IFF - Icahn Enterprises LP: An Update On Its Ballooning Unit Count

2023-08-11 13:30:00 ET

Summary

- Total IEP units outstanding increased by over 10% in the second quarter alone, contributing to a further decrease in IEP's Net Asset Value (NAV) per unit.

- This occurred despite an increasing number of outside investors, almost 70%, taking distributions in cash rather than units on June 30.

- This also occurred despite no "At-the-Market" offerings being done in Q2.

- These factors, along with a substantially lower market price for the units, put continued downward pressure on IEP's per unit NAV.

- IEP continues to trade at a multiple of its underlying NAV, and even its newly announced lower distribution surely looks unsustainable.

An Update to My Recent Article

On July 24, Seeking Alpha published an article of mine titled " Some Implications of Icahn Enterprises LP's Ballooning Unit Count " ( IEP ). In it, I warned about the company's continuing rapid increase in its units outstanding as a result of Carl Icahn, as well as some outside investors, taking distributions in units rather than cash, along with the impact of additional units being issued under IEP's "At-The-Market" (ATM) offerings. I used the information available at the time to estimate the possible size of these offerings in Q2, along with possible buybacks under its new $500 million buyback authorization, in addition to possible decreases in IEP's net asset value ((NAV)) to arrive at an estimated range for IEP's NAV per unit at June 30.

I concluded "I expect the actual per unit NAV to be below my $14.23 "base case", likely between $13.25 and $14." This turned out to be overoptimistic, as the actual figure was $12.78 and the unit count increased by more than I expected.

In this article, I discuss details of the actual increases in total units outstanding as well as what caused some of the "negative variances," in terms of higher unit count and lower NAV, based largely upon the 10-Q which was filed with the SEC on August 4. I also discuss some other issues about which IEP investors should be aware.

No "At-the-Market" Offerings in Q2

A quite surprising disclosure in the 10-Q was this:

During the three months ended June 30, 2023, we did not sell depositary units pursuant to our Open Market Sale Agreement. During the six months ended June 30, 2023, we sold 3,395,353 depository units pursuant to the Open Market Sale Agreement, resulting in gross proceeds of $175 million

So, almost 3.4 million units sold in Q1 generating $175 million in cash but none in Q2. The Q1 figure was consistent with the average quarterly figures in 2022, when a total of 14.6 million units were sold, or an average of 3.6 million units per quarter. Per page 42 of the 2022 10-K:

During the year ended December 31, 2022, Icahn Enterprises sold 14,619,272 depositary units pursuant to these agreements, resulting in gross proceeds of $759 million.

I had assumed that the "At-the-Market" (ATM) offerings in Q2 were much less than the prior quarters due to the Hindenburg report in early May but I assumed that prior to the report, the ATM offerings would have continued at its normal pace of one million units or more per month. I therefore guesstimated that one million units had been issued in Q2.

These "At-the-Market" offerings boost IEP's per unit NAV as can clearly be seen from the Q1 figures. The 3.4 million units sold, raising $175 million, means they were sold at an average of $51.54, while the per unit NAV at the end of the quarter was only $15.63. Collecting $175 million for units worth only $52.3 million is a "pretty good deal" (to put it mildly) for pre-existing unit holders. Without it, the per-unit NAV would have been at least $.25 lower at March 31, despite the additional shares being issued.

For an unexplained reason, the program was at least temporarily suspended at the beginning of the quarter. This was a month before the Hindenburg report. The program is administered through Jefferies & Co., the only analyst firm on Wall Street which covers IEP.

What made Jefferies and IEP stop then? It's not impossible that either, or both, realized there was likely to be a large decrease in the per unit NAV in the quarter. It is interesting that after IEP released results in early May, Jefferies was still positive IEP then and reiterated its buy recommendation, despite the company having just reported poor Q1 results. However, it did dramatically decrease its price target then, saying this:

Our revised PT [to $43.00 from $70.00] reflects lower cash flows from the underlying business units vs previous forecasts as segments like auto, real estate and home fashion remain under pressure. While parent liquidity to support the current $8/annual dividend remains plentiful ($6.6B available liquidity, of which $1.9B is cash and cash equivalents), we are now assuming the current dividend begins to decline by 10% per annum beginning in 2026 vs maintenance of the current rate in our previous dividend discount model.

It was obvious then that the distribution was not sustainable, despite Jefferies indicating it could stay at its $2 quarterly level through 2025 (and incorrectly refers to it as a dividend rather than a distribution). I was quite vocal in my prior article that it needed to be slashed, likely sooner rather than later. Enough information had previously been disclosed in IEP's financial statements to determine that the MLP units were grossly overvalued in the market. Simply comparing the market price to NAV, along with a quick look at the company's recent track record and seeing that the long investment portfolio largely consisted of staid old-line companies which was then hedged with a large short portfolio made the likelihood of any investment home runs extremely unlikely at best.

Carl Icahn and the founder of Jefferies had a long relationship going back to Icahn's corporate raider days in the 1980's. It should also be noted that Icahn helped bail out Jefferies & Co. during the great financial crisis, and according to the FT, Jefferies has given IEP "50 buy recommendations in a row" since 2013, which I don't think was hyperbole.

It is also interesting that the front page of the June 30 10-Q filed last Friday stated: " As of August 3, 2023 , there were 393,458,414 of Icahn Enterprises' depositary units outstanding. " This is the same figure as the one reported on the June 30 balance sheet in the same filing. This means the ATM offering program had not yet restarted as of August 3.

I have sometimes wondered why Hindenburg released its report when it did. Shorting stocks successfully requires a timing catalyst. I wonder if Hindenburg had noticed that the ATM offerings had been suspended as of April 1. This would have indicated something might be up and would have been a possible catalyst. It would be quite interesting to hear an official rationale for the ATM suspension then.

Total Units Outstanding at June 30 Were Higher Than I Expected

In my prior article, I had calculated that 392,230,976 units were outstanding at June 30 based upon the following from a filing by Carl Icahn on July 5 :

The Reporting Persons may be deemed to beneficially own, in the aggregate, 334,494,577 Depositary Units, representing approximately 85.28% of the Issuer's outstanding Depositary Units (based upon: (i) the 369,197,424 Depositary Units stated to be outstanding as of May 9, 2023 by the Issuer in the Issuer's Form 10-Q filing filed with the Securities and Exchange Commission on May 10, 2023; plus (ii) the 23,016,917 Depositary Units issued to the Reporting Persons by the Issuer on June 30, 2023 in connection with a regular quarterly distribution of Depositary Units by the Issuer).

This seemed to be a "no-brainer" extremely simple calculation (334,494,577/.8528), but then IEP reported in its 10-Q that 393,454,198 units were actually outstanding as of June 30, a difference of 1,224,198 units. The only way this could have been possible would have been if Icahn hadn't included the additional units also issued to outside IEP unit holders on June 30. In fact, if you read the fine print above, the disclosure simply stated that the calculation was based upon units outstanding on May 9 plus the units Icahn received on June 30; no mention of the units issued to others on June 30.

This does not result in a material percentage difference in units outstanding, , but the 1.2 million additional units were material when I tried to reconcile what I thought was the total unit count at June 30. I stated in the article (referencing non-Icahn additions) that " With a net increase of only 766,000, this means IEP likely bought back a considerable number of shares, at least 1.25 million and possibly more than double that. "

In fact, the increase in units owned by others was not about 766,000 units, but instead was over 1.2 million units higher, and there were no buybacks. It is interesting that these 1.2 million shares were almost exactly equal to the 1.25 million shares I was trying to find/reconcile to and had assumed must have been due to buybacks.

Although 1.2 million units, one way or the other, out of almost 400 million, may be considered a minor detail, anyone who wants to do a model for IEP's NAV at September 30 will have to take into account that Icahn's filing for the September 27 distribution will likely not include the additional units issued to outside investors on that date. Not understanding the details of Icahn's June 30 disclosure had actually caused me to make a completely incorrect assumption in my prior article about whether IEP had made any buybacks under its recent $500 million authorization.

The "Nitty-Gritty": Unit Count increases in Q2

I have created the following table, which shows the increase in units owned by both Icahn and the outside investors as a result of the two distribution reinvestments which occurred during the quarter. The figures in bold were the ones reported in the 10-Q's and Icahn's recent 13-D/A filings (" General Statement of Acquisition of Beneficial Ownership-amendment" ), while the non-bolded ones were the result of a bit of math utilizing the bolded figures. (Sudoku anyone?)

Unit Growth-Most Recent Quarter (Company SEC filings and Author Calculations)

{kind=link}

In addition to seeing that 36.5 million units were added during the quarter, over a 10% increase, the table provides a few other insights.

First, we know that Icahn's ownership of almost 300 million units when the first quarter distribution was announced means he received a distribution equal to almost $600 million. He reinvested these distributions and received almost 11.5 million shares as a result, meaning the average price was about $52.26, consistent with IEP's market price at the time. He then received over 23 million units on June 30 with the distribution from his 311.5 million units, meaning the average price was $27.06, consistent with the much lower market price then. Investors should focus on the increasingly dilutive impact the lower market price has on the company; Icahn received double the shares on June 30 that he had received on April 19.

This information also provides insights as to the proportion of IEP's outside investors who are reinvesting their distributions. The almost 57 million units owned by others at March 31, gave them a distribution of $114 million. The almost 750,000-unit addition, at $52.26 each, means that about $39.2 million (34.4%) was reinvested, with the remaining $75 million (65.6%) being paid out in cash.

On 6/30, the holders of the 57.7 million units then were entitled to about $115.4 million. With 1.244 million additional units being issued at $27.06, this means about $33.7 million (29.2%) was reinvested, while the remaining $81.1 million (70.8%) was paid out in cash. Despite the much lower price per unit for the second payment, a higher percentage of unit holders decided to take their distributions in cash rather than additional units. I do not believe IEP explicitly discloses anywhere the exact number of outside investor units which are reinvested on each distribution date, and I believe providing recent reinvestment figures and particularly a methodology for future ones, is of material benefit to anyone trying to evaluate IEP as an investment.

This means that even with halving of the distribution in the current quarter, the payment will be around $45 million to outside investors, which decreases total NAV as well as NAV per unit. There was a comment in the conference call that Icahn will be taking some of his distribution in cash also. If he takes 50% in cash, this would be another $167 million. These two amounts, at over $200 million, would reduce IEP's NAV from $5 billion to less than $4.8 billion. This total figure is one which IEP's and Icahn's creditors focus on.

The remaining unit count would still increase materially with IEP now trading at well under $25. Even at $25, Icahn would receive about 6.7 million additional units (or 13.4 million units if he instead decides to again take all his payments in units) and the other holders a few hundred thousand more, bringing the total to more than 401 million.

As a result, under this scenario, if IEP does not have any "NAV earnings," NAV per unit will decrease this quarter to less than $12 ($4.8 billion NAV /401 million units). For NAV to remain at $12.78, "NAV earnings" would need to be about $.80 per unit, or a total of about $320 million. Earning $320 million in one quarter on a $5 billion (or less) NAV equity base is highly unlikely on an ongoing basis, although possible in occasional quarters.

IEP's Shrinking Asset Base

There seems to be faith among some investors that Carl Icahn will "get his mojo back" and he still may hit some investment "home runs". Part of what is overlooked is that IEP's asset size (and equity base) has decreased dramatically over the past decade. Therefore, even if IEP does make some great investments, it won't make up for the huge losses it has incurred.

No one has examined this issue in detail as far as I am aware. I may do so at some time in the future, but in the meantime, I think it's worthwhile to take a brief look at a portion of IEP's assets, its securities portfolio and the changes in it over the past six months, as reported on page 16 of the June 30, 2023 10-Q:

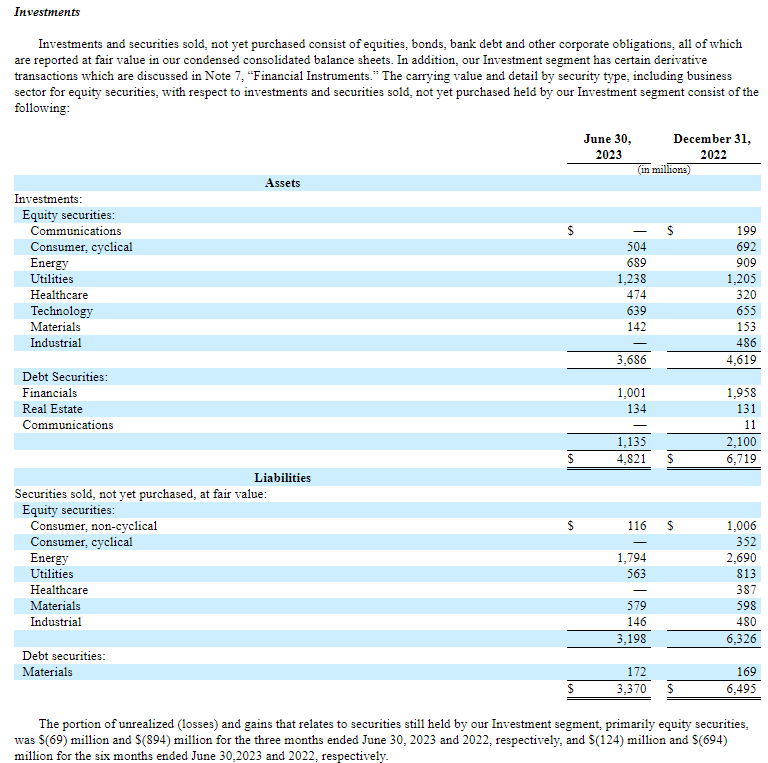

Icahn Enterprises -Long and Short Securities Positions (IEP June 30 SEC Filing)

{kind=link}

The first item to notice is the section labeled " Liabilities-Securities Sold not Yet Purchased, at Fair Value " This is the bulk of IEP's short portfolio, although there are also some derivatives listed separately which might be considered short (or long) positions. IEP has correctly represented that it has scaled back its short portfolio considerably, with it decreasing by almost 50% in the past six months, from $6.5 billion to $3.4 billion. Some investors seem to have misinterpreted Icahn's comments to mean it has totally eliminated its short portfolio, however.

What the company has not emphasized, however, is that it has scaled back its long securities portfolio considerably as well, by about $1.9 billion. The decrease in both the long and short portfolio was likely necessitated by its decreasing equity base. However, as the short portfolio has decreased more than the long portfolio, it is now net long by about $1.4 billion whereas it had been almost net neutral at December 31, 2022.

Although the above table does not list specific securities, they are grouped by industry and IEP is both long and short in the same industry groups. This is the classic definition of a hedge fund, where stable returns take precedence over less stable but potentially outsized returns. This makes it even harder to see how IEP might hit a home run anytime soon.

Looking at "Energy" is particularly enlightening. It shows a long position of $689 million and a short position of $1.794 billion, or a net "Energy" short position of $1.105 billion. This doesn't tell the whole story though, as CVR Energy( CVI ) is listed as an investment rather than a security, and the market value of its investment on June 30 was $2.133 billion per the NAV reported in its August 4 earnings press release. As a result, I would consider its gross Energy long position to be $2.822 billion, and its net position, after subtracting the $1.794 billion short, to be $1.028 billion, so only a bit over 1/3 net long in the sector. The only way outsize returns can be achieved is if IEP's long positions go up and the short positions in the same industry go down. Call me skeptical.

Carl Icahn's Rededication to Activism

On August 4, Icahn Enterprises issued its earnings press release and then another one a few minutes later. In the earnings release , the company stated:

Subsequent to the quarter, I have entered into a three-year term loan agreement with my personal lenders (see Form 8-K filed on July 10, 2023) which in my opinion has significantly diffused the effects of the misleading Hindenburg report, and focused on our activist strategy and reduced our hedge book. These actions have been a major factor in what I believe is IEP turning the corner in July. In the month of July, our publicly traded securities, which are included in our indicative net asset value, experienced over a $500 million increase in value, net of all hedge positions .

Shortly after issuing its earnings press, IEP issued another press release stating:

we have reset our focus on our core activism strategy. We have long believed that activism is the best investment paradigm."

In the last few days, two of IEP's activist targets have reported much worse than expected results and the stock prices have tanked.

One was International Flavors and Fragrances ( IFF ). In February, Carl Icahn reached a settlement agreement with IFF with one new board member being appointed per the Wall Street Journal . IFF's stock price was about $110 then. On August 7, IFF reported substantial misses on revenue as well as earnings and revised downward its guidance. The following day, IFF decreased by $15.56, to $64.78, a plunge of over 19%. IFF closed at $77.83 on June 30, so it is now hurting rather than helping IEP's NAV in the current quarter.

Then, on August 9, Illumina ( ILMN ), another Icahn activist target where he had recently obtained a board seat, reported worse than expected results and the stock dropped a few percent after-hours, although it now seems to have bounced back.

In fact, the entire S&P was up by almost 3% in July, and down by almost as much in the first 9 days of August. As a result, much of IEP's $500 million NAV gain in July has likely evaporated in the past week or so.

Icahn's activist strategy does not work well if the potential fundamentals are not great. In any case, if any IEP investors think there is hidden value in any of its portfolio companies, buy the individual stocks at their current market prices, not IEP at more than twice the market price of the underlying assets.

Summary

My negativity regarding Icahn Enterprises primarily relates to a valuation call. It is trading at more than two times its NAV, a reasonable benchmark for intrinsic value, particularly with most of IEP's assets consisting of publicly traded securities. Many IEP investors have focused on an unsustainable quarterly distribution rather than the fundamentals. Others have unrealistic hopes that the company will be able to achieve truly outsize investment returns in the near future, justifying paying two times NAV.

Eventually, the fundamentals will rule (as they have begun to). If anyone desires to become/remain an IEP investor, I would suggest that, at a minimum, all distributions be taken in cash rather than additional units. I still think such investors may be playing a "game of chicken" in advance of the next likely distribution cut.

Finally, at the risk of being quite repetitive, if you wish to invest alongside "legendary investor Carl Icahn" buy individual stocks in his portfolio at par rather than IEP at twice the price. I have done so; I have a long position in CVR Partners ( UAN ), a fertilizer manufacturer in which IEP has an indirect investment.

For further details see:

Icahn Enterprises LP: An Update On Its Ballooning Unit Count