DOV - IDEX Corporation: Strong Growth Doesn't Change The Picture

2023-05-02 04:12:26 ET

Summary

- IDEX Corporation continues to expand at a rapid pace on both its top and bottom lines.

- Despite this, shares have failed to really appreciate alongside the market in recent months, but this is hardly surprising.

- Even a quality business that should continue to grow can become fully valued or overvalued, and this is no exception.

The problem with buying stock in companies that are trading at lofty levels is that, even when things go better than expected, you could experience some lackluster results from a shareholder return perspective. One really great example that I could point to of this taking place involves IDEX Corporation ( IEX ), a business that's focused on a variety of market segments such as the production of fluid and metering technologies, Various health and science fields, fire and safety products, and more. Much of the company's work centers around the production and sale of pumps, ceiling solutions, and similar products. Well, on April 26th, the management team at the business reported rather impressive results covering the first quarter of the company's 2023 fiscal year. Normally, you would think that this would warrant a surge of optimism. But in response to this development, shares of the company pulled back and are currently down 4.2% compared to where they were the day before earnings were announced. Those who are bullish about the company may view this as a good buying opportunity. But given how shares are currently priced, I do believe that there are better prospects to consider at this time.

Solid results weren’t enough

In late September of last year, I came to a conclusion about IDEX Corporation stock that I still hold today. Historically speaking, the company had continued to generate strong growth in both its top and bottom lines. A combination of robust organic growth, as well as acquisitions, helped to propel the company higher. In all likelihood, that growth looked set to continue. This led me to conclude that the company was a great player in that space. But because of how shares were priced, I had no choice but to rate it a ‘hold’ to reflect my view that shares had limited upside, especially relative to the broader market, for the foreseeable future. Since then, the company has more or less lived up to this rating. While the S&P 500 is up 8.1%, shares of it have increased only 0.6%.

{kind=link}

Author - SEC EDGAR Data

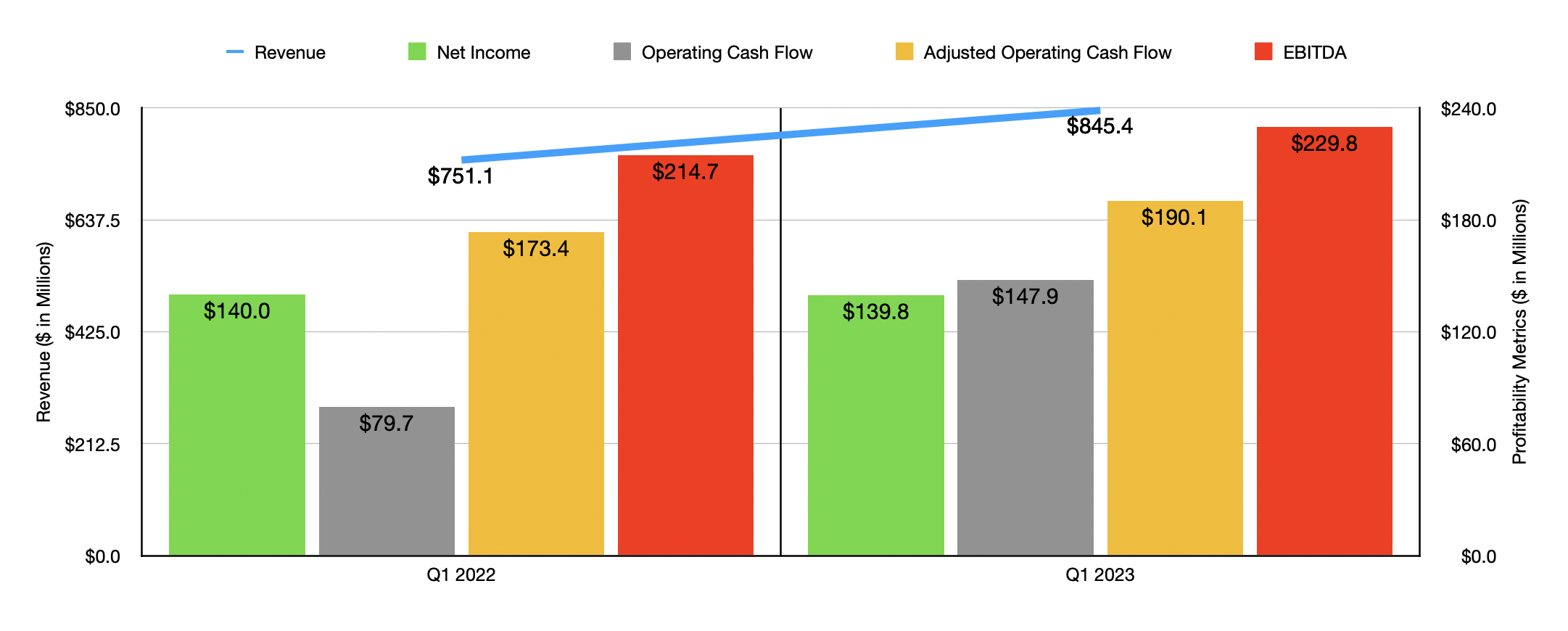

The most recent data provided by management covers the first quarter of the company's 2023 fiscal year that was just reported on April 26th. During that quarter, revenue came in at $845.4 million. In addition to being 12.6% higher than the $751.1 million the company reported one year earlier, it also represented outperformance compared to what analysts expected to the tune of $26.5 million. Given the company's history, it shouldn't be a surprise that the largest chunk of its growth came from acquisitions. In fact, in 2022, the company engaged in three sizable acquisitions. The last of these, which occurred in November of last year, was of Muon Group and was done in exchange for $713 million. This is not to say that the company did not benefit from organic growth. In fact, organic revenue was up 6% year over year. This growth came even in spite of a 2% headwind associated with foreign currency fluctuations.

On the bottom line, the picture was a bit more complicated. Net income for the company actually dipped slightly, falling from $140 million to $139.8 million. The biggest hit to the company came from a 23% increase in selling, general, and administrative costs. This was driven largely by acquisition activities, including amortization associated with its acquisitions. Higher employee-related costs were also a factor. On a per share basis, however, the company actually did better because of a decrease in share count. Earnings per share rose from $1.83 to $1.84. This beat analysts’ expectations by $0.07 per share. Adjusted earnings per share of $2.09 beat analysts’ expectations by the same amount. Other profitability metrics, however, performed incredibly well. Operating cash flow nearly doubled from $79.7 million to $147.9 million. If we adjust for changes in working capital, we would still get an increase from $173.4 million to $190.1 million. Meanwhile, EBITDA for the business expanded from $214.7 million to $229.8 million.

{kind=link}

Author - SEC EDGAR Data

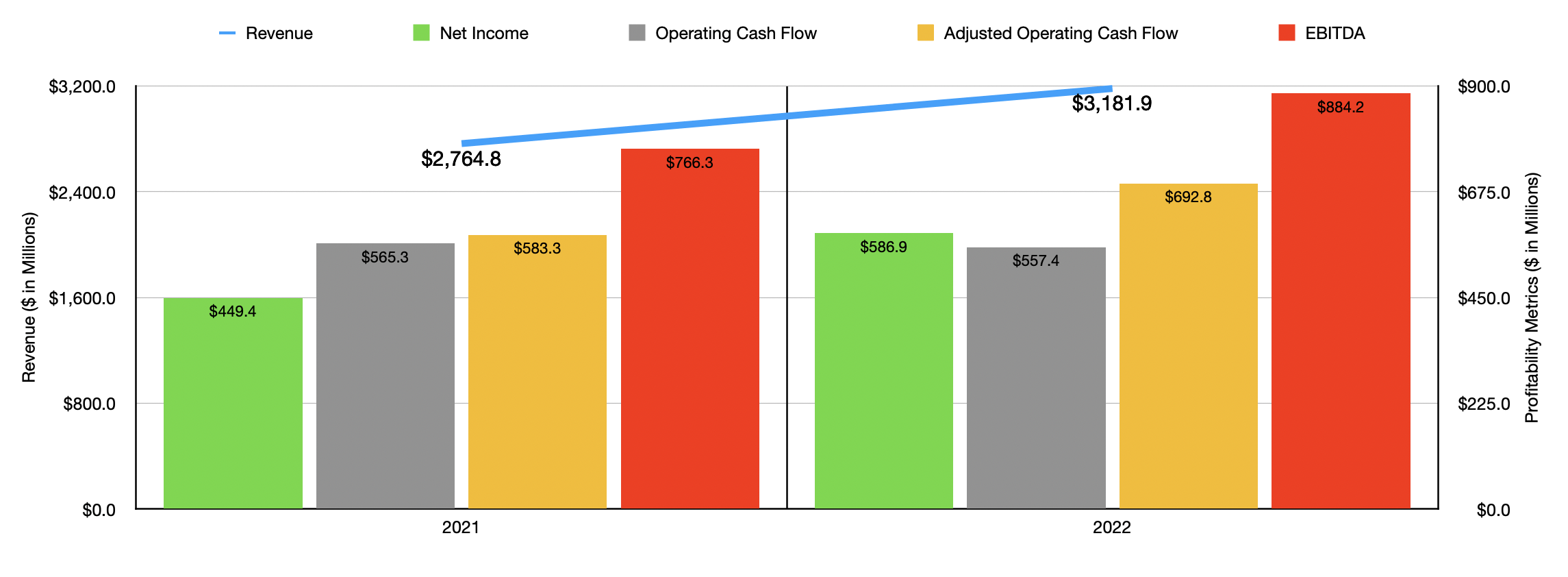

It is worth noting that the first quarter of the 2023 fiscal year was not a one-time thing. As I mentioned earlier in the article, the company has a solid track record for growth. In the chart above, for instance, you can see financial results from 2021 to 2022 . A combination of organic growth and acquisitions pushed revenue up from $2.76 billion to $3.18 billion. And with the exception of operating cash flow, every profitability metric for the company increased year over year as well.

To make matters even more perplexing, management does continue to expect growth this year. Though that growth certainly will be weaker than the market might prefer. Organic revenue this year should be between 0% and 3% above what it was last year. Overall revenue, meanwhile, should be between $3.33 billion and $3.40 billion. At the midpoint, this would translate to a year over year growth rate of 5.6%. We don't yet know the full impact of acquisitions, the most recent of which was announced just recently at a price of about $110 million. Earnings per share should be between $7.30 and $7.60, which translate to net profits of between $552.5 million and $576.5 million. Adjusted earnings per share should be higher at between $8.25 and $8.55. Management is also forecasting EBITDA of between $915 million and $946 million. If we assume that other profitability metrics will climb at the same rate that it's expected to, then we would expect adjusted operating cash flow of $729.1 million.

{kind=link}

Author - SEC EDGAR Data

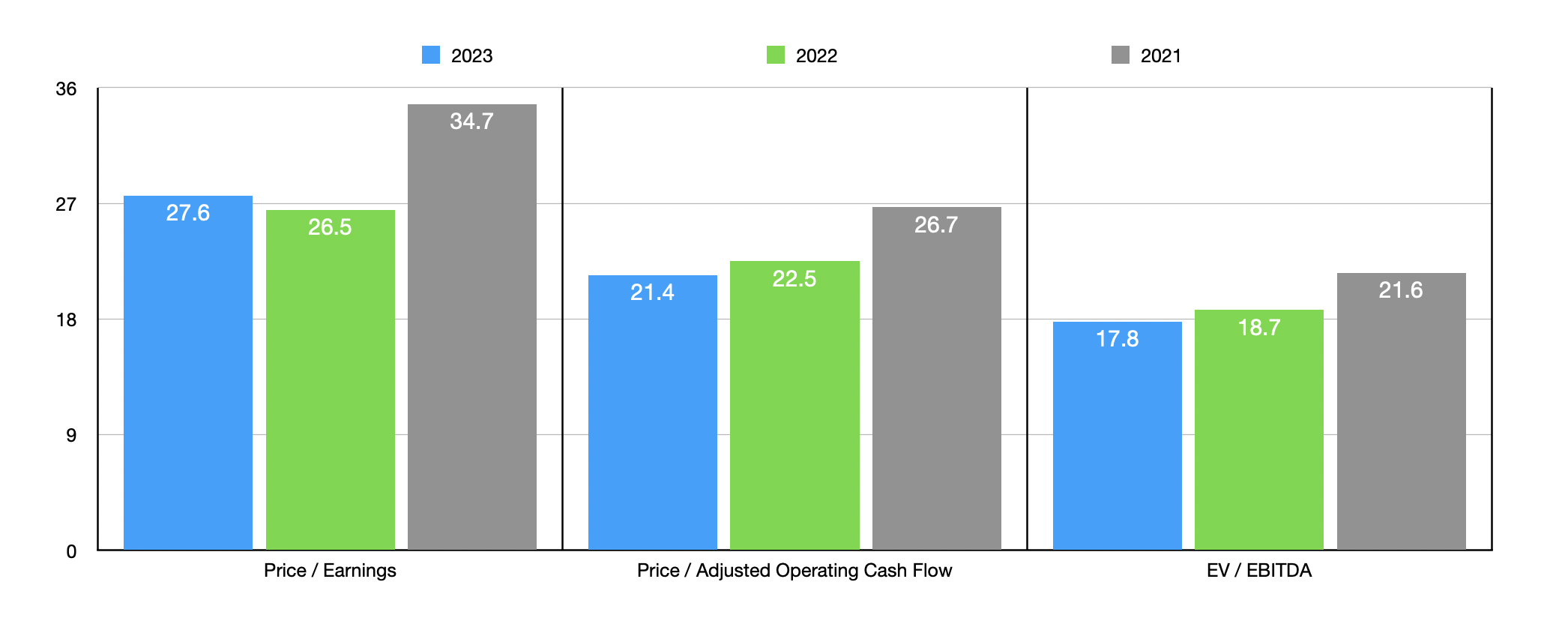

Taking these figures, and also using data from 2021 and 2022, I decided to price the company in the chart above. As you can see, shares do locate a bit lofty on an absolute basis, irrespective of the year that we rely on. Relative to similar companies, however, the firm does look to be either fairly valued or slightly on the cheap end. You can see what I mean in the table below where I compare the data from 2022 to the data from five similar entities. On a price to earnings basis, three of the five companies were cheaper than IDEX Corporation. But when it comes to the price to operating cash flow approach, only one was cheaper, while with the EV to EBITDA approach, two of the five were cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| IDEX Corporation |

| 26.5 |

| 22.5 |

| 18.7 |

| Xylem Inc. ( XYL ) |

| 53.0 |

| 31.5 |

| 27.1 |

| Dover ( DOV ) |

| 19.5 |

| 20.3 |

| 13.7 |

| Nordson ( NDSN ) |

| 25.2 |

| 24.2 |

| 17.6 |

| Stanley Black & Decker ( SWK ) |

| 12.7 |

| N/A |

| 21.4 |

| Ingersoll Rand ( IR ) |

| 38.5 |

| 27.2 |

| 19.0 |

Takeaway

I continue to be impressed by the quality and growth demonstrated by the management team at IDEX Corporation. The company is an interesting firm and it has a solid track record. I have no reason to doubt that it will continue to deliver like it has in the past. But this doesn't mean that the company makes for a great prospect. Yes, management did exceed analysts’ expectations on both the top and bottom lines. But because of how pricey shares are, the company only saw downside from a shareholder return perspective. Eventually, I have no doubt that the stock will go up. But while investors are waiting for that to happen, they are missing out on better opportunities elsewhere.

For further details see:

IDEX Corporation: Strong Growth Doesn't Change The Picture