ICL - ICL Group: Cheap Valuation Given The Market Opportunities

2023-09-26 06:10:26 ET

Summary

- ICL Group is a well-diversified company that serves various industries, including agriculture and industrial manufacturing.

- The company holds a 20% market share in the phosphate solutions market, which is expected to experience steady growth.

- Despite technical indicators not favoring a buy, ICL offers a solid dividend and potential for future growth, making it a favorable investment option.

The fertilizer market is quite a lucrative one that is heavily driven by market trends and how inventory levels are looking for farmers. In particularly tough years of farming and planting, the necessity of fertilizers is more broadly essential. In times when the weather and climate are more forgiving, it's less widely used. Over the long term, though, this quite often balances out. ICL Group Ltd (ICL) is a very well-diversified company that serves a broad set of markets. The company has been moving into industrial products as a bromine supplier but also into battery solutions being a phosphate solutions provider. ICL has managed to gather up a 20% market share here and right now offers a fantastic broad and diverse investment opportunity. The shares seem cheap at a mere 10x earnings multiple. ICL gets a buy from me.

Operational Overview

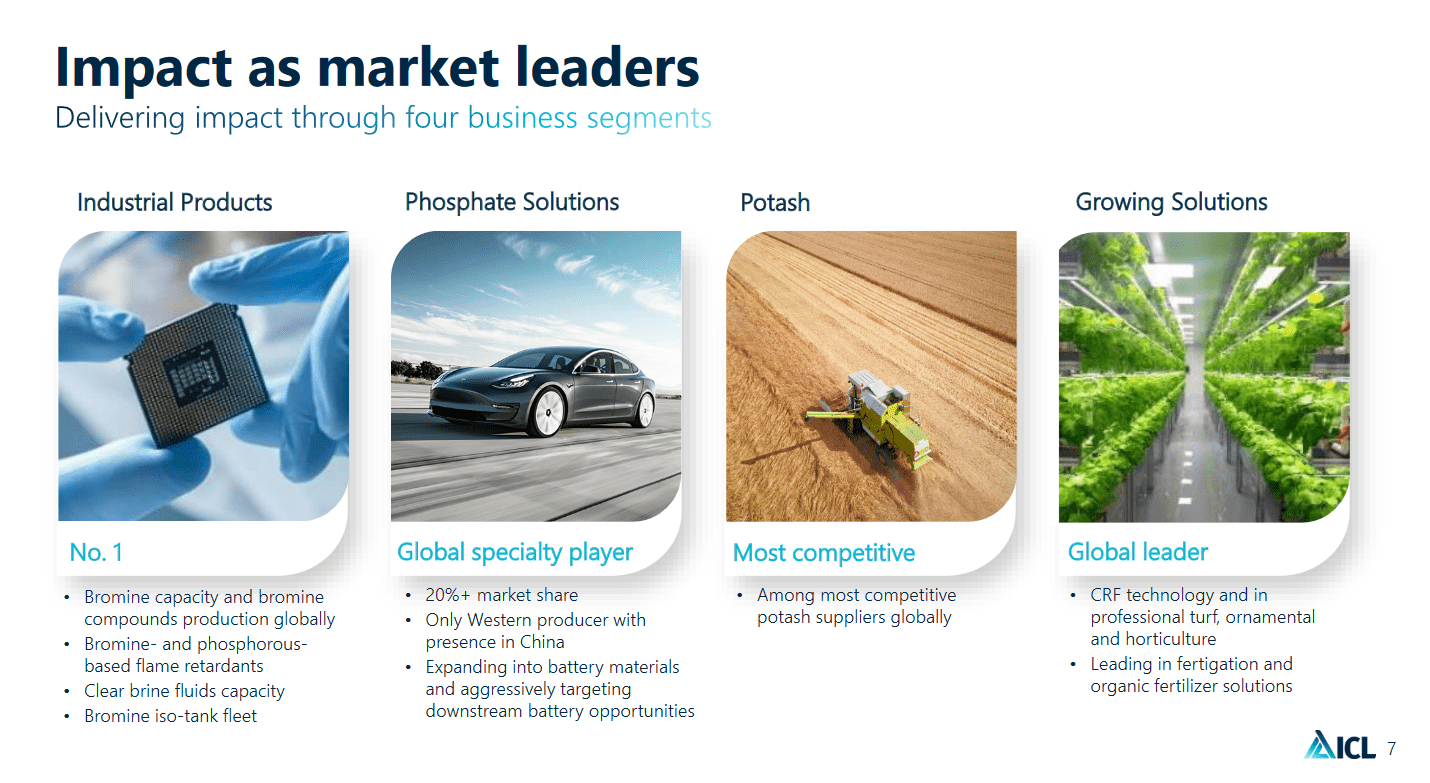

Established in 1968 and headquartered in Tel Aviv, Israel, ICL is a renowned global company specializing in minerals and chemicals. ICL operates across four key segments, which include Industrial Products, Potash, Phosphate Solutions, and Innovative Ag Solutions. The company's diversified portfolio encompasses a wide array of products and solutions tailored to meet the unique needs of various industries, ranging from agriculture to industrial manufacturing.

Market Overview (Investor Presentation)

{kind=link}

As we have discussed, ICL has managed to become a leader in several spaces that it operates in right now. The phosphate solutions for example hold a 20% market share right now. The phosphate market is expected to generate steady growth for the coming years at a CAGR of 3.2% in total.

Technicals

{kind=link}

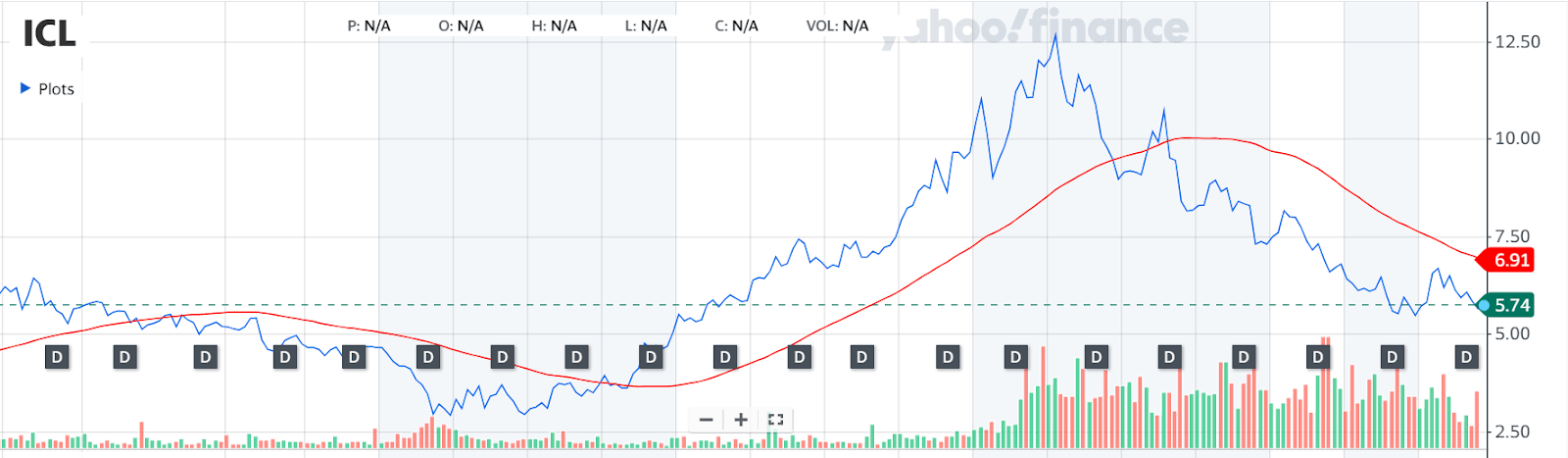

The technicals for ICL don't go in the favor of a buy, unfortunately. I like to include these but don't solely rely on them for an investment. If we look back to when ICL last crossed the redline, which is the moving average, then it neutered into a massive bull run, and inversely, once it went below it quite rapidly saw a decrease in the share price. I think the market is right now going to enter a phase of consolidation. But once demand starts to pick up once again, the share price could potentially reach above the moving average and enter into another bull run. I like the risk/reward profile of that as I believe in the fundamental demand for the several end markets that ICL serves.

{kind=link}

Taking a look at the RSI of ICL as well it sits around 42 right now. This is around the same as when the company last moved above the moving average. However, the bull run began at an RSI of roughly 15 in September 2020. Should we see similar levels I think that ICL would potentially move up to be a strong buy rather than just a buy.

Dividend Summary (Investor Presentation)

Besides, ICL right now also has a solid dividend at over 10% and a payout ratio that doesn't even go above 50%. That is a decent place to be in and I would estimate that even if the share price consolidates or stagnates, the value you get from the dividend makes up for quite a lot of that.

Comparison To Intrepid Potash Inc

{kind=link}

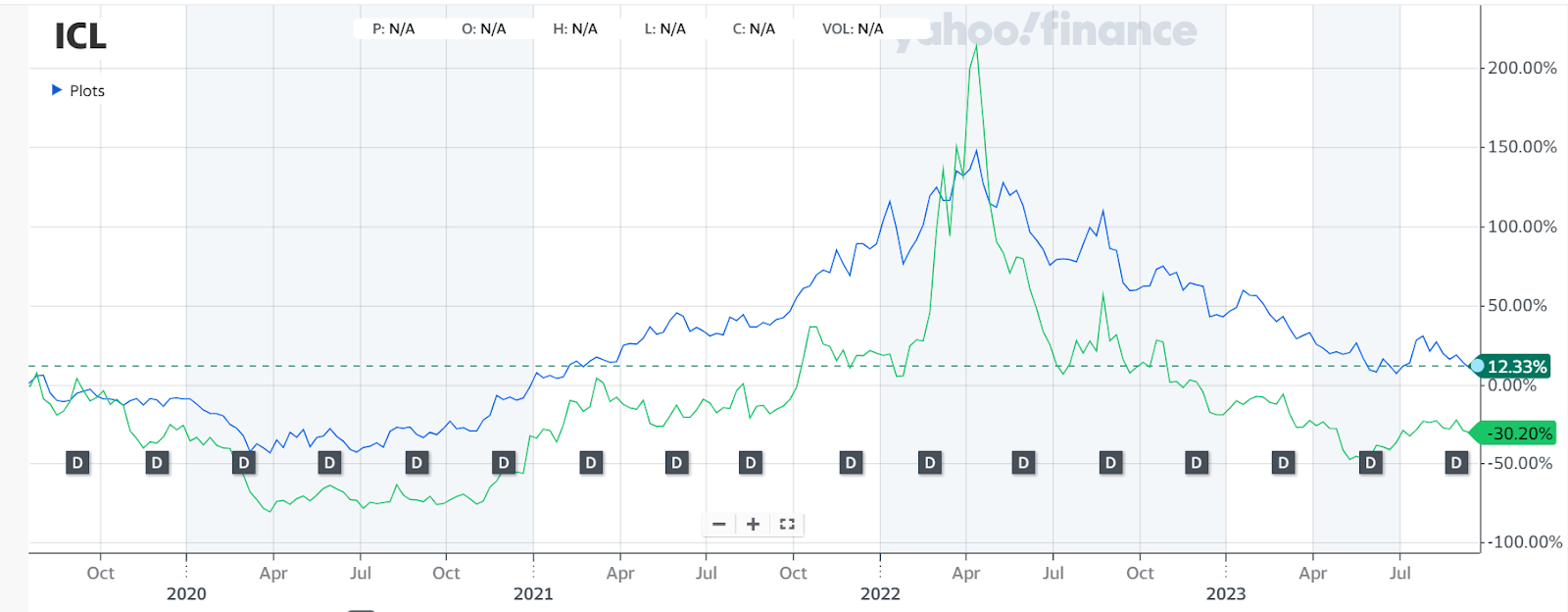

Seeing as a large portion of ICL revenues comes from potash, nearly 30% from the last quarter, comparing it to another pureplay potash company seems fair. On the chart above we can see that at one point Intrepid Potash Inc (IPI) managed to outperform ICL by quite a bit. However, since then, the return has been far worse for IPI.

Business Segments (Investor Presentation)

What has helped yield a more stable development to the sales price for ICL I think is the diversified set of revenues the company has. In times of less favorable potash prices, it's easier to rely on other sources instead. They both quite clearly showcase that they have traded at a similar pattern. But for the investors that would prefer a more stable dividend-yielding company the ICL looks like the best option, which is why I will be preferring them over IPI right now.

Assessing The Value

Perhaps one of the more important parts of this article, assessing the value of ICL right now. As I have a buy rating on them, I, of course, see them as favorable values to invest in.

P/E (Seeking Alpha)

First out is the p/e, which is at 9.9 FWD. The rapid increase from the TTM comes from the decrease in potash prices and from less activity and volumes in the markets. This still doesn't discourage a buy and makes me still bullish on the outlooks.

p/fcf (Seeking Alpha)

Supporting the dividend is strong cash flows for ICL, which right now has a multiple of 4.3. The TTM FCF is at $987 million, sufficient to cover almost the entire dividend on its own. Combining the two discounts of 30% and 41% we get an average of 35% which is also the upside I see the share price offering in the short to medium term right now. A sufficient upside potential that a buy rating is fitting in my opinion.

Risks

ICL thrives in a cyclical industry, and its growth prospects are closely intertwined with the fluctuations in commodity prices, particularly phosphates and potash. In the year 2022, the company experienced notable success, propelled by soaring potash prices. Any adverse shifts in these crucial commodity prices have the potential to impact the overall value of ICL. The general rule with commodity companies is that would buy when the valuation looks sky-high and sell when they're cheap. That is usually a good indication of when a company is making a strong amount of profit and when they are instead seeing compressing margins. However, I think that ICL is an expectation given the diversified nature of the business. For a pure copper company, for example, that methodology would work, but not here. The price looks cheap and any inherent risks with volatile commodity prices aren't sufficient to suppress the buy thesis.

Potash Prices (Ycharts)

Given the global reach of the company, it remains susceptible to the vagaries of foreign exchange rate fluctuations. Consequently, the business has been adversely affected by the strengthening of the USD. However, it's essential to note that in the future, as the USD potentially weakens in comparison to other currencies, this could yield a positive impact on the firm's overall value. The USD has grown a lot stronger in the last 12 months, which I think comes from the rising interest rates in the country, making it more appealing to hold capital in USD right now. I don't think interest rates are going to be sticking around this high forever, so neglecting a buy case based on a high USD exchange rate seems unjustified.

Last Pointers

The potash market may have seen a lot of volatility lately, but with the inherent diversified nature of ICL, I think that they offer a favorable risk/reward opportunity right now. The yield is high at around 10% and my estimates suggest an immediate upside potential of 35% should the market value of ICL be the same as the rest of the sector. ICL gets a buy from me.

For further details see:

ICL Group: Cheap Valuation Given The Market Opportunities