ICLR - ICON: Starting Valuations And Business Returns Are 2 Major Hurdles

2023-11-26 22:14:52 ET

Summary

- The market's response after ICON's Q3 numbers indicates it is forecasting a period of better business for the company in 2024.

- ICLR's projected earnings growth out to 2025 is 9-14% on sales growth of 5-7%.

- Despite a strong company, current multiples are expensive, increasing starting valuations and reducing short-term return potential.

Investment updates

Multiple investment facts have changed within the ICON ( ICLR ) debate since my August publication. I had revised my outlook on the company to neutral at that time, citing various reasons. Notably, ICLR has since surpassed this expectation with excellence and now trades at 52-week highs.

What has changed? Two critical things. Three, really. First, the Fed's decision to pause rates at its November FOMC meeting. This ignited a new flame of risk appetite among investors. Two, the company's Q3 numbers, which the market is now forecasting a period of better business for ICLR in '24. Strong backlog and guidance maintained - all conducive to robust business. Three, the company's own economics, with projected earnings growth of 9-14% for the years to come.

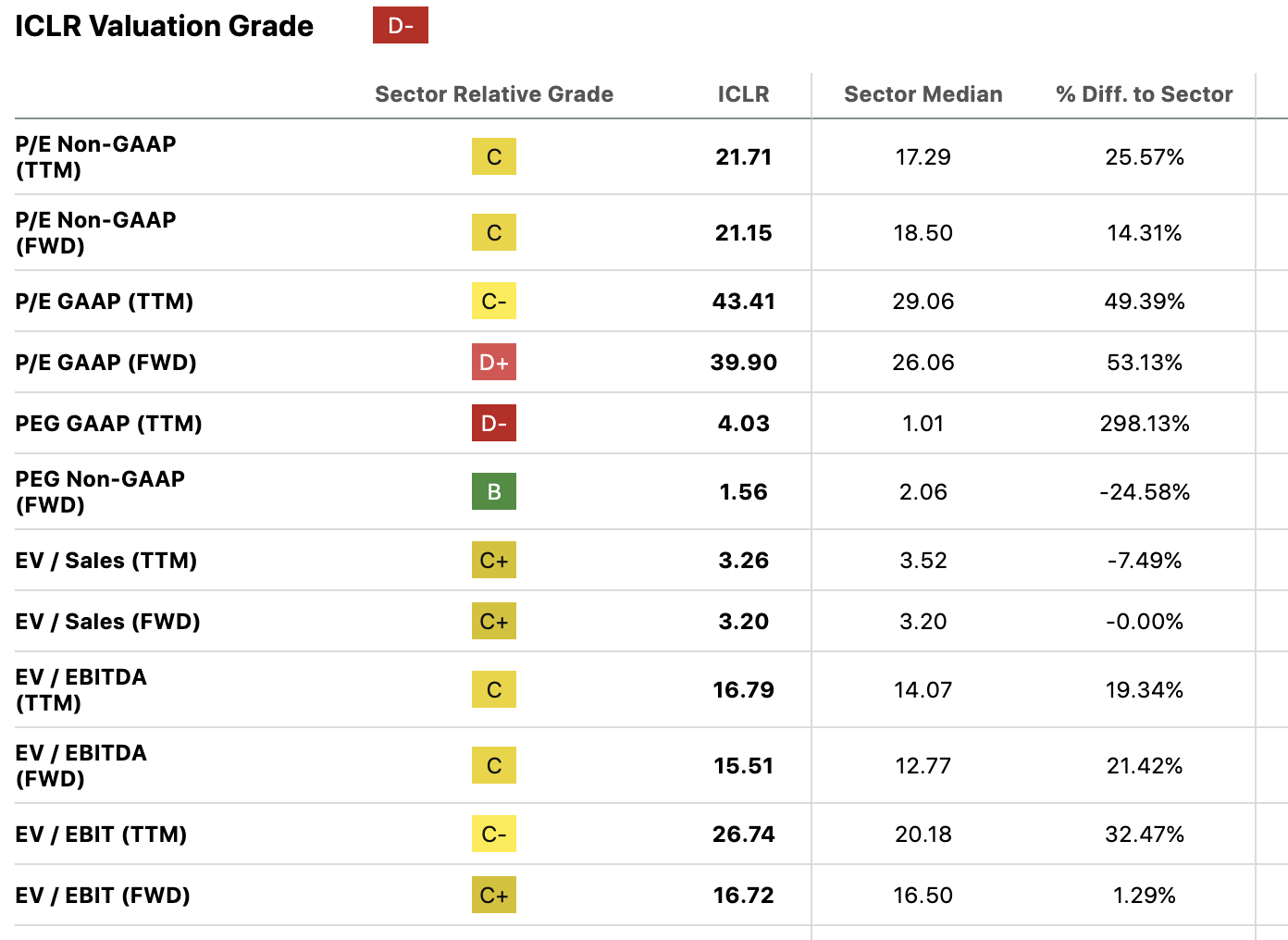

Collectively, this is an attractive value proposition. Acquiring ownership would be handsomely rewarded. But you'd be paying $21 for every $1 of that earnings growth and asked to pay 2.5x the company's book value for just a 6% rate of return on the equity. My suspicions are this might not be quite worth it for the investor of a 1-3 years horizon when there are similarly priced items with equal risk, but better return prospects.

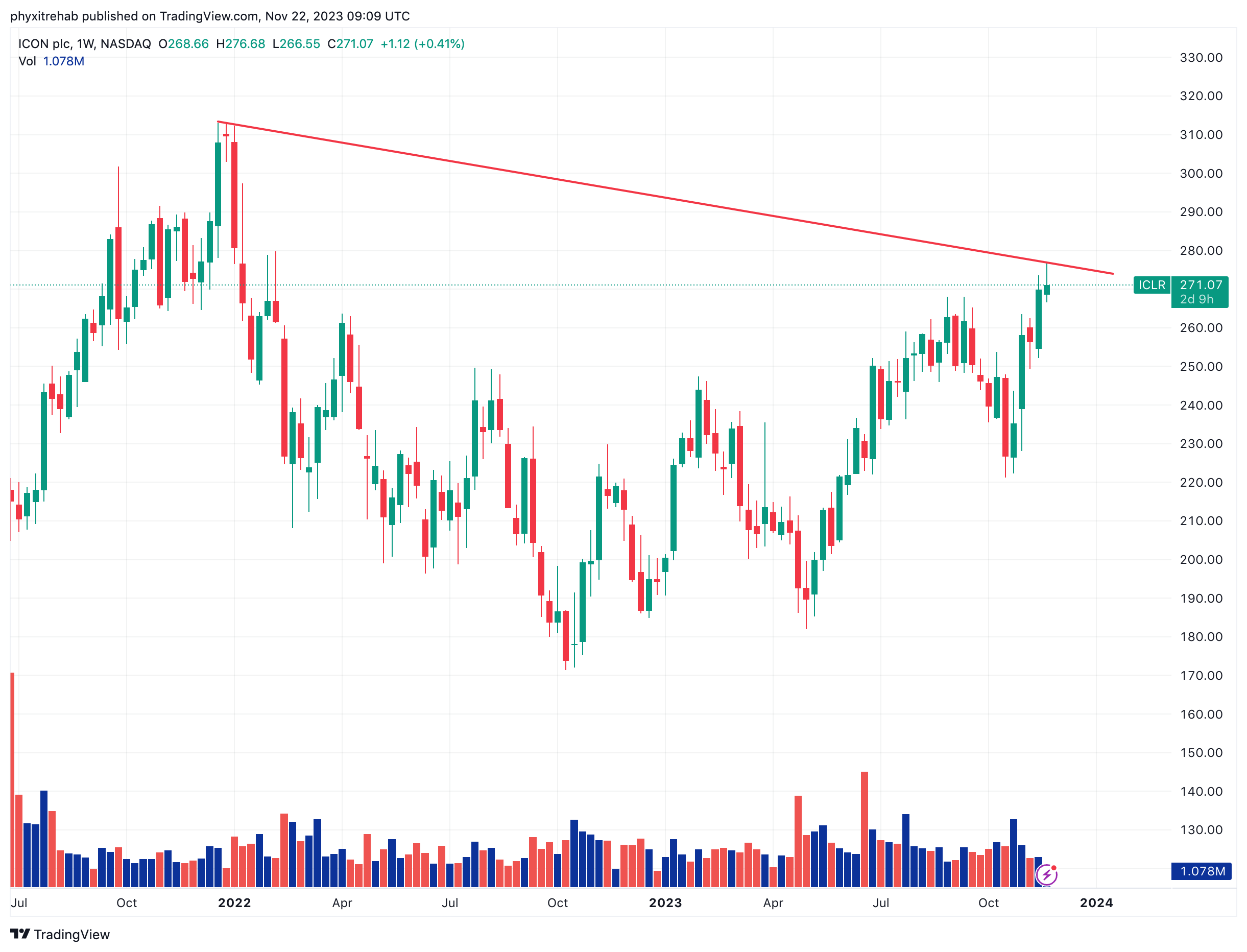

You see can below (Figure 1) ICLR has been bought heavily on each sharp pullback to the end of the range since its uptrend first began in October last year. It has now retaken all of its 2023 range and set 52-week highs, as mentioned. This is a critical juncture for investors. There is scope to allocate with another consolidation below 15x earnings.

Based on the combination of:

(1). Over-stretched multiples at 21x earnings, 2.5x book value with 6% ROE

(2). ICLR's asset-heavy business that is lagging on business returns

I reiterate my judgement on the company as a hold. This report will discuss the fact pattern to this decision.

Figure 1.

{kind=link}

What's changed in the investment thesis for ICLR, and what hasn't

Q3 earnings insights

ICLR posted its Q3 numbers on October 26th. The post-earnings drift in its stock price has been very positive. So the market is projecting a period of better business for ICLR going forward, driven by insights from the 3rd quarter.

Financial health and strategy was the theme for ICLR in Q3. Management is clearly diverting its attention to solidifying its balance sheet. It left the quarter with assets of $17Bn, long-term debt of $3.9Bn, equity of nearly $9Bn producing a trailing return of ~6% on that. The critical takeouts are as follows:

(1). Financials:

-

Revenues + business wins: Q3 revenue came to $2.05Bn, up 5.8% YoY. Meanwhile, gross business wins for the quarter tallied $3.05Bn, leading to net business wins of $2.58Bn and a book-to-bill ratio of 1.26. A book/bill of >1 is ideal, as indicates more work coming in (demand) than can be supplied, and sports growth. The closing backlog registers at $22.2Bn, growing 2.6% sequentially from Q2 2023 and by 10% YoY.

-

It pulled this to Q3 adj. EBITDA of $432.5mm or 21% of revenues, a margin increase of 14% YoY. Q3 2022 earnings of $163.7mm or $1.97/share were up 10% YoY.

(2). Financial health and strategic moves:

-

Debt management: The company made a prudent $300mm repayment on its Term Loan B debt balance. This reduced the net debt balance to $3.7Bn on a leverage ratio (net debt-to-adjusted EBITDA) of 2.3x.

-

Strategic acquisitions: In October '23, ICLR acquired Philips Pharma Solutions, adding breadth to its medical imaging and cardiac safety lines.

-

Credit rating upgrade: S&P Global Ratings upgraded ICLR's credit rating to investment grade in October. From a cash flow perspective, this is critical and helps the company's valuation. This should be taken seriously in my opinion (in the current climate).

(3). Guidance:

- Management reaffirmed its FY'23 guidance, projecting $8,.1-$8.21Bn in sales, calling for 4.3%-6.1% YoY growth at the top line. It is looking to earnings of $12.63 to $12.91 per share on this, 7.5%-10% growth from 2022.

This kind of earnings profile supports a firm moving ahead with its business at a sensible rate of growth.

Investment outlook across multiple investment horizons

Understanding of first one's horizon and second the investment needs at each point is crucial. ICLR's investment returns at different horizons are dictated by different factors. The company might appeal to investors of different holding periods. ICLR's investment outlook is summarised by the expected returns over the following:

- Short term (coming 12 months). Most heavily influenced by starting valuations/multiples and/or catalysts. ICLR is priced at 21x forward earnings and 16.7x forward EBIT and isn't on sale. Paying 2x book value gets you 6% company ROE, around 3% for the investor. Seems like a better entry point below 11-12x EBIT could be warranted. But the market is still paying 18x+ for the benchmark, so that can't be discounted. My rating is neutral in the ST.

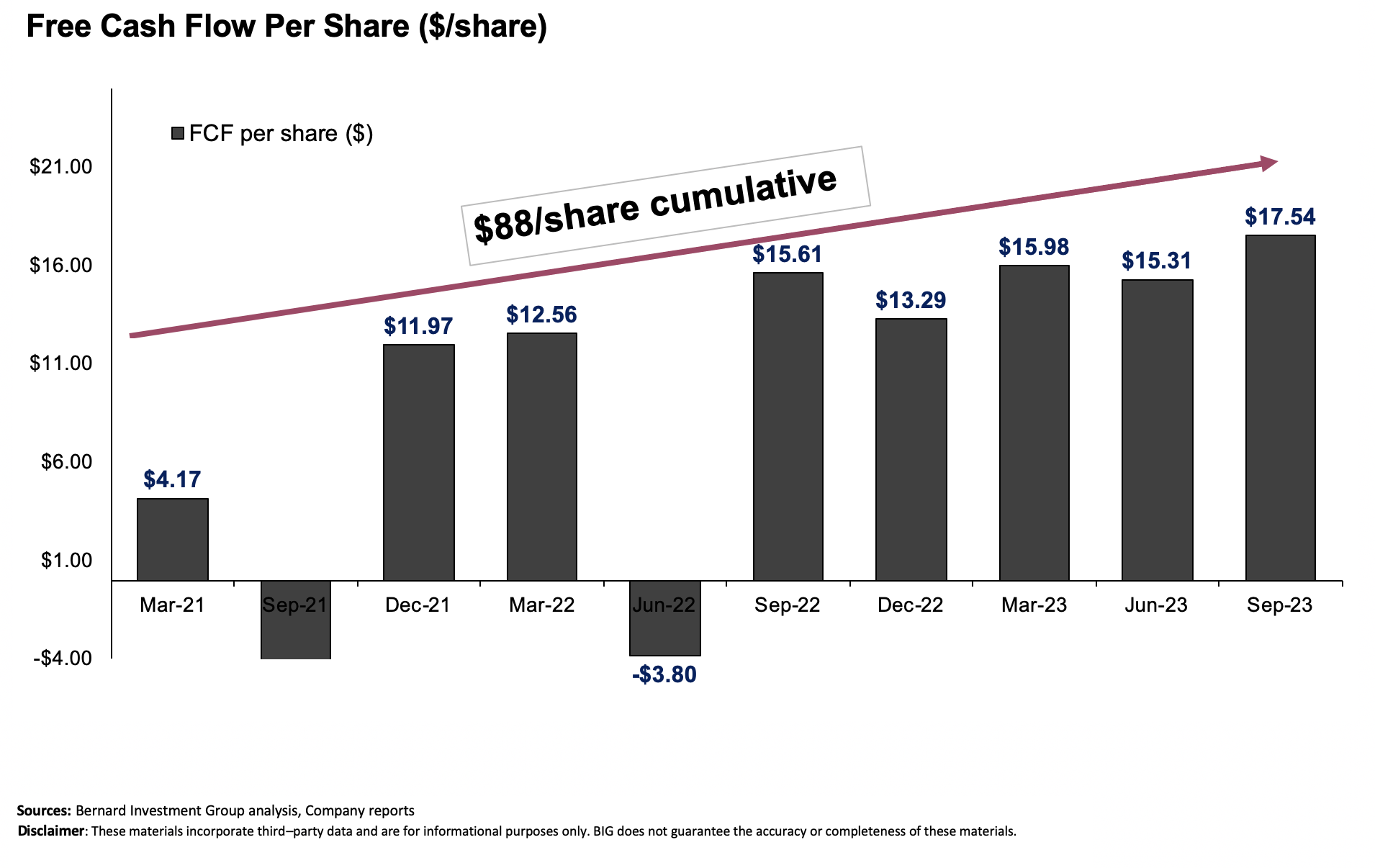

- Mid term (1-3 years). Sales and earnings growth most critical. The market is pricing in better growth for the company - 8 to 14% earnings, 5-7% sales from 2023-'25. This is large, mature business kind of stuff. Importantly, stock returns may mimic this level of growth, so it depends on portfolio expectations. No reason to be upset with those kinds of returns. We must factor in the company's $88 per share cumulative free cash flow since 2021 too. It has thrown off >$15/share of FCF in 4 out of 5 last quarters (TTM basis). These are again constructive views.

Figure 2.

{kind=link}

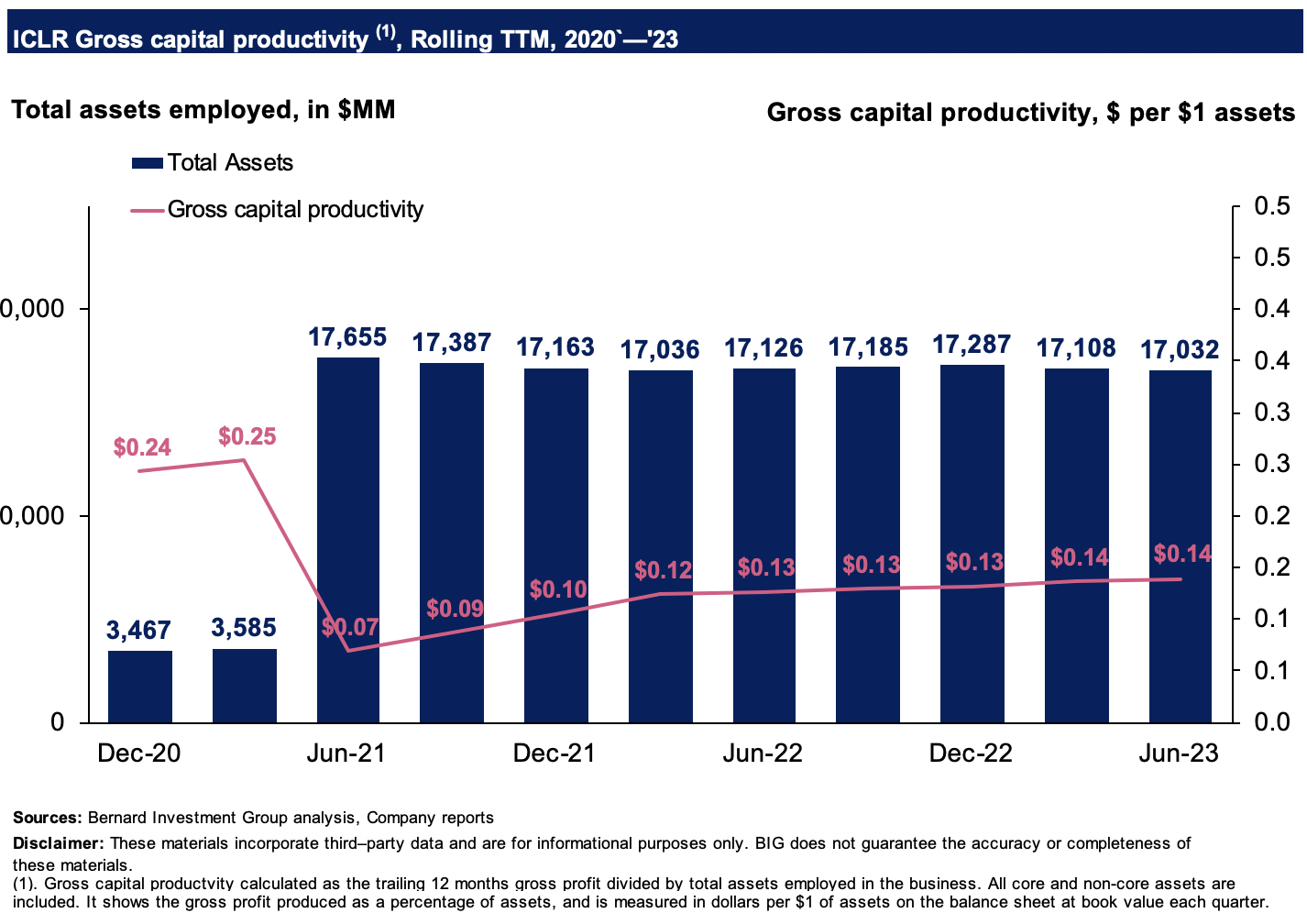

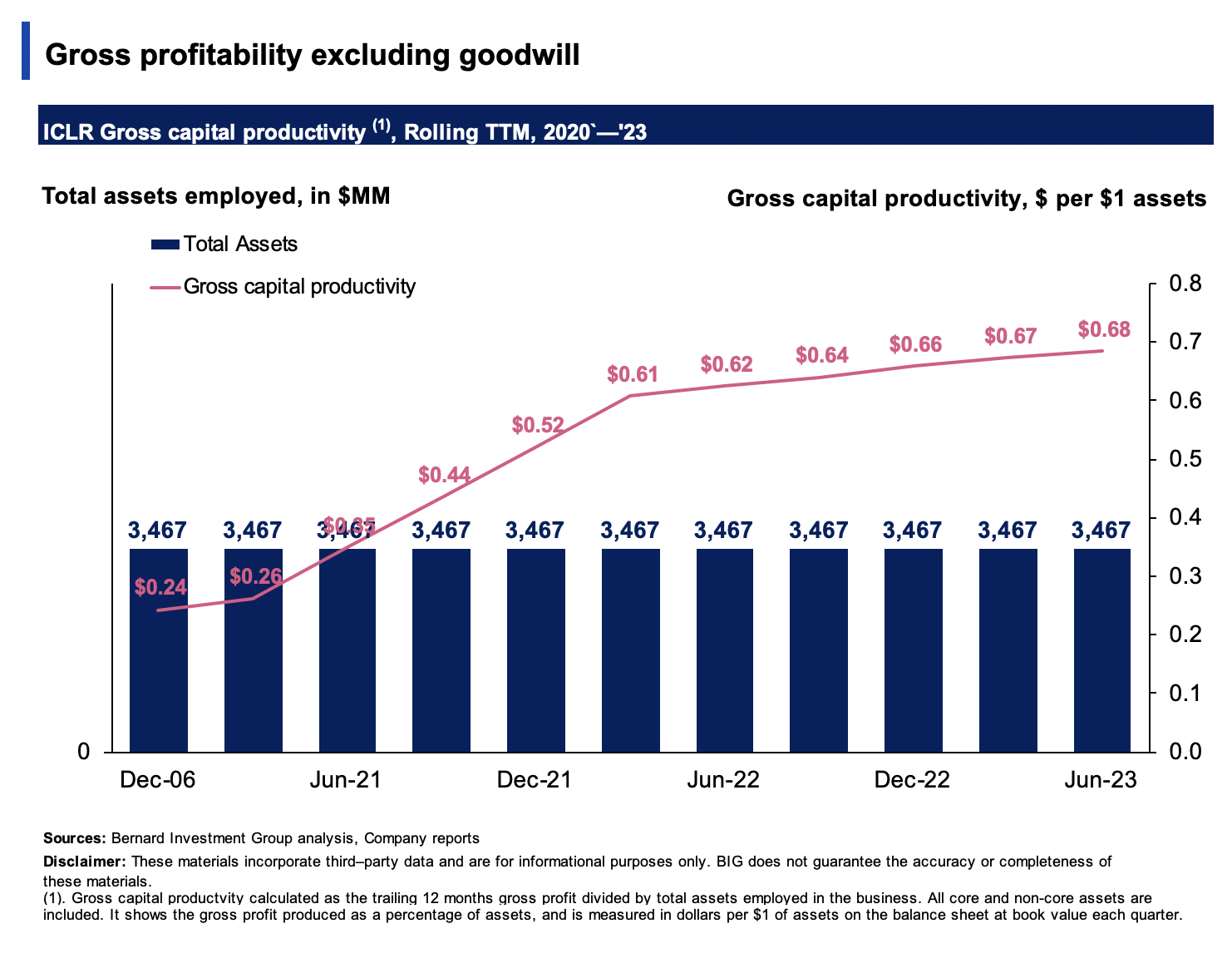

- Long term (3 years+). Mixed outlook at this point in time. I touched on this in the last analysis - the disconnect in business returns to market values. The point is ICLR is now an asset-heavy business. Since completing the PRA Health Sciences acquisition in '21, it now rotates back just $0.14 in gross per $1 in assets employed on the balance sheet. Around 50% of that asset value is in goodwill, granted. Strip goodwill out, and you have a company doing up to $0.68 in gross per dollar of assets. Time will see if the investment materializes.

Figure 3.

{kind=link}

Figure 4.

{kind=link}

Valuation and conclusion

There is expensive growth on the table in buying ICLR today. You are paying $21 per $1 in future earnings, 14% premium to the sector. You would also pay 16-17x EBIT and 2.5x book value. With an ROE of 6%, the investor ROE of 3% drops to 3% when paying the 2.5x multiple, and you're buying a 3% cash flow yield at ICLR's current marks.

I wouldn't suggest any of these offerings are of value. So the investment can't be rated a buy on valuation. The business underneath this valuation is sensible and deserves to keep this kind of multiple. Second, there have been 9 revisions to ICLR's earnings over the last 3 months. Third, the company's projections are notable.

In that vein, unless you're willing to pay a premium of around 14% to the sector, then you won't be satisfied with ICLR at 21x earnings. There are more selective opportunities with better-starting multiples in my opinion. This supports a neutral viewpoint.

Figure 5.

{kind=link}

In short, we have on our hands a balanced investment debate. On the bullish side, we have sales + earnings growth, decent business returns ex-goodwill, and stable FCF per share. On the less optimistic side we have pricey valuations and an asset-heavy business model, mostly tied up in goodwill. The point is that with all that has changed since my last analysis, there isn't enough to get me hungry enough to start allocating again at 21x earnings. Below the sector multiple of 18.5x might be more attractive, of closer to 1x book value, as you're only getting 6% ROE anyhow. Net-net, I reiterate my judgement on ICLR as a hold.

For further details see:

ICON: Starting Valuations And Business Returns Are 2 Major Hurdles