ICLR - ICON: Economic Business Returns Lagging Capital Charge Revise To Hold

2023-08-16 04:29:58 ET

Summary

- ICON came in with a reasonable set of growth percentages in its Q2 numbers.

- The acquisition of PRA Health has not added the expected value to ICON I had hoped, potentially dragging down shareholder value.

- The debate centers around the treatment of goodwill in valuing ICLR, with the company yet to create long-term shareholder value from the acquisition.

- Net-net, revise to hold.

Investment briefing

Since my June publication on ICON ( ICLR ) the position has moved 18% into the money. I'm now going to exit the position with this money return, taking profits at the current market value as I write. Based on the economic characteristics discussed here today, my outlook on ICLR's equity stock has revised from bullish to neutral. Chiefly, the PRA Health acquisition hasn't compounded the firm's intrinsic value as I'd hoped back last time and may potentially be a drag on shareholder value going forward.

Net-net, based on my revised assumptions, I've got ICLR priced at the current market value. This report will run through what's changed in the outlook and the economic reasoning why.

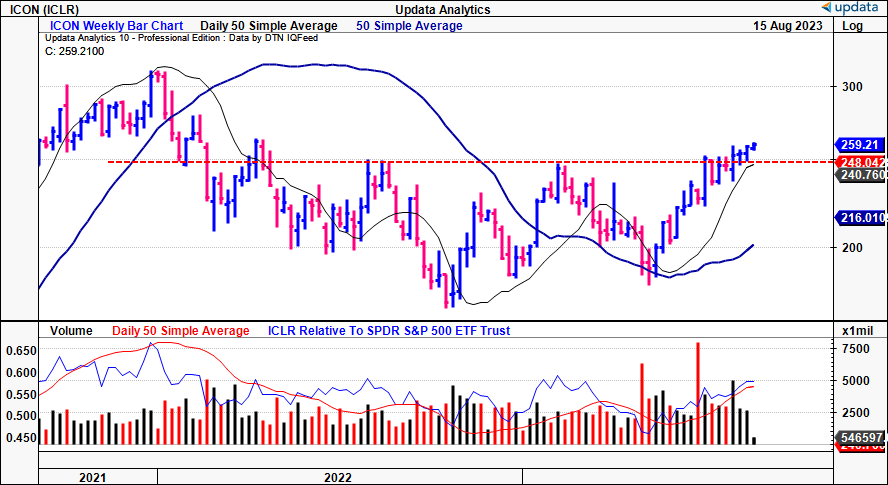

Figure 1. ICLR price evolution

{kind=link}

Updates to critical investment facts

1. Q2 earnings breakdown

It was another stride in financial growth for the company last period . For starters, gross business wins pulled a decent height of $2.86 Bn, counterbalanced by $441mm of cancellations. This wins/cancellations axis booked net awards of $2.42 Bn for the quarter, reflecting a net book-to-bill ratio of 1.2x.

Order backlog rose to a new record of $21.7Bn, up 2.2% sequentially and 8.5% YoY. It burned through 9.5% of its existing backlog over the 12 months to Q2. Moreover, days sales outstanding ("DSO") increased 12 days YoY to 52 days by end of the quarter. Despite increased duration in sales to cash, it was down 2 days sequentially. On this, quarterly revenues were at $2Bn for the first time in ICLR's history. It pulled this down to adj. EBITDA of $414.2mm and earnings of $1.40/share.

It booked $204mm in OCF for the quarter and clipped an 18% growth in free cash flow to the firm YoY. Management are eyeing free cash flow of ~ for FY'23. Should DSO continue trending down, this isn't an unreasonable estimate in my view.

Figure 2. ICLR Q2 FY'23 and 2023 YTD operating statistics

Data: BIG Insights, Company filings

{kind=link}

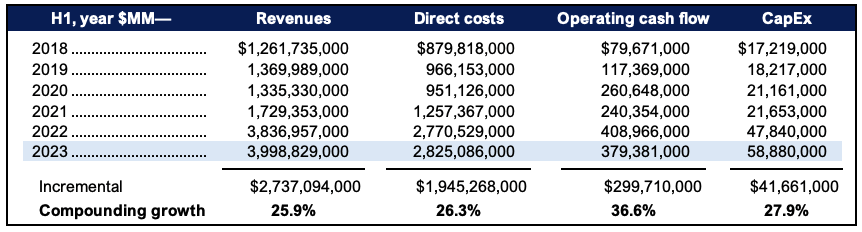

Winding back the clock to 2018 you can see the impact of the company's PRA Health Sciences acquisition from 2021 (discussed later). Results from the first half of each year are shown. This added ~$2Bn in incremental semi-annual revenues, ~$1.5Bn in direct costs, along with $140mm in OCF. At the same time, ICLR requires an additional $58mm in semiannual CapEx to maintain its current-steady state.

Figure 3.

Data: BIG Insights, Company filings

{kind=link}

2. Contributions from PRA investment

As a reminder, ICLR completed the acquisition of PRA in July 2021 on a c.$12Bn cash and scrip consideration. It used a combination of cash and debt (~$6Bn) to finance the transaction. From the deal it booked ~$8Bn in goodwill on the balance sheet and ~$4Bn in net working capital.

Firms typically create value for shareholders in 4 primary ways [either separately or combined]-new products/services, increasing current capacity, operational efficiencies/margins, and lastly, acquisitions. The headwind isn't the cash to invest, it's the profitable opportunities to deploy the capital-especially with cash at c.4-5% at the moment. Companies of a certain size and maturity often lack the organic opportunities to allocate growth capital; thus, acquisitions are often the route of choice to add business and shareholder value.

In my view, this is why the PRA acquisition is potentially valuable to ICLR. It represents an opportunity to deploy capital to grow the top-line - which has obviously occurred, given the record $2Bn quarter in Q2. It has produced an additional $842mm in post-tax earnings from this, throwing off an additional $1Bn in cash to shareholders in the process (both figures are from the time of the acquisition and in TTM values).

The market is valuing ICLR as a function of the PRA transaction's outcome in my opinion. The debate on its market value really depends on how you treat the accounting goodwill in the equation. What's more important to extrapolate is the economic goodwill produced from the transaction. Economic goodwill looks at the tangible and intangible value of a business and is not necessarily reflected in its accounting goodwill on the balance sheet. In ICLR's case, we can see it as the competitive advantage it gained (or lost) after buying PRA, to 1) generate higher profits and 2) maintain a sustainable position in the market over the long run. The questions we want answers to are:

- Did the transaction improve ICRL's economic durability and/or competitive outlook?

- Did it increase ICLR's propensity to produce additional, sustainable profit growth without eroding shareholder value?

Key shareholder statistics from the investment are noted in Figure 4 and Figure 5. The gross asset value of $12.8Bn had produced an additional $842mm in earnings after-tax, otherwise, 6.6% return on investment to date, corresponding to $0.06 for every $1 invested to buy PRA.

Critically, the change in market value is also 6.6%, matching the business returns. The market therefore recognizes the additional contributions from PRA very clearly. In dollar terms, since it bought PRA, ICLR's market value has increased $16/share as I write, from earnings growth of $10.25/share. The acquisition 'cost' is $155/share. Thus, it has produced:

- $10.25/share in earnings on $155/share of gross asset value paid for PRA Health (6.6% return)

- $0.10/share in additional market value from the investment (16/155 = 0.1)

- $1.60 in market value for every $1 in returns on new capital (16/10 = 1.60).

These aren't the most attractive returns on investment so far. These figures exclude new capital contributions and changes in the underlying marketplace, but do a good job in portraying the economics post-deal. For ICLR's owners, the investment return is 8%.

Figure 4.

Note: Earnings are represented as net operating profit after tax. (Data: BIG Insights, Company filings)

Figure 5.

Note: Earnings are represented as net operating profit after tax. (BIG Insights)

The accounting treatment of goodwill in the firm's profitability makes a considerable difference. Excluding it from the calculus, you're looking at 25% trailing ROIC, up from 11% just after the transaction. But including it, it is just 9%. The hurdle rate in all my analyses is 12%-corresponding to long-term market averages. Hence, the goodwill charge is a negative for the firm's economic goodwill.

Figure 6.

BIG Insights

Valuation

The potential issues raised in argument (2) above are the following:

- The firm is now a more asset-heavy business. It dollars employed in fixed and intangible assets alone is $5Bn higher vs. pre-acquisition, to maintain a sustainable rate of business growth, but produces an additional $100-$200mm in trailing post-tax earnings (using rolling TTM periods).

- Consequently, the headwind is for ICLR to produce earnings on such assets considerably higher than market rates of return. As an 'investment return' [from the PRA outlay], you're currently not above the 12% required to beat the long-term market return on capital.

The risk is that asset-heavy businesses are generally at risk of producing low rates of return from earnings. That means, less likely to produce enough capital to fund growth initiatives, produce real growth (outside of inflation), distribute as cash flows to owners, and make future acquisitions.

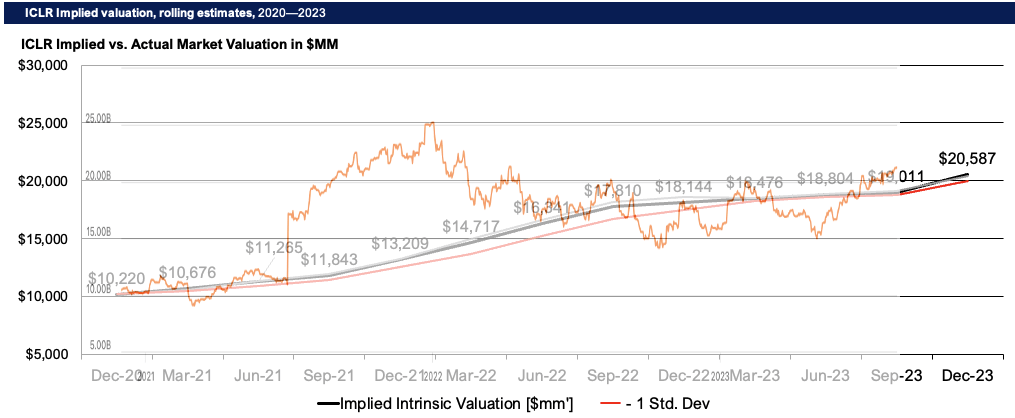

As a result, my estimations have ICLR now resting at a fair value after paring back my growth and value assumptions. This gets me to ~$260/share, down from the $304 raised last time. I get to the ~$21Bn in market value from the returns on capital and earning reinvestment forecasts out to FY'23. The PRA deal hasn't added the kind of value I was aiming for in buying ICLR, and clipping a c.20% return on my ICLR long position is a sensible use of capital in my opinion.

The stock also sells at 42x forward earnings and 40x cash flow, just 2.5% cash flow yield. It seems difficult for ICLR to grow into this valuation by best estimation. With all that's been discussed today, I'd need ICLR printing at least $2.5Bn in annualized post-tax income off the $14.14Bn employed into the business. On management's forecasts, it looks to ~$1.4Bn this year, nearly $1Bn behind. This supports a revised outlook to hold in my opinion.

Figure 7.

{kind=link}

In short

After collecting ~18% on my ICLR position since June I'm closing the position to allocate the capital to more profitable opportunities. This analysis covered the contributions from the company's PRA Health acquisition, which had offered unique value up until the June publication, but has since diminished in my view.

The debate centres around the treatment of goodwill in valuing ICLR. The operating economics of ICRL's business are vastly different with its inclusion. On the one hand, it represents a transfer of wealth from the acquiring firm to the target firm's shareholders. On the other, it is a non-operating asset, not directly 'contributing' to profits. Buffett, in his typical eloquence offers a unique perspective: "When an overexcited management purchases a business at a silly price...the silliness ends up in the goodwill account. [It then] remains on the books as an "asset", just as if the acquisition had been a sensible one".

From the economic benefits it has produced to date, ICLR has yet to create long-term shareholder value from its PRA Health acquisition in my view. Key words there are the long-term value. Up to my last publication, things were looking good on this front. The market agreed. However, the pace hasn't kept up and this supports my revised neutral view. Net-net, revise to hold.

For further details see:

ICON: Economic Business Returns Lagging Capital Charge, Revise To Hold