IDXX - IDEXX Laboratories Could Beat FY23 Guidance But Valuation Is An Issue

2023-05-12 10:05:26 ET

Summary

- IDXX reported positive 1Q23 results, with consistent organic growth in the US and an accelerated growth rate in international CAG Dx.

- IDXX has experienced positive trends in both wellness and non-wellness testing, indicating strong demand from pet owners in the US.

- The valuation of IDXX is my key concern. While the quality of the business justifies a premium, the extent of the premium remains a subject of debate.

Thesis

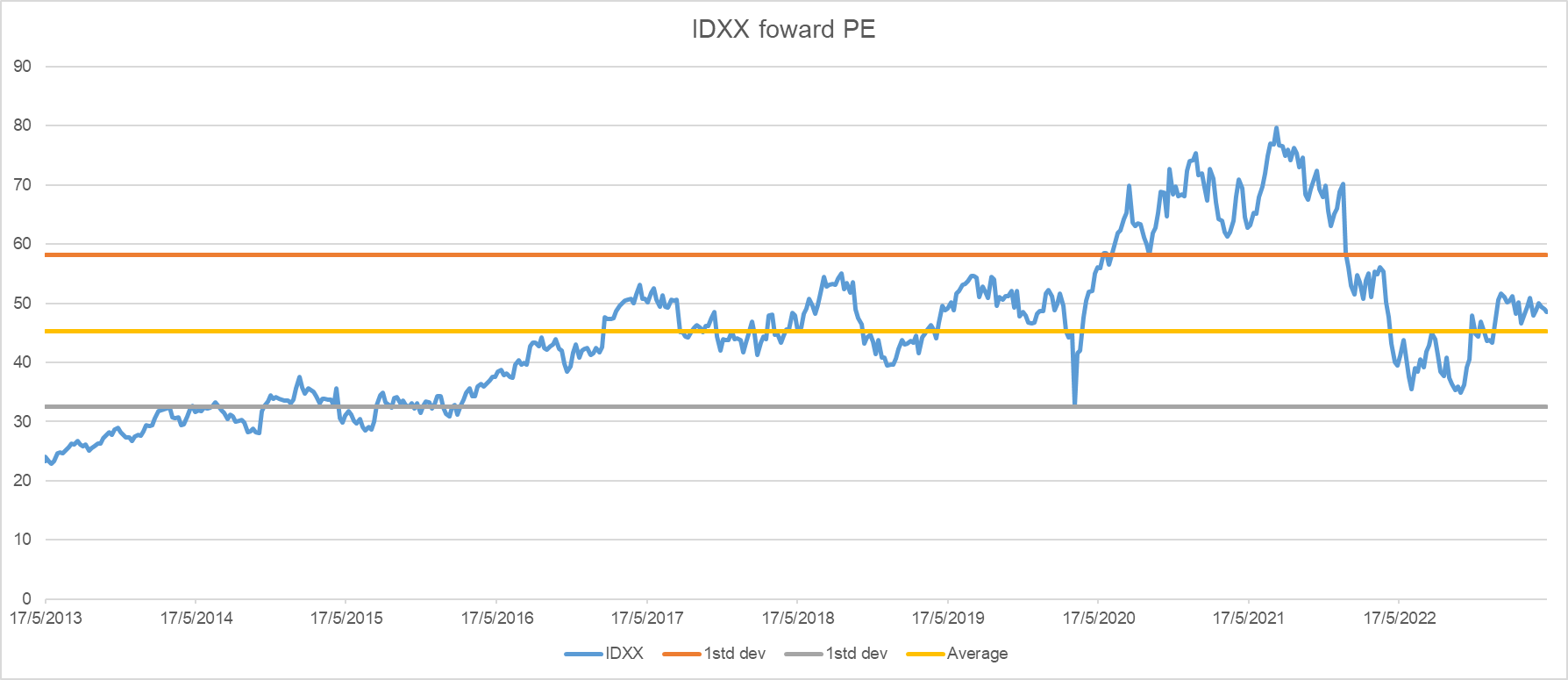

IDEXX Laboratories (IDXX) provides diagnostic, detection, and information systems for veterinary, food, and water testing applications through its international network of veterinary reference laboratories. The 1Q23 results were positive, and management raised the lower end of their full-year guidance, which was slightly disappointing because I had anticipated that they would raise the higher end of the guidance on the strength of the 1Q. Management did note that FY23 guidance would be impacted negatively by higher lab staffing costs, certain capitalized costs, and unfavorable FX. However, with steady Dx utilization in both the US and internationally, I believe IDXX has what it takes to beat this guidance. What exit multiple should this stock trade at is my main concern. The IDXX price-earnings multiple is extremely high at nearly 60x LTM earnings, or 48x forward earnings. I agree that IDXX runs a solid business and exhibits some monopolistic features, but this price tag seems excessive for a company that can only sustain double-digit earnings growth in the long run. Considering its average valuation over time, I believe the best course of action is to buy it at a discount. As a result, my current recommendation is to hold.

1Q23 Results review

Consistent organic growth in US CAG Dx of 13.6% surpassed IDXX's 11.5% target embedded in the high end of guidance; this was due to moderate growth in clinical visits, net price realization of 8 to 9%, and stable growth in Dx utilization (5%). Overall, prices were in line with 1H guidance for 8-9%, and management remains confident that Dx utilization growth will be stable in the mid-single digits, with little effect on volumes from price increases. The growth rate of international CAG Dx accelerated to 7.8% in 1Q23 from 5.9% in 4Q22. The macro environment and lower same-store clinical visits constrained growth, limiting both international veterinary visits and reference lab growth.

Demand

Even though the weak macro environment has sucked the lifeblood out of many victims (businesses) across many industries in the US, it was great to see healthy pet owners' demand. IDXX was successful where other businesses that could not pass on rising costs ultimately went out of business. IDXX has reported positive trends for both wellness and non-wellness testing, indicating continued high demand from American pet owners. While IDXX is experiencing some macroeconomic impact in Europe, management notes that regional trends appear manageable. The fact that management only increased the lower end of FY23 guidance is somewhat discouraging, but I interpret this as a sign of management's desire to play it safe. As the year progresses and management gains more certainty, I expect it to move the timing of its guidance up. Overall visits are something I am keeping an eye on. Although clinical visits were slightly up, overall visitation was down by less than one percent during the quarter. Management emphasized how this exceeded their expectations and cited encouraging developments in areas such as capacity expansion, software enhancements, and efficiency gains. Looking at the bigger picture, it appears that percentage-wise, growth in FY23 would be easier as well, after the rough patch in FY22. A good absolute growth should be supported by this, a gradual easing of vet pressures, and healthy price increases. Together, they would amount to substantial percentage growth thanks to both strong absolute growth and an easy comparison base. In addition, I believe that IDXX is well positioned to generate sustainable double-digit top-line growth over the long term, thanks to the sector's favorable longer-term macro tailwinds in animal health.

Valuation

The constant debate I have with myself before considering investing in IDXX is the valuation and what exit multiple should be assigned to this stock. While some investors may argue that a significant premium is justified given the business's quality, I agree. The question is, how much premium should be paid? If we look at some of the other peers in similar industries like Bio-Rad ( BIO ) and Danaher ( DHR ), IDXX is trading at a significant premium (is this premium too high to invest today?)

{kind=link}

Valuation is important, and I believe the best approach is a DCF model combined with a market exit multiple. The end result was a risk/reward ratio that was unappealing at the current multiple. My assumption is that earnings can continue to grow at 12% per year, combined with 2% share buybacks, resulting in 14% EPS growth over the next decade. The exit multiple assumption, which I modeled (1.5x, 2x, 2.5x the S&P average multiple), comes next. Given the business quality and other factors, my best guess is that this will trade in the mid-30s range, implying that the stock is currently fairly valued. When we compare the downside and upside scenarios, the risk-reward ratio is 1:1, which is not appealing in my opinion.

Own calculation

Conclusion

IDXX reported positive 1Q23 results, with consistent organic growth in the US and an acceleration of growth in international markets. Demand for veterinary testing remains strong, despite the challenging macroeconomic environment. While management raised the lower end of their full-year guidance, the decision to not raise the higher end of the guidance may be a cautious approach. As the year progresses and uncertainties ease, I see potential for upward revisions to the guidance. One key concern is the valuation of IDXX. The stock currently trades at a high price-earnings multiple, which some argue is justified given the quality of the business. However, the question of how much premium should be paid remains. Comparisons to other companies in similar growth and competitive positions suggest that IDXX may be trading at a significant premium. Valuation analysis using a discounted cash flow model and market exit multiples indicate that the stock is currently fairly valued.

For further details see:

IDEXX Laboratories Could Beat FY23 Guidance, But Valuation Is An Issue