IDXX - IDEXX Laboratories Q4 Earnings: Strong Margin Expansion But Too Expensive

Summary

- IDEXX Laboratories' share price has increased over 55% since last October.

- The pet healthcare company has a huge TAM and is benefiting from strong tailwinds.

- Its Q4 earnings were strong as margins improved once again while guidance also indicates accelerating growth.

- However, the valuation is high and offers little potential upside.

- I rate the company as a hold.

Investment Thesis

IDEXX Laboratories ( IDXX ) may not be a household name, but the company has been one of the best-performing compounders in the past decade, with shares up over 1,100% during the period, significantly outpacing the broad indexes. The company has strong fundamentals and continues to benefit from the massive addressable market and secular tailwinds. It also sees growth opportunities in software and has strong operating leverage. IDEXX Laboratories reported earnings on Monday and the results are impressive as margins continue to increase, while guidance also exceeded expectations. However, after the 50%+ run-up in share price since June, the current valuation is very stretched and offers little potential upside. Therefore I rate the company as a hold.

Why IDEXX Laboratories?

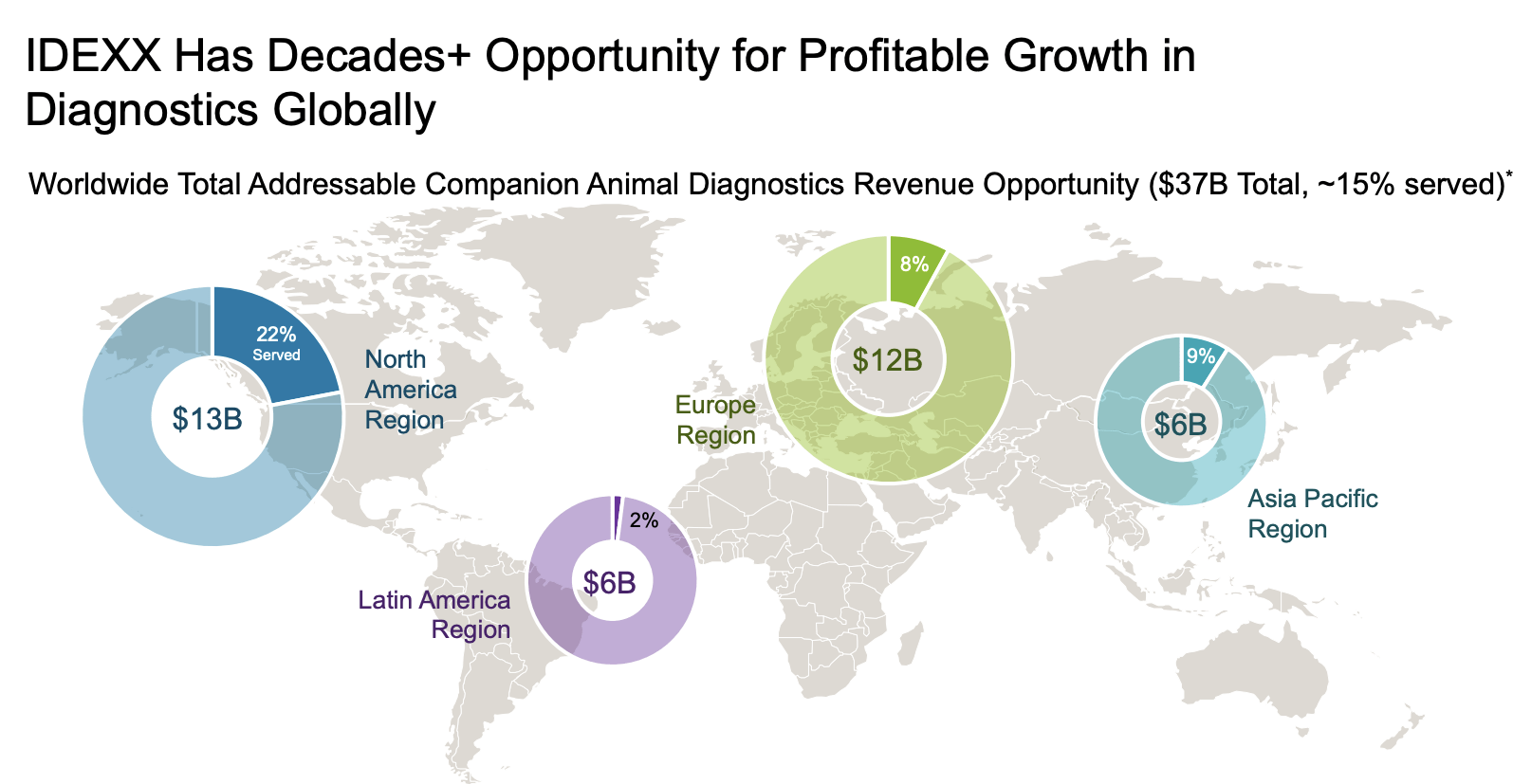

IDEXX Laboratories is a US-based pet healthcare company. It mainly provides diagnostics devices and operational software to veterinary hospitals and clinics across the globe. It also offers testing solutions for the water and livestock industry, but only represents a small portion of its business. The TAM (total addressable market) for companion animal diagnostics is huge. According to the company , the global TAM is estimated to be $37 billion, with the US accounting for $13 billion. While according to Grand View Research , the market is expected to grow at a CAGR (compounded annual growth rate) of 11.2% from 2020 to 2030. IDEXX’s current revenue run rate translates to a penetration rate of only 15%, which suggests ample room for further expansion.

The number of companion animals has been growing faster in the past few years as more and more people prefer pets over kids, especially for younger generations. The pandemic also caused a bump in numbers as people got isolated during lockdowns. From 2010 to 2019, the annual increase in the US pet population was roughly 1%. The figure has grown substantially to 5% in 2020 and 2021. This creates a long-term tailwind because as the pet gets older, more money will need to be spent on diagnostic and other services. For instance, the diagnostic revenue generated by an 11+-year-old pet is 310% higher than a < 1-year-old pet. This should be a notable growth driver moving forward. I believe the market will continue to expand rapidly which should benefit IDEXX Laboratories.

{kind=link}

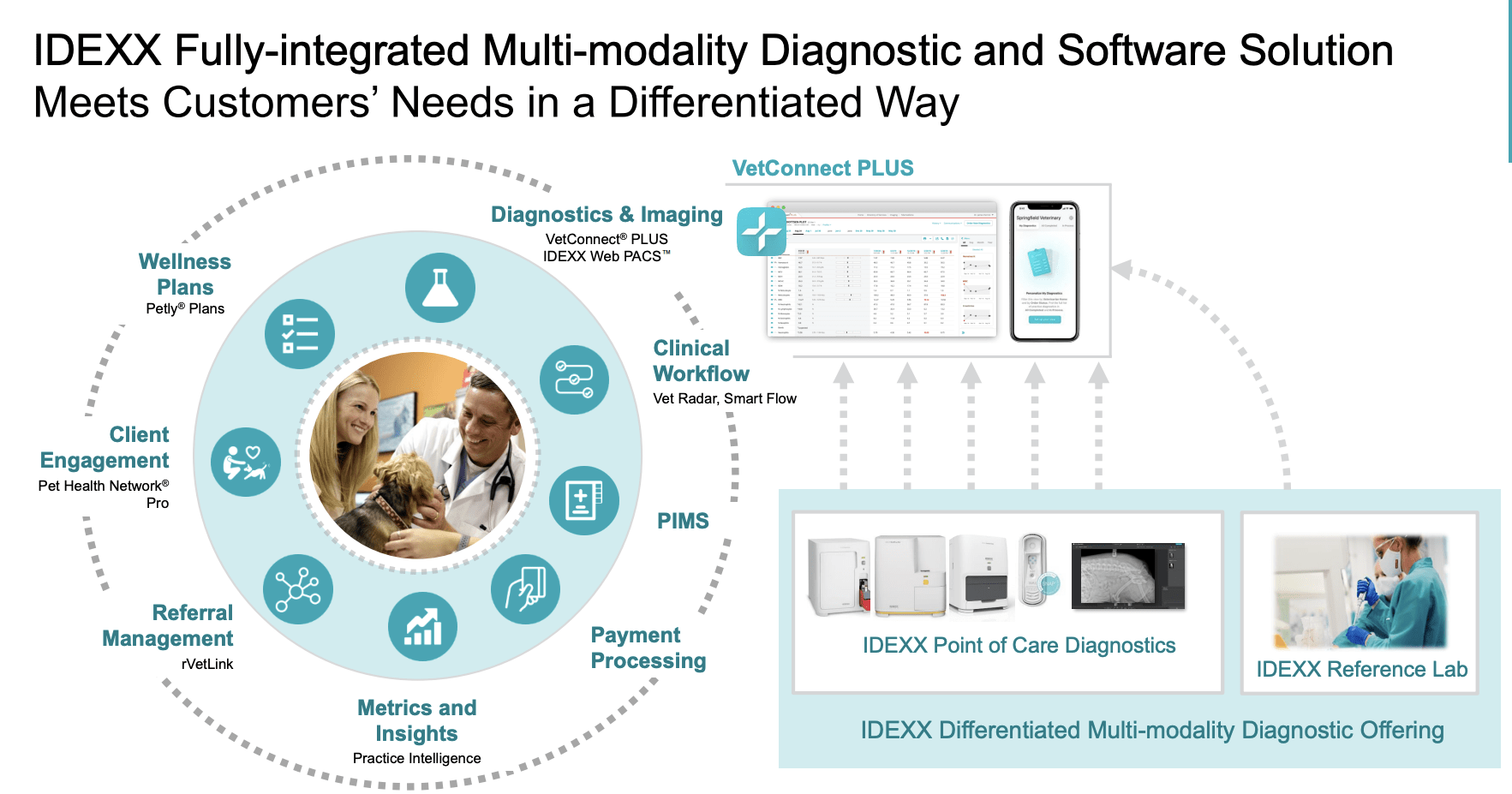

Veterinary software is another emerging growth opportunity. The space is currently highly fragmented and filled with legacy technologies. IDEXX Laboratories saw this opportunity and started to offer an integrated solution that allows clinics and hospitals to improve their workflows. The software can also connect to IDEXX Laboratories’ existing diagnostic and lab instruments for optimal efficiency. It is seeing strong traction as the company is able to leverage its large customer base to distribute the product. Software should be a notable growth driver moving forward in my opinion.

Jay Mazelsky, CEO, on software products :

This business includes an end-to-end stack of software products that create a seamless connected ecosystem across the whole tech clinic, which in turn enables deeper diagnostic insights, supports pet owner communications creates workflow efficiencies and help support greater diagnostics usage and revenue growth.

{kind=link}

Financials and Valuation

A large part of IDEXX’s thesis is its ever-improving profitability and the latest result demonstrated that once again. The company announced its fourth-quarter earnings earlier this week and posted yet another double beat. It reported total revenue of $828.6 million, up 3.4% YoY (year over year) from $801.1 million. On a constant currency basis, revenue was up 7.3%. CAG (companion animal group) revenue was up 4.1% YoY from $719.1 million to $748.5 million, representing 90.3% of total revenue. Most of the growth was driven by the increase in revenue from software and rapid assay products, which increased by 15.3% and 7.1% respectively. The water segment was up 5.9% YoY from $37.1 to $39.3 million, while LPD (livestock, poultry, and dairy) revenue was down 1.7% YoY from $34 million to $33.4 million.

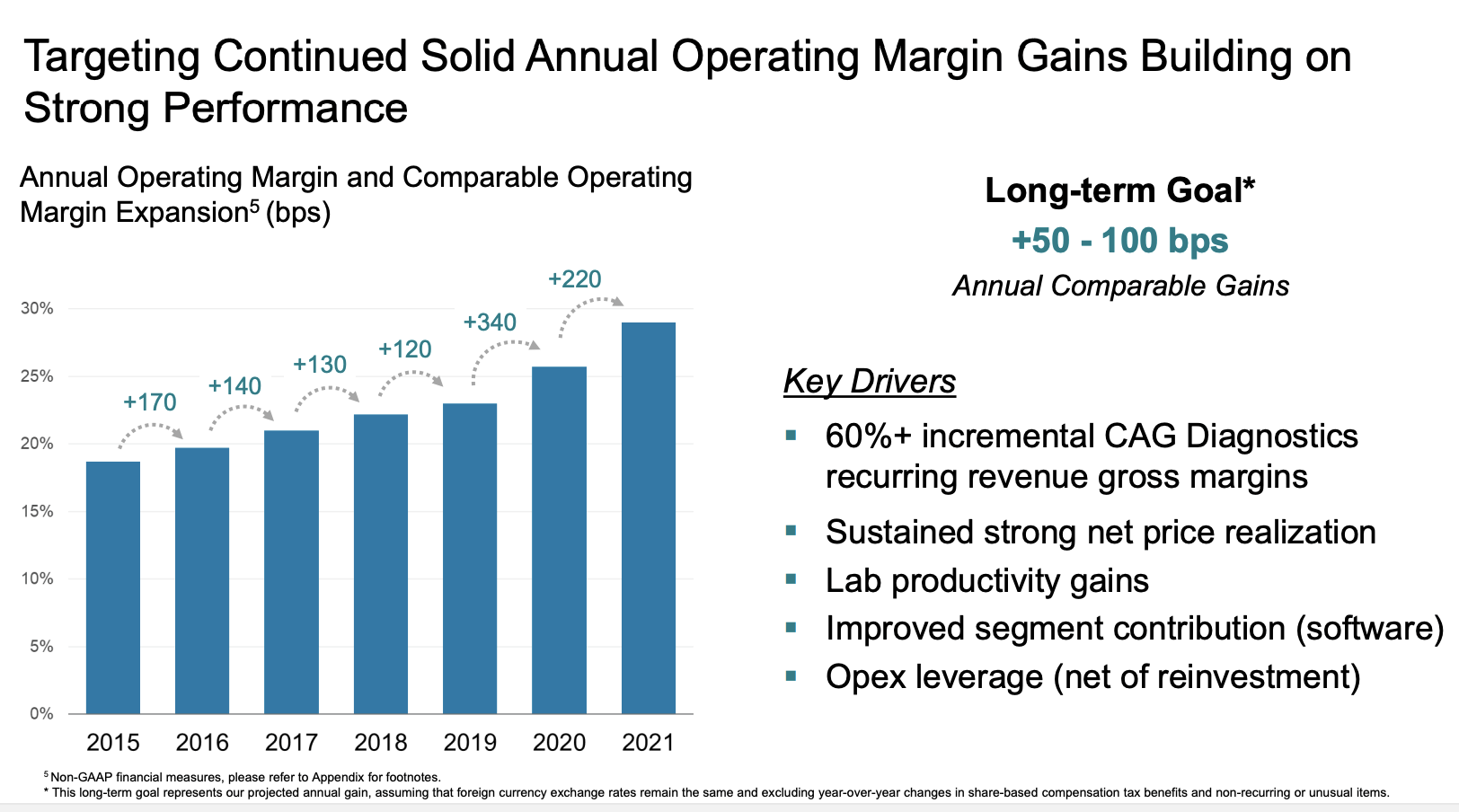

Margin expansion is a strong growth driver for IDEXX's bottom line. The company has grown its operating margins every year since 2015 and it is targeting a long-term annual increase of 50–100 basis points. Gross profit for the quarter was $484.9 million, up 6% YoY compared to $456.4 million. The gross profit margin increased by 150 basis points from 57% to 58.5%, led by an improved product mix. Operating income increased 14% YoY from $199.2 million to $233 million, as the operating margin grew 240 basis points from 24.9% to 27.1%. This is contributed by conservative S&M (sales and marketing) spending and lower R&D expenses. EPS for the quarter was $2.05, or an increase of 8%. The company also provided encouraging guidance. Revenue for 2023 is forecasted to be $3.59 billion to $3.69 billion, or an increase of 7%-10% on a constant currency basis. While the EPS is expected to grow even faster at 19%-26%, benefiting from strong operating leverage.

{kind=link}

Investors Takeaway

I like IDEXX Laboratories a lot but the price is a big issue. The company operates in the attractive pet healthcare industry which is highly resilient and has a massive TAM. The number of pets will only continue to increase over time, increasing the demand for IDEXX’s products. There aren't many players in the space due to high entry barriers therefore the company has very strong pricing power. It also sees emerging growth opportunities in segments such as software. These catalysts combined with margin expansion should provide durable bottom-line growth for the company. However, the current valuation is very elevated. The company rallied over 50% since October and is now trading at a PE ratio of 63.2x. This is near the high end of its historical average and meaningfully above peers such as Zoetis ( ZTS ) and Thermo Fisher ( TMO ), which are trading near mid-thirties times PE. Even with strong fundamentals, I do not see much potential upside from the current price. Therefore I rate the company as a hold.

For further details see:

IDEXX Laboratories Q4 Earnings: Strong Margin Expansion But Too Expensive