IPWR - Ideal Power: Future Looks Bright But Wait For The Wheels To Start Spinning

2023-10-26 07:34:17 ET

Summary

- Ideal Power Inc. is heavily involved in the EV market with its B-TRAN semiconductor switch technology, which offers cost savings and performance benefits for EV manufacturers.

- The company's B-TRAN technology has the potential to revolutionize the power switching market and create more sustainable and efficient power systems.

- While IPWR has significant growth potential in the EV market, it currently does not generate significant revenues and investors should wait for concrete revenue growth before considering investment.

Investment Rundown

Ideal Power Inc (IPWR) is an exciting and interesting company that is engaged in the EV market quite heavily. Their technology revolves around their B-TRAN product which is a semiconductor switch essentially. There are several advantages that we will cover below, but to keep it short, it enables lower costs and solid performance metrics for EV manufacturers. My rating concludes a hold right now for the company, much because I want to see concrete revenue growth and get a better picture of how it may look for the company. Right now the business doesn't generate any significant revenues, or none at all really, just whatever they get from milestone payments or some project completions.

The future looks bright though and I think maintaining exposure to it seems advisable, but to gauge a better investment opportunity I think it is also advisable to wait until revenues start to come in, which is most likely going to be both next year and the years beyond that. Estimates are for $1.4 million in revenues next year, which puts IPWR at a very expensive FWD p/s of 34, one not worth paying despite the potential growth opportunities.

Company Segments

IPWR is at the forefront of innovation, dedicated to advancing and bringing to market its pioneering bidirectional bipolar junction TRANsistor solid-state switch technology. One of its notable offerings is the SymCool Power Module, engineered to cater to the specific requirements of the solid-state circuit breaker market, with a focus on minimizing conduction loss.

{kind=link}

Although the EV market represents a substantial opportunity for B-TRAN power switches due to their potential to enhance mileage and reduce battery size, key considerations regarding product design cycles must be factored in. These cycles typically span 3 to 5 years, meaning that near-term revenue generation, apart from milestone payments derived from development projects, may not be immediately forthcoming.

Markets They Are In

IPWR continues to make significant progress toward the commercialization of its groundbreaking B-TRAN technology. B-TRAN boasts the potential to revolutionize the power switching market with its exceptional bidirectional switching capabilities, significantly reducing switching and production losses while simultaneously optimizing its thermal efficiency.

{kind=link}

The commercialization of B-TRAN represents a notable step forward for IPWR and the broader power electronics sector. As the technology matures and finds broader adoption, it could potentially redefine the way power is managed and converted, offering a compelling solution for modern energy challenges and fostering more sustainable and efficient power systems. Investors and industry observers are keenly watching IPWR progress as B-TRAN inches closer to market availability.

{kind=link}

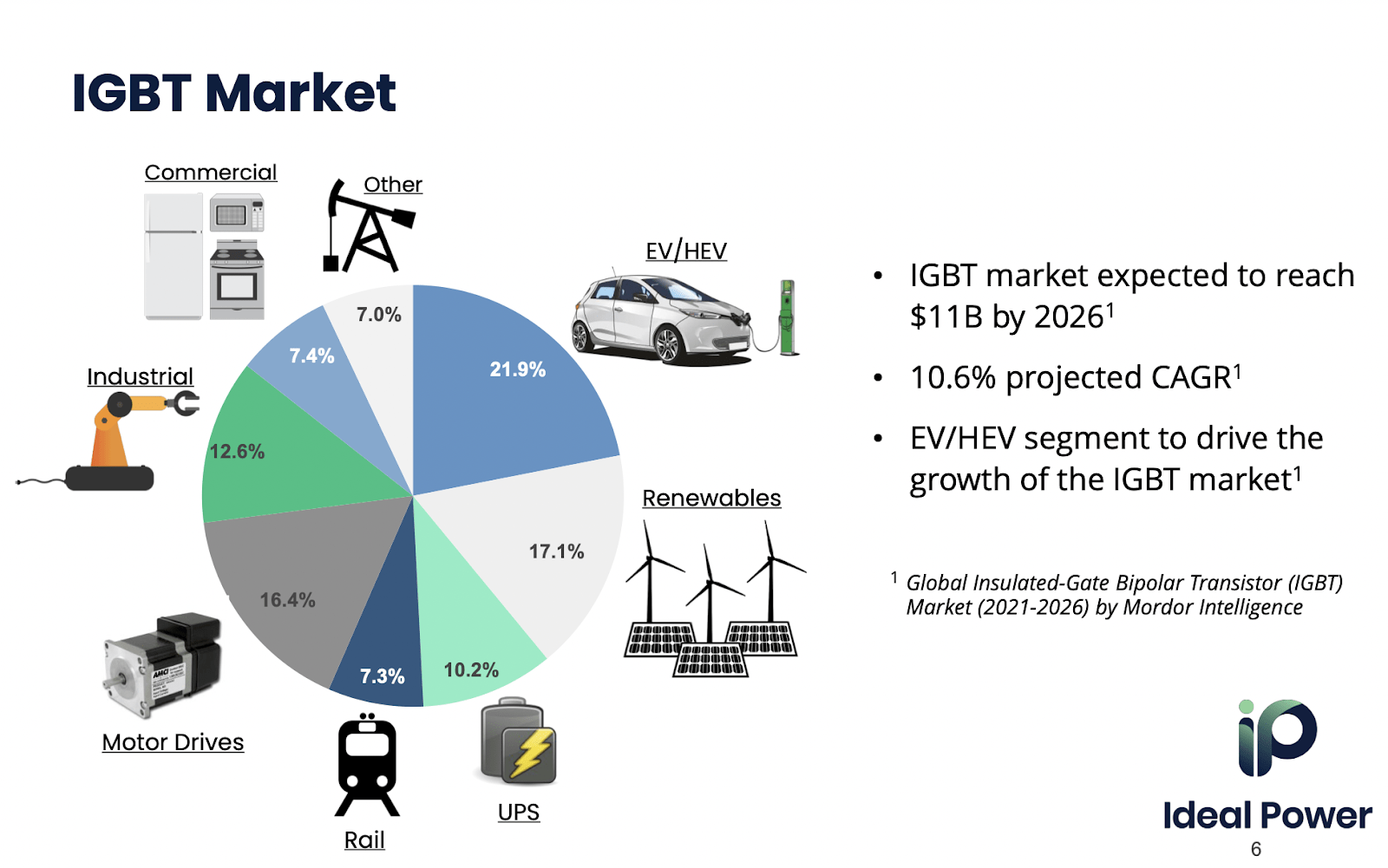

With the market that IPWR is set to reach over $11 billion in valuation by 2026, it presents a solid opportunity for the company to generate significant amounts of revenue. Should they gather up just 5 % of this market that would equate to roughly $550 million in annual revenues. With the market cap under $50 million right now it offers a decent risk/reward for simply holding shares in my opinion. The main industry that is driving this growth is EV manufacturing. Just the last few years the sale of EV cars has more than tripled, and the outlook seems better than ever for the industry. There might be some short-term pain now as interest rates have risen, but I think it's unlikely it will substantially suppress long-term growth.

Setting some price targets for the company, I think that in due time it seems likely that IPWR can gather up a substantial amount of market share, much because of the large amount of patents already gathered and the advantages of the technology. Should they achieve around $300 million in revenues by 2030, which if the market grows in a similar pattern would mean a market share of around 1 - 2%, something quite reasonable I think. With the current market cap being under $50 million and setting a fair p/s of 1 means an upside of $250 million in valuation or roughly 5x from current levels. Should the shares continue on their current dilution rate we might be looking at shares outstanding of around 20 million by then. This would equate to revenue per share of $15 and with a p/s of one we land at that same price target. over 7 years that becomes a CAGR of 12.4%. This is beating out most index funds by a fair bit, but I am not willing to take the risk and add more until we see these revenues begin to manifest, for the moment I do rate it a hold, and expect there to be quite a lot of volatility given the small market cap it currently has.

Risks

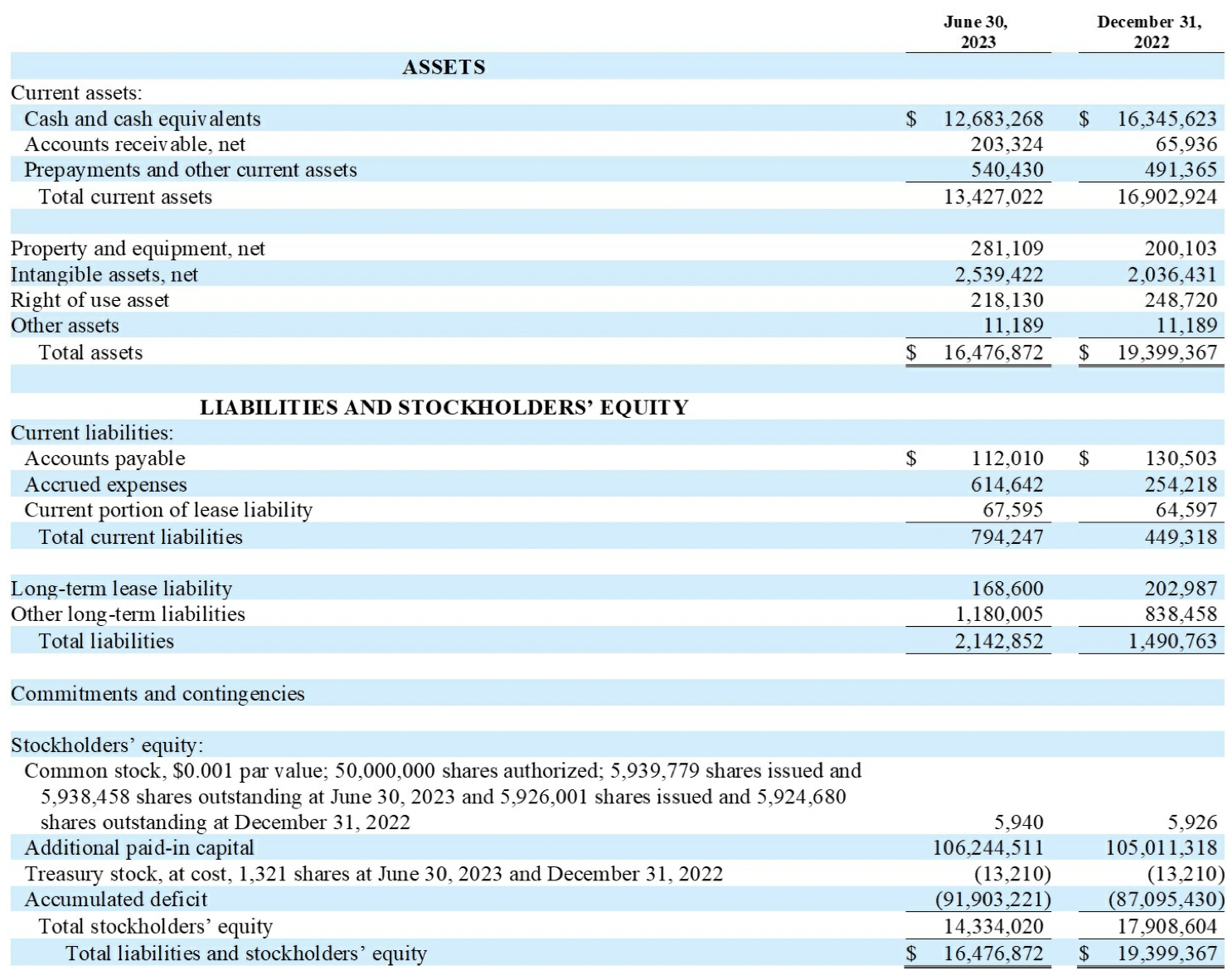

The apparent risk here revolves around the potential discrepancy between the company's expectations of market acceptance and the actual pace at which it occurs. In the event of a slower market uptake, the company might find itself in need of additional financing to bridge the gap. This supplementary funding could likely take the form of share dilution, which may not be unfamiliar territory for the company, especially given the fact that its shares have nearly doubled in value since 2020 and show the potential for further growth over the next 3 to 5 years. With the company being completely debt-free right now I do think a substantial amount of the risk is not present. There isn't a fear of IPWR needing to issue shares to pay the debt, but rather to finance operations. Operating expenses in the last 12 months have grown to $8.8 million, the highest in the company's history. Cash covers this by around 1.5x, but should debt be taken on in 2024 then the book value would decrease and that metric IPWR may look even more expensive. It already has a p/b premium of 45% to the rest of the industrial sector.

Shares Outstanding (Seeking Alpha)

It's important to note that an accelerated or unchecked dilution of shares could raise concerns in the market, potentially leading to a reduction in the company's valuation. Managing the balance between securing necessary financing and preserving shareholder confidence is a delicate tightrope act, underscoring the importance of prudent financial planning and clear communication with investors as the company navigates the road ahead.

Financials

Looking at the financials is perhaps the most important here I think. Seeing as there are no revenues yet being generated that makes it reasonable to base a valuation on that.

{kind=link}

Looking at the balance sheet we can see a depreciation in the cash position by around $4 million since the end of 2022. This is because IPWR needs to cover operating expenses which is perfectly natural given the state of their business. What I find the most appealing here though is the debt position, or rather lack of it. IPWR has been able to survive and grow without taking on too much debt and overleveraging themselves. This I think speaks very well of how IPWR will fare in a higher interest rate environment, meaning it will be less affected. Debt will essentially not be a cause of lower net earnings, but it doesn't stop the fact the bottom line is negative and causes IPWR to dilute to fund operations.

All in all, the financials look solid and I do expect more dilution of shares, but it seems a better route to go down rather than taking on debt when rates are high and capital expensive.

Final Words

IPWR is a very small company so allocating a smaller portion of a portfolio to them is advisable in my opinion to keep proper risk management. The price has fallen in recent months but I don't think the risk/reward is at a point where it makes sense to buy. I want to see revenue improvement before suggesting something higher. As we have covered though, the market opportunity is massive, and should IPWR gather a small single-digit market share it presents a strong ROI for investors. Concluding, though, I view IPWR as a hold for now.

For further details see:

Ideal Power: Future Looks Bright But Wait For The Wheels To Start Spinning