ICLR - ICON plc: Market Repricing Higher Revising To Buy At 33x Forward P/E

Summary

- ICON plc has set new highs after re-rating to the upside from late FY22.

- The company posted FY23E' guidance in January, where investors were swift to price in the growth forecasts.

- We believe there's scope for the stock to continue repricing higher.

- Net-net, revise to buy at 33x adjusted P/E.

Investment Summary

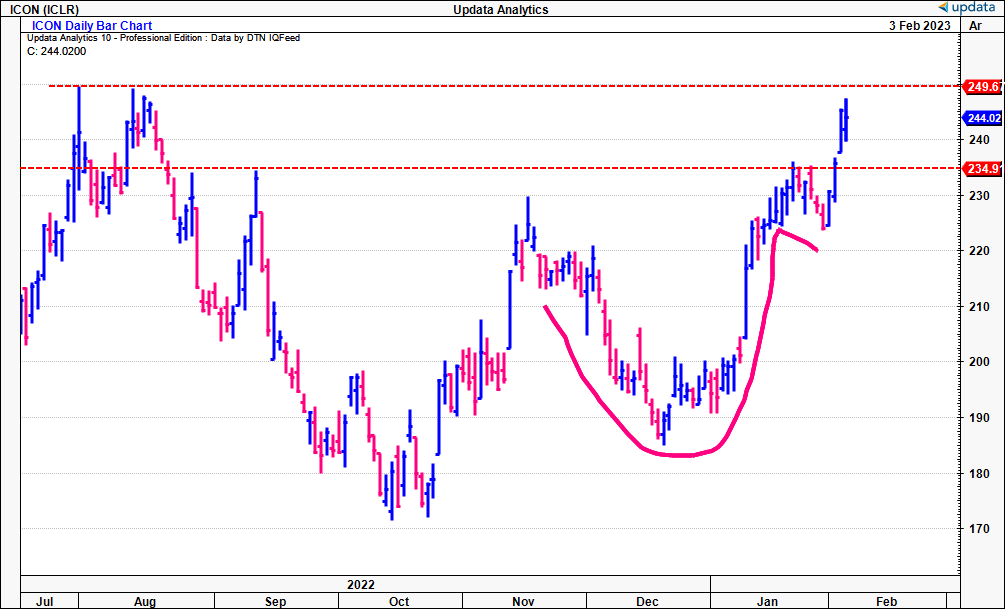

Shares of ICON plc ( ICLR ) have just broken to new highs this past week of trade and now look to test longer-term resistance levels. In previous analysis, we noted fundamental and technical headwinds compressing share price growth for the company. Check them both out here:

- ICON: Retain Hold, Latest Rally Faces Pressure

- ICON: Long-Term Cash Compounder That Looks Overpriced

Coming into its FY22' earnings date, penned in for end of this month, we are more constructive on the stock after ICLR announced its FY23E' and FY22' preliminary results in January. For the last 12 months, management expect turnover in-line with previous guidance. For the coming 12 months of FY23', it expects ~680bps YoY growth at the top-line to $8.3Bn at the upper end of range.

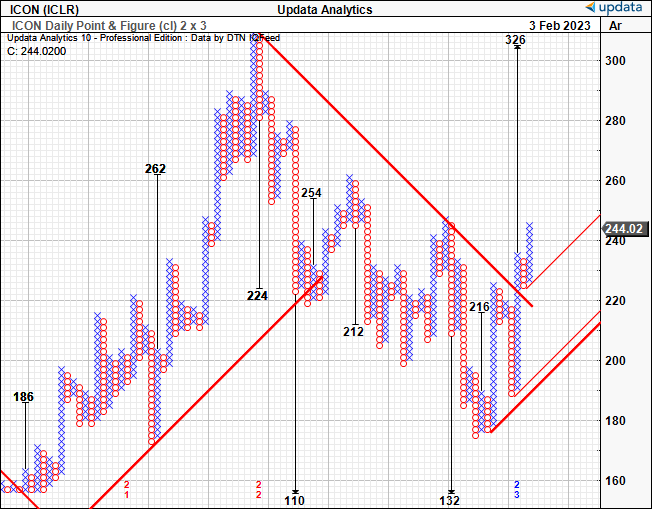

The price response was meaningfully positive after the announcement, and investors were swift to price in the company's growth numbers with a rally off previous lows [Exhibit1]. After a short pullback the stock has spiked off this level and now looks to test its FY22' highs in the cup and handle shown below. Net-net, we rate ICLR a buy, seeking upsides to $326.

Exhibit 1. ICLR thrusting off lows, breaking above previous highs and looking to test FY22' resistance

{kind=link}

ICLR justifying further re-rating?

A firm creates value for its shareholders when it generates a high return on invested capital ("ROIC") above the cost of capital. This economic profit ("EP") differs from the accounting profits stated in a company's financial statements, and is essential to create additional value for equity holders. An EP means a small portion of post-tax earnings is needed to fuel growth, leaving the remainder as distributable cash to shareholders (either hypothetical, or via buybacks or dividends). The key point from this is, whenever the ROIC is less than the cost of capital ("r"), any growth is actually destructive to value for shareholders (i.e., ROIC < r). In the same breath, when ROIC=r, growth is neutral to value. These concepts underline the fundamental tenets of our core investment principles – we want companies that require low reinvestment of post-tax earnings to grow, and can distribute high amounts of free cash to equity holders ("FCFE").

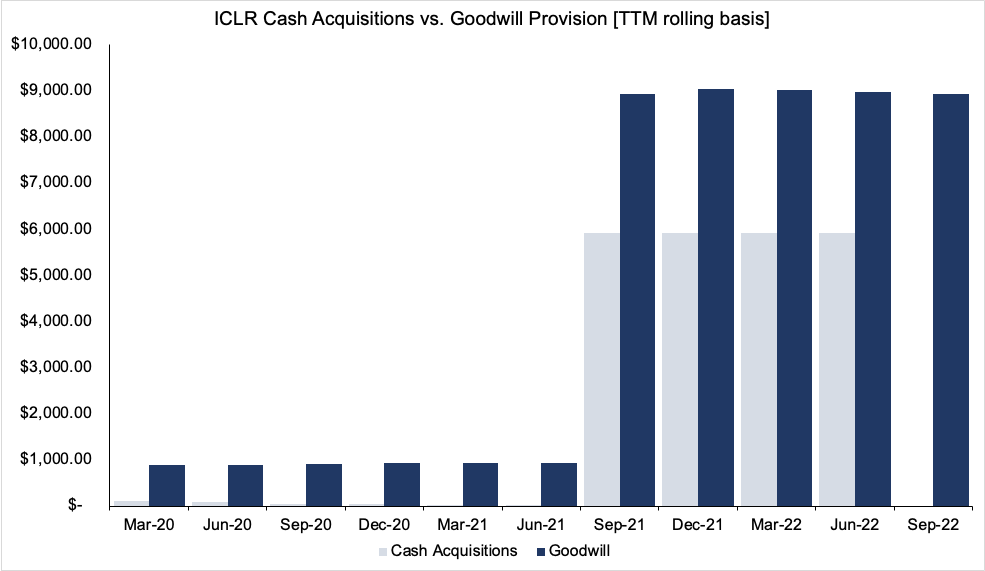

How you choose to view these ROIC and growth dynamics for ICLR depends a lot on how one treats goodwill in the process. It can be argued that goodwill should be included in the calculations of invested capital, as it often signifies the premium paid for acquisitions [or acquisitions of intangible assets], and therefore represents a transfer of wealth from the acquiring company to the target firm. On the other hand, goodwill doesn't generate operating income, and therefore mightn't accurately measure the return on the cash earnings of the company. Goodwill is also a non-operating, non-cash asset, that must be measured for impairment each period. For ICLR, cash acquisitions versus goodwill are plotted in Exhibit 2, and we will comparisons with goodwill vs. ex-goodwill in the series below.

Exhibit 2.

Note: Rolling TTM periods are used to provide an 11 period lookback where each period is 12 months (Data: Author, using data from ICLR SEC Filings)

{kind=link}

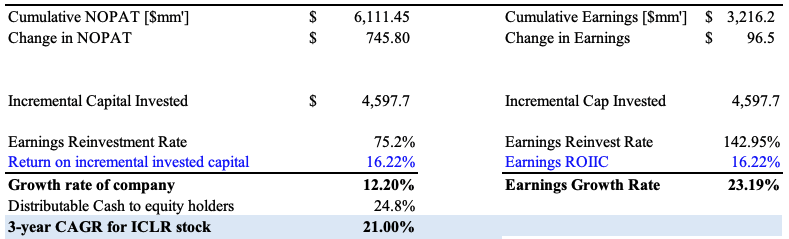

Here we use rolling TTM periods from Q1 FY20' to the latest available data at Q3 FY22'. The company generated $6.1Bn in cumulative NOPAT, for an additional growth of $745mm in NOPAT over the same time. For earnings, the numbers are $3.2Bn and $96mm, respectively. In the first scenario, where we include goodwill into the calculus, ROIC is pulled in from 25% to 8.1% in the last period. In the second, excluding goodwill, the periodic ROIC tightened from 58% to 21.7%. This displays the points raised earlier in clear detail. ROIC can be calculated using an operating and financing approach, the operating approach discussed here. However, using the financing approach, results are remarkably similar throughout the entire analysis listed above and below.

Exhibit 3.

Data: Author, using data from ICLR SEC Filings

Exhibit 4.

Data: Author, using data from ICLR SEC Filings

In order to achieve the levels above, ICLR invested another $4.6Bn in capital over this time, resulting in an incremental return on invested capital ("ROIIC") of 16.2% [ex-goodwill]. Ultimately, the growth rate in NOPAT and earnings was 12.2% and 23.2%, respectively, the latter matching the 3-year CAGR of the ICLR share price of 21%. Distributable cash to equity holders was ~25%. These are the same when baking goodwill into our calculus.

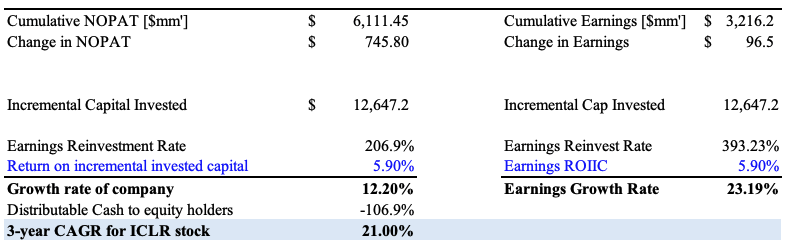

However, the key difference arises when we look at the required reinvestment of post-tax earnings required to achieve the ROIIC and growth rates. Growth comes at a cost, and not all growth is created equally. Moreover, we mentioned goodwill can represent a transfer of wealth from equity holders over to the target firm. Hence, if we portray it in this light for ICLR, its ROIIC dips to 5.9%, and the required reinvestment of post-tax earnings is in the triple digits [Exhibit 6]. Moreover, the amount of capital investment jumps to more than $12Bn, despite the same growth rates of the company. In this scenario, growth came at a large cost to equity holders.

Exhibit 5. ICLR ROIIC and growth rates ex-goodwill

Data: Author, using data from ICLR SEC Filings

{kind=link}

Exhibit 6. As above, including goodwill

Data: Author, using data from ICLR SEC Filings

{kind=link}

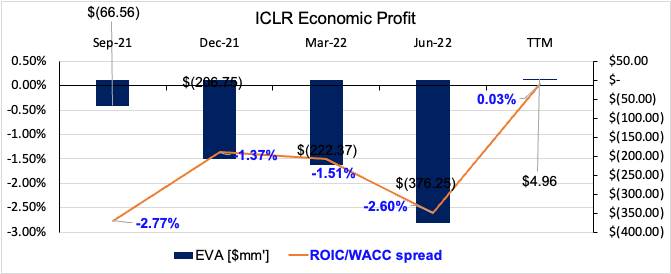

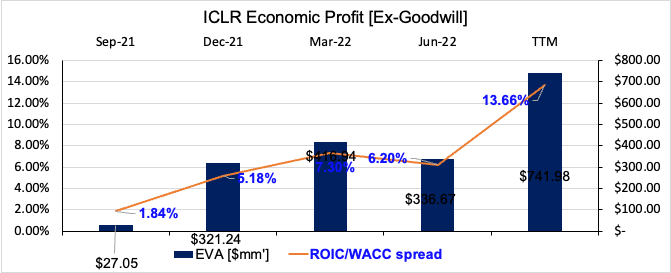

Again, a firm generates value for equity holders when the ROIC exceeds the hurdle rate. Alas, here is where the calculus really becomes important for ICLR. FY22' was undoubtedly a bear market across the broad indices, yet, companies with a high ROIC/WACC spread still outperformed respective benchmarks, as the market flocked to quality. In-line with analysis above, including goodwill, ICLR booked an economic loss from Q3 FY21–TTM, and without, an economic profit over the same time. Moreover, the stock re-rated to the downside off highs of $306 over this same period.

Exhibit 7.

Data: Author, using data from ICLR SEC Filings

{kind=link}

Exhibit 8.

Data: Author, using data from ICLR SEC Filings

{kind=link}

This displays our points on the treatment of goodwill in perfect detail. What matters most is the market's treatment of it, and, based on recent reversal in ICLR's share price, there's a probability it has overlooked its potential hinderance on the company's growth prospects. This has implications on equity valuations.

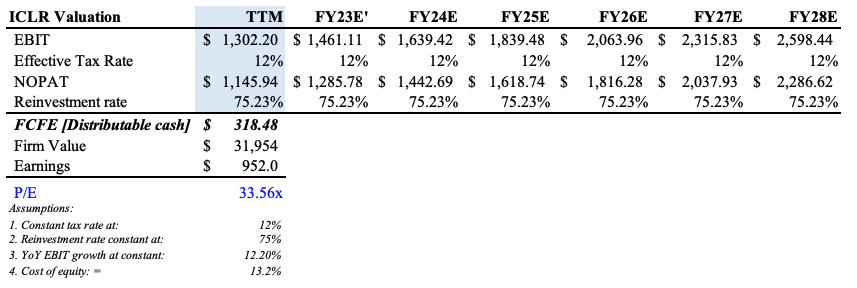

Valuation

We've chosen to value ICLR without penalizing it for the premium paid for its cash acquisitions. We've also given it a 12% effective tax rate for FY23E', below company forecasts, and presumed a similar 75% earnings reinvestment rate to fuel a 12% CAGR into the coming 5-years. Using a cost of equity of 13% based on the earnings yield and growth rates, per Roberts (1991) , we see ICLR fairly valued at a justified 33.5x forward P/E, ahead of consensus estimates.

Exhibit 9.

{kind=link}

Moreover, we have upside targets to $326 from market generated data obtained from our point and figure studies shown below.

Exhibit 10. Upside targets to $326

{kind=link}

In short

After a period of expensive growth, we believe there's scope for ICLR to reprice higher in FY23' and shift back towards its FY22' highs. Much of the investment debate hinges on whether one chooses to penalize the company for goodwill, or not. Net-net, we rate it a buy.

For further details see:

ICON plc: Market Repricing Higher, Revising To Buy At 33x Forward P/E