IDXX - IDEXX: A Realistic Path To 12-14% Annual Returns

2023-11-02 12:27:23 ET

Summary

- IDEXX Laboratories operates in the veterinarian health sector and has experienced double-digit revenue growth in recent years.

- The company is facing short-term headwinds due to lower vet visits caused by economic challenges.

- IDEXX is focused on clinic efficiency, innovation, and expanding its commercial footprint to drive long-term growth, paving the way for elevated long-term gains.

Introduction

I'm a dividend (growth) investor. However, I also have some non-dividend-paying stocks on my radar - especially in industries with consistent growth, high entry barriers, and anti-cyclical demand. Healthcare is one of these sectors.

This brings me to IDEXX Laboratories ( IDXX ) .

On June 29, I initiated coverage in an article titled IDEXX: One Of The Best Compounders On The Market .

Founded in 1983, IDEXX operates in one of my favorite healthcare segments: veterinarian health. The company is focused on an area that not only allows it to make a lot of money but also has a big impact on animal health.

The company, whose name is based on IDX, the abbreviation for immunodiagnostics, specializes in the development, manufacturing, and distribution of products and services that provide veterinarians with diagnostics and information management-based products.

These in-clinic diagnostics solutions mainly target companion animals.

{kind=link}

IDEXX Laboratories

This is one of the fastest-growing healthcare markets, boosted by our love for dogs, cats, and other animals.

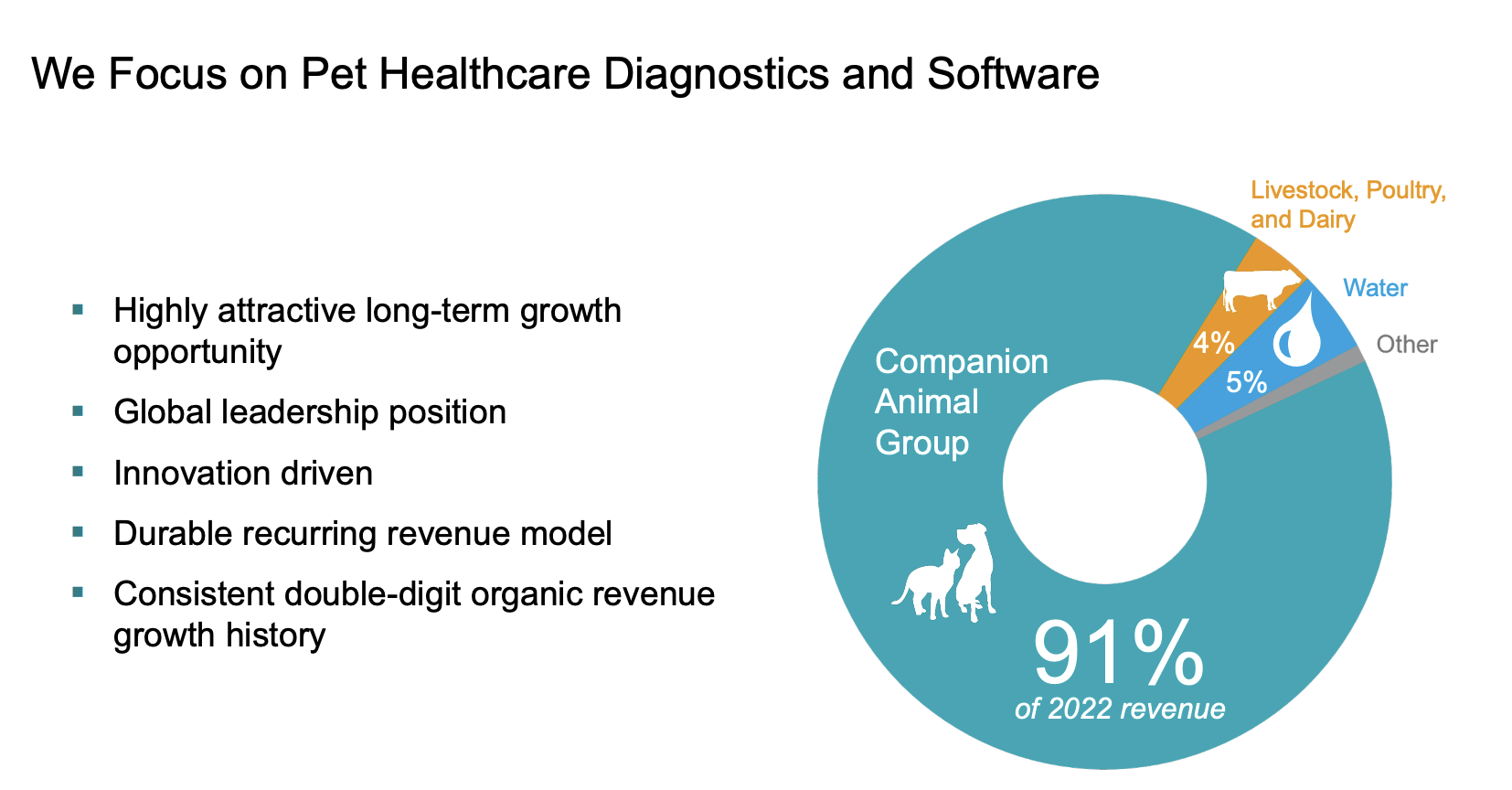

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Companion Animal Group | ||||

| 2,890 | ||||

| 89.9 % | ||||

| 3,059 | ||||

| 90.8 % | ||||

| Water | ||||

| 147 | ||||

| 4.6 % | ||||

| 156 | ||||

| 4.6 % | ||||

| Livestock, Poultry and Dairy | ||||

| 136 | ||||

| 4.2 % | ||||

| 123 | ||||

| 3.6 % | ||||

| Other | ||||

| 43 | ||||

| 1.3 % | ||||

| 30 | ||||

| 0.9 % |

Over the past few years, the company has compounded its total revenue by double-digits, generating most of its revenues from recurring operations and services.

This is one of the best qualities a wealth compounder can have, as it benefits from both a rising installed base and recurring revenues.

{kind=link}

IDEXX Laboratories

Even better, not only does the company benefit from secular growth in veterinarian health requirements, but it also benefits from anti-cyclical demand.

According to the company :

- 88% of pet owners say their animals have a positive impact on their mental health and well-being. I can attest to that.

- 84% say taking care of a pet's health is as important as their own health.

- 85% would reduce personal spending before cutting pet-related costs.

{kind=link}

IDEXX Laboratories

Furthermore, the company is serving just a tiny fraction of the total addressable market. In the U.S., its biggest market, it services just a fifth of the market.

{kind=link}

IDEXX Laboratories

Having said that, the reason I'm writing this article is to update my bull case.

As strong as IDEXX may be, it's running into some headwinds.

The problem is that economic growth has gotten so weak that we have reached the point where people are forced to cut spending, resulting in lower vet visits.

Hence, IDXX, which has returned 640% over the past ten years, is now in its steepest downtrend since the Great Financial Crisis, dropping almost 50% from its 2021 all-time high.

In this article, I'll walk you through its just-released earnings and explain what to make of the risk/reward.

So, let's get to it!

Long-Term Growth, Short-Term Headwinds

Even if fast-growing companies have strong long-term potential, shorter-term headwinds often result in valuation adjustments.

After all, companies that trade at "elevated" valuations need to justify these multiples.

With that in mind, the company is still doing well. Very well, actually.

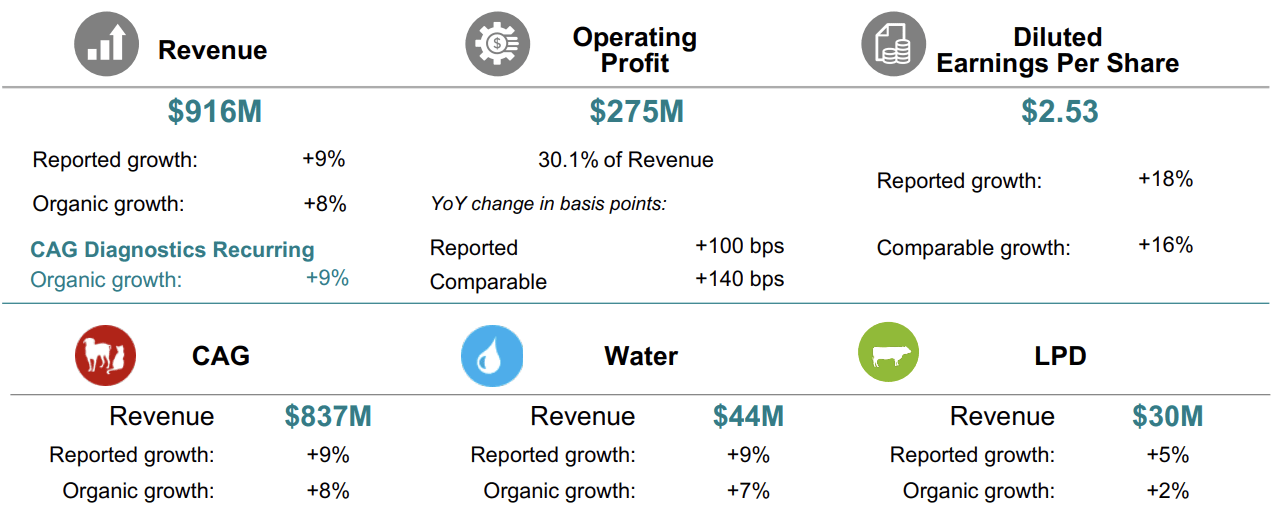

IDEXX achieved 8% organic revenue growth in the third quarter.

Key drivers were the sustained benefits from execution drivers, including premium instrument placements, new business gains, customer retention, and growth in recurring veterinary software revenues. CAG Diagnostics' recurring revenues were up by 9% organically.

{kind=link}

IDEXX Laboratories

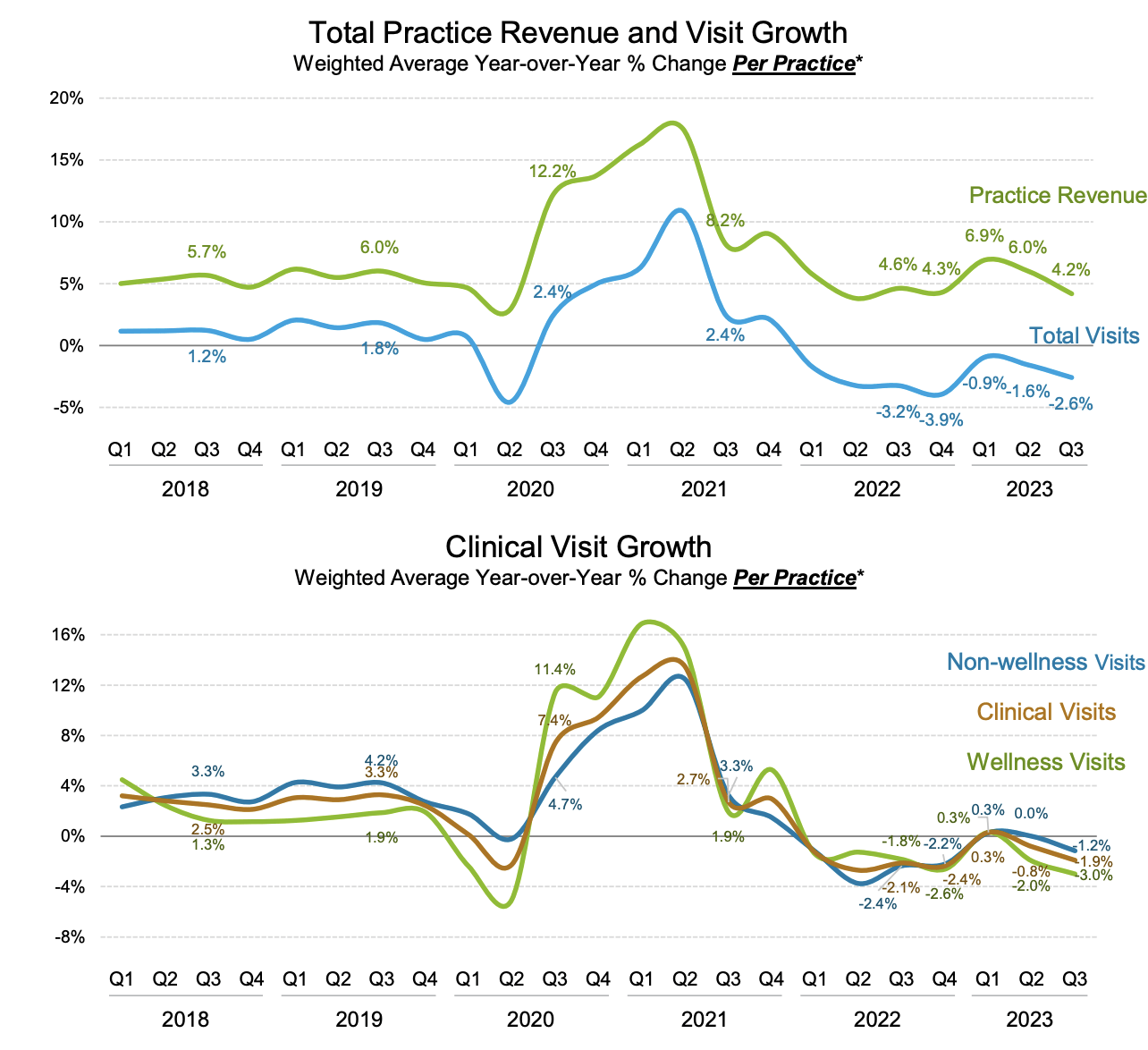

Unfortunately, the company saw a 2% same-store decline in U.S. clinical visits, below expectations, which is the issue I mentioned earlier, as consumers are not in a good place right now.

I think we are all aware of elevated inflation and the struggles some people have to get by.

While practice revenues are still growing (this includes pricing), total visits are down in all segments (non-wellness, clinics, and wellness).

{kind=link}

IDEXX Laboratories

Despite this, operating profit results exceeded expectations due to gross margin gains and operating expense leverage. Earnings per share reached $2.53 per share, an 18% increase.

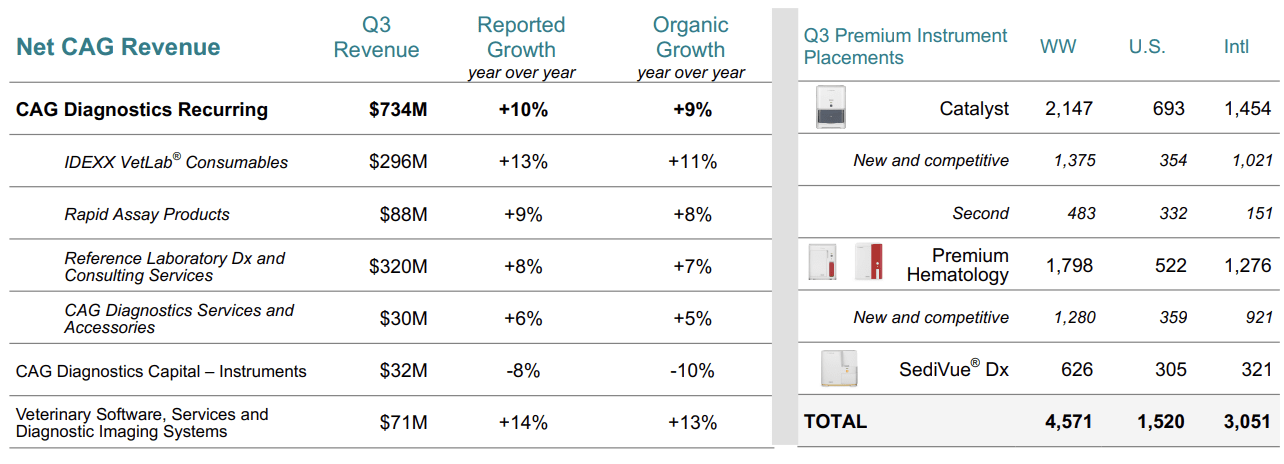

- CAG Diagnostics' recurring revenue increased 9% organically, with 8.3% growth in the U.S. and 10.3% growth in international regions.

- Veterinary Software and Diagnostic Imaging revenues grew by 13% organically, driven by recurring Software revenues.

- CAG instrument revenues were down 10% organically due to comparisons with high prior-year levels.

- IDEXX VetLab consumable revenues increased by 11% organically.

- Global Rapid Assay revenues expanded by 8% organically.

- Water revenues grew by 7% organically.

- Livestock, Poultry, and Dairy revenues increased by 2% organically, with strong U.S. gains.

{kind=link}

IDEXX Laboratories

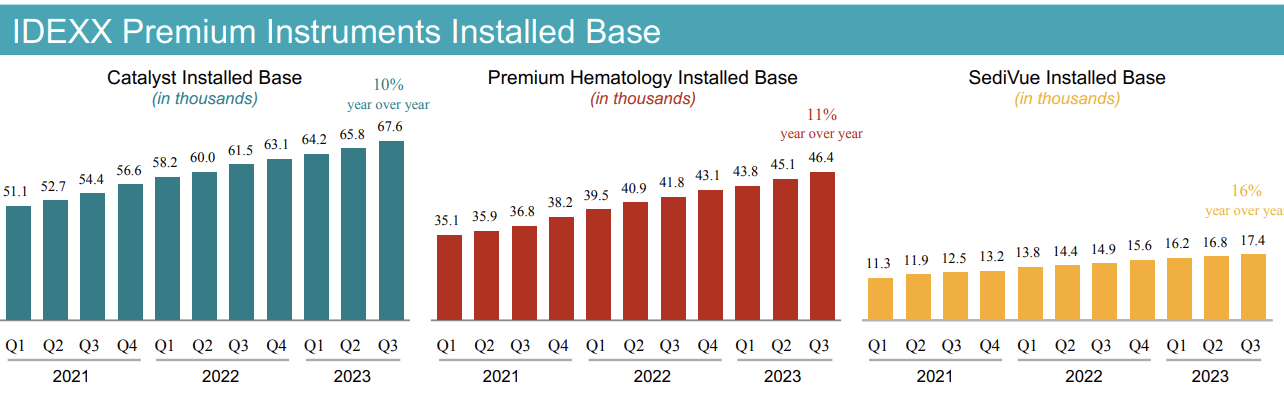

Regardless of the current headwinds, I like these results a lot, especially because the company's installed base continues to grow smoothly.

- The catalyst installed base is growing at 10% per year.

- The Premium hematology installed base is growing by 11% per year.

- The SediVue installed base is growing by 16%. This system analyzes urine.

{kind=link}

IDEXX Laboratories

Furthermore, gross profit increased 8% with a gross margin of 59.9%, up 30 basis points.

This gain was attributed to higher net price realization, business mix, and improved software service gross margins.

Operating expenses increased by 4%, but IDEXX is planning for a higher level of OpEx growth in Q4.

During its earnings call, the company noted that Diagnostics revenue remains the fastest-growing area of veterinary clinic revenues, driven by the need for testing to determine a patient's health status and treatment path.

Moreover, despite challenges in clinic visit levels due to capacity management issues and macroeconomic dynamics, productivity remains a top priority for veterinary clinics.

IDEXX solutions, particularly software-enabled multi-modality offerings, help clinics address these challenges.

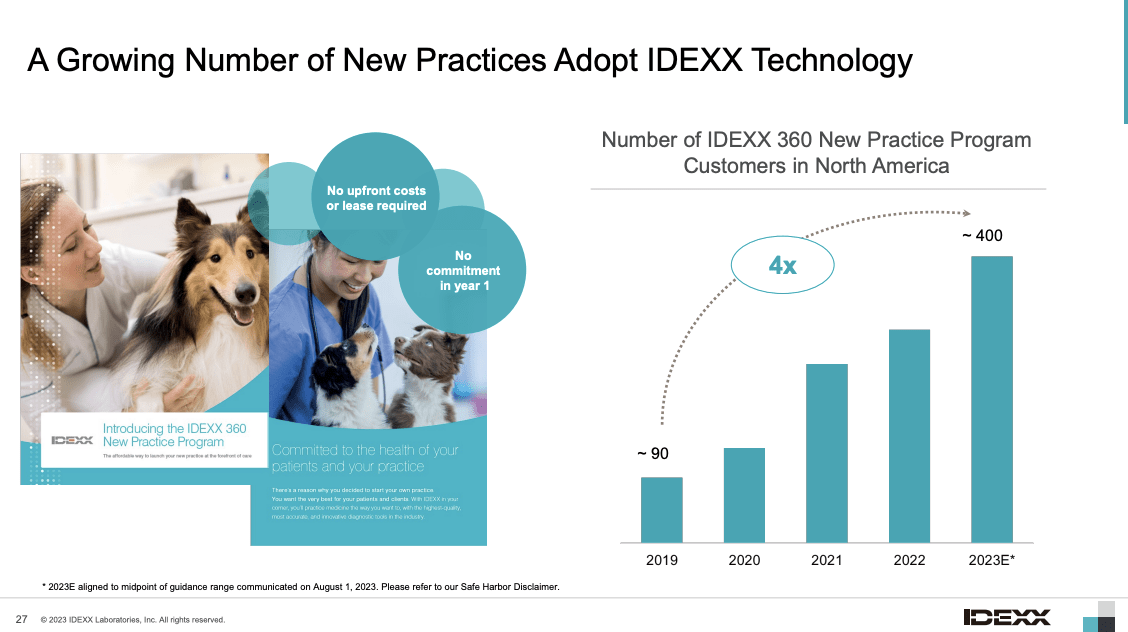

Hence, IDEXX is expanding its commercial footprint in the U.S., focusing on deploying its commercial playbook worldwide.

{kind=link}

IDEXX Laboratories

This includes focusing on the importance of software in improving clinic efficiency, with clinics embracing software to enhance patient processing, diagnostics interpretation, and pet-owner communication.

Cloud-based PIMS products represent a significant portion of placements, reflecting technology adoption trends.

As one can imagine, the company is also dedicated to advancing its innovation agenda, including an advanced test menu and assays that provide new clinical insights.

IDEXX has launched a new testing assay that helps detect kidney injury earlier and more definitively. Further expansions to the reference lab testing menu are expected.

The company also opened a new reference laboratory in Perth, Western Australia, to improve turnaround times for test results, as it aims to provide sustainable long-term value through the expansion of its global reference lab footprint.

As a result, despite headwinds, IDEXX has maintained its high-end reported EPS outlook and narrowed the full-year EPS guidance range. It now stands at $9.74 to $9.90 per share, with a $0.05 per share increase at the midpoint.

These adjustments are driven by changes in organic revenue growth and improvements in the company's operating margins.

Additionally, the company has a sub-0.5x leverage ratio, which indicates rock-solid financial health, meaning we don't have to worry about elevated rates.

So, where's the value?

Valuation

This is where it gets tricky.

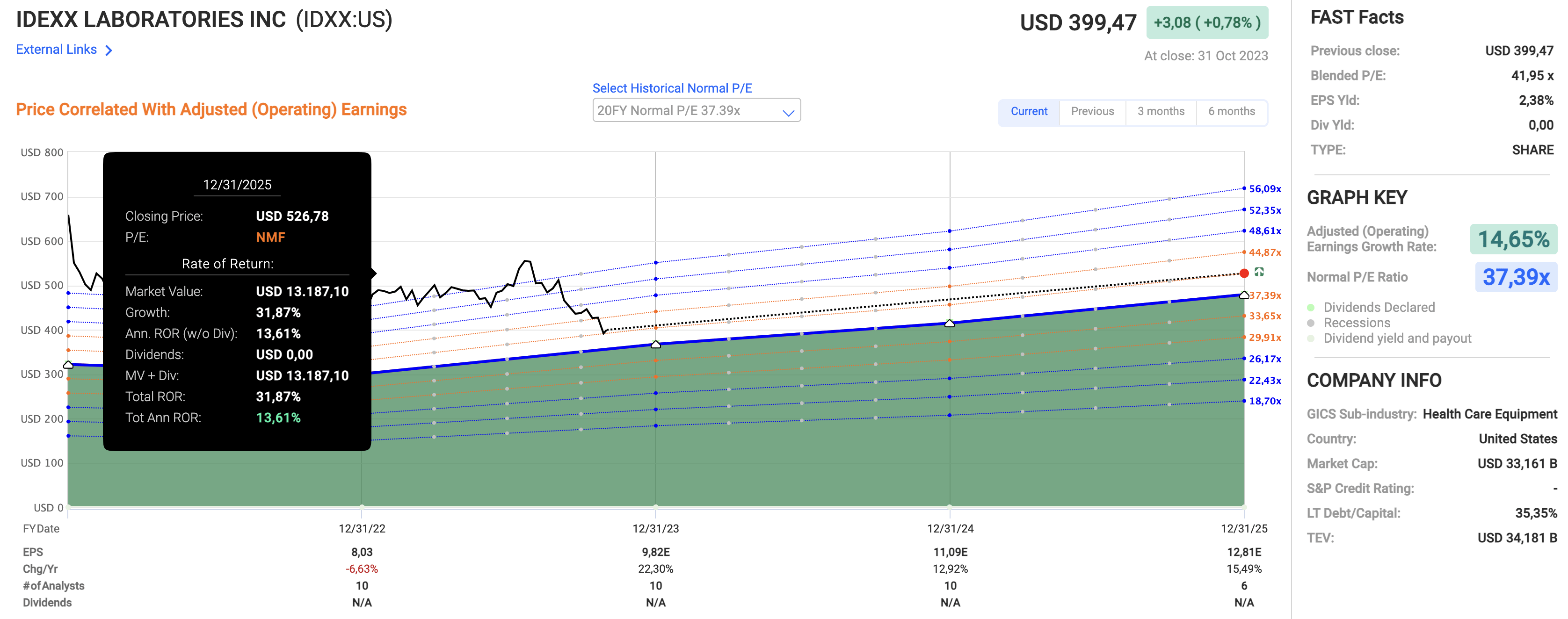

While the stock has almost lost half of its value since 2021, it's still trading at 42x earnings.

Although one might make the case that this is an elevated valuation, the company is expected to maintain high growth.

- This year, EPS is expected to grow by 22%.

- EPS growth is expected to slow to 13% next year, followed by a potential rebound to 15% in 2025.

- If the company maintains its current valuation, it could return 14% per year through 2025 (as seen in the chart below).

{kind=link}

FAST Graphs

Despite current headwinds, IDEXX is essentially as strong as it ever was. The only problem is that it was seriously undervalued during the first post-pandemic years, which required some selling.

The current consensus price target is $567, which is 46% above the current price.

Nonetheless, investors need to be aware that if the economy keeps deteriorating, we could see more selling. IDEXX could even hit $300, which I consider deep value.

I (obviously) remain Bullish , but I have to warn people that markets can stay irrational longer than impatient investors can stay solvent, especially if the Fed is forced to keep rates elevated despite a weakening economy.

On a long-term basis, I expect IDEXX to return at least 12% to 14% per year, outperforming the market and most healthcare suppliers.

Takeaway

While IDEXX is facing some short-term headwinds due to economic challenges affecting vet visits, it remains a strong player in the healthcare industry.

The company's long-term growth potential is supported by its ability to generate rapidly rising recurring revenues and a growing installed base.

IDEXX is adapting to the changing landscape by focusing on clinic efficiency and innovation, such as advanced testing assays.

Although the stock's valuation may seem elevated at 42x earnings, it's expected to maintain high growth.

With a consensus price target of $567, IDEXX offers the potential for significant gains.

However, in volatile markets, it's essential to exercise caution.

While I am bullish on IDEXX's long-term prospects, it's crucial to remember that markets can be unpredictable.

Nonetheless, IDEXX is well-positioned to outperform the market and its peers, with a potential return of 12% to 14% per year in the long run.

For further details see:

IDEXX: A Realistic Path To 12-14% Annual Returns