ICLR - ICON PLC: Disconnect From Fundamentals Unfairly Punished

2023-06-02 23:58:15 ET

Summary

- ICON PLC shares set higher lows in June, and the company presents strong fundamentals and economic earnings for shareholders.

- ICLR has shown robust financial performance, with a 9% YoY increase in revenue and a 200bps expansion in gross margin YoY.

- I reiterate ICLR as a buy, revising the price target to $304, and keeping the long-term $326 target.

Investment Summary

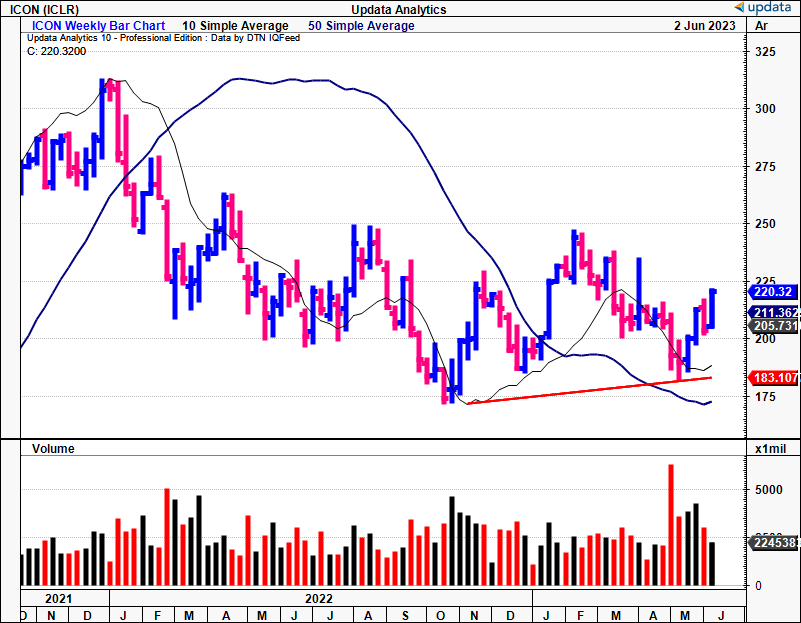

Despite a difficult run since the last publication , shares of ICON PLC ( ICLR ) have set higher lows rolling into the month of June. Those long of ICLR stock may have been bitterly disappointed when it failed to break past the February highs; however, this recent recovery is noteworthy.

Furthermore, the company presents to us with robust fundamentals and long-term data to work from, whereby it produces characteristically strong economic earnings for shareholders. Whilst many in the market have endured a tough clip to growth and earnings, ICLR not so. Shareholders have seen their book value increase from $32/share in 2020 t0 $105/share as I write, whilst it has grown its top-line by 186% cumulatively over this time. I believe this discount is unwarranted, given these fundamental strengths.

Its Q1 FY'23 numbers were further evidence of this. In that vein, I am reiterating ICRL as a buy, revising the price target to $304, keeping the long-term $326 target ascertained from my previous ICLR analysis.

Figure 1.

{kind=link}

Data: Updata

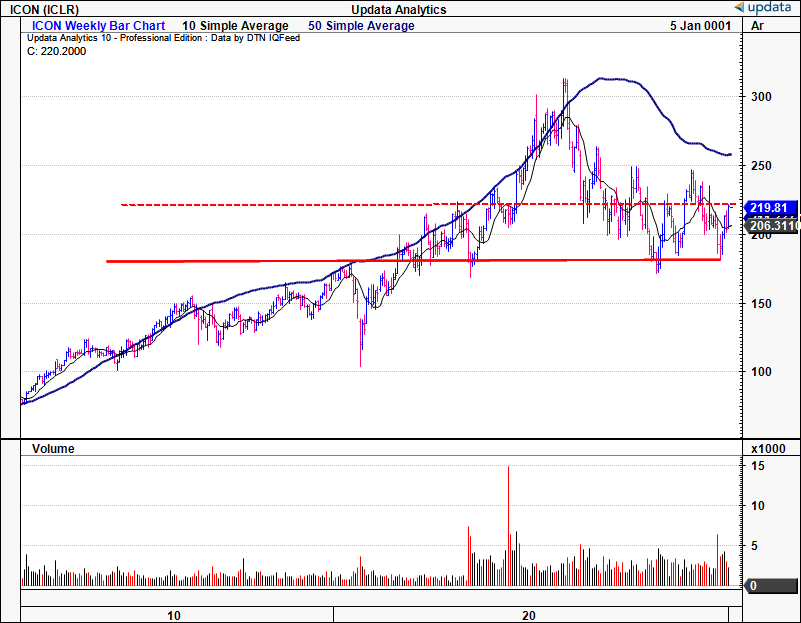

Figure 1a. – ICLR Long-term chart and levels

{kind=link}

Data: Updata

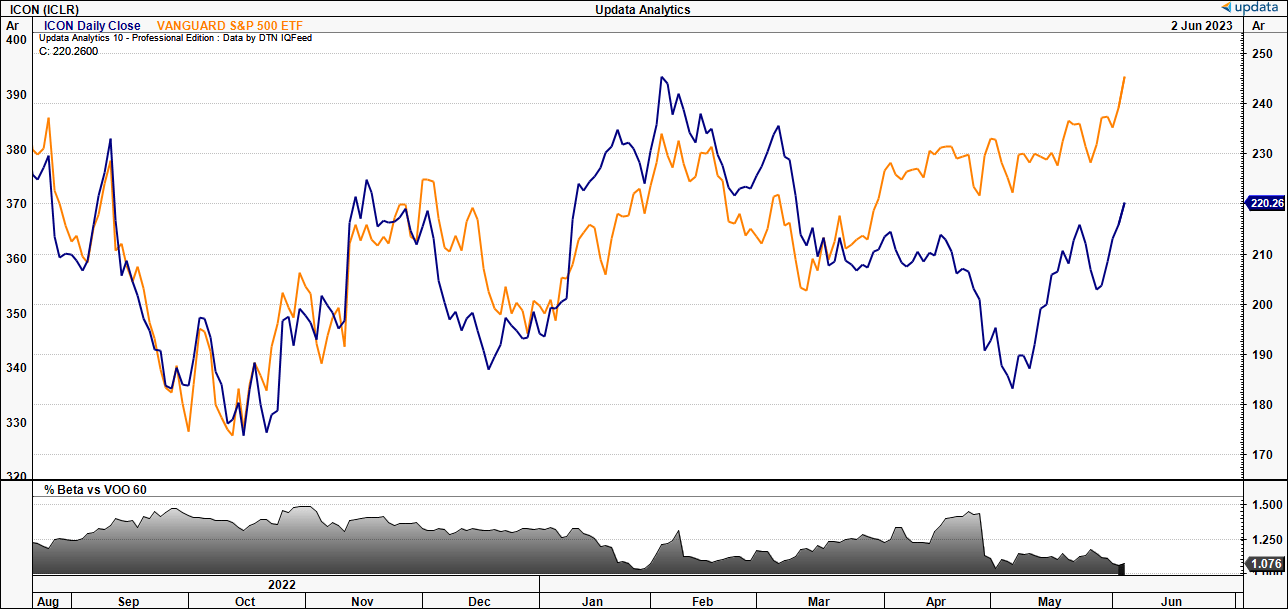

Figure 2. – ICLR versus S&P 500 Index, 2022–date

{kind=link}

Quarterly dissection

First to the high-level takeouts, and there were many. I am looking to these specific insights as potential catalysts for the company moving forward as well, so keep a close on eye on each one.

Quarterly Takeouts

1. Technology investment for value creation

- ICLR continues investing heavily into innovation and new sources of income. This approach enables the development of solutions that deliver tangible value to its customers, namely, return on the incremental capital invested to these innovations. For example, OneSearch, ICON's integrated AI tool for site identification and selection, is a prime example of this philosophy in action. It is delivering "remarkably better delivery of studies" per CEO Steve Cutler on the call. For example, OneSearch has significantly reduced 53% in the median time required for site identification for study enrolment, enhancing operational efficiency.

- Furthermore, the tool has resulted in a 50% decrease in non-enrolling sites on ICLR studies. The major benefit – streamlining the study process and improving overall outcomes. This is incredibly valuable in my opinion because I cannot tell you how long things can get held up in clinical trials which ultimately can affect investment performance.

2. Strong financial performance and growth

- Amidst the complexities and uncertainties of the market, ICON has demonstrated robust financial performance, showcasing its resilience and ability to thrive. Excluding COVID-related work on a constant currency basis, the company booked 9% year-over-year increase in revenue. Underlining this, gross bookings increased by 6% sequentially, indicating sustained demand for its services.

- I thought it was important to mention the firm's cost management strategies, along with the execution of its hub location strategy. This added across 17.2% in adj. EBITDA during the quarter, which was tremendously beneficial to see. Furthermore, solid direct fee revenue growth fueled a 200bps expansion in gross margin year-over-year.

3. Expansion of Backlog and Diversification of Customer Base

- Backlog could be a key tailwind moving forward as it is converted at a 2–4% rate over the coming 12-months. This could be a big push to free cash flow if costs are managed well as they have been to this point.

- In the first quarter, the company achieved gross business wins of $2.86 billion, contributing to a record backlog of $21.2 billion.

- This represents a 2.4% increase from the previous quarter and an 8.4% year-on-year growth. In my view, such backlog expansion underscores the firm's ability to secure new contracts and projects, highlighting its strong reputation and client trust. I am looking to companies who are growing their top line and dishing out revenue guidance (versus EBITDA/EPS) as evidence of pricing/contract strengths going forward. This is good evidence of just that in my opinion.

- Moreover, the company has successfully reduced customer concentration risks by diversifying its revenue streams. This has distributed revenue more evenly across the top-line and hedges any large-sigma events. While the top customer accounted for 8.8% of total revenue in Q1, the top 5 represented 28.8%. Comparatively, the top 10 and 25 customers accounting for 42.6% and 63.5% of revenue, respectively.

Cumulative returns are a major talking point

Taking a high-level view and noting observable trends is a fruitful exercise in this instance. For one, you can clearly see the momentum ICLR is building around its core business. To analyse this I took quarterly and annual financial data from ICLR dating back to 2020 and ran it through a number of statistical and investment tests. Numbers were converted into a rolling TTM basis. I am bullish on ICLR from these findings and form the view it can sustain this kind of positive trajectory going forward. Why?

One, analysis of the data reveals significant trends in revenue growth and operating income for the company since FY'20. Starting with the revenue growth rate, it is observed that the company has experienced a remarkable increase since Q1 2020. Calculations show that the revenue growth rate since Q1 2020 is approximately 183.52%.

- [Revenue Growth Rate = (($7.81Bn - $2.76Bn) / $2.7625Bn) * 100 = 183.52% ]

To me this indicates a substantial growth in the company's top-line and therefore volume and/or pricing over the analyzed period. Looking forward, this bears in well and supports my investment thesis.

Two, turning to the growth in operating income, it is evident that the company has also made considerable progress. By comparing the operating income figures from Q1 FY'20–'23, growth rates were calculated for different periods. For example, the growth in operating income since FY'20 is ~126.5%, reflecting a significant improvement in profitability over the testing period. Similarly, the increase in operating income since FY'21 is approximately 95.82%, further evidence of this continued momentum. Finally, the growth in operating income since FY'22 is estimated at 9.31%, indicating a more modest rate but still showcasing a positive trend.

Three, the spectacle here is that ICLR has effectively managed its costs and operations tremendously well to drive this increase in profitability. This has no doubt created value and been one reason perhaps the company's book value has increased from $32.42 in 2020 to $105.60 at the time of writing, 220% change. We don't get paid for yesterday's gains, for sure, but in a time when most company's incurred substantial asset write downs these past few years, ICLR is creating equity value for its shareholders.

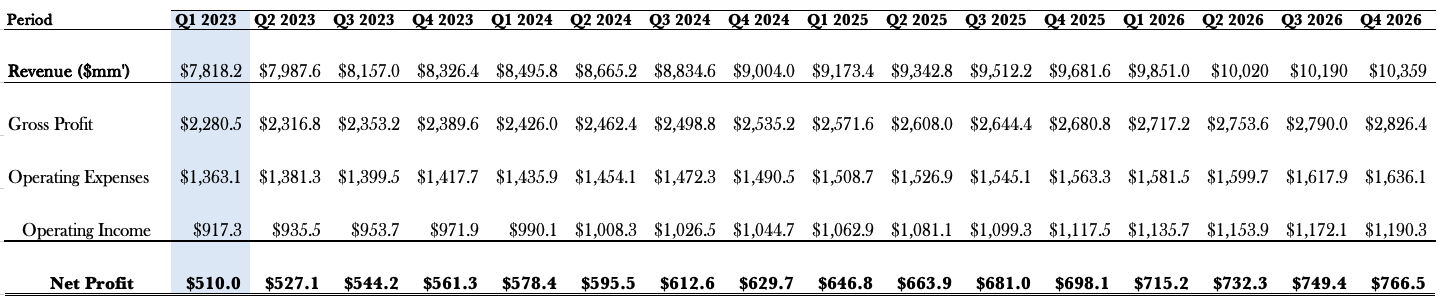

Four, looking ahead to 2024, we can make projections based on a number of assumptions [Figure 3]. By considering the revenue figures from Q1'18–'23, the average top-line growth rate is calculated to be around 2.00%. Further, management project $7.94–$8.34Bn at the top this year. My numbers have the company's revenue for FY'23 at $7.97Bn and thus I am in-line with management's view. I'd call $2.4Bn in gross on this and $971mm in operating profit, and would estimate the firm to bring this to $561mm in FY'23 earnings.

Figure 3.

{kind=link}

Data: Author Estimates

Additional financial statement forensics

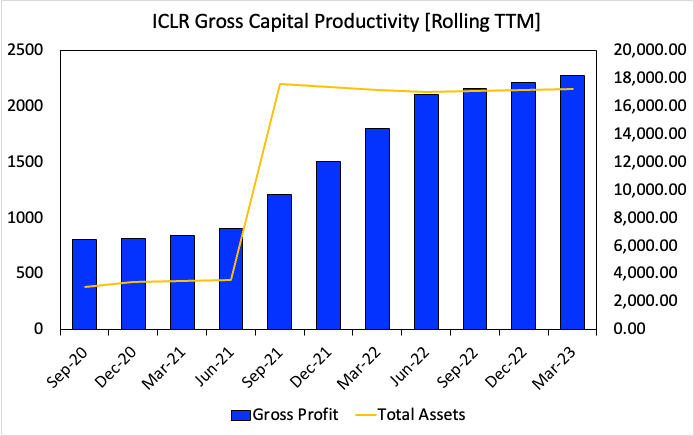

To add further clarity to the investment debate, there are two additional points that must be added to the list of critical factors. First, is the company's gross productivity, seen in Figure 4.

Here, the rolling TTM gross profit is divided by the book value of the firm's total assets each quarter to derive the gross quarterly productivity. This represents the gross return generated per $1 of capital investment into productive/operating assets. This is also done back to 2020.

As noted, the firm has been accumulating assets over the last 2-years yet the cumulative gain in gross profits has exploded from less than $500mm to $2.28Bn in the TTM. I am looking to $2.4Bn in FY'23, not unreasonable to expect.

Figure 4.

{kind=link}

Data: Author, ICLR SEC Filings

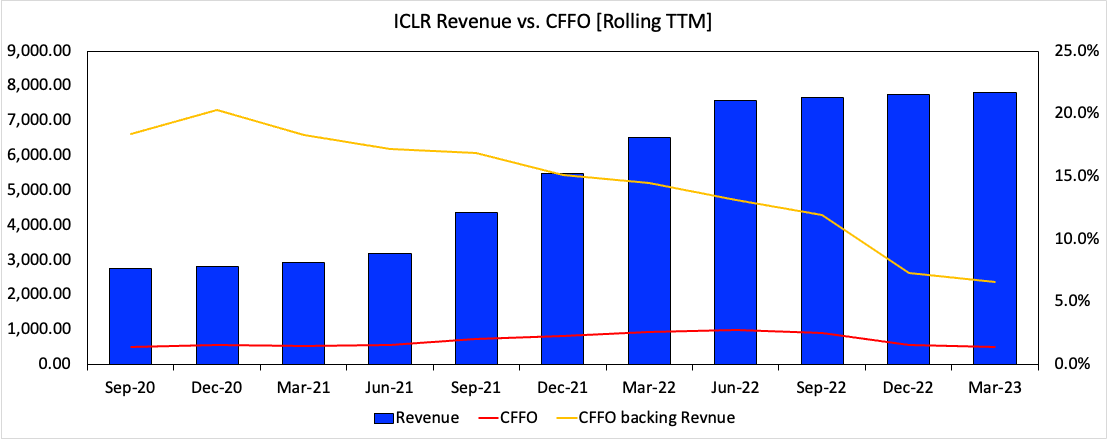

Second, you can observe some additional critical facts in Figure 5. Perhaps most notably, is the reduction in operating cash flow backing revenues. This is not a concern for me, as it is expected with the top-line growth also an increase in NWC density, and therefore accounts receivable over time. Still, the firm is generating substantial operating cash flows in the realms of $500mm–$900mm on a cyclical basis. To me, this is still a good absolute number, but with only 7% CFFO backing turnover, I'd like to perhaps see some improvement there.

Figure 5.

{kind=link}

Data: Author, ICLR SEC Filings

Valuation and conclusion

The market has priced ICLR as a large premium at 31x forward earnings. This is 16% ahead of the sector, but the question is, does this represent value. On non-GAAP forward P/E, you're looking at 17x. In my opinion, the 13x forward EBITDA multiple is far more telling of the firm's business model. Looking to this, you can see tit trading at a small discount to peers. Hence, the valuation debate is balanced.

In my view, a 17x forward P/E (non-GAAP multiple) is fair and indicates there is valuation upside still to be made with this name, with momentum catching a "B" rating on the quant system. At this multiple at my FY'23 EBITDA numbers I get to $304 per share in valuation (17x1,470/82 = $304). This supports a buy thesis, even at the varying valuation story.

In short, I believe there is still scope for ICLR to trade higher off its current lows. Business economics are sound, and there is evidence the firm can attract further investment through its growth operations. Specifically, you're looking at hefty growth numbers over the last 3-years, and this sets a good precedent going forward. Net-net, reiterate buy at $304 price target.

For further details see:

ICON PLC: Disconnect From Fundamentals, Unfairly Punished