IDXX - IDEXX: Best In Class Growth And Recession-Resistant With Hefty Valuation

2023-07-21 09:59:48 ET

Summary

- IDEXX Laboratories, a leader in pet diagnostic and software products, is targeting 10%+ organic sales growth and 15-20% EPS growth, making it a high-quality company.

- The company is focusing on diagnostics penetration growth and software solutions, with Q1 FY23 showing a 9.8% increase in organic sales and a 14% organic increase in veterinary software and diagnostic imaging revenues.

- Despite the company's growth, the current stock price is considered overvalued, trading at more than 45 times the free cash flow, leading to a "Hold.

IDEXX Laboratories ( IDXX ) is a global leader in pet diagnostic and software products and services. I always view IDEXX and Zoetis ( ZTS ) as the two best players in the animal health industry. Zoetis is the leader in animal drugs, while IDEXX is the undisputed leader in animal diagnostics. IDEXX is targeting 10%+ organic sales growth, 50-100bps of annual operating margin expansion, and 15-20% EPS growth. I believe it is truly a high-quality, recession-resistant growth company.

Why I Favor IDEXX?

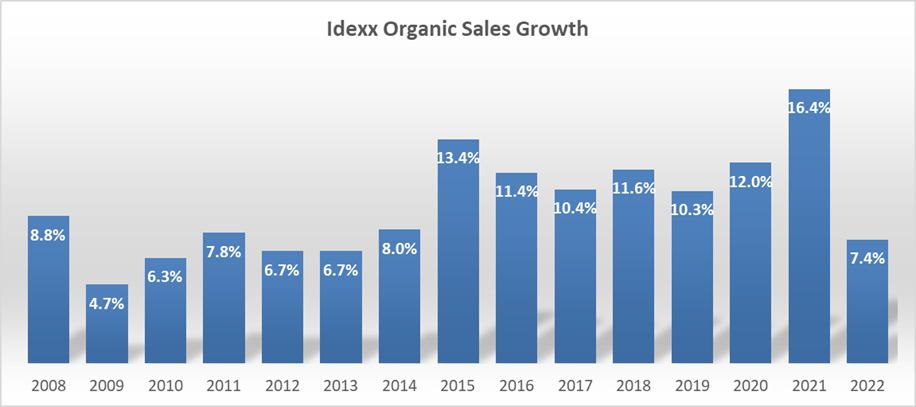

Long-term and Recession-Resistant Growth : IDEXX has never experienced a negative growth year since 2008, and their growth rate has consistently remained in the high-single-digit or double digits. The pet healthcare sector has proven to be resilient during times of economic uncertainty and has outperformed in every recovery cycle.

IDEXX 10Ks, Author's Calculation

{kind=link}

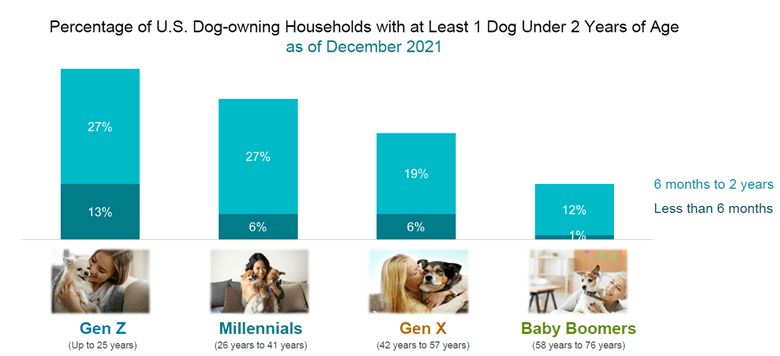

Pet owners are usually willing to make financial trade-offs to care for their pets, regardless of the economic conditions. They are increasingly prioritizing the health and wellness of their animals. This trend is particularly fueled by Gen Z, millennials, and high-income households, who are actively humanizing their pets. I believe the animal health or pet care industry is a very attractive space for long-term investments.

{kind=link}

IDEXX generates 90% of its revenues from the companion animal group, which presents long-term growth opportunities with high operating margins (26%+), and ROIC.

Looking ahead, IDEXX aims to achieve impressive long-term targets, including 10%+ organic sales growth, 50-100bps of annual operating margin expansion, and 15-20% EPS growth. The company's growth rate is truly remarkable to me.

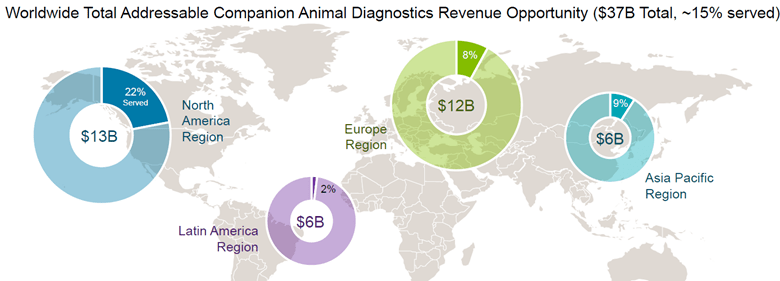

Diagnostics Penetration Growth : There is a significant growth opportunity from pet diagnostics penetration. Even in the most mature market, the US, only 22% of regions have currently been served, according to IDEXX's estimates.

{kind=link}

IDEXX has made strategic investments in diagnostic menus, new and existing platform extensions, and integrated software into their existing diagnostic products. Additionally, the company is focusing on geographic expansion. I believe these investments will enable them to further penetrate global markets.

Software Solutions and Cloud-Based Ecosystem : IDEXX is building its software franchises, covering practice information management, VetConnect Plus, clinical decision support systems, and a pet owner engagement platform. These software solutions enable IDEXX to achieve a higher recurring revenue mix and monetize its existing diagnostic equipment installed base.

IDEXX's software solutions play a crucial role in diagnostics utilization, creating a connected ecosystem that enhances diagnostics workflow, provides deeper clinical insights, and supports pet-owner communication.

In Q1 FY23, IDEXX's organic sales increased by 9.8%. However, their veterinary software and diagnostic imaging revenues experienced even stronger growth, with a 14% organic increase. The company sees ongoing momentum in cloud-based software placements. I believe their investments in software will help improve customer retention and accelerate organic sales growth.

Downside Risks

Instrument Placements : In Q1 FY23, IDEXX experienced a 17% growth in instrument placements. However, it's important to note that instrument placement can be sensitive to the macro environment. IDEXX acknowledges that they are still facing macro pressures on same-store sales growth. Nevertheless, they have factored the potential weakness into their guidance.

Reduced clinical visits headwinds : The current high inflation environment is more likely to result in reduced clinical visit growth. In the US, clinic visits remained flat in Q1 FY23. IDEXX's growth is closely tied to clinical visit growth, as well as volume and price growth. Although they are still experiencing volume and price growth, I would expect reduced clinical visits in the coming quarters.

Near-term Financial Outlook

IDEXX is scheduled to release its Q2 results on August 1, 2023, before the market opens. The company expects its full-year revenue growth outlook to range from 7.5% to 10%, both as reported and organically. The projected operating margin is anticipated to be between 29.0% and 29.5%, including an estimated 60 basis points of year-over-year unfavorable net margin impact from FX. At the high-end, this reflects an outlook for approximately 340 basis points in comparable operating margin expansion.

Given their strong Q1 results, IDEXX is maintaining consistent high-end targets for the full-year guidance. For Q2, they anticipate overall organic revenue growth to be consistent with the midpoint to the higher end of the full-year growth outlook range, with approximately 1% headwind from FX. The operating margin is guided in the range of 29% to 29.5%.

DCF Valuation

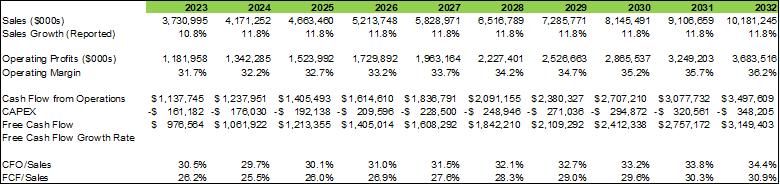

My DCF model assumes 11% of organic sales growth and 0.8% of acquisition growth, and the operating margin gets expanded to 36.2% in FY32. The model is using 4% of terminal growth rate, 10% of WACC, and 19% of tax rate. In the model, the free cash flow conversion is estimated to reach 30.9% in FY32.

IDEXX DCF Model- Author's Calculation

{kind=link}

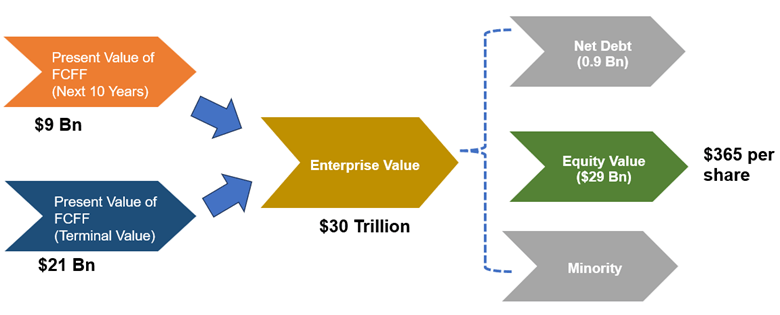

With these assumptions, the present values of FCFF over the next 10 years and terminal are $9 billion and $21 billion in the model. Adjusting the debt and cash, the fair value is $365 per share, as per my estimates. The current stock price is significantly overvalued.

IDEXX DCF Model - Author's Calculation

{kind=link}

In my model, IDEXX is projected to generate less than $1 billion of free cash flow in FY23. As a result, the current stock price is trading at more than 45 times the free cash flow, which is considered very expensive.

End Notes

I admire Zoetis and IDEXX for their phenomenal growth and recession-resistant business models. However, I must note that IDEXX has consistently traded at a hefty valuation. I would reconsider investing in it if there is a stock market downturn in the future. As of now, I would assign a "Hold" rating at their current price.

For further details see:

IDEXX: Best In Class Growth And Recession-Resistant With Hefty Valuation