IDXX - IDEXX: One Of The Best Compounders On The Market

2023-06-29 18:01:38 ET

Summary

- IDEXX Laboratories, a healthcare supplier specializing in veterinary health diagnostics and research, is a potential high-performing compounder due to its wide-moat business model, anti-cyclical customers, strong pricing power, and high free cash flow conversion.

- Despite not offering dividends, IDEXX has returned nearly 1,000% over the past decade, and its focus on fast-growing veterinary healthcare and aim to increase its installed base of premium instruments could contribute to further revenue expansion.

- While the valuation isn't highly attractive, I'm a buyer if we encounter potential stock price weakness.

Introduction

In this article, I initiate coverage of IDEXX Laboratories ( IDXX ) , a healthcare supplier with the potential to remain one of the best compounders on the market.

After covering a number of healthcare companies in the past few weeks, I wanted to shed some light on this Westbrook, Maine-based giant that operates in the diagnostics and research industry - specifically in veterinarian health.

While the company doesn't come with a dividend nor a valuation that looks attractive at first sight, it has everything that makes a compounding stock successful. This includes a wide-moat business model, anti-cyclical customers, strong pricing power, innovation, a healthy balance sheet, consistent growth, and high free cash flow conversion.

In this article, I'll walk you through my thoughts as I explain why IDXX is on my watchlist, despite my focus on dividend-paying stocks.

So, let's get to it!

Compounding With IDEXX

Let me start this article by quoting C WorldWide Asset Management , which researched the power of compounders. Compounders are companies that can deliver sustainable long-term growth. Stock prices of compounders display exponential growth and outperforming returns.

While they are not great for income-focused investors, I believe that owning at least a few compounders offers tremendous value for every type of investor.

This is what the asset manager concluded in its paper (emphasis added):

It is said that Albert Einstein described compounding interest as the most powerful force in the universe. We firmly believe that the long-term trend in company earnings with high cash conversion determines the generation of returns , and that finding compounders is the holy grail of investing. The mindset of being on a constant search for compounders is a better use of time than exhausting one’s intellectual capital and time on trading in and out of stocks and segments of the market in a desire to look good in the short term.

In other words, C WorldWide is telling us to identify companies with consistent earnings growth and high cash conversion instead of wasting our time trading stocks.

I wholeheartedly agree with this.

Usually, I focus on dividend growth stocks. Dividend growth compounders, so to speak. In this article, we discuss a company that returns cash through buybacks, which is great for the long-term total return, but not great for investors that are looking for high income.

With that said, IDXX has been a fantastic compounder.

- Over the past ten years, the stock has returned close to 1,000%. This translates to almost 25% per year with a standard deviation of 29%.

- Over the past five years, IDXX shares have returned 17.4% per year with a standard deviation of 36%, amplified by the pandemic.

So, what is IDEXX?

Fast-Growing Veterinarian Healthcare Exposure & Operational Excellence

IDEXX was founded in 1983. The name is based on IDX, the abbreviation for immunodiagnostics.

The company specializes in the development, manufacturing, and distribution of products and services for a number of industries, including companion animal veterinary, livestock, and poultry diagnostics.

{kind=link}

IDEXX Laboratories

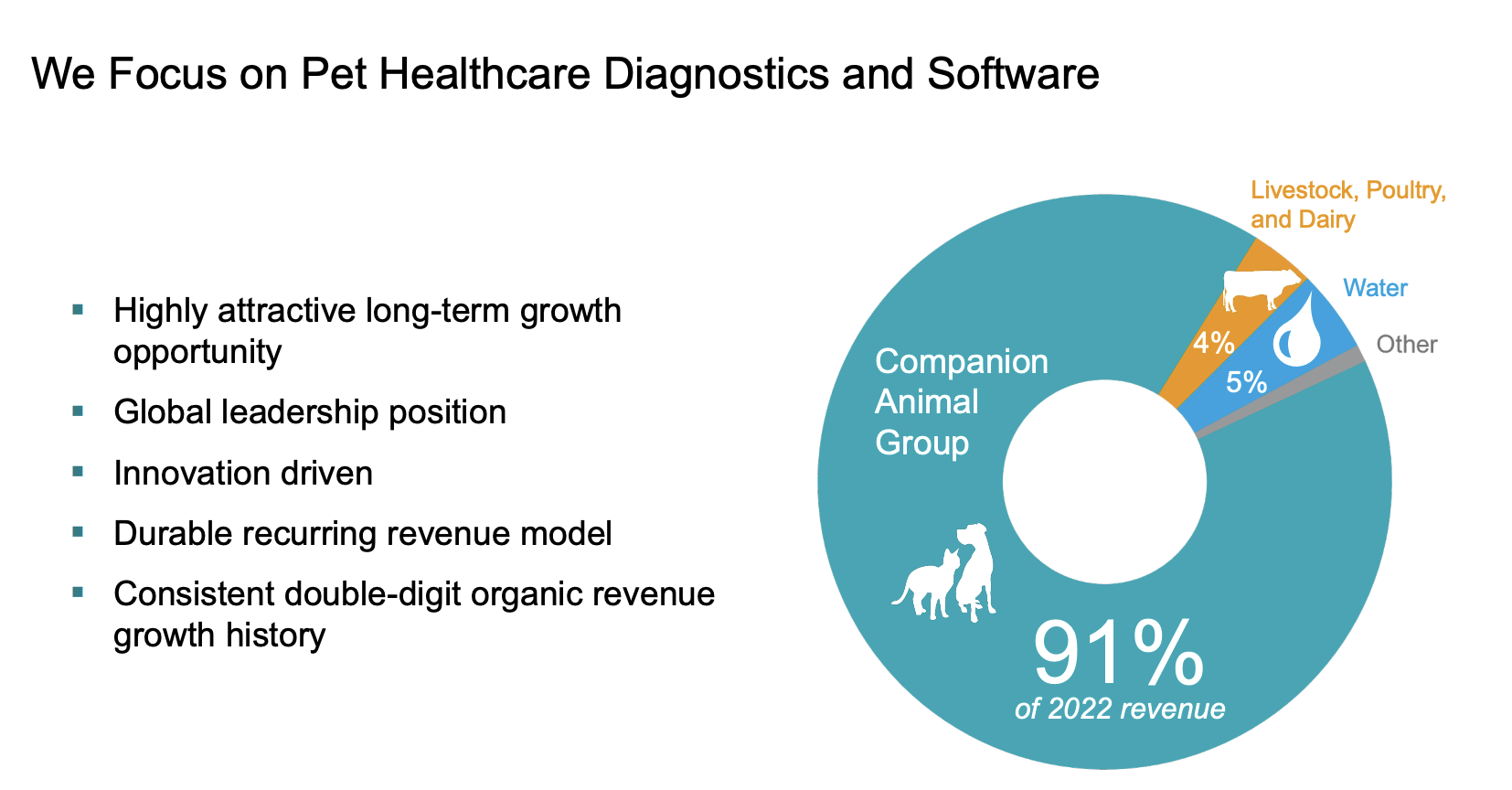

IDEXX operates through three main business segments: Companion Animal Group ("CAG"), Water quality products, and Livestock, Poultry, and Dairy.

They also have an "Other" operating segment that combines their human medical diagnostic products and services business with out-licensing arrangements.

In its CAG segment, the company provides diagnostic and information management-based products and services to the companion animal veterinary industry. They offer in-clinic diagnostic solutions, outside reference laboratory services, and veterinary software and services.

The company benefits from a number of growth drivers. Not only is healthcare equipment a great business to be in, but the company is doing business in an industry with significant secular growth. According to the company , 95% of companion animals are considered part of the family. In developed nations like the US, UK, and Germany, between 76% and 87% of pet parents go to at least one screening per year.

Meanwhile, pet spending remains at just 1.6% of household income in the US. Diagnostics accounts for 0.1%.

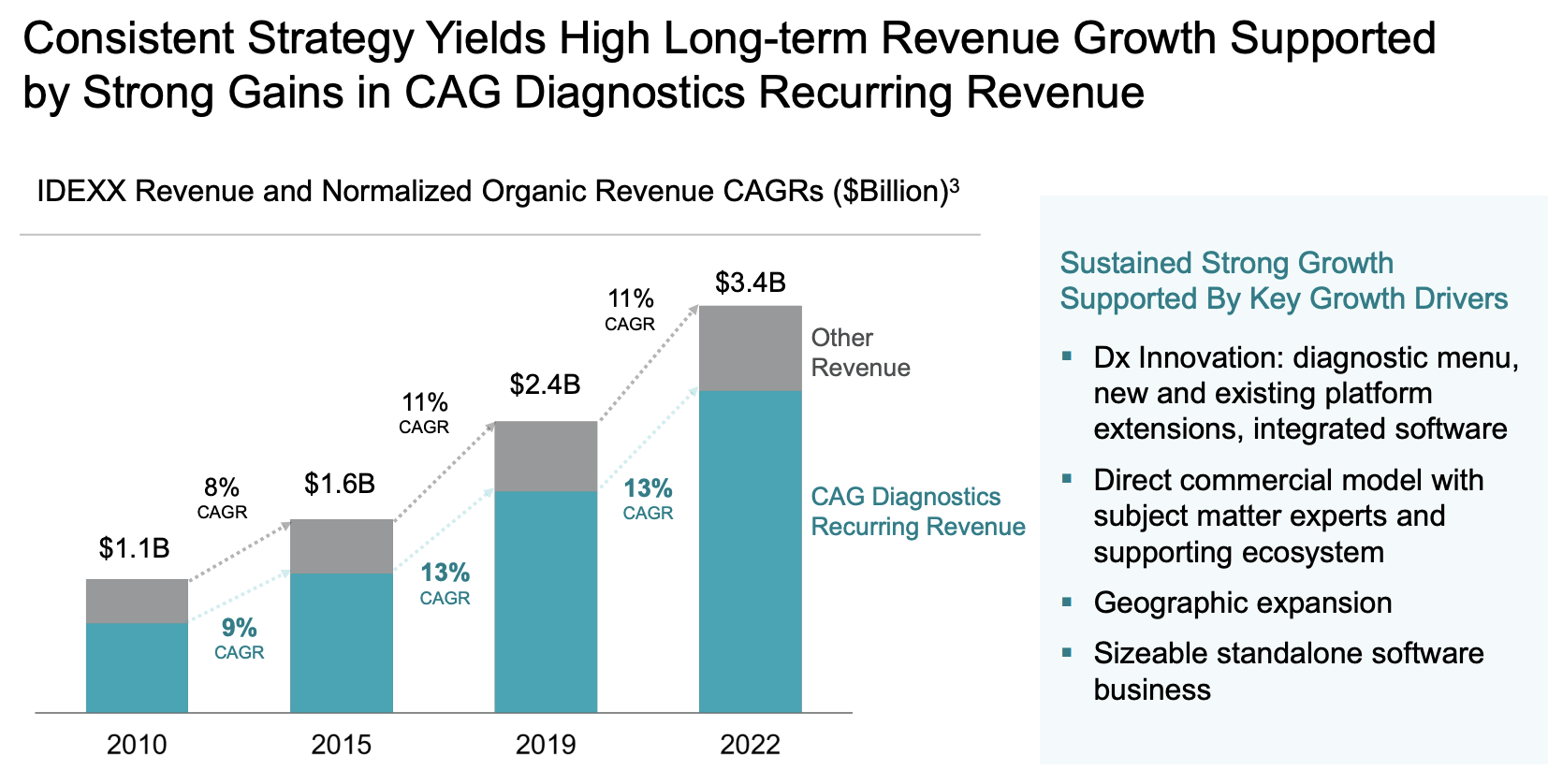

Thanks to these developments, IDEXX has strong long-term revenue growth. In 2010, the company generated $1.1 billion in revenue. Last year, that number was $3.4 billion.

{kind=link}

IDEXX Laboratories

Even better, the compounding annual growth rate has not weakened.

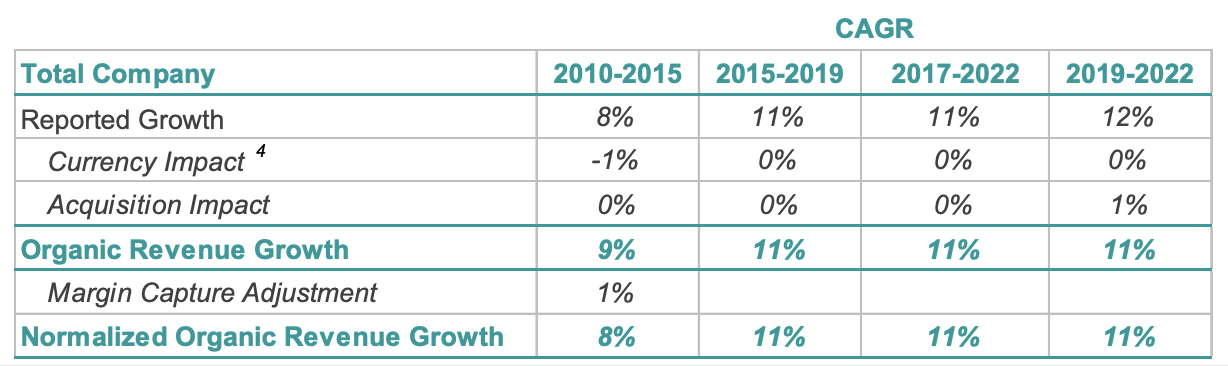

But wait, that's still not everything. IDXX's growth has been organic. The overview below shows that compounding growth was entirely driven by organic growth, not M&A.

{kind=link}

IDEXX Laboratories

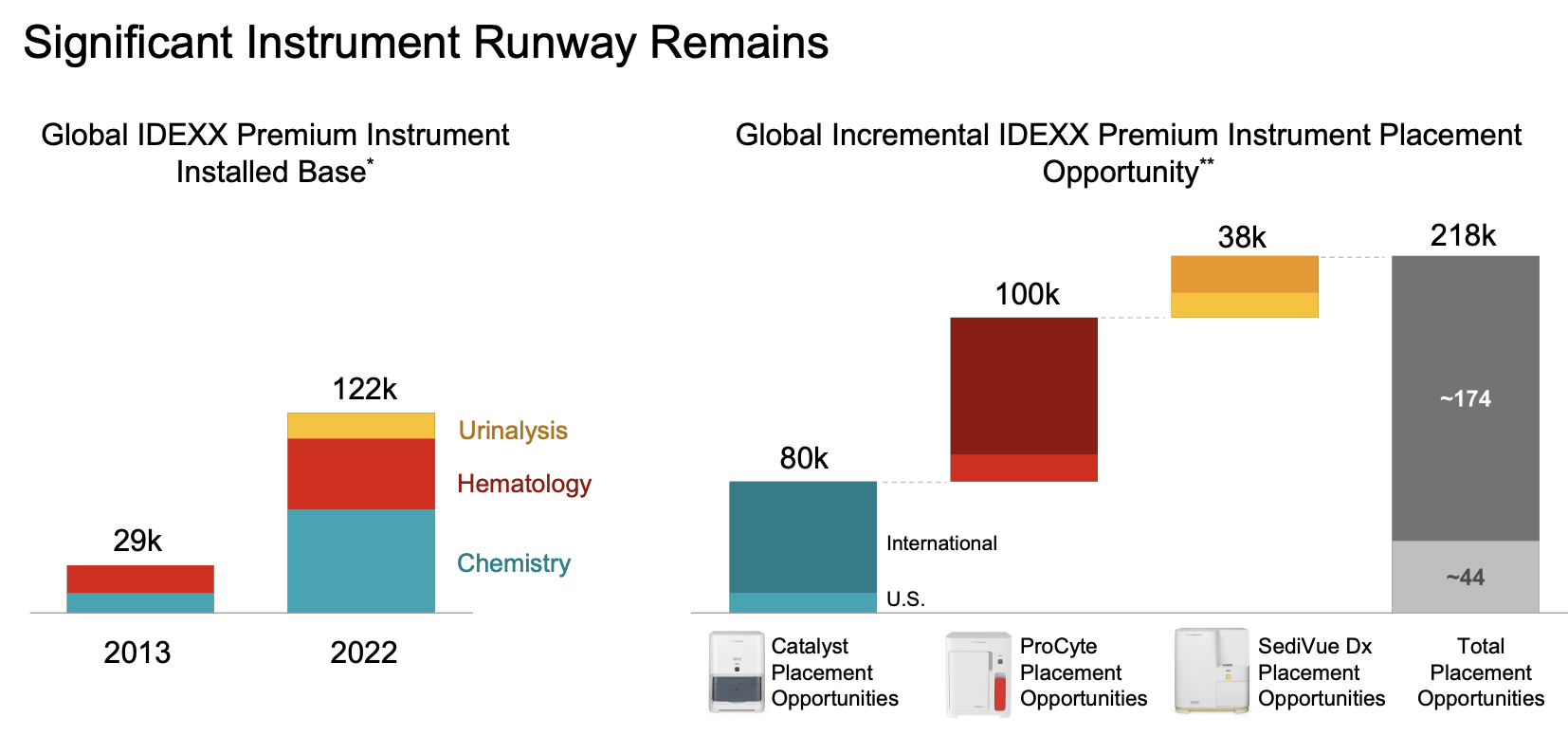

Given the company's view on the market, it believes that its current installed base of premium instruments of 122K units is far from what it can achieve.

The company is looking to reach an installed base of close to 220K premium instruments. Most of which is expected to come from its ProCyte program, which is able to perform a full analysis of multiple characteristics of each white blood cell.

{kind=link}

IDEXX Laboratories

This is what the company wrote about the ProCyte One in 2021 when it launched a new version:

ProCyte One reimagines point-of-care hematology with a radically simple workflow that virtually eliminates complexity without sacrificing performance," said Jay Mazelsky, President and Chief Executive Officer of IDEXX Laboratories. "Sometimes innovation is about making things simple in order to expand capabilities and advance what's possible.

With this in mind, not only does the company benefit from a rapidly rising installed base of recurring revenue, but it is also great at managing margins and generating strong free cash flow. These are important factors that determine if a company can generate high long-term compounding returns, as we discussed in the first part of this article.

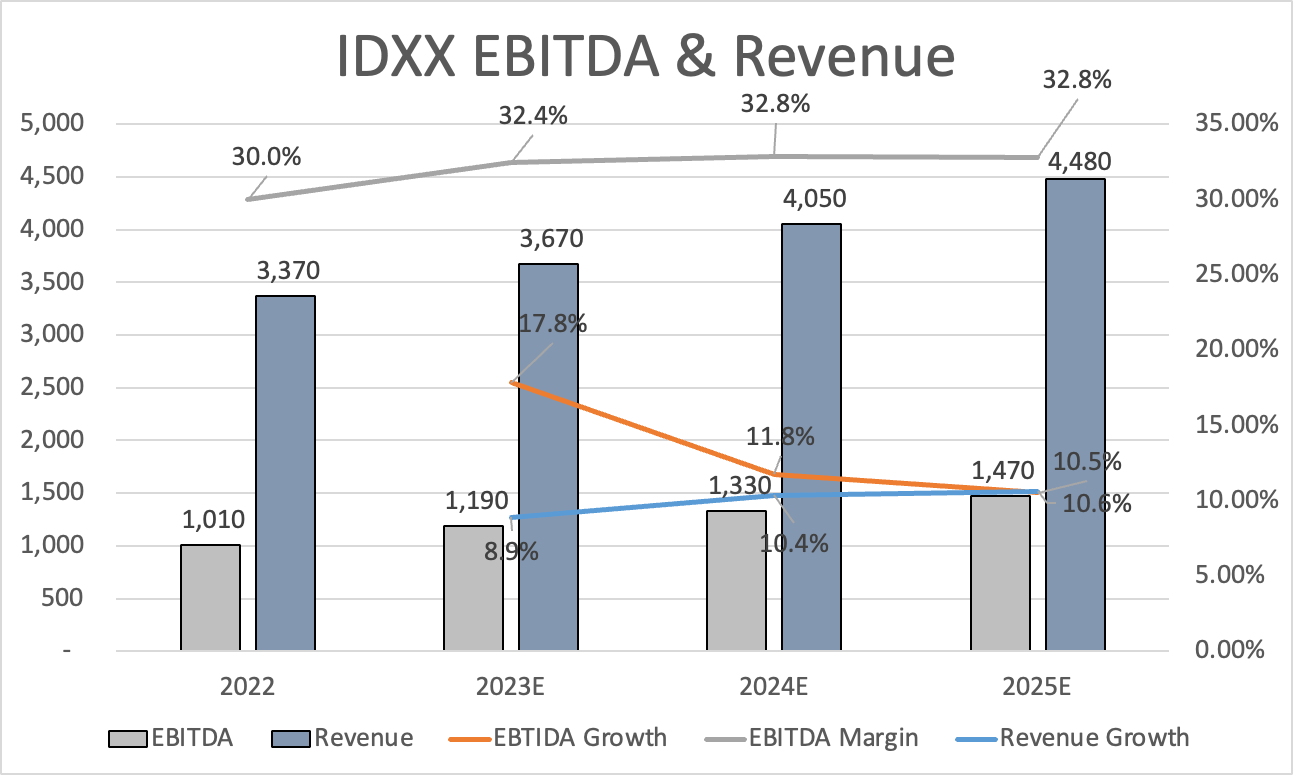

Since 2013, revenue has surged 160%. Thanks to higher margins, EBITDA and net income have soared by 225% and 278%, respectively. Free cash flow has risen by 175%.

Furthermore, cash conversion has been strong. The median is close to 90%, which means that $0.90 of every $1.00 in net income ends up as cash. This is a great sign of efficiency. After all, cash can be used for debt reduction and buybacks. A high net income is fine. However, when a company has a low FCF conversion, it's a bad sign. This is not the case here.

The FCF conversion rate is currently 66%. That number is expected to improve to at least 80% on a full-year basis.

This is usually the part where I discuss dividends. In the case of IDEXX, we're not dealing with dividends.

IDEXX buys back stock while maintaining a healthy balance sheet. This is what the company said in its first-quarter earnings call :

Our balance sheet remains in a strong position. We ended the quarter with leverage ratios of 1.1x gross and 1x net of cash down modestly from Q4 levels. Share repurchases over the last year supported a 1.9% reduction in diluted shares outstanding. We didn't allocate capital to share repurchases in the first quarter, as we manage our balance sheet relatively more conservatively in the current interest rate environment.

On a side note, the company has a BBB+ credit rating, which is one step below the A-range.

The company also dilutes stock, as it uses share-based compensation. However, SBC has been muted, which means that buybacks did end up reducing the number of shares in the past. Especially in the tech sector, it sometimes happens that aggressive buybacks do not end up reducing the number of shares, as aggressive SBC is used to reward employees.

Here's an overview of IDEXX's SBC and buybacks of the past there years:

- 2022: SBC $50 million, buybacks $812 million.

- 2021: SBC $38 million, buybacks $747 million.

- 2020: SBC $31 million, buybacks $183 million.

As a result, over the past ten years, the company bought back 23% of its shares, which contributed to the aforementioned outperformance.

With that in mind, let's take a closer look at recent developments and the company's valuation.

Recent Developments & Valuation

Not only did the company do well in the past, but IDEXX also had a solid start to 2023, with overall revenues increasing by 10% organically.

The growth was driven by a nearly 12% organic growth in CAG Diagnostics' recurring revenues. The increase in CAG Diagnostics' recurring revenue was supported by solid volume gains and benefits from higher net price realization, with the US experiencing nearly 14% organic growth.

Key execution metrics remained strong globally, including record first-quarter premium instrument placements, continued solid new business gains, and sustained high growth in recurring veterinary software revenues.

Operating profits and EPS increased by 18% on a comparable basis, reflecting solid organic revenue growth, better-than-expected gross margin gains, and benefits from a $16 million customer contract resolution payment.

Furthermore, IDEXX's full-year outlook for reported revenues is $3.6-$3.7 billion, with an estimated organic revenue growth range of 7.5-10%.

- The company maintains its outlook for solid operating margin performance in 2023, with reported operating margins expected to be in the range of 29-29.5%.

- The updated EPS outlook is $9.33-$9.75 per share, with foreign exchange impacts expected to decrease EPS by approximately $0.23 for the full year.

These numbers and developments support the company's longer-term bull case.

So, what does this mean in terms of valuation?

The company is trading at 31x 2024 EBITDA, which is based on its $40.7 billion market cap, $690 million in expected net debt, and $1.3 billion in expected EBITDA. Analysts expect long-term annual EBITDA growth to remain in the double-digit range.

{kind=link}

Leo Nelissen

This valuation is not cheap.

However, it is close to the longer-term median. Investors seem to be unwilling to let IDXX shares get to levels that might seem cheap. They continue pricing in high future growth. I agree with that. It's just unfortunate that we're not dealing with an attractive valuation.

The stock is currently trading 29% below its all-time high and 55% above its 52-week low.

The consensus price target is $560, which is 14% above the current price. I agree with that.

However, in order for me to buy this stock, I want to see a move lower to $400. There is a big risk that it won't fall that far, but it's a risk I'm willing to take, as I believe that sticky inflation and the Fed's response could be (short-term) bearish.

My stock rating is bullish to reflect the company's growth potential.

Takeaway

IDEXX Laboratories is a compelling compounder with sustainable long-term growth potential in the diagnostics and research industry.

Despite lacking dividends and an attractive valuation, IDXX possesses the key ingredients of a successful compounding stock. With a wide-moat business model, anti-cyclical customers, strong pricing power, innovation, a robust balance sheet, consistent growth, and high free cash flow conversion, IDXX has been an exceptional performer, delivering close to 1,000% returns over the past decade.

The company's focus on fast-growing veterinarian healthcare further contributes to its revenue expansion. As IDXX aims to increase its installed base of premium instruments, it stands to benefit from recurring revenue and efficient margin management.

Although IDXX doesn't have a dividend, I'm considering buying this stock if I get it close to $400.

For further details see:

IDEXX: One Of The Best Compounders On The Market