SMG - ICL's Growth Momentum Could Stall In 2023 Amidst Challenging Market Conditions

Summary

- ICL had an excellent 2022 due to a $74 increase in potash price per ton. However, the company has provided lower guidance for 2023 due to the global slowdown.

- The company faces uncertain geopolitical situations, supply chain disruptions and higher inflation which can impact its value going forward.

- Despite the correction in P/E multiple from 9x in September 2022 to 4.5x, the company does not trade at discount due to challenging growth outlook.

Investment Hypothesis

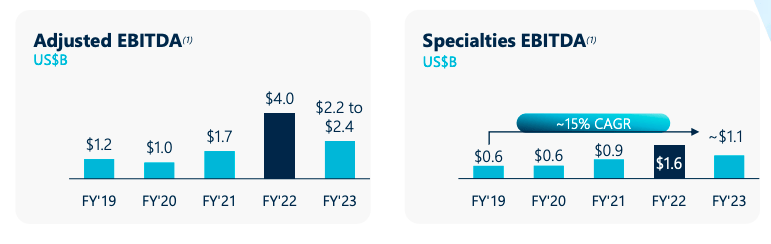

Despite an excellent year in 2022 due to a $74 increase in potash prices per ton and higher selling prices of speciality products and phosphates, it is unlikely that ICL Group Ltd (ICL) can continue this momentum in 2023. Further, the company has lowered its EBITDA guidance for 2023 to $2.2 to $2.4 billion against $4 billion in 2022.

As ICL operates in a cyclical industry, much of its value comes from the movement of commodity prices. As commodity prices will come down with easing inflation, ICL's selling prices will also come down but will get offset by higher volume. Therefore, the net effect on value will depend on an increase in volume against the price decrease.

Due to uncertain macroeconomic conditions and supply chain disruptions, the company's growth will halt in 2023 after spectacular 2021 and 2022. However, the company has a good product mix and has invested in new facilities for growth. Thus, at the current price, the company is valued fairly. Thus, investors with ICL shares in the portfolio can continue to hold. However, new investors should wait until Q1 2023 results before adding them to their portfolios.

About ICL Group

ICL Group Ltd , founded in 1968 and headquartered in Tel Aviv, Israel, is a global speciality minerals and chemicals company operating in four segments - Industrial Products, Potash, Phosphate Solutions and Innovative Ag Solutions. The company changed its name to ICL Group from Israel Chemicals Ltd in May 2020. As of 2023, the company has 12,500 employees. The company has a vertically integrated business model . It is involved in the mining, processing and marketing minerals and chemicals, which allows the company to control the entire value chain from raw material sourcing to distribution.

{kind=link}

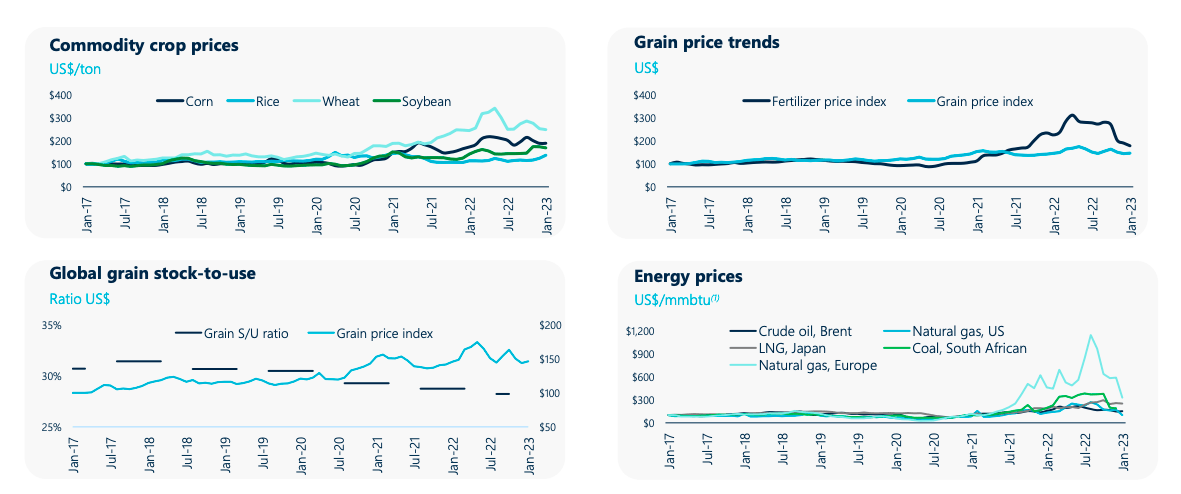

As the company operates in a volatile commodity segment, it is impacted by macroeconomic and geopolitical conditions. For instance, the Russia-Ukraine war increased fertilizer prices resulting in the lowest gray stock-to-use ratio in 2022, which is forecasted to remain low in 2023. Further, due to the war , there was a 5% decline in global fertilizer consumption in 2022. However, due to the rising concern over the global food crisis , fertilizer volumes will go up in 2023 due to higher consumption. In addition, due to higher inflation in 2022, resulting in higher interest rates, the buying power of customers in the electronics, housing and automotive segment have declined. As the company operates in these critical industries, the reduction in buying power will impact its revenues in 2023.

According to the company, the re-opening of China after the zero covid policy will improve its business momentum in 2023. Further, a higher focus on ESG-related spending and the electric vehicles revolution, where countries are spending massively on mobility transformation technologies, will augur well for the company in 2023. The company also observes improvement in supply chain issues in 2023, which can reduce input costs.

In the last year, the company has made significant investments to expand its capacity. For instance, on January 25th 2023, the company announced investing $400 million to build a lithium iron phosphate materials plant in St. Louis. The plant will become operational in 2024 and produce LFP material for the global lithium battery industry. In addition, on January 11th 2023, the company signed a long-term agreement with General Mills to supply phosphate and provide related solutions to North America with the potential for international expansion.

According to Phil Brown , president of ICL Phosphate Specialties and managing director of North America for ICL.

Our focus is always on the customer and on delivering best-in-class products, quality and service. We're pleased General Mills appreciates our efforts and is also dedicated to providing best-in-class products to their customers. We're looking forward to working with their R&D team to find new ways to support their product development and are excited to turn to our global innovation team for support.

The company launched ICLeaf - A diagnostic tool to help farmers maximize yield in India. The tool is available for India's grape, cotton, banana, tomato and pomegranate crops. It will help farmers plan for optimum nutrient management by identifying deficiencies that will help them improve yields and increase sales.

According to Elad Aharonson , president of Growing Solutions for ICL.

As a company focused on creating impactful solutions for humanity's sustainability challenges in the global food, agriculture and industrial markets, we are proud to introduce our new and advanced Israeli technology, which will help farmers gain greater visibility into their fields and maximize yields.

The company also entered into a long-term supply deal with India Potash for the supply of organic polysulphate till 2026 for an aggregate amount of 1 million metric tonnes, and each shipment containing a minimum of 25,000 tons. The prices and payment terms are fixed between Indian Potash and ICL from time to time.

In 2022, the company also invested in startups and partnerships. For instance, in May 2022, it teamed up with startup accelerator StartLife to develop the next generation of crop nutrition and food tech startups.

According to Hadar Sutovsky , vice president of External Innovation at ICL Group.

ICL Planet Startup Hub seeks to establish a new generation of plant nutrition solutions, and we aim to invest in startups which can make a meaningful difference.

ICL has invested $10 million in Evogen , a developer of life-science-based products. The amount will get invested in Lavine Bio, which develops microbiome-based products for use in the food and agriculture industry. The partnership aims to develop bio-stimulant products to improve the efficiency of fertilizers.

According to Elad Aharonson , president of Growing Solutions for ICL.

ICL is committed to creating impactful solutions for humanity's sustainability challenges in the global food, agriculture and industrial markets. This collaboration with Lavie Bio resonates with our sustainability goals and values. The collaboration demonstrates ICL's commitment to bringing to market new, sustainable technologies for our customers. It also provides a strong platform to enter the ag-biologicals market, which we see as highly complementary to our existing agriculture business. Following an extensive evaluation of Lavie Bio's technical capabilities, we enthusiastically look forward to collaborating with them to bring much-needed novel ag-biological products to the global market.

{kind=link}

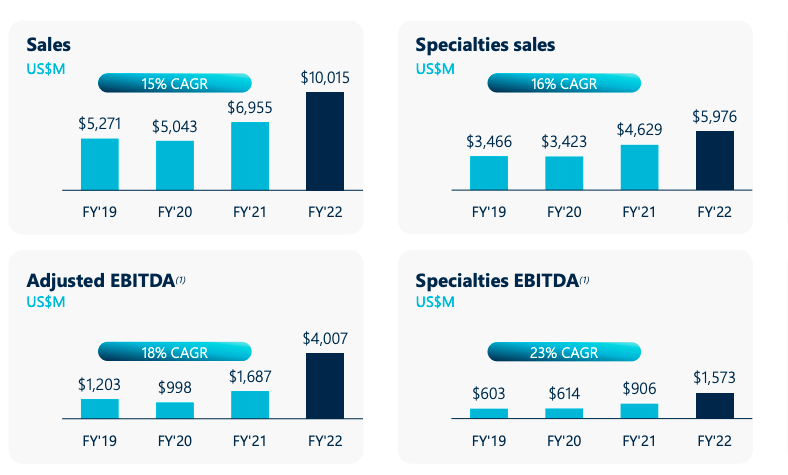

ICL reported its Q4 2022 and 2022 annual results on February 15th 2023, where the company reported $10 billion in revenues, an increase of 44% against 2021. Further, it reported an annual operating income of $3.5 billion in 2022, 194% more than in 2021, with $4 billion in adj.EBITDA at 40% EBITDA margin.

{kind=link}

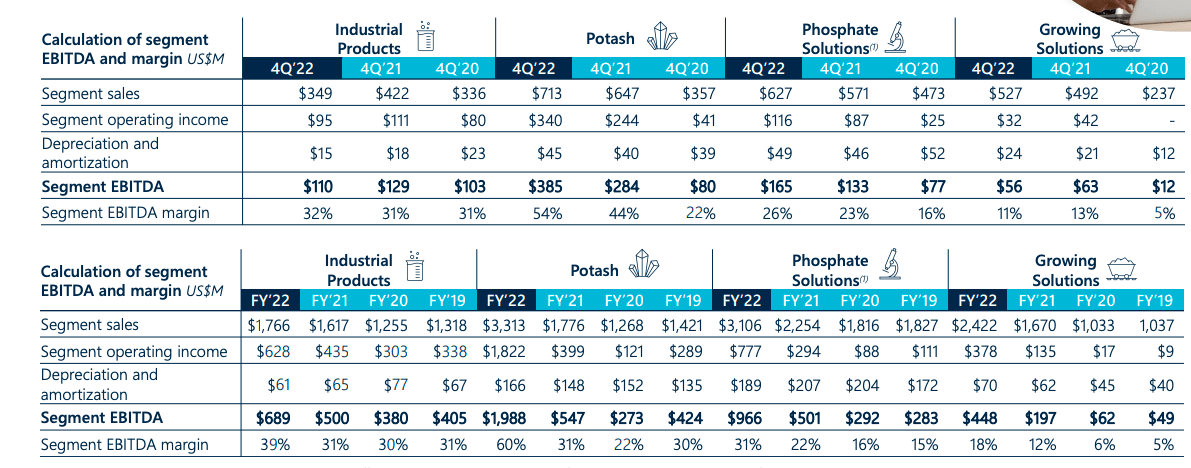

In Q4 2022, the company reported $2.09 billion in revenues, a 2.5% growth year on year, with adjusted EBITDA of $698 million at a 33% EBITDA margin.

{kind=link}

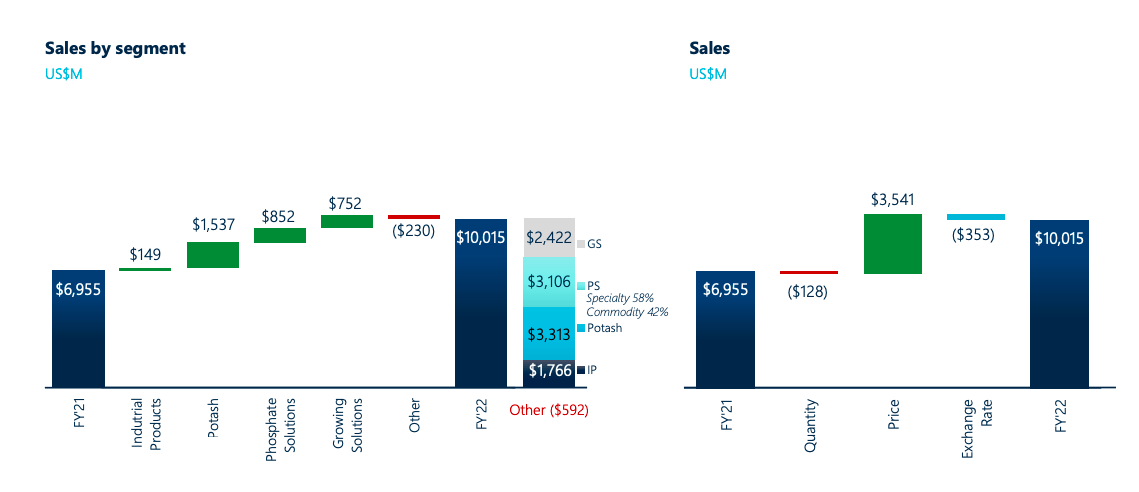

Revenues from potash doubled in 2022 from $1.7 billion to $3.3 billion, and EBITDA tripled from $547 million in 2021 to $1.98 billion in 2022, generating a 60% EBITDA margin due to a $74 increase in potash price per ton YoY. In addition, all the other segments - Industrial products, Phosphate solutions and Growing solutions witnessed an improvement in revenues and EBITDA due to higher selling prices.

In the fourth quarter, the company's production increased by 36,000 tonnes over the last year due to operational improvements implemented at ICL Dead sea and ICL Liberia. However, the companies sold 79,000 tonnes in potash lesser than last year due to lower sales volumes in Brazil and Asia despite the higher sales in India, Europe and the US.

According to Raviv Zoller , president and CEO of ICL.

ICL delivered record sales of more than $10 billion and EBITDA of more than $4 billion for 2022, and this amount exceeded our guidance, which we raised each quarter. As expected, we saw a return to more traditional seasonality in the fourth quarter. Throughout the year, we navigated global uncertainty, supply chain challenges, and cost inflation while simultaneously focusing on operating efficiency and productivity, introducing new innovative products, and delivering value to all stakeholders.

{kind=link}

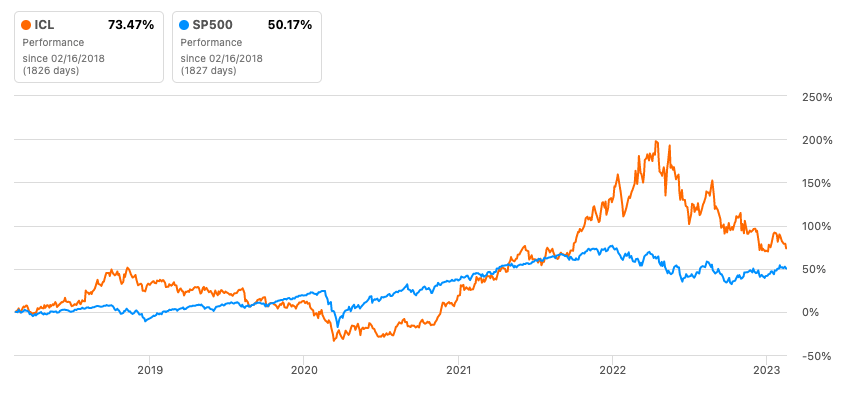

In the last five years, ICL gave a return of 73.47% which is better than the S&P500 index. However, in the last year, the company's returns declined by 28.7% against the S&P 500's decline of 6.88%, primarily due to higher inflation resulting in higher volatility in the commodity costs and geopolitical issues like the Russia-Ukraine war and Covid lockdown in China.

Author Calculations

The last two years were excellent for the company reporting revenue growth of 38% and 44%. In the last five years, ICL grew at 13.1% CAGR.

Author Calculations

In the last two years, the company reported an improvement in gross margin, EBIT margin and Net margin, with gross margin expanding to 50.2% in 2022 from 35.1% in 2021 due to higher opportunities in the specialities business, higher economies of scale and improved pricing strategy. In addition, the company's EBIT margin has doubled from 16.8% in 2021 to 35.1% due to consistent cost discipline and improved product mix optimization.

Author Calculations

The company's asset turnover has improved in the last two years, which shows its higher efficiency in using its assets to generate revenues. ICL achieved better asset turnover due to higher production volume, better inventory management and improvement in account receivables collection, and better managing its capital expenditures. As a result, the company improved its asset efficiency to 17.7% in 2022 from 10.3% in 2021, implying its efficiency in using its assets to generate higher profitability.

Author Calculations

The company's day sales outstanding reduced from 60 days in 2021 to 55 days in 2022, implying that it is collecting payments from its customers quickly, resulting in better cash flows and reducing the risk of bad debt. However, the company's cash conversion cycle increased to 115 days in 2022 from 103 days in 2021 due to the Russia-Ukraine war, which resulted in higher input costs and supply chain disruptions.

Author Calculations

The current ratio for ICL has increased from 1.5x in 2021 to 1.7x in 2022, implying that the company has a stronger liquidity position and is better prepared to meet its short-term financial obligations. However, its net working capital margin has improved slightly from 18.9% in 2021 to 19.4% in 2022, primarily due to higher inflation resulting in higher input costs and supply chain disruptions.

Author Calculations

Although the company saw an increase in capital expenditures in 2022 from $611 million to $747 million, its capital expenditure margin has declined from 8.8% to 7.5%. Further, ICL's operating leverage has declined from 6.67 in 2022 to 4.55 in 2021, implying lower operating leverage and less sensitivity in operating income to revenue changes. Thus, the company's risk profile has declined in the last two years.

Author Calculations

Though ICL's debt has decreased from $3 billion in 2021 to $2.82 billion in 2022, its debt-to-capital ratio has increased primarily due to a decline in market cap. Nevertheless, the company has maintained its interest coverage ratio of 10.8x, indicating that it can pay the interest expenses from the operating income.

Author Calculations

The company's ROIC, ROA and ROE have improved dramatically in the last two years. In the last year, the company doubled its ROA, ROIC and ROE, implying that it effectively managed its assets, invested capital wisely and generated substantial profits by reducing costs, increasing prices, and improving revenues and operational efficiency.

Author Calculations

The company's levered free cash flow doubled to $1.27 billion in 2022 from $454 million in 2021, while its free cash flow margin almost doubled from 6.5% in 2021 to 12.8% in 2022, implying that it was able to generate substantial cash after accounting for its capital expenditures and debt obligations. As a result, the company had a fantastic 2022, declaring $1.2 billion in dividends of $1.27 billion in free cash flows.

Outlook for 2023

{kind=link}

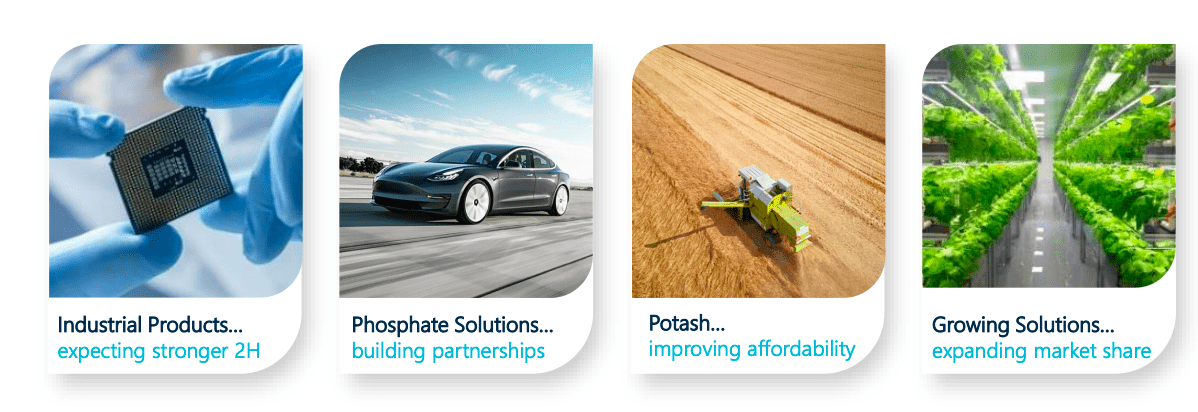

ICL expects stronger 2H 2023 for its Industrial products. The company will leverage its LFP expansion in St. Louis for Phosphate Solutions to build partnerships with leading global automotive OEMs. The company expects improving affordability to benefit farmers and suppliers in the potash business. The company plans to continue growing its market share in the growing solutions.

{kind=link}

The company expects an adjusted EBITDA of $2.2 to $2.4 billion in 2023, a 45% decline against 2022. Further, the EBITDA of specialities business will decline from $1.6 billion in 2023 to $1.1 billion in 2022 due to uncertain political situations, higher inflation and global slowdown.

Risks

ICL operates in a cyclical industry, and much of its growth will depend on the commodity prices of phosphates and potash. The company had a good year in 2022 due to high potash prices. However, commodity prices will ease as inflation decreases, which can increase consumption. Thus, any adverse movement in commodity prices will affect the company's value.

As the company operates globally, it is exposed to foreign exchange fluctuations. As a result, the company faces a negative impact due to the strengthening of the USD, but in the future, as the USD weakens against other currencies, it will positively impact the firm value.

Valuation

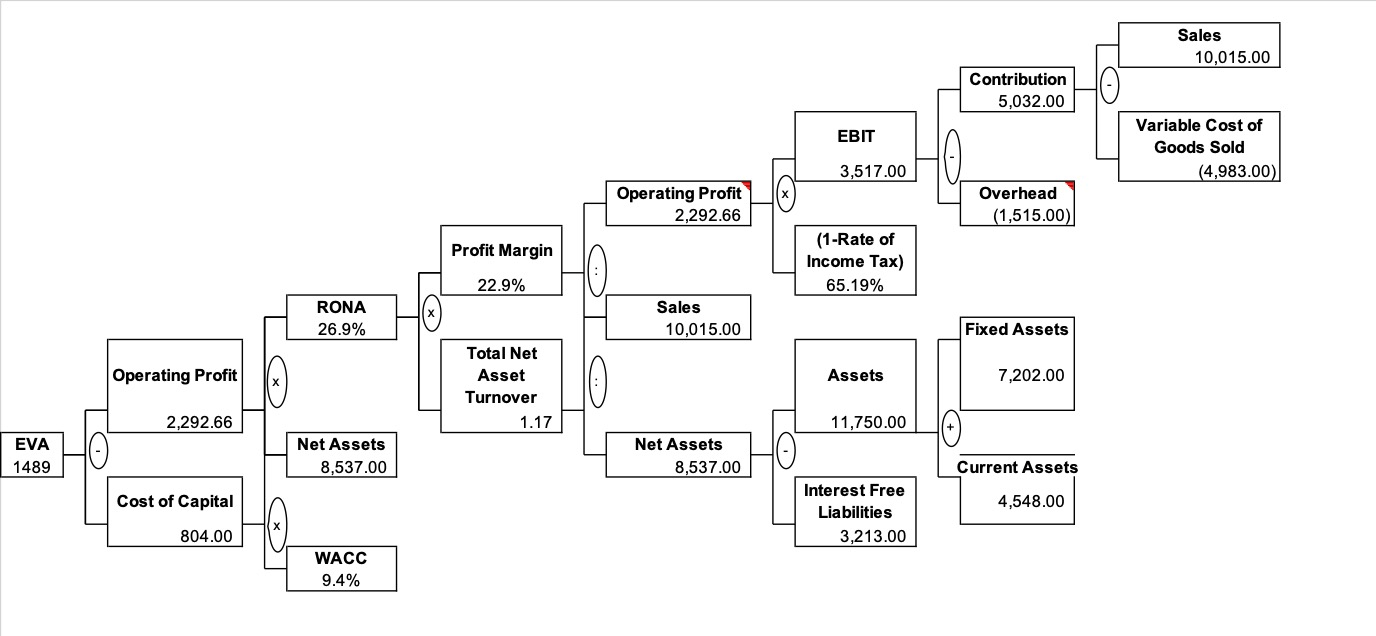

Before valuing ICL using the Discounted Cash Flow approach, I want to examine whether the company generates excess value over the cost of capital. For this, I derive the Economic Value Added for the company to measure its economic profit by deducting the cost of capital from its after-tax operating profit.

{kind=link}

I arrive at EVA of $1.49 billion for ICL, implying that the company is generating $1.49 billion in excess value over the cost of capital.

Author Calculations

ICL's P/E ratio has declined from 22x in 2021 to 4.5x in 2022 despite an improvement in EPS from $0.6 to $1.68 because the market expects its growth rate to slow down next year due to a global slowdown. Further, ICL's profitability depends on global commodity prices. As a result, the company has also lowered its revenue and EBITDA guidance for 2023. Considering all this, it is unsurprising that ICL's P/E multiple has contracted.

Further, I benchmark ICL against its competitors to understand how the company performs against its peers. I identify the following companies for my benchmarking analysis.

- CF Industries Holdings (CF)

- FMC Corporation (FMC)

- The Mosaic Company (MOS)

- The Scotts Miracle-Gro Company (SMG)

{kind=link}

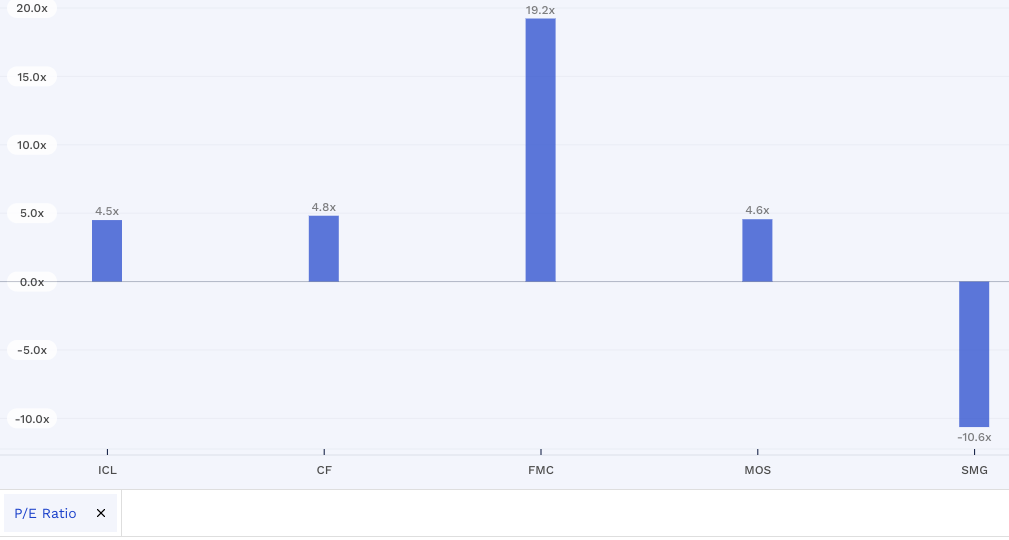

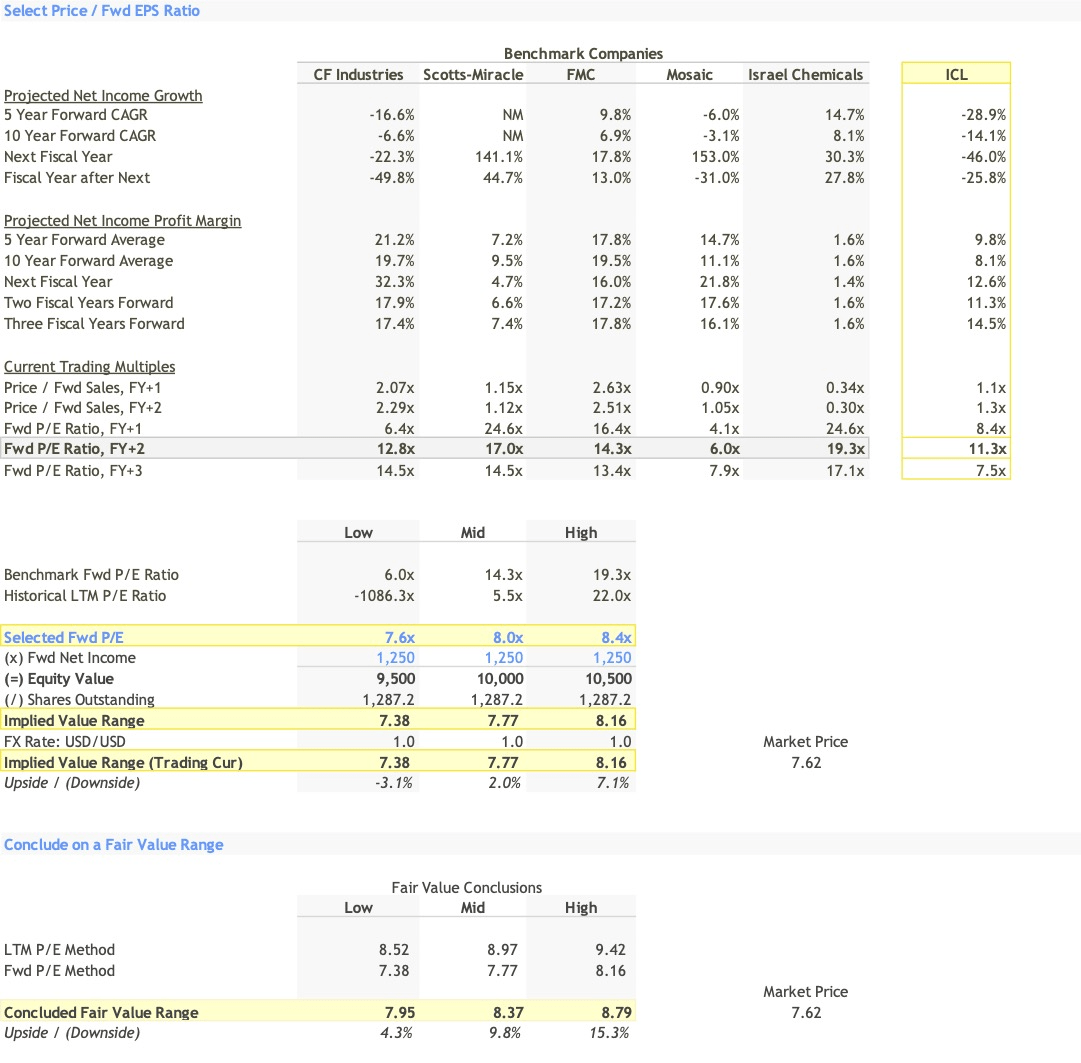

Though the company's P/E multiple has declined in 2023, it trades at the same level as CF Industries and The Mosaic company, which implies that the correction in P/E is more industry-specific and less firm-specific.

{kind=link}

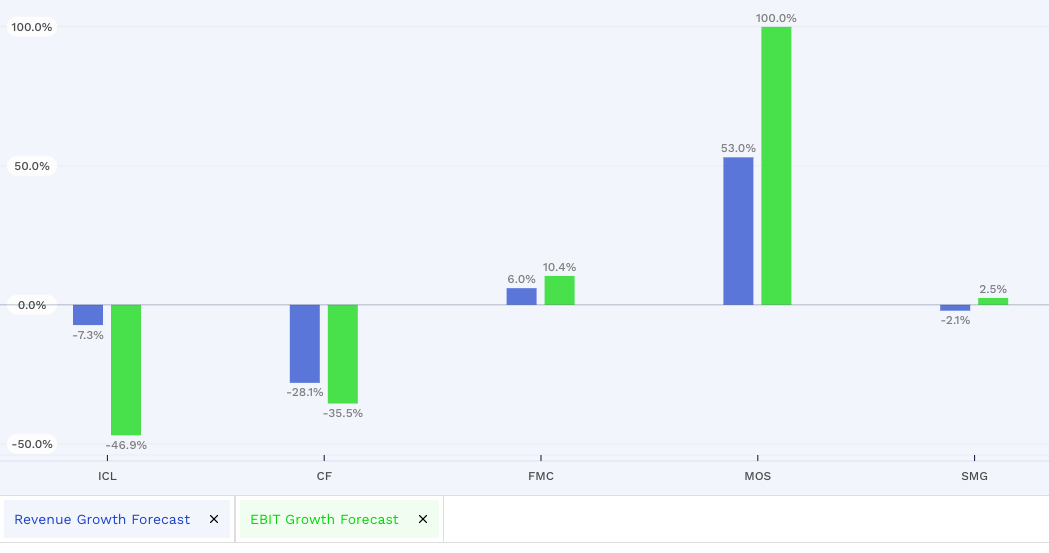

All the companies, except Mosaic company, will have a negative revenue growth rate and EBIT growth projected for 2023. However, due to the challenging macroeconomic conditions in 2023, the P/E ratio of all these companies has been corrected.

{kind=link}

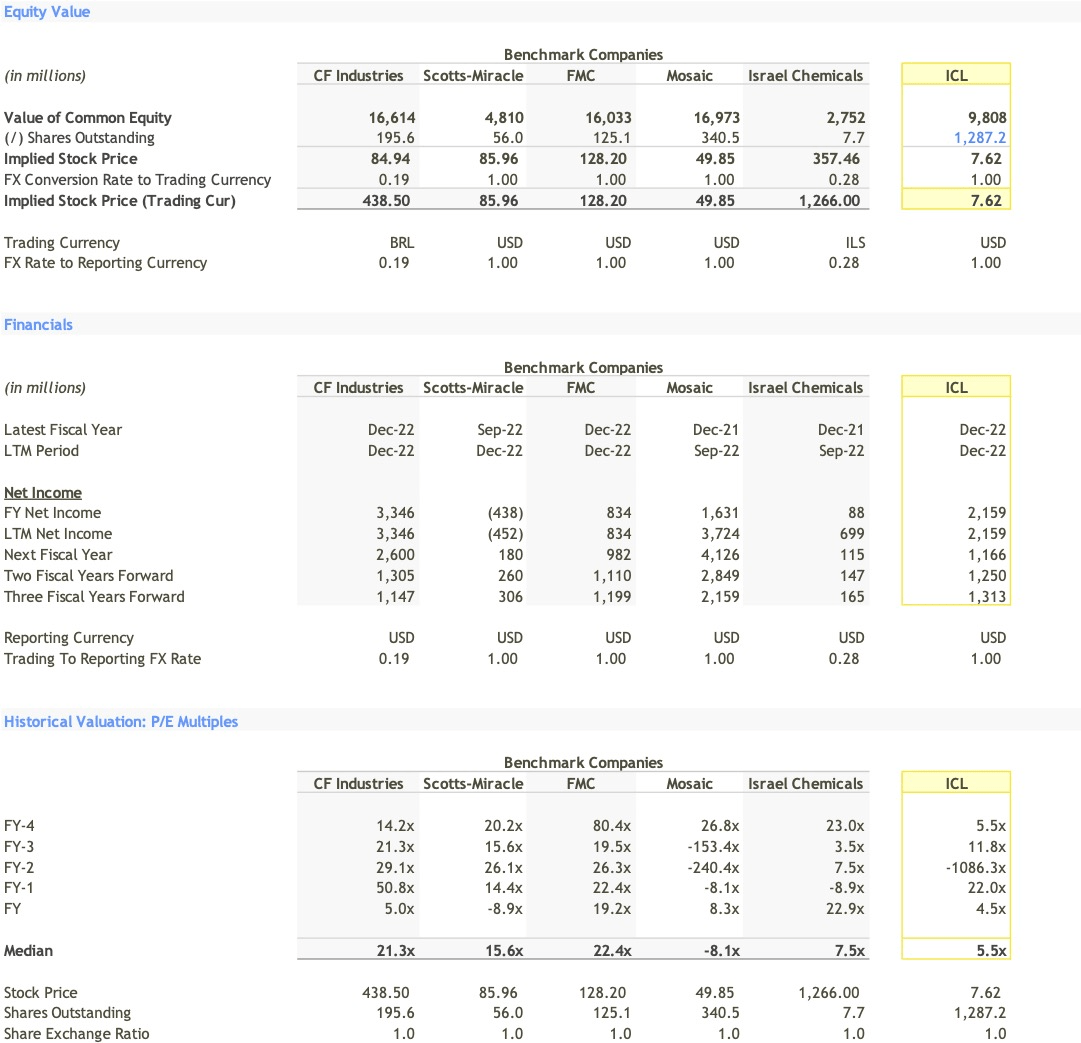

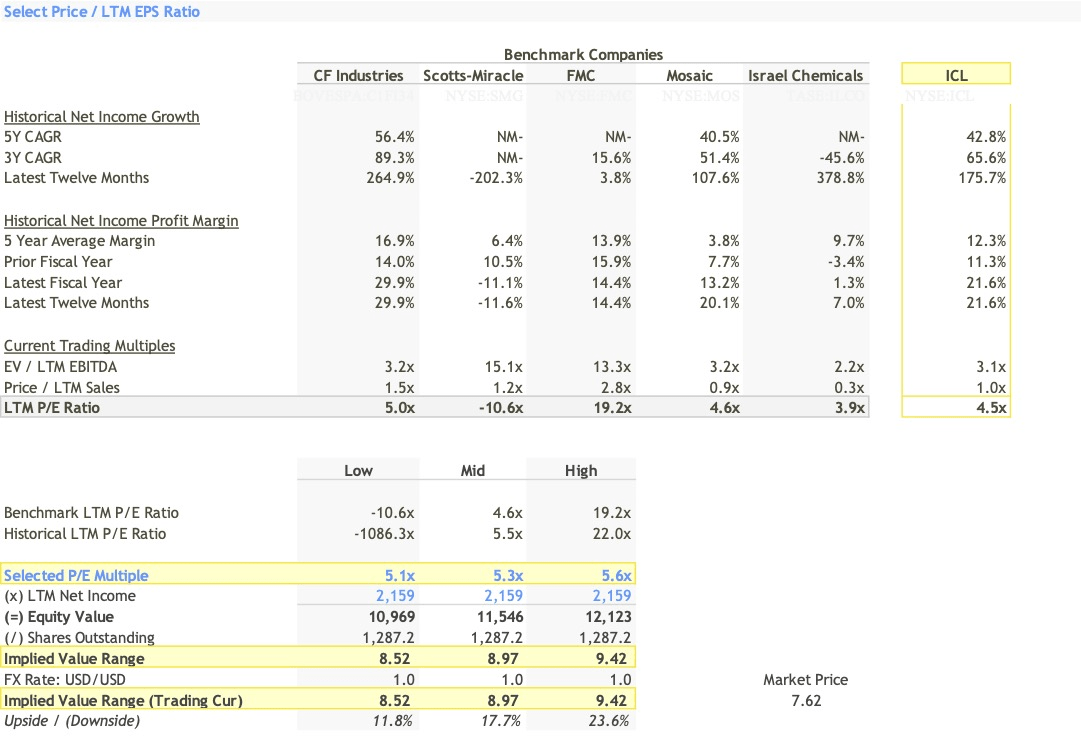

For the comparables valuation, I look at the P/E multiples of the companies for the last five years and arrive at the median P/E. For ICL, the median P/E multiple is 5.5x, higher than the current P/E of 4.5x. Further, I also take the median of the LTM P/E of the benchmarked companies, which is 4.6x. Then I take the average of the median of ICL's last five-year P/E multiples and the LTM P/E of the benchmarked companies to arrive at the P/E multiple of 5.3x.

{kind=link}

At an LTM net income of $2.1 billion, I arrive at the implied value for ICL at $8.97 per share, giving it a 17.7% upside against the current trading price.

To calculate the forward P/E multiple, I forecast the net income for ICL at $1.1 billion for 2023 and $1.25 billion for 2024.

{kind=link}

At the forward P/E of 8x, the implied value for ICL is $7.7 per share, implying that the company is trading at a fair value. I average the implied value obtained from LTM and forward P/E multiple to arrive at an implied value of $8.37 per share. At this price, ICL looks fairly valued by comparable valuation.

{kind=link}

For the DCF model, the following are my assumptions:

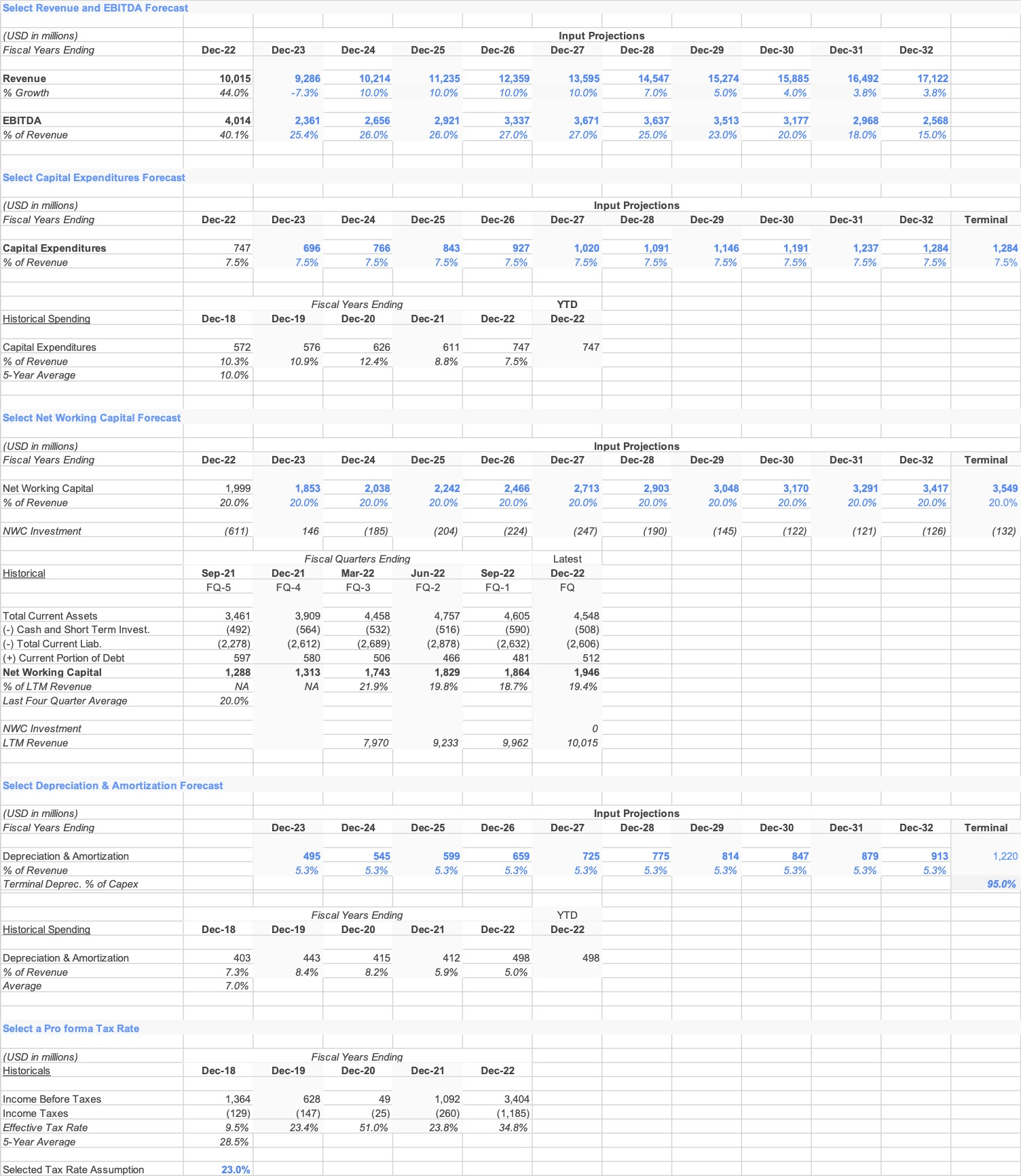

Revenues will decline to $9.2 billion in 2023 and grow by 10% for the next five years before converging to a risk-free rate in the terminal year. My ten-year revenue forecast CAGR is 5.5%.

I assume the EBITDA will decline to $2.3 billion in 2023 as per the guidance given by the company and will converge to the industry average of 15% in the terminal year.

The company's capex and NWC margin for 2022 was 7.5% and 20%. Therefore, I assume the Capex and NWC margin for the next ten years as 7.5% and 20%.

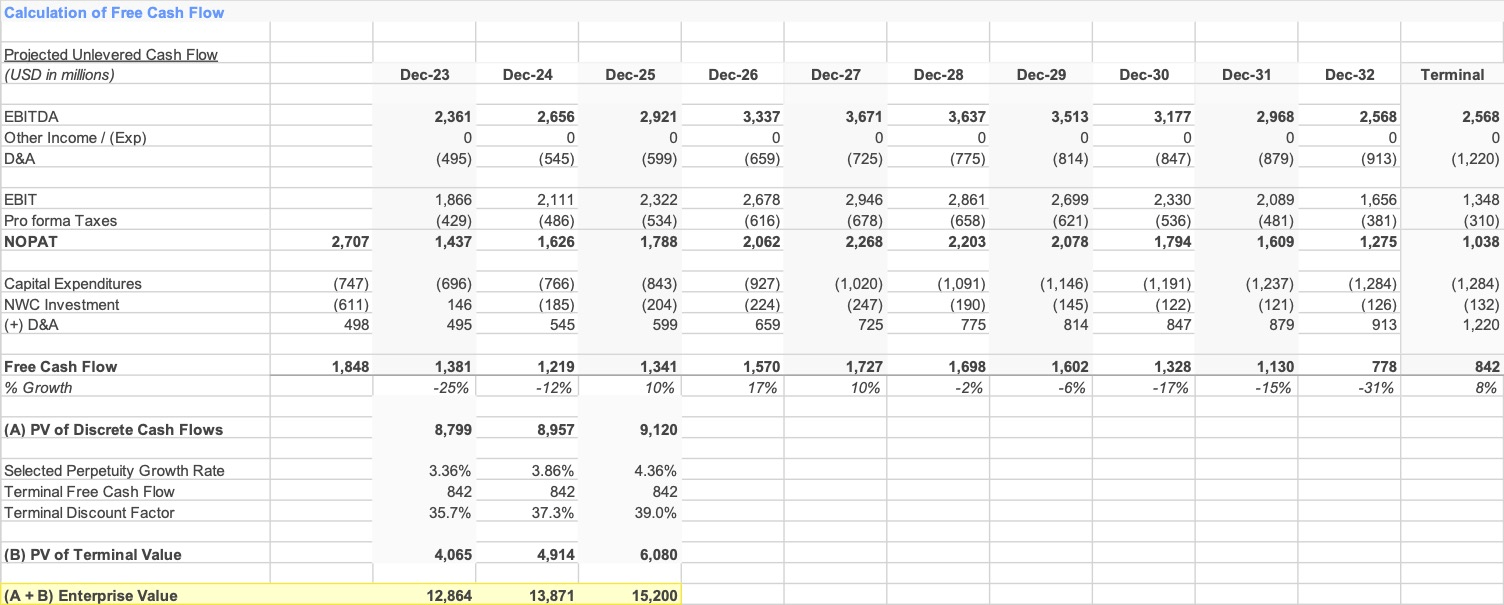

For WACC, I assume the ten-year US treasury bond rate of 3.65% is risk-free.

I assume the company will not change its current debt-to-capital ratio, thus arriving at an after-tax cost of debt of 3.5%.

I assume the ERP for the US is at 5.5%.

For arriving at the unlevered beta, I take the bottom-up beta of all chemical companies to arrive at 1.42 and 22.5% debt to capital ratio; the levered beta is 11.1%.

The cost of equity is 13.3%, and the cost of capital is 10.5%.

{kind=link}

I incorporate the above assumptions to arrive at $13.8 billion as enterprise value.

Author Calculations

Adding cash and subtracting debt and other liabilities, I arrive at the equity value of $11.3 billion and $8.78 per share, giving it a 15% upside against the current price of $7.62.

I arrive at the fair value of $8.37 per share using comparables valuation and $8.78 per share using DCF valuation. I conclude my analysis by stating that ICL trades at a 10% discount over the current market price. The company will have a challenging 2023, and the market has considered that and revised the prices accordingly. However, over the longer term, this stock is a good buy for value investors who want higher dividends and stable cash flows.

For further details see:

ICL's Growth Momentum Could Stall In 2023 Amidst Challenging Market Conditions