IDYA - Ideaya Biosciences: Eye Cancer Therapy Drives Gains - More Upside Ahead

2023-08-11 15:41:02 ET

Summary

- Ideaya Biosciences has made strong progress in the treatment of ocular cancer, with its stock price increasing over 150% since its IPO.

- The company's lead candidate, Darovasertib, has shown promising results in Phase 2 studies, with high response rates and a tolerable safety profile.

- Ideaya has initiated a potential registration-enabling Phase 2/3 clinical trial in combo with Pfizer's Xalkori - the market opportunity could be $500m - $1bn.

- Daro could succeed as a monotherapy in uveal melanoma also - the label expansion opportunities would be significant.

- GSK is a development partner on two other programs with development and milestones pledged of ~$1bn per candidate - the outlook for Ideaya driving further share price is positive in my view.

Investment Update - Ideaya's Strong Progress In Ocular Cancer

Ideaya Biosciences ( IDYA ) is a "precision medicine" oncology company that IPO'd in May 2019, raising $57.5m via the issuance of 5.75m shares at $10 per share. The stock price is currently trading at $25.50 - up over 150% since the IPO.

I last covered Ideaya for Seeking Alpha in June last year, giving the company a "Buy" recommendation, based on its diverse range of opportunities, Big Pharma partnerships, and upcoming data readout for lead candidate Darovasertib, a small molecule protein kinase C ("PKC") inhibitor indicated for genetically-defined cancers having GNAQ or GNA11 gene mutations, in combination with crizotinib, an investigational cMET inhibitor, in patients having metastatic uveal melanoma ("MUM").

Since my "Buy" recommendation, shares have risen >110% in value. The first jump in valuation occurred, as I had predicted, in September last year, when Ideaya released data from the 37-patient Phase 2 combination study, at the expansion dose of 300mg twice-a-day darovasertib and 200mg twice-a-day crizotinib. Crizotinib is marketed and sold by Pfizer ( PFE ) - one of Ideaya's three major Pharma partners, the others being Amgen ( AMGN ) and GSK ( GSK) - under the brand name Xalkori, earning >$400m of revenues in 2022.

Study Results Strong Enough To Move Into A Registrational Study

89% of patients showed tumor shrinkage in any-line MUM, with an 83% disease control rate. In first-line MUM, 4 of 8 evaluable patients had a confirmed partial response, and the Overall Response Rate ("ORR") across all 35 patients was 31% (11/35).

The median Progression Free Survival ("PFS") had not been reached, but was more than five months in evaluable first line MUM patients. The safety profile also appeared to be tolerable - according to the data press release:

Patients reported predominantly Grade 1 or 2 drug-related adverse events: all patients experienced a drug-related AE, of which 76% were reported as Grade 1 or 2 and 24% were reported as Grade 3.

One patient using darovasertib as a monotherapy experienced a 75% reduction in their eye lesion after just two weeks on therapy, with observed improvement in visual symptoms, while a darovasertib / crizotinib combo patient achieved tumor shrinkage of ~67%.

After the data were reported, Ideaya shares doubled in value, leaping from $9, to $18 in value. Dr. Matt Maurer, M.D., Vice President, Head of Clinical Oncology and Medical Affairs at Ideaya commented that:

The clinical efficacy observed in first-line patients in these interim Phase 2 data presents an opportunity to pursue a front-line strategy and provides a rationale for a potential registration-enabling clinical trial in MUM.

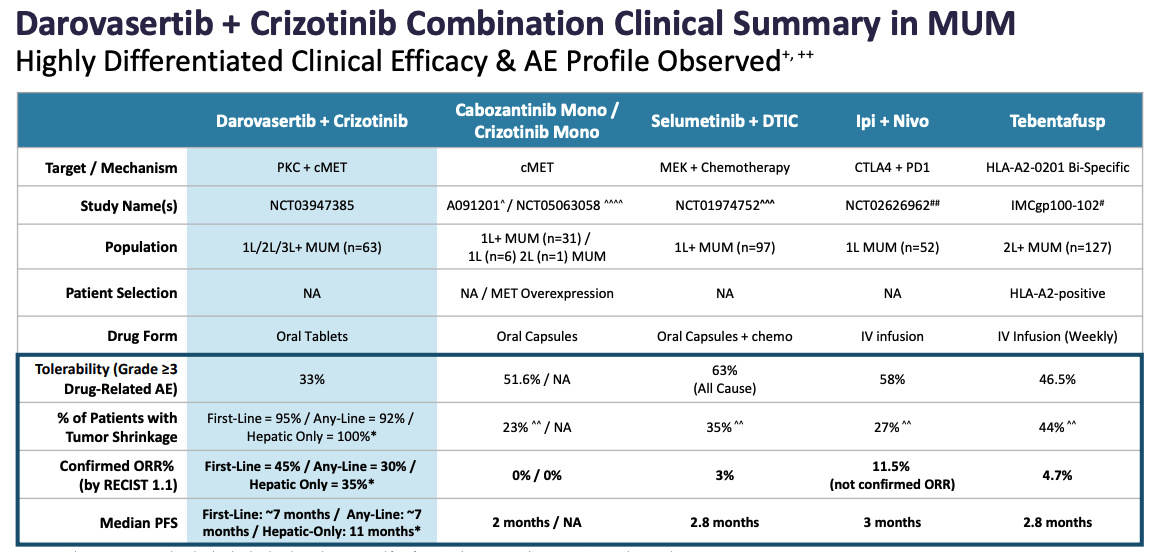

In April this year, the share price surged again - reaching a high of $25 by early June - as Ideaya released final data from the Phase 2 study, with a confirmed ORR of 45%, disease control rate ("DCR") of 90%, and median PFS of ~7m in the 20 evaluable first line patients. Across 63 any-line patients, the ORR was 30%.

{kind=link}

MUM is an indication with a patient population of ~4.5k patients across the US and Europe, Ideaya estimates, and as we can see in the slide above - from an Ideaya presentation - the combo of Darovasertib + Crizotinib has returned best-in-class data versus several key rivals.

Although clinical trial comparisons can often be misleading, the combo's data appears superior to Crizotinib as a monotherapy, selumetinib - marketed and sold as Koselugo by AstraZeneca ( AZN ) in the indication of neurofibromatosis, earning ~$200m per annum - + dacarbazine ("DTIC), Bristol Myers Squibbs' ( BMY ) well established Opdivo (nivolumab) / Yervoy (ipilimumab) combo, and Tebentafusp - approved by the FDA to treat MUM under the brand name Kimmtrak, but only in HLA-A2 positive patients where its data - not shown in Ideaya's table - is much more impressive. Kimmtrak - developed by Immunocore ( IMCR ) - market cap ~$2.9bn - earned ~$140m of revenues in its first year on the market.

After discussions with the FDA, Ideaya has now initiated a potential registration-enabling Phase 2/3 clinical trial in Q2 2023 in first-line HLA-A2 negative MUM patients, that will include an open label study with Phase 2 patients continuing on treatment, and a 230-patient study that will compare Darovasertib + Crizotinib against Opdivo / Yervoy, and a PD1 inhibitor, likely Merck's mega blockbuster cancer drug Keytruda. The primary endpoints will likely be PFS or Overall Survival ("OS"), or both.

Market Opportunity & Label Expansion Possibilities

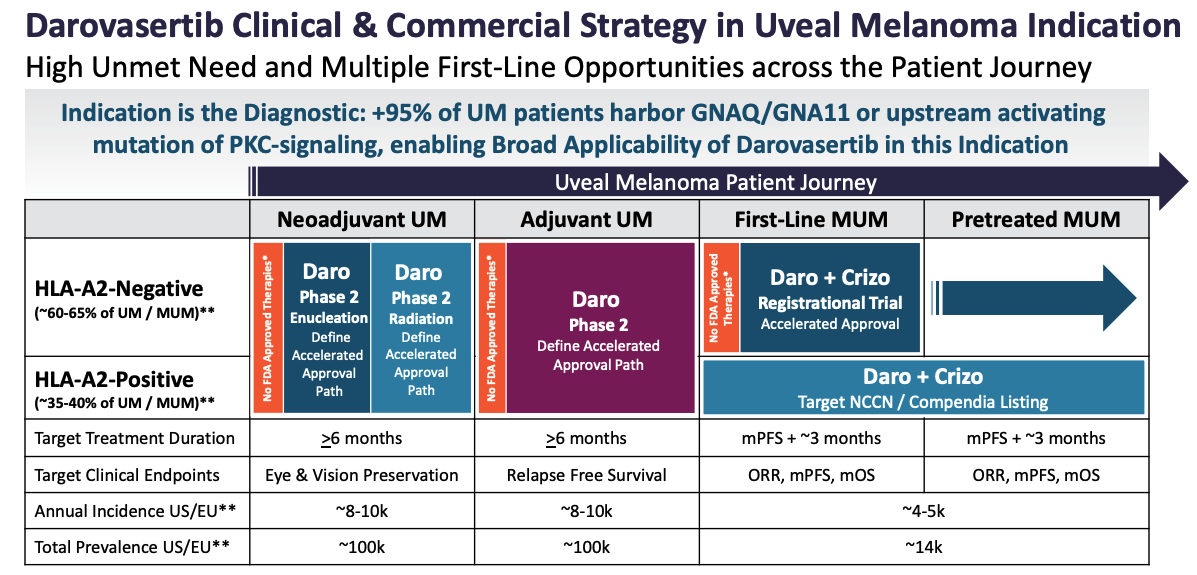

As mentioned, the addressable patient population should Daro + Crizo be approved in HLA-A2 negative MUM - and the combo has already been awarded a Fast Track designation by the FDA, and an Orphan Drug Designation (meaning the combo would have seven years of statutory marketing exclusivity) - would be an initial ~4k patients.

Kimmtrak apparently costs ~$400k for a course of treatment, therefore a theoretical market opportunity in this indication could be ~$1.6bn - analysts have suggested a more modest figure of $400m in the US - if European approval is also secured, that figure may well double, perhaps giving the combo a shot at achieving blockbuster (>$1bn per annum) peak sales.

Even that may be significantly undervaluing the opportunity in play, however, as the Phase 2 studies also showed that Daro could be effective as a monotherapy in the adjuvant and neoadjuvant settings. A Phase 2 study has been initiated in these indications, with data potentially being shared at the European Society for Medical Oncology conference ("ESMO") in October.

{kind=link}

As we can see above, Ideaya believes the adjuvant and neo-adjuvant patient populations are twice as large as first-line MUM, being 8-10k patients, and the drug may not be restricted to HLA-A2 negative patients in these indications, meaning it could target Kimmtrak's market share.

While the market's enthusiasm for Ideaya over the past 12 months has been evident, with shares up >40% so far this year, the company's market cap is "just" $1.5bn. Given a rule of thumb that a commercial stage biotech / pharmaceuticals typically trades at ~3x sales, and considering the fact that Ideaya is plotting course to a market opportunity that may easily exceed $1bn per annum, you could make the argument that shares remain significantly undervalued, and there is still a triple digit percentage upside opportunity in play.

Ideaya - Pipeline ex-Darovasertib & Partnerships

The single-asset risk in relation to Ideaya is arguably not especially high, either.

{kind=link}

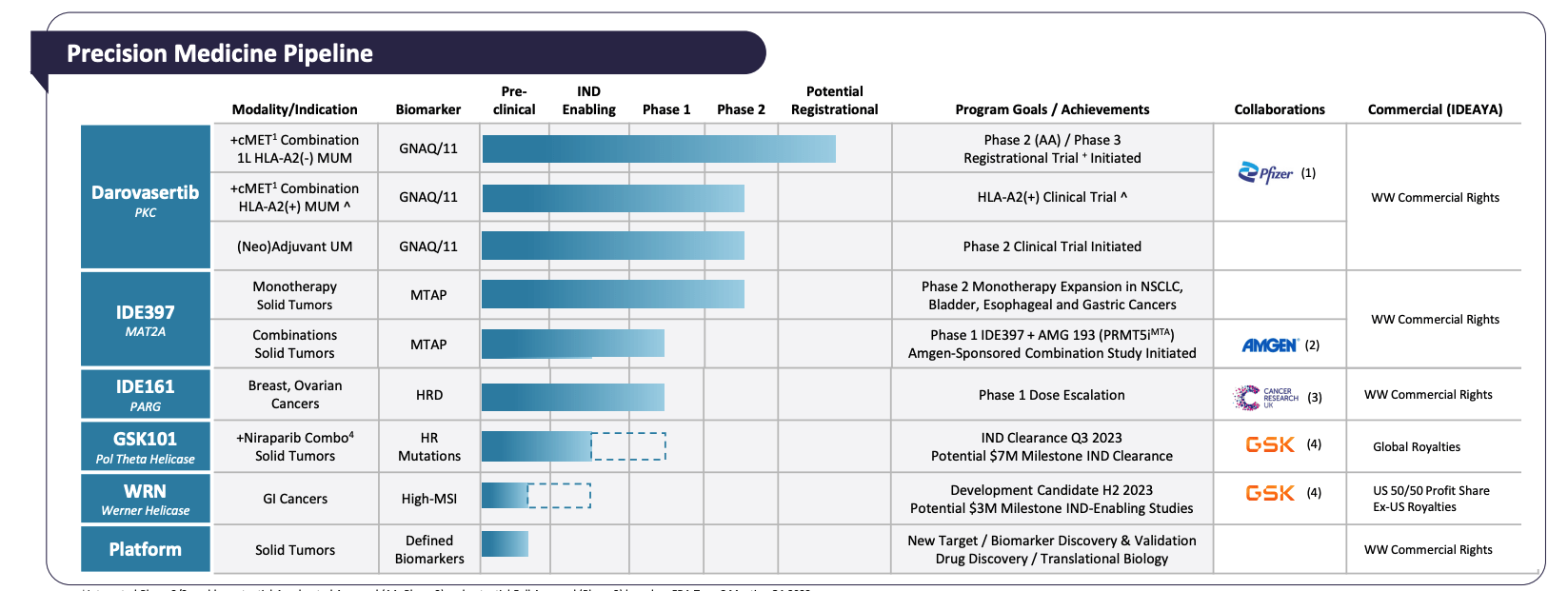

As we can see above, Ideaya has two other clinical drug candidates - IDE397, a small molecule methionine adenosyltransferase 2a, or MAT2A, inhibitor, and IDE161, a small molecule poly (ADP-ribose) glycohydrolase, or PARG, inhibitor.

IDE397 targets some of the largest cancer indications in its Phase 2 study. Although only ~15% of patients with solid tumors have MTAP deletion, that still likely represents a population large enough to support blockbuster revenues. Progress reported in Ideaya's Q2 2023 earnings press release - which the company released yesterday - showed that:

Preliminary clinical data for IDE397 shows responses in multiple MTAP-deletion high-priority tumor types based on experience across several patients in the early phase of the monotherapy dose expansion.

These include an earlier-reported unconfirmed partial response which was subsequently confirmed (~47% tumor reduction) in one of the high-priority tumor types and an additional observed~33% tumor reduction in NSCLC as measured by CT-PET.

Amgen has opted to enter IDE397 into a study alongside its candidate AMG-193 - an investigational methylthioadenosine- (MTA-) cooperative protein arginine methyltransferase 5 (PRMT5) inhibitor into a Phase 1/2 study of ~180 patients with solid tumors having MTAP deletion, with a planned expansion into the Non-Small Cell Lung Cancer ("NSCLC').

There are no milestone payments due from Amgen - both companies retain full commercial rights to their respective drugs - but study costs are shared, and it is encouraging to see that one of the US' largest Pharma companies has selected Ideaya as a partner.

GSK is a paying partner, however - Ideaya received an upfront payment from the UK based Pharma in 2020 of $100m, in exchange for access to Ideaya's "synthetic lethality" programs targeting methionine adenosyltransferase 2a ("MAT2A"), DNA Polymerase Theta ("Pol Theta" or "POLQ"), and Werner Helicase ("WRN").

Last August, GSK waived its right to co-develop IDE397 and several other compounds, causing the market to sell Ideaya and drive its share price under $10, but it retains interest in the POLQ programs, pledging $485m of development and regulatory milestone payments per program, plus $475m of commercial milestones per program.

The first of those programs is likely to secure an Investigational New Drug approval from the FDA - allowing in-human studies to begin - this quarter, and the same milestones apply to the Ideaya's WRN programs also.

Q2 Earnings & Financial Situation

Drug development is an expensive business, although Ideaya's spending is relatively modest compared to biotech's of a similar size, in my view. Net loss in Q2 2023 - announced yesterday - was $27.9m, and $49.9m across 1H23. The company was able to report a strong cash position of $510m, which management says are:

...anticipated to fund IDEAYA's planned operations into 2027 and support the company's activities through potential achievement of multiple preclinical and clinical milestones across multiple programs.

The company reported a modest $11.4m of collaboration revenues across 1H23 - down from $17m in the prior year period - net loss per share increased from $(0.93) in 1H22, to $(0.99) in 1H23.

Concluding Thoughts - Evidence Suggests Darovasertib Is Credible Approval Shot - Market Opportunity Supports Valuation Growth

To conclude this update on Ideaya, progress has been serene since my last note, with the initial promise of Darovasertib seemingly confirmed by the positive Phase 2 data. So far as I am aware, there are no clear timelines for when we may get a first look at the pivotal Phase 2/3 study data for Daro + Criz in MUM, but a best guess would be that data may be available early in 2024, and, if positive, approval granted in time for a commercial launch in early 2025.

That is a long time to wait, and biotech valuations typically drift downward in the absence of data catalysts, plus other factors - like GSK's waiving the opportunity to co-develop IDE397 for example, can create mini market sell-offs.

As such, although, as I have argued earlier in this post, approval of Daro / Criz could send Ideaya's valuation surging towards ~$3bn, doubling the current share price, cheaper entry points may present themselves in the next 12-18 months, particularly if other projects falter - the GSK programs, for example, or the Amgen collaboration.

In my experience, biotech valuations are disproportionately attached to the lead candidate, however, and given the label expansion opportunities associated with Daro as a monotherapy, a valuation of $3bn may even prove to be conservative for Ideaya - if the company has a bonafide blockbuster asset on its hands.

Another bonus is there seems to be not much in the way of competition for Daro - at least by drug development standards. Immunocore's Kimmtrak is an obvious competitor - although its data in HLA-A2 negative MUM is apparently poor - but otherwise, few competitors have advanced beyond Phase 1 studies in MUM, or with a PKC inhibitor.

Mentioned in Ideaya's 2022 10K submission ( annual report ) are Varian Biopharmaceuticals, Exscientia ( EXAI ), and HotSpot Therapeutics, whilst in the MUM indication, the biggest threat on the horizon appears to be Swiss Pharma giant Novartis ( NVS ), which has an antibody drug conjugate in a Phase 1/2 study.

In summary, investors should be aware that a study setback for a company like Ideaya can be a devastating blow - if any previously undetected safety issues emerge in the Phase 2/3 study or efficacy is not proven, I'd expect the share price to fall by at least half.

On balance, however, the road ahead for Ideaya with Daro looks somewhat promising, and may well support a significantly higher company valuation in time, in my view. I am looking forward to the ESMO monotherapy data in October, and will be monitoring the share price closely - the risk/reward in play with Ideaya seems to me to be unusually positive.

For further details see:

Ideaya Biosciences: Eye Cancer Therapy Drives Gains - More Upside Ahead