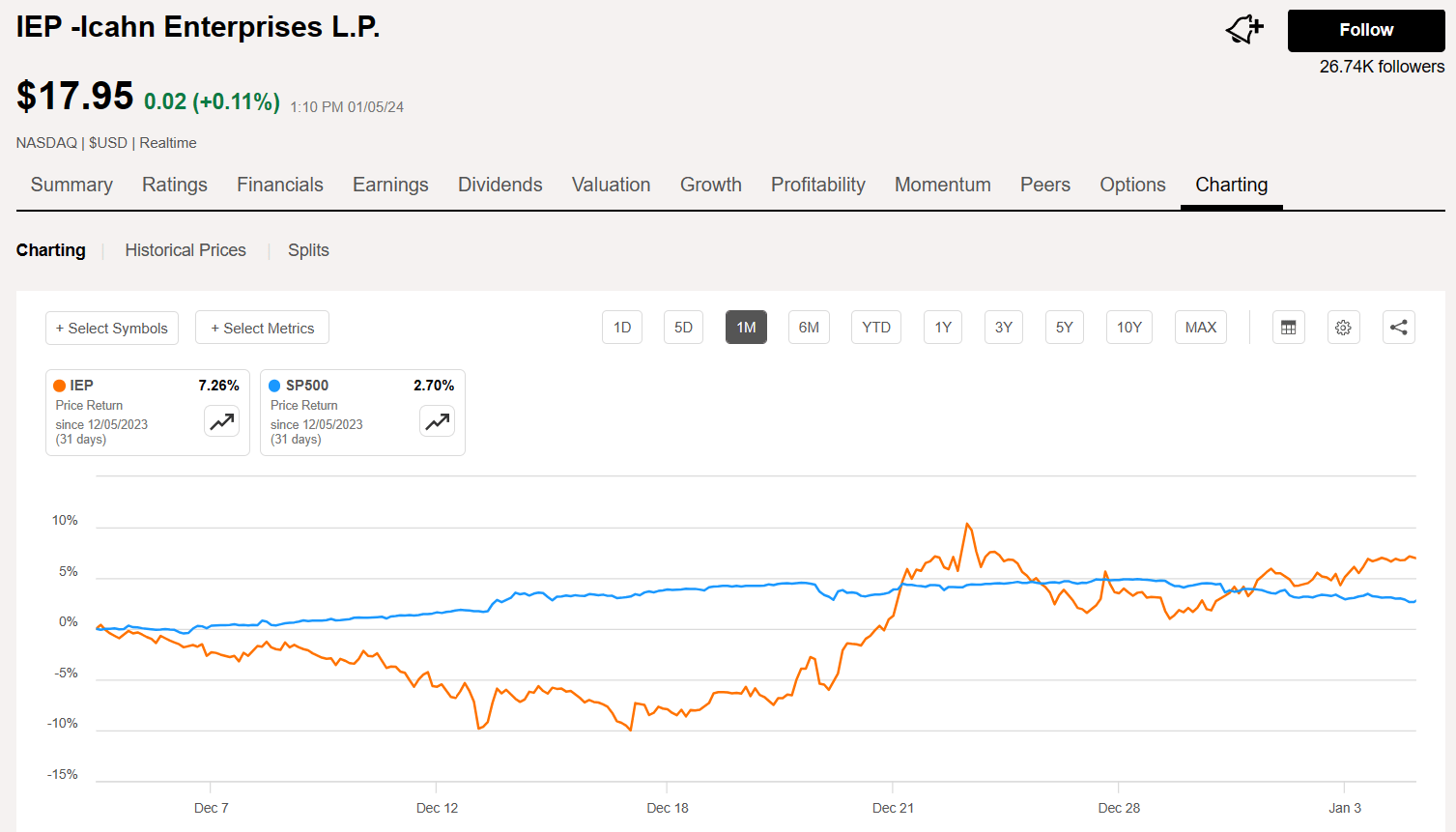

Although Carl holds a large stake in the company it has performed poorly on a total return basis over the past 3 years, and especially in the past year, although it has begun to recover just in the past month.

{kind=link}

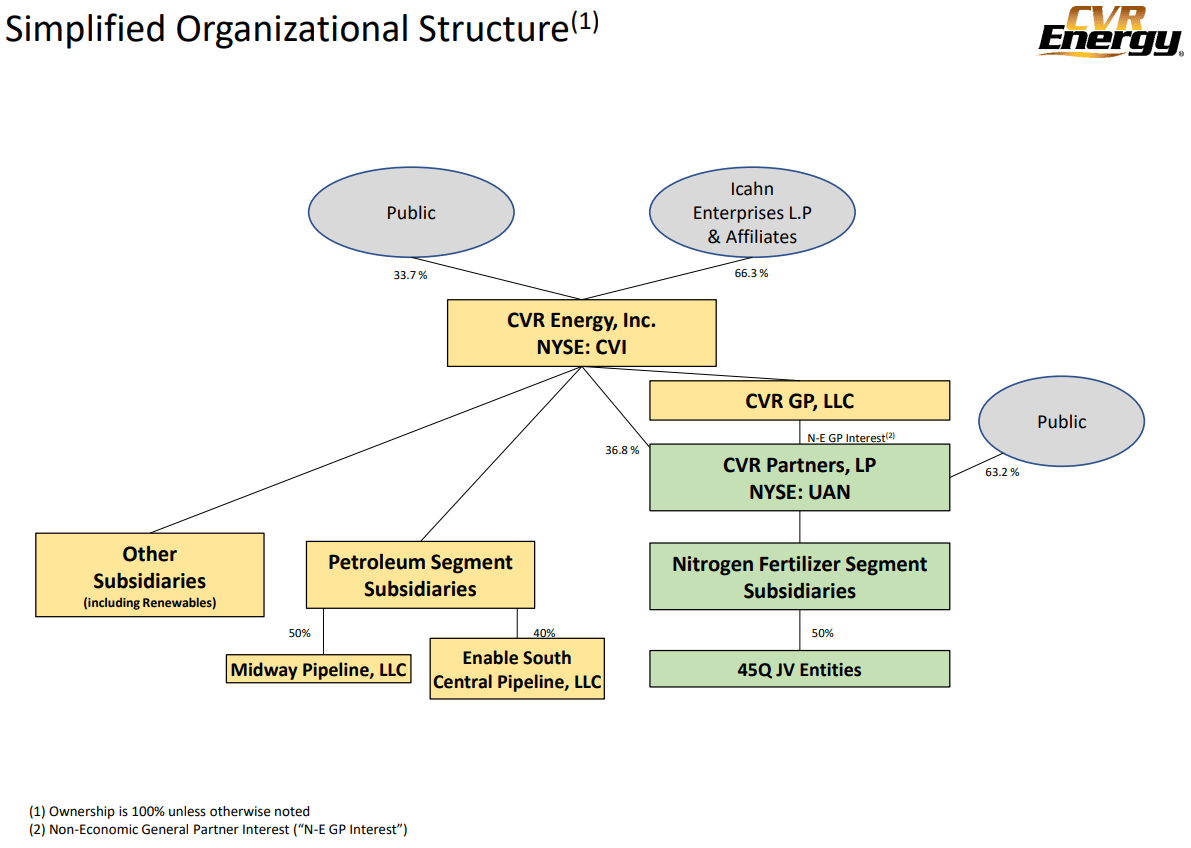

However, two other companies that Icahn also holds ownership stakes and large insider positions in either directly or indirectly have performed better. Those two companies include CVR Energy ( CVI ) and CVR Partners (UAN). The organizational structure of the 3 companies is graphically shown in this slide from the CVR Energy January 2024 investor presentation .

{kind=link}

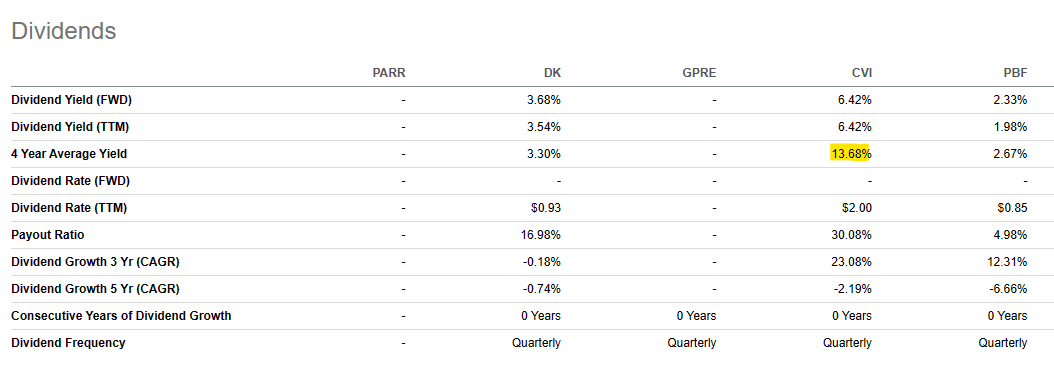

Like IEP, both CVI and UAN are MLPs and issue a K-1 at tax time and both offer high yield distributions. UAN pays a variable distribution on a quarterly basis and the most recent was $1.55 per share declared October 31 for the November quarter. CVI pays a variable quarterly dividend as well that amounts to about 14.5% annual yield based on $4.50 in dividends paid in 2023 (more on that below). Although short interest in IEP has dropped to about 8%, CVI still has high short interest at 21.5%.

{kind=link}

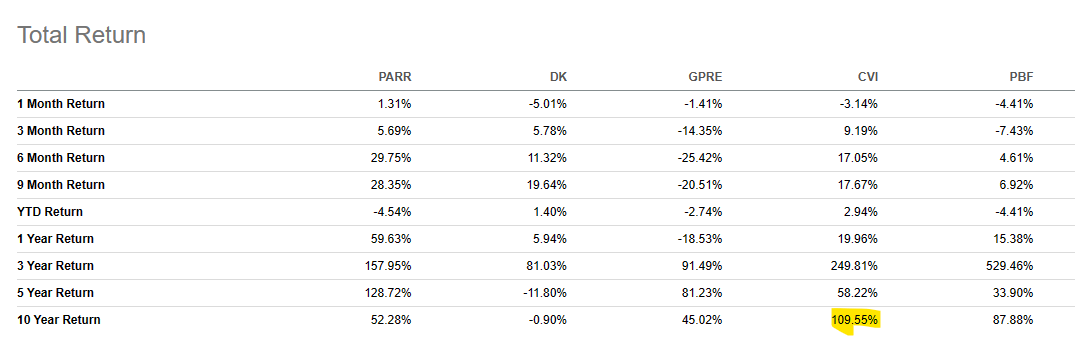

Icahn holds about 66% of the outstanding shares (units) of CVR Energy, even after selling about 4M units back in September. CVI is mostly a refiner and compared to its peers it has performed much better over the past 10 years.

{kind=link}

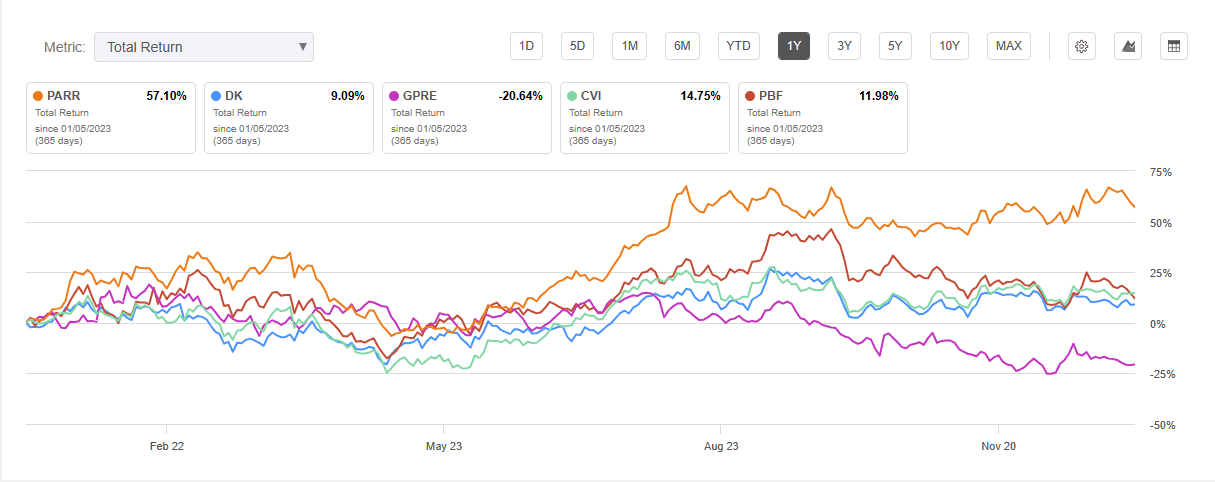

CVI is a close second in the past 1-year based on total return behind Par Pacific Holdings ( PARR ) and is neck and neck with PBF Energy ( PBF ) and Delek US Holdings (DK).

{kind=link}

However, from an income investor’s perspective, the yield from CVI far exceeds any of its peers with a 4-year average annual yield of about 13.7%.

{kind=link}

On a technical and fundamental basis with a forward P/E of 5.6, CVI is undervalued and on track to continue its outperformance in 2024. I rate the stock a Buy and will try to explain why I feel that it should be on your list to consider as we go through another energy transition in the coming year.

{kind=link}

Oil and Commodities on the Rise in 2024

According to a recent call by Goldman Sachs commodities analyst Daan Struyven, commodities such as gold, copper, oil, and aluminum are likely to see increasing demand in 2024.

OECD (Organization for Economic Cooperation and Development) commercial oil stocks’ spare capacity is at 6% of global demand because of OPEC supply cuts and U.S. shale supply growth, said Struyven. “While this spare capacity effectively delays the oil super cycle, it doesn't necessarily prevent it, given how tight long-term supply drivers such as oil reserve life and oil capex still look,” he said.

Furthermore, the wars in the Middle East and Russia/Ukraine continue to be headwinds for the oil sector. On the other hand, slower demand could keep oil prices near $80/barrel according to this story from Reuters, although geopolitical unrest could create some additional price volatility with greater concerns over geopolitics in 2024 compared to 2023. In fact, most forecasts now point to higher oil prices due to the increased geopolitical uncertainty.

The U.S. Energy Information Administration ( EIA ) predicts prices for Brent crude, the global benchmark, will average $93 per barrel, up from an expected 2023 global average of $84 per barrel. Brent crude currently trades near $80 per barrel. It fell as low as $71.84 per barrel in late June before surging as high as $96.55 per barrel in late September as Saudi Arabia extended production cuts.

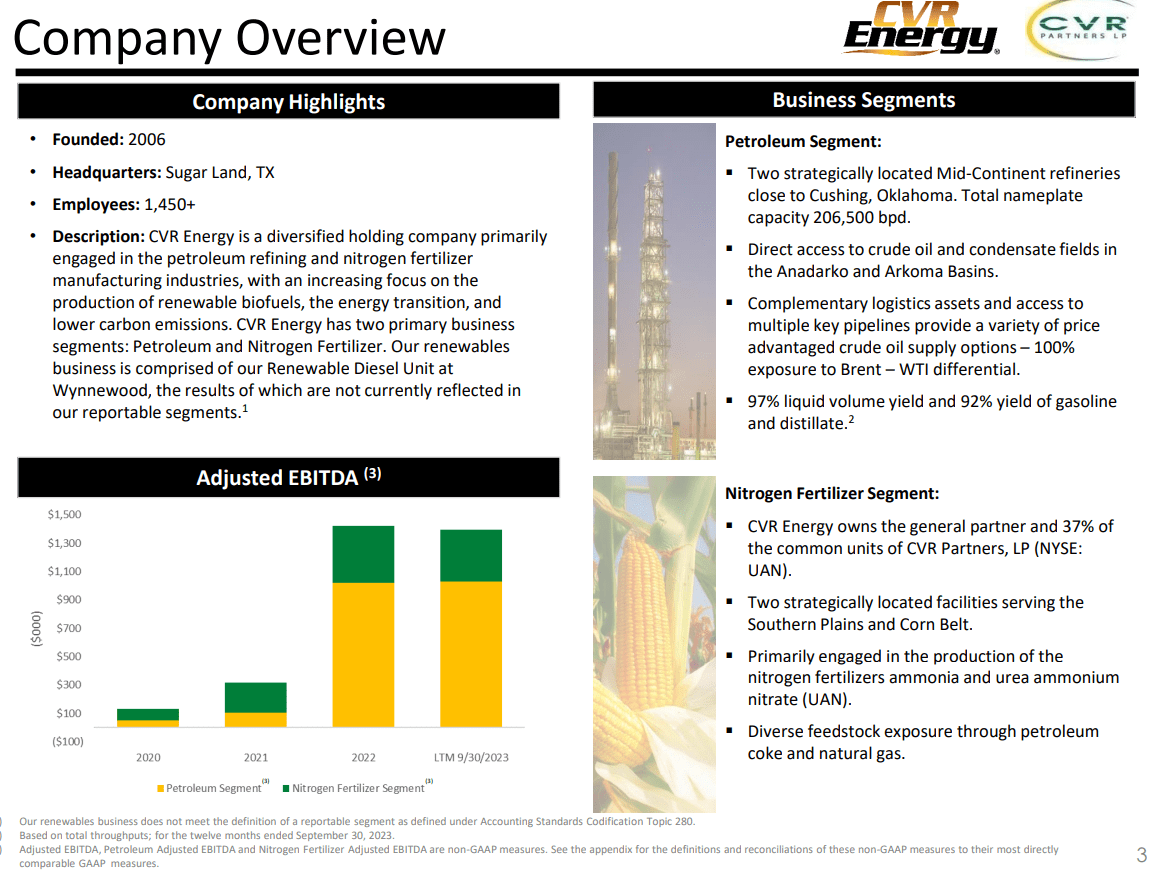

CVR Energy is mostly a refining and renewables company as explained on the slide below from the January 2024 investor presentation, so the price of oil is only one aspect to consider when determining a fair value. And the company has seen a huge increase in EBITDA over the past couple of years, mostly from the petroleum refining segment.

{kind=link}

CVR Energy also owns the general partner and 37% of the units of CVR Partners, so the performance of UAN stock and the nitrogen fertilizer business also directly impacts CVI. Fertilizer prices were recovering in 2023 up until about the end of October but have been sliding since then as shown on this price chart from YCharts .

{kind=link}

Correspondingly, you can see how the price of UAN has mostly followed the trend down over the past year, with some recovery beginning to appear now in January. The price of UAN appears to have bottomed out in mid-December at about $62 and is now on the rise again in 2024.

{kind=link}

As explained in this recent article on UAN, there are a lot of complicating international factors impacting fertilizer prices, including seasonal factors:

Right now, prices appear to have bottomed and have been increasing. Ammonia has led the way, but UAN prices should follow. The market is just very thin this time of year for the product.

A lot of international factors can impact nitrogen fertilizer prices, including Chinese exports, Indian and Brazilian imports, and international gas prices, so there is always risk associated with fertilizer names.

While UAN is rated a Buy by most SA analysts and a Hold by Wall Street, that business represents about one third of the overall EBITDA contribution to CVI. The outlook for 2024 looks positive for UAN, which bodes well for that part of the CVI business segment. For example, the US has become an exporter of nitrogen fertilizer to Europe as a result of the Ukraine conflict, which has led to increased demand for UAN products. Reduced supply due to restrictions on exports from China have added to the positive demand/supply imbalance in favor of UAN as explained in this slide from the January presentation.

{kind=link}

The other major business segments include petroleum refining and renewable biofuels, which are seeing an increased focus since February 2023.

Renewable Biofuels Business Segment

{kind=link}

The changing landscape and growing acceptance of renewable diesel have opened the door for CVI to benefit from their capital investments in that business segment. This report on growth in renewable energy in the US discusses the growing acceptance and generation of renewable biofuels:

In addition to landfill gas, biofuels can be synthesized from dedicated crops, trees and grasses, agricultural waste, and algae feedstock; these include renewable forms of diesel, ethanol, butanol, methane, and other hydrocarbons. Corn ethanol is the most widely used biofuel in the United States. Roughly 39 percent of the U.S. corn crop was diverted to the production of ethanol for gasoline in 2019, up from 20 percent in 2006. Gasoline with up to 10 percent ethanol (E10) can be used in most vehicles without further modification, while special flexible fuel vehicles can use a gasoline-ethanol blend that has up to 85 percent ethanol (E85).

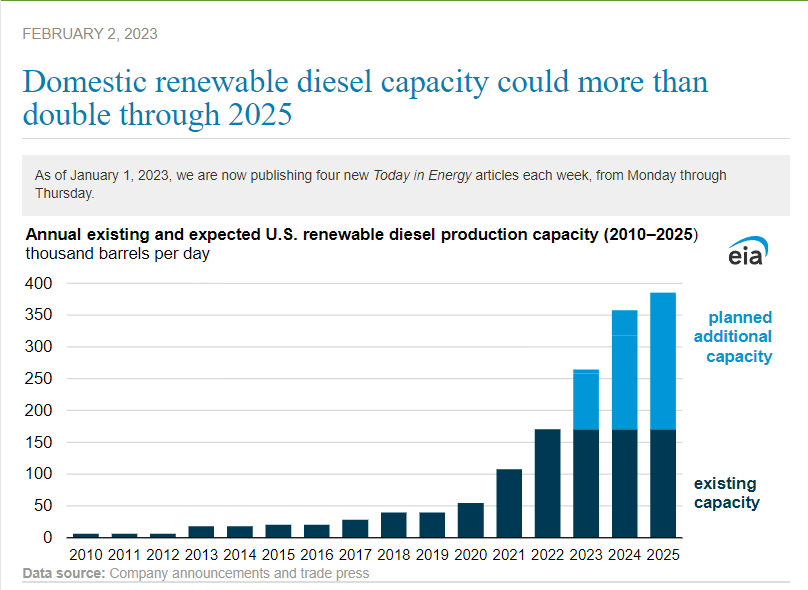

Published in February 2023, this report from EIA illustrates the growing increase in domestic renewable diesel capacity since 2010 that is projected to further increase dramatically over the next few years.

Investment in new renewable diesel production capacity has recently grown significantly in the United States because of renewable diesel’s interchangeability with petroleum diesel in existing petroleum infrastructure and because of government incentives.

{kind=link}

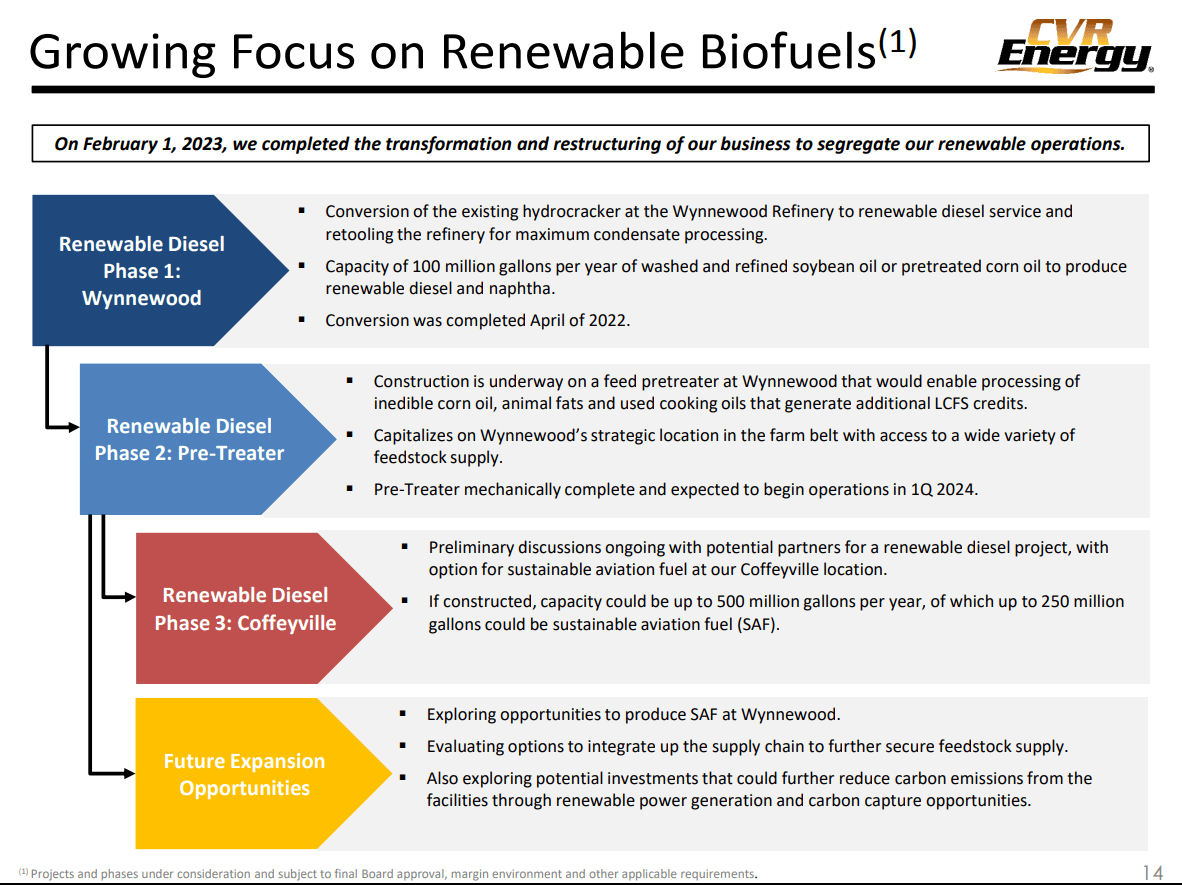

The Wynnewood renewable diesel facility was completed as part of Phase 1 in April 2022 and now has the capacity to process 100 million gallons per year of washed and refined soybean oil and pretreated corn oil to produce renewable diesel and naphtha. It was one of eight new refineries of renewable diesel that began production in 2022 and 2023. Phase 2 will add a diesel pre-treater to help increase capacity and generate LCFS credits and is expected to be begin operations in Q1 2024.

Petroleum Refining Business Segment

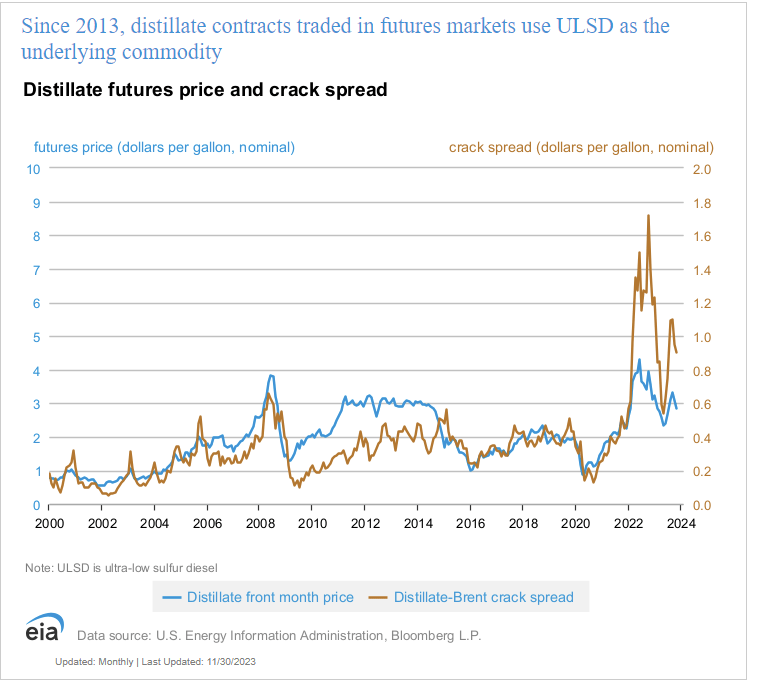

The bulk of the revenues generated by CVI is from refining petroleum products and that is how most investors view the company. As discussed in previous articles covering CVI, the refining business is cyclical, there is not a lot of new refining capacity coming online, and crack spreads narrowed in 2020 after the Covid pandemic and then jumped higher in 2022. They have since retreated but remain at higher levels, as shown in this chart from the EIA. The volatility in crack spreads leads to uncertainty and an unwillingness to dedicate large amounts of capital to new refining projects.

{kind=link}

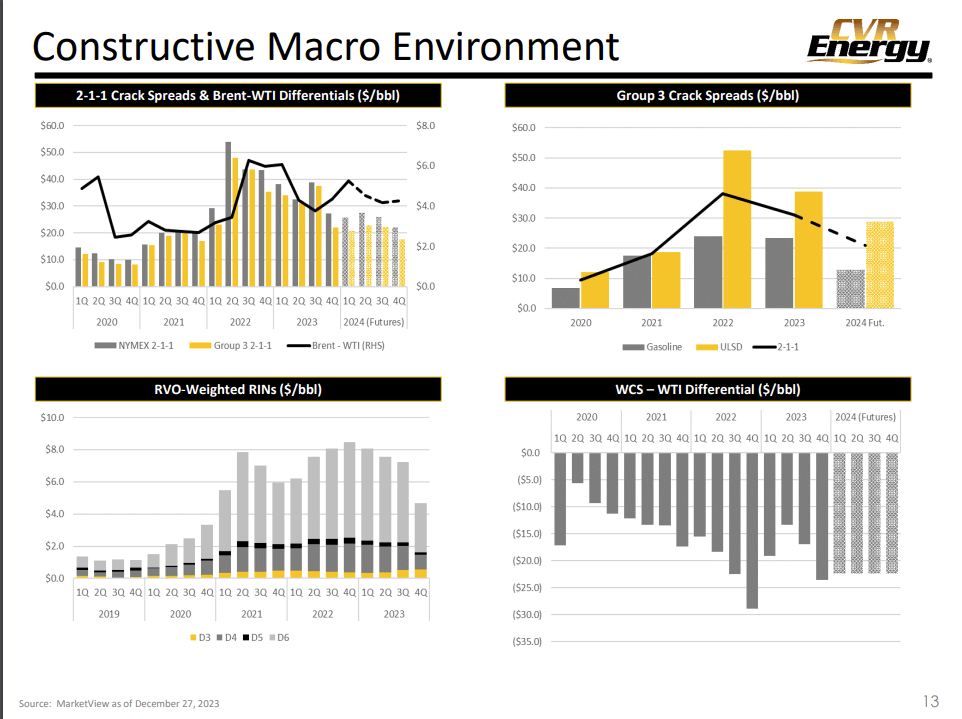

Another way of looking at it is the differential between crude oil prices and the crack spread, which is showing a favorable trend based on the constructive macro environment that CVI depicts on this slide from the January presentation.

{kind=link}

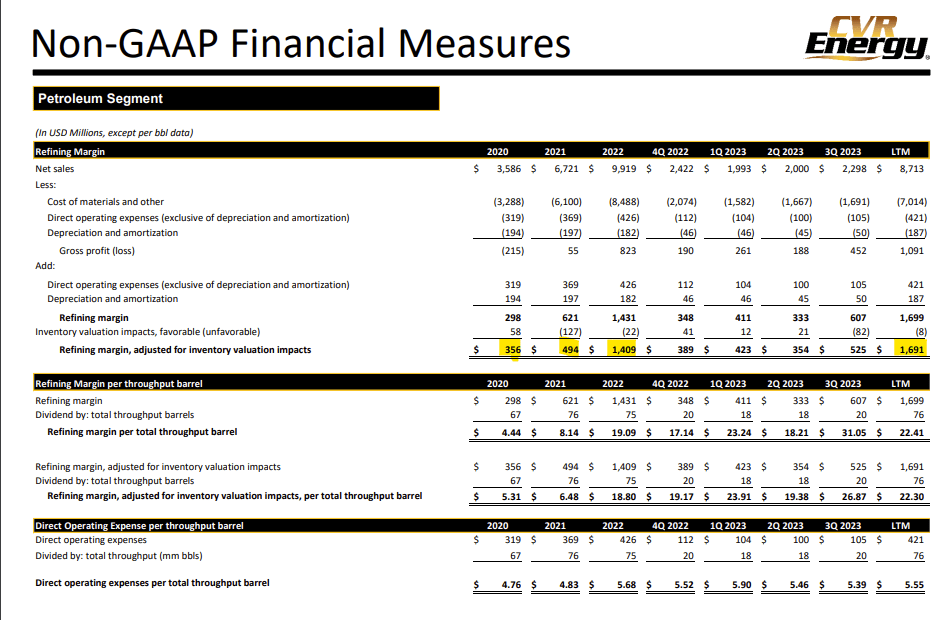

Looking at it from a financial perspective, it is apparent that the refining margins have been improving year over year since 2020 through the 3 rd quarter of 2023.

{kind=link}

Adjusted EBITDA has also been tracking upward since 2020 with 2023 approaching 2022 levels as of Q3.

{kind=link}

Based on comments made during the October 31 Q3 earnings call , company management is cautious about the outlook for Q4 and believes that significant geopolitical risk could negatively impact the market. CEO Dave Lamp had this to say about the outlook for Q4:

Starting with Refining, crack spreads remained elevated in the third quarter of 2023 with gas and diesel cracks both increasing relative to the second quarter.

Although U.S. Refining product demand is down in general, gasoline inventories are roughly in line with five-year averages and distillate inventories are over 12% below the five-year average. Reduced Refining capacity in the United States, ongoing turnaround activity and a string of unplanned outages during 2023 have all helped keep refined product inventories in check. Exports of gasoline and diesel have also continued to be strong, consistently averaging over 2 million barrels per day so far in 2023.

Distributions

In 2023, the company declared and issued regular and special distributions totaling $4.50 YTD through Q3 2023, which amounts to a yield of about 14.5% on an annual basis. The dividend history shows that a regular quarterly dividend of $0.50 was paid each quarter with a $1.00 special paid in Q2 and another $1.50 special paid in Q3.

{kind=link}

The stated annual yield that you will see on most sites that summarize the distribution for CVI show a yield of about 6%, but that does not include the specials that have been paid out for the past two quarters (or the two specials paid in 2022). For investors interested in realizing income from their investments in an energy stock, CVI offers some respectable shareholder returns.

In my opinion and based on this review of the stock with the increasing growth prospects for renewables, fertilizer, and refining margins, I believe that 2024 will likely include either an increase in the regular distribution, or more specials, or potentially both because of the improvement in financials and prospects for further growth in each of the business segments.

Risks and Summary

The primary risk to the stock performance in 2024 as mentioned above is the prospect of continued geopolitical instability and the potential negative impact that can have on global energy demand and the prices of oil, natural gas, ammonia, and other commodities. As those input costs rise and if crack spreads continue to decline, CVI will have a tougher time growing EBITDA and further increasing refining margins.

On the other hand, with growing demand for and increasing capacity to deliver renewable energy like biodiesel and ethanol, CVI stands to benefit from the inflationary pressures that we saw in 2023 and that may continue into 2024. Also, the short attacks on Carl Icahn and his businesses are starting to diminish now and will be seeking new targets as the stock prices of IEP, UAN, and CVI recover. At the current price of about $31 it is my opinion that CVI should be considered a Buy for investors seeking income along with some capital appreciation over the next few years as the energy transition continues.

For further details see:

Icahn Enterprises: Avoid And Consider CVR Energy Instead