DHR - IDEXX Laboratories: Valuation Rerating Doesn't Seem Justified

2024-01-16 11:00:00 ET

Summary

- IDEXX Laboratories has outperformed the broader market and continues to show strong growth in its diagnostic products and services for pets.

- The company is shifting towards recurring revenue streams, which improves sales visibility and customer retention.

- IDEXX sees a significant growth opportunity in the global pet diagnostics market, with a 25-year estimated 9% compound annual growth rate. However, the assumptions behind this estimate are aggressive.

- IDEXX stock is likely overvalued, unless they can show the long-term (15-20 years) growth runway they expect.

IDEXX Laboratories (IDXX) has continued outperforming the broader market since my initial coverage in October 2022 , doubling the S&P 500 total return of 25%. I deemed the company too expensive back then. Let's see if it has outperformed expectations since then to justify the price increase and if it could present a compelling investment in the future.

Investment thesis recap

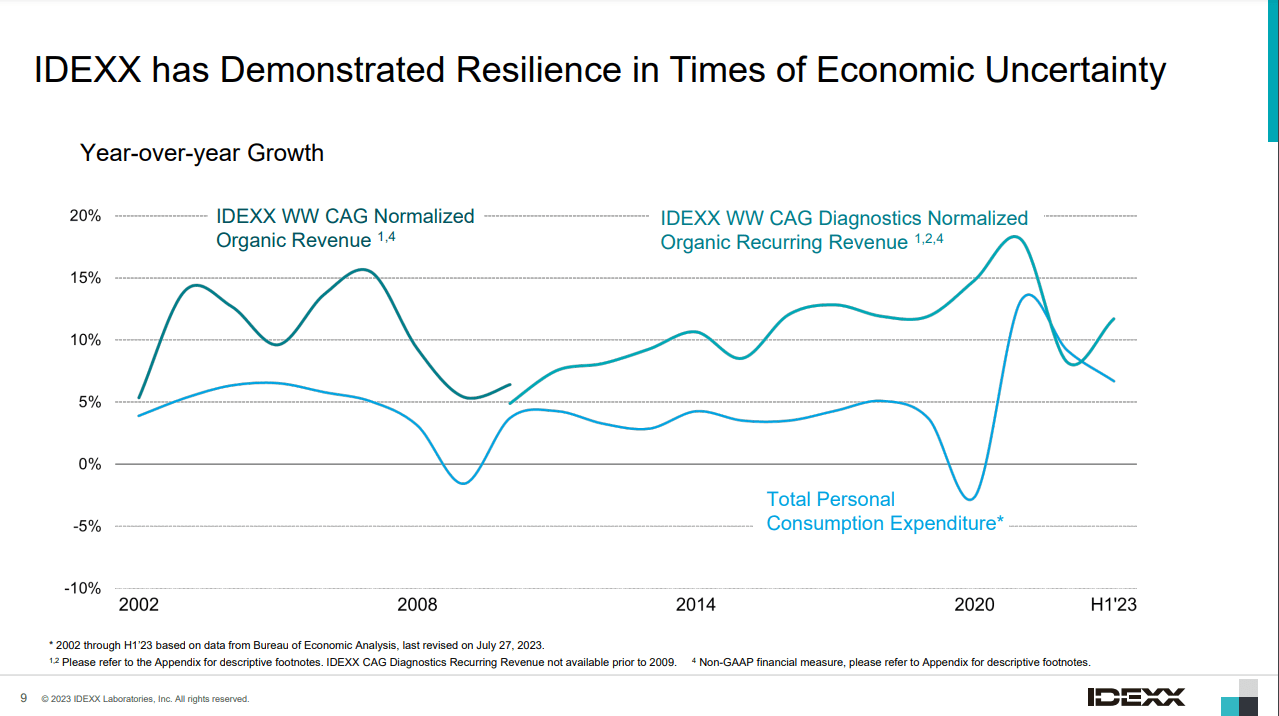

IDEXX is a leading provider of diagnostic products and services predominantly (over 90% of sales) in the Companion Animal segment (pets). The industry is very resilient because of the close bond between pets and owners and the willingness of owners to sacrifice other spending to care for their pets.

Pet Healthcare resilience (IDEXX Investor Day)

{kind=link}

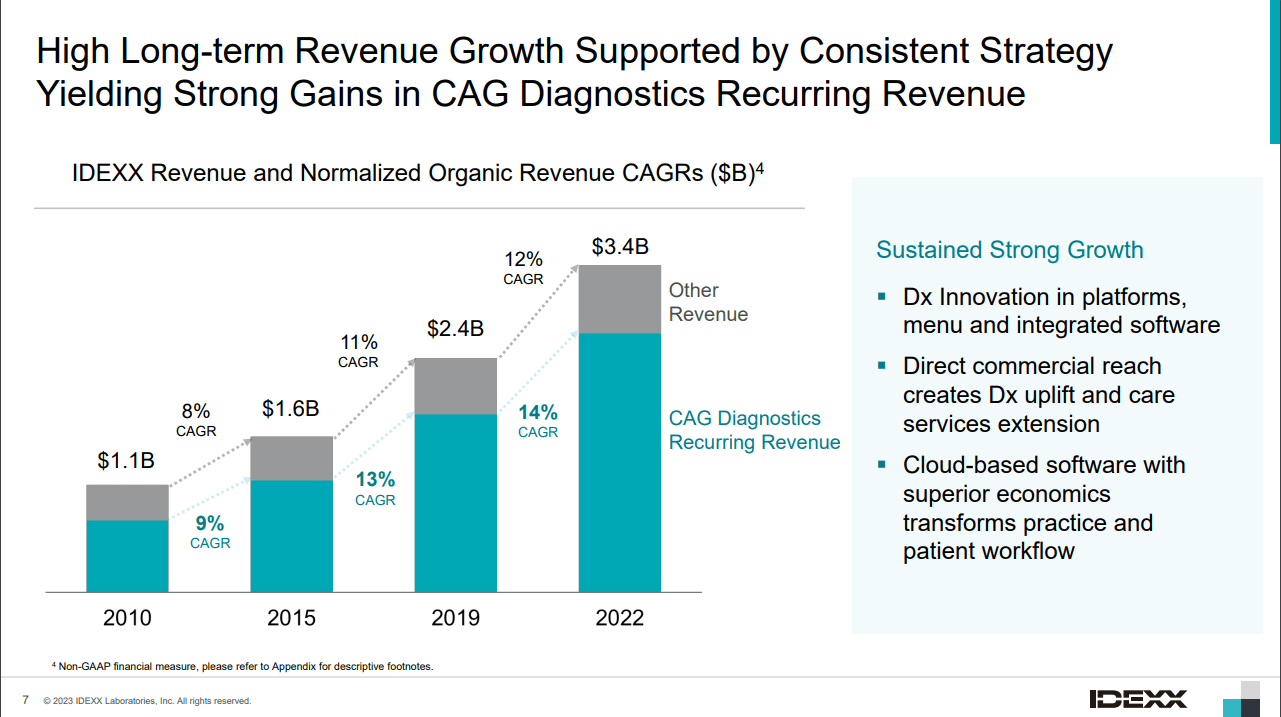

IDEXX shifts more and more of its sales to recurring revenue streams, outgrowing its other revenue portion. Recurring revenue is particularly attractive for companies, as it improves sales visibility and lowers the potential for large volatility in results. Services, consumables and software subscriptions are all ways IDEXX leverages to grow recurring sales. This reminds me a lot of how Danaher (DHR) grows its recurring revenue in the life sciences industry.

Driving recurring revenue (IDEXX Investor Day)

{kind=link}

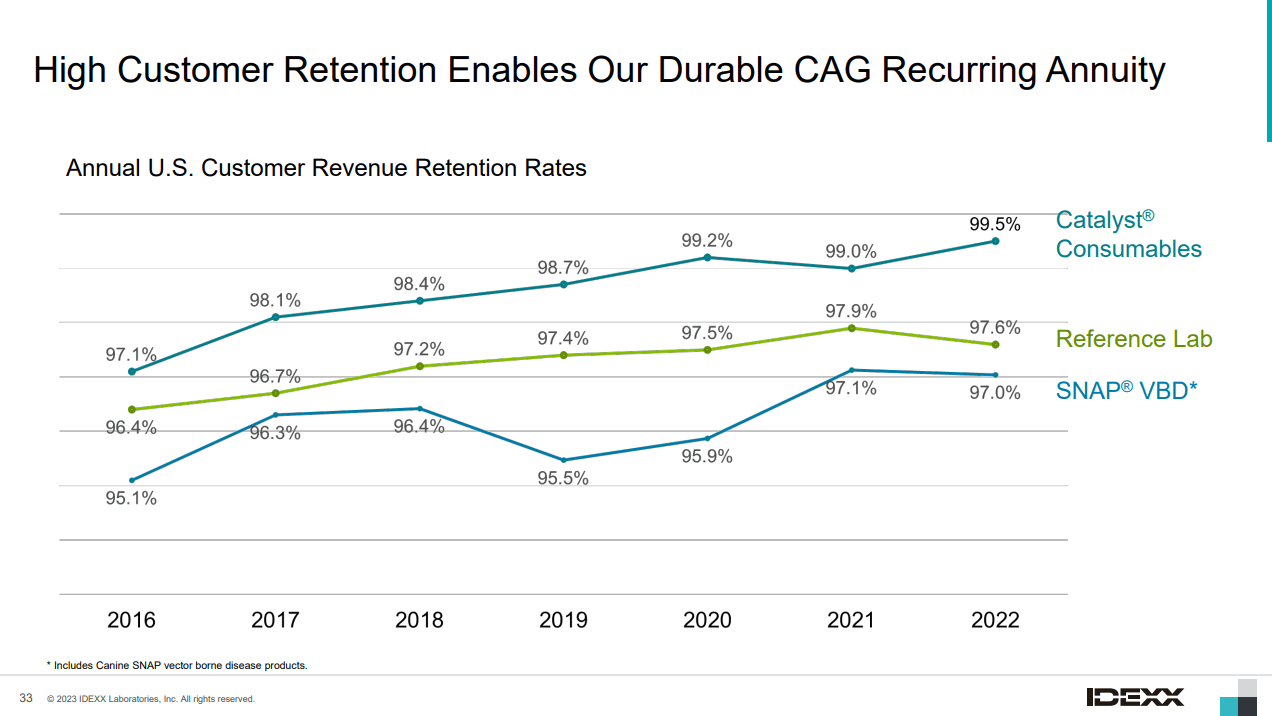

We can see that IDEXX enjoys a very high and growing customer retention. Retaining most of your customers as a recurring revenue business gives you a massive cost advantage in Sales and Marketing. It showcases the high-value customers derive from the offering.

{kind=link}

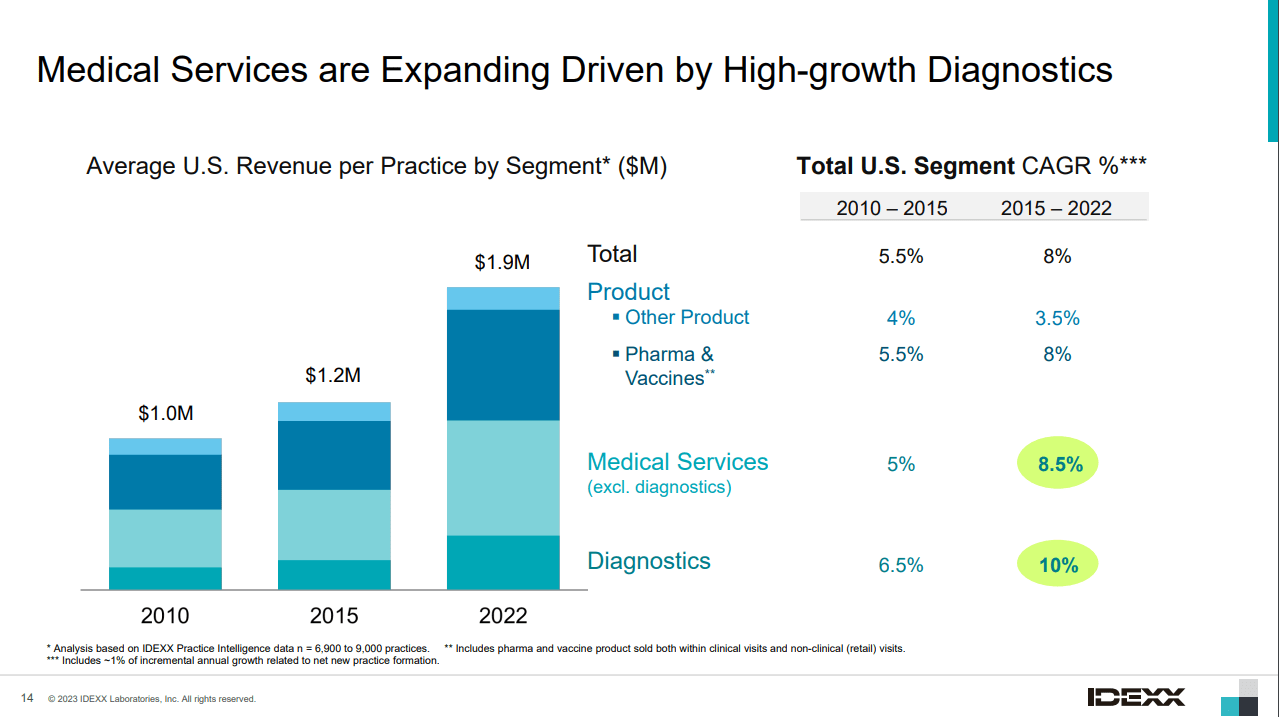

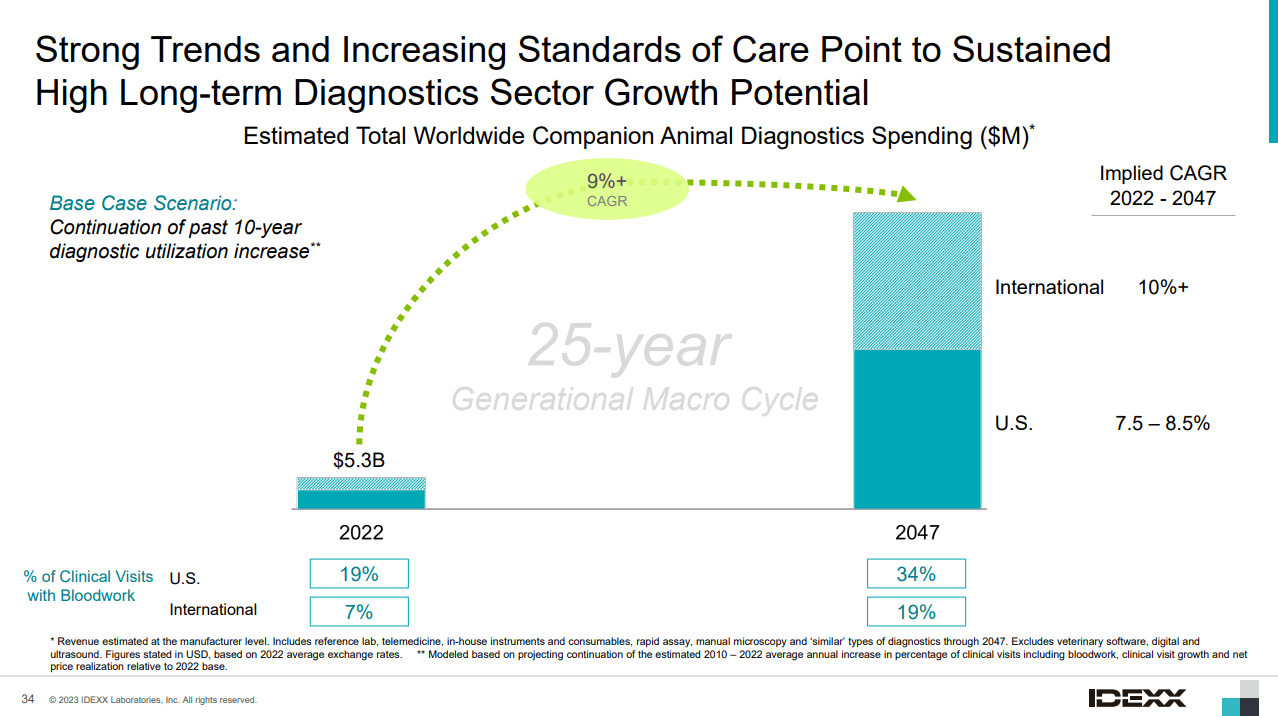

Based on the average US revenue per pet practice, total spending has increased rapidly over the last 12 years, with medical services and diagnostics growing the fastest. IDEXX expects this trend to continue for a very long time. The company estimates a large white space in the $45 billion global opportunity in pet diagnostics. The US is the leading market, with just 22% served in a potential $17 billion market, while Europe is the second largest region at a possible $14 billion and 9% served.

{kind=link}

Growth opportunity

IDEXX has set out a very optimistic and far-out industry estimate, calling for a 25-year 9% CAGR, led by international with 10%+ and US with 7.5-8.5% growth in Companion Animal Diagnostics spending. This comes back to the estimate that most of the potential market is still underserved. In my opinion, the assumption lies in the global adoption of the American way of life, where international pet owners will start to spend more and more on their pets and grow into the same utilization as US customers. I find these assumptions very aggressive; 25 years is a very long time to forecast a trend. The pet population in the US has historically grown by 1% until the pandemic, accelerated in 2020 and 2021, and decelerated back to 2% in 2022. In my opinion, the pandemic was a one-time boost, and we now return to historic growth patterns. Younger people so far are more willing to use diagnostic services for their pets, which could help facilitate this long macro trend.

Several positive factors drive spending: Pet Population, average life span, and younger people's willingness to spend more on pets.

{kind=link}

IDEXX is tough to value

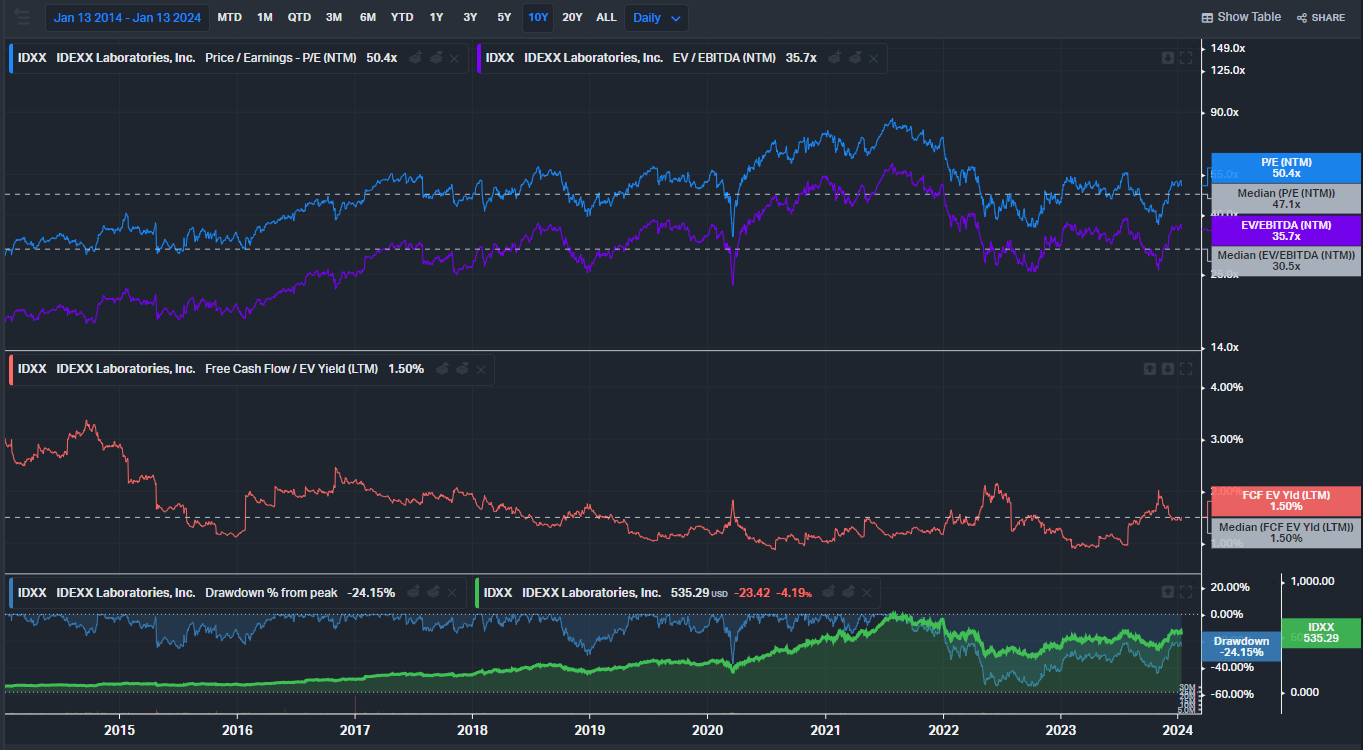

To value IDEXX, I'm looking at historical multiples and using an inverse DCF model. Since the last article, IDEXX saw significant multiple expansion, rising from 38.8 PE to 50.4 and from 27 EBITDA to 35 times. The company now trades above its median valuation for the last decade again. Earnings surprised every quarter since then with modest beats around 5% on EPS and revenue in line. IDEXX performed well but did not fundamentally outperform to justify such a treatment. On a multiple bases the company looks overvalued.

{kind=link}

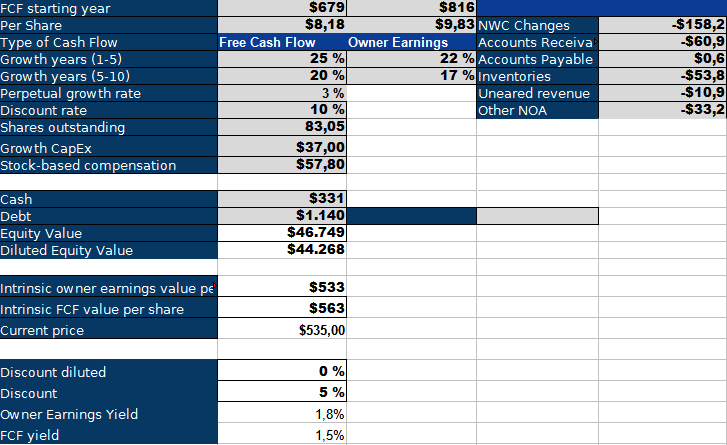

I changed my inverse DCF model quite a bit since last time.

- I now use FCF and Owner Earnings (FCF + Growth CapEx - SBC +/- Change in NWC), emphasizing the latter.

- I do not use share count change anymore because it double counts FCF (FCF was first used in the cash flow and then used again to reduce the shares outstanding at the end of the period)

{kind=link}

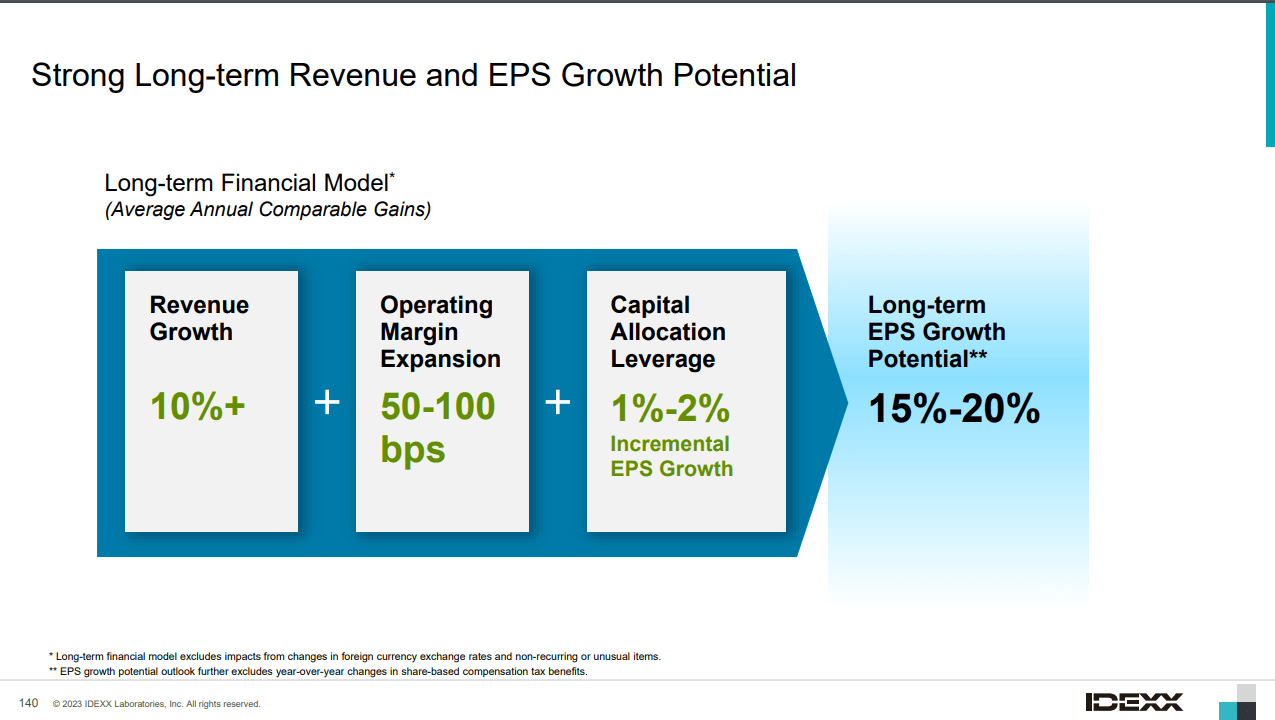

The model suggests that IDEXX is priced to grow Owner Earnings by 22% in the next five years, followed by five years of 17% growth. This is above the long-term EPS growth potential the company stated on its Investor Day. I believe achieving the required growth rates will be tough, especially as operating margins expanded nicely from 20% in 2014 to 30% this year. An incremental 50-100 bps annual expansion will leverage EPS less than in the past. Buybacks are also becoming less effective as the company trades at rich multiples, and the annual FCF could only reduce outstanding shares by 1.5%. Using the inverse DCF model, IDEXX also looks overvalued.

{kind=link}

While both methods indicate an overvalued stock, we must consider the ambitious management estimate of a 25-year macro growth cycle for the companion animal diagnostic market at a 9% CAGR. While I believe the company will undoubtedly see multiple compression and won't trade at 50 times earnings in 25 years, a compounded growth rate of 9% over 25 years would certainly undervalue IDEXX today. The danger of DCF models is that they typically only account for ten years of growth and then return to a GDP growth rate. If a company can show an extended growth outperformance after the ten-year growth period, then the stock is most likely undervalued. I prefer to be conservative in my estimates, and I do not feel confident going out more than ten years in my model, but I see the potential and, for that reason, will keep the hold rating on the business.

For further details see:

IDEXX Laboratories: Valuation Rerating Doesn't Seem Justified