ICLR - ICON: Long-Term Cash Compounder That Looks Overpriced

- ICON delivered a solid Q2 FY22 earnings with upsides in revenue, although missed consensus EPS.

- The company is a long-term cash compounder that averages triple-digit FCF conversion on a sequential basis.

- It has also consistently generated a positive return on capital in the years to date.

- Despite this, the market has it richly priced by estimate, and we see it fairly valued back towards $179.

Investment summary

This report outlines our neutral stance on ICON Plc (ICLR) shares. The company's Q2 FY22 earnings illustrate a firm bedrock of fundamentals to work with, however valuations have us on the sideline. ICLR is a long-term cash compounder that has averaged ~$145 million in quarterly FCF conversion over the years to date, whilst bumping ROIC to ~7% in the last quarter. Despite this, we believe the market has it over priced, and aren't satisfied with overpaying at the book value level. As such, we feel it is fairly priced at $179. With these points in mind, we rate the stock neutral, although look forward to keeping a close eye on its next moves.

Exhibit 1. ICLR 6-month price action

{kind=link}

Q2 earnings illustrate earnings quality on show

Second quarter earnings came in strong with gross business wins of $2.76 billion. There were $441 million (~16%) of cancellations throughout the quarter, resulting in net awards of $2.2 billion. This gives ICLR a book to bill of $1.25 billion. The inclusion of 2 additional awards this quarter saw backlog grow to $20 billion, ~19.7% YoY and ~210bps QoQ increase. It churned through ~9.9% of backlog during the quarter (~40% annualized), in line with Q1. Revenue also came in exceptionally strong with a 122% YoY gain to $1.94 million. It also realized a negative Forex impact producing a ~350bps headwind to revenue.

Exhibit 2.

Data: HB Insights, ICLR SEC FIlings

In that vein, long-term profitability earnings trends continue to be a standout for the company, and continued into this quarter. Gross margin came in ~800bps higher YoY to 28.4% and was attributed to operational efficiencies and growth in revenue from direct fees. It also saw SG&A expense of $194.4 million ($2.39/share) or ~10% of turnover. Management expect this 10% to extend throughout H2 FY22 as well.

Moving down the P&L, it printed quarterly non-GAAP operating income of $328 million ($4.03/share) and EBITDA of $354 million. It also paid a net interest expense of $43 million on its outstanding liabilities and foresees full-year interest expense heading to $210 million ($2.58/share), up $50 million from previous assumptions.

Operating income carried down to a GAAP net profit of $178 million which saw diluted EPS of $1.41. The result saw management update full-year guidance "to reflect the impacts of macroeconomic factors by our expected results". It now expects YoY revenue growth of 40-43%, calling for $7.7-$7.8 billion at the top.

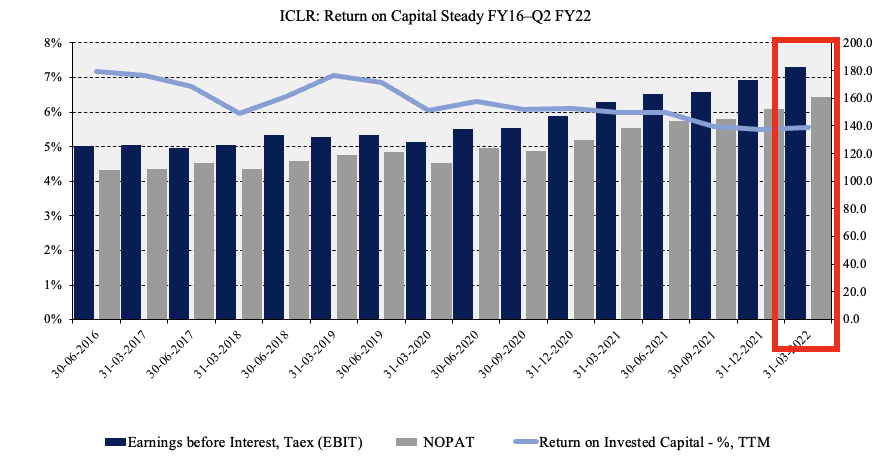

ICLR has continued to generate substantial return on invested capital over the period from FY16 to date. This is important in the current environment. It has averaged ~$145 million in FCF conversion since FY16 to Q2 FY22. Hence, Q2 FY22's FCF of $176 million was an above-average result. It has also continued to compound FCF at 21% geometrically on a sequential basis during that time.

As seen in the chart below, it continues to grow NOPAT and ROIC has held steady alongside this. Here we checked how much NOPAT is generated from last year's invested capital, and we observed it deliver a return on investment of ~7%, whereas its WACC is currently ~7%. The ROIC/WACC ratio is therefore 1x, and is extremely conducive for ICLR to access capital in the forward looking regime. With this asset/liability matching, the case is made for further profitability down the line.

Exhibit 3. ICLR continues to generate substantial quarterly return on investment – measured by NOPAT / last year's invested capital.

{kind=link}

As such, we see substantial liquidity available for the company and believe it has ~23 quarters of runway left on its cash position, as seen in Exhibit 4. In this sense, we are confident in its ability to continue compounding FCF and generate ROIC.

Exhibit 4.

Data: HB Insights Estimates

Valuation

The stock is richly priced at more than 103x P/E and even more so on a forward looking basis. It also trades at ~2.3x book value and is trading at 3.4x sales. It is also richly priced at ~107x FCF, and investors realize a 0.9% yield on this. Multiples are therefore unattractive but not a realistic view of the corporate value in this instance anyways.

Exhibit 5. Multiples and comps

Data: HB insights

In an environment that agrees with value it's prudent to examine things this way. If we were to actually pay 2.3x book, or 2.93x EV/book value, we'd theoretically be paying $228 and $290 respectively. As such we estimate ICLR to be overvalued by ~27% and price the stock at $179 per share accordingly.

Moreover, ICLR achieved a stellar FCF ROE last quarter of ~12.7%, as seen in Exhibit 6. This is an above-average result that speaks to the company's cash-conversion ability. However, this is ICLR's ROE, and we need to adjust to reflect what we'd 'pay'. Doing so we see the FCF ROE slip to just 5.5%, giving an equity duration of more than 13 years.

Exhibit 6. We'd be overpaying at ~3x Enterprise value to the book value, reducing our ROE to 5.5%.

Data: HB Insights Estimates

Additional market factors

In addition to the above, the ICLR share price has strengthened against the pharmaceuticals and medical research sector. The stock has caught a bid since July, however had been looking to diverge from the sector to the upside since May, seen below.

However, there is the case this could be sector beta, as preceding the uptick in relative strength, it saw an upshift in covariance structure relative to the sector. This is important as we're seeking to identify idiosyncratic risk premia in H2 FY22. Outbidding the sector into strength whilst reducing covariance structure is a point of evidence for this. Hence, the next moves for ICLR are crucial to identify its position within the marketplace, in order to gauge directional movement on the stock.

Exhibit 7. Gaining in relative strength to peers although this could be sector beta judging by the pattern of movement below

Data: Updata

In short

Following another robust period of top-bottom growth, ICLR looks positioned to weather any macroeconomic storm thrown its way. With a long-term pattern of geometric cash conversion, steady operating income growth and substantial return on capital, these are characteristics investors certainly will pay a premium for looking ahead.

However, in an environment conducive to value, ICLR looks to be overpriced. We therefore price the stock at $179 and believe there is more compelling value opportunities located within the large-cap medical technology/research domain. In view of its robust fundamentals, yet lofty valuation, we rate shares neutral.

For further details see:

ICON: Long-Term Cash Compounder That Looks Overpriced