VEA - IDV ETF: Tasty Yield But Not Too Comforting Otherwise

2023-11-17 13:14:05 ET

Summary

- The iShares International Select Dividend ETF offers coverage to 100 high dividend-yielding developed market securities outside the US.

- We pick out some of the flaws in IDV's screening process.

- The ETF has a high yield but poor dividend growth and has delivered lower returns compared to a popular plain vanilla developed markets ETF.

- Global dividends already appear to be plateauing, and banks which dominate this portfolio are likely to be less generous.

- IDV does not look like a compelling option on the charts either.

The iShares International Select Dividend ETF ( IDV ) is a 26-year-old ETF, with over $4bn in AUM, that offers coverage to high dividend-yielding developed market securities, outside the US (do note that REITs are not considered).

Screening Is Not Rock-Solid

Before IDV's underlying index (The Dow Jones EPAC Select Dividend Index) arrives at the final portfolio of 100 odd stocks, it puts these through a whole host of screeners. Whilst most of these screeners are quite useful, and help augment the core goal of identifying reliable high-yielders, we find that some of the screeners are quite half-baked. This translates into a rather underwhelming performance of the ETF, which we touch upon later.

The initial universe comprises stocks from both the S&P EPAC BMI and the S&P Canada BMI indices. When exploring foreign counters, one can often get wedged with illiquid and high-risk names, and IDV does make an effort to reduce this risk by inculcating liquidity and market-cap screeners. Essentially, micro-cap stocks get weeded out, as IDV only considers stocks with a market cap of $1bn+. These stocks are also required to have a 3-month average daily dollar trading value of at least $3m.

Then you have a screener that requires a dividend track record of a minimum of 3 consecutive years (which in fairness is a pretty low bar).

Where we feel IDV misses the trick, is its emphasis on earnings-related metrics rather than cash-flow-related metrics. Firstly, it asks for these stocks to have just one period of "non-negative" TTM (trailing twelve months) EPS. EPS numbers can very often be skewed by non-cash items or one-off figures, and with IDV only demanding 1 year of data, this screener feels rather superfluous as you aren't going to get a great deal of insight from that.

Then there's yet another earnings-related metric - the 5-year dividend coverage ratio of a stock that is required to be higher than 1.18x, or greater than or equal to 66% of the corresponding S&P BMI country index.

It also appears that IDV is not overly keen to pursue dividend growers, but is rather just content with dividend-paying stocks as one of its screeners only requires that the TTM DPS must either be greater or equal to the 3-year average.

Eventually, note that the stocks that make the final cut are weighted based on the indicated annual yield (special dividends are excluded).

Is IDV Worth Pursuing?

If you aren't too pedantic about IDV's screening system and are still debating whether to take a position in this product, here are a few considerations that could help you arrive at a decision.

The yield on offer is a real attraction; whilst your plain vanilla flagship developed markets ETF - [[VEA]] currently only offers a figure of 3%, IDV's figure is almost 400bps higher at nearly 7%! Note that IDV's current yield is also a good 60bps more than its own historical average.

Supplementing that yield, you also want to see if this ETF has grown its distributions at a healthy pace. Unfortunately, IDV scores pretty poorly on that front. Note that over the last decade, the dividends have only grown at less than 0.6%, and in the more recent three-year period, the growth has only come in at 0.67%. That doesn't make for a great pitch, and it tells you that the high yield is largely a function of the weak denominator effect (dwindling ETF price).

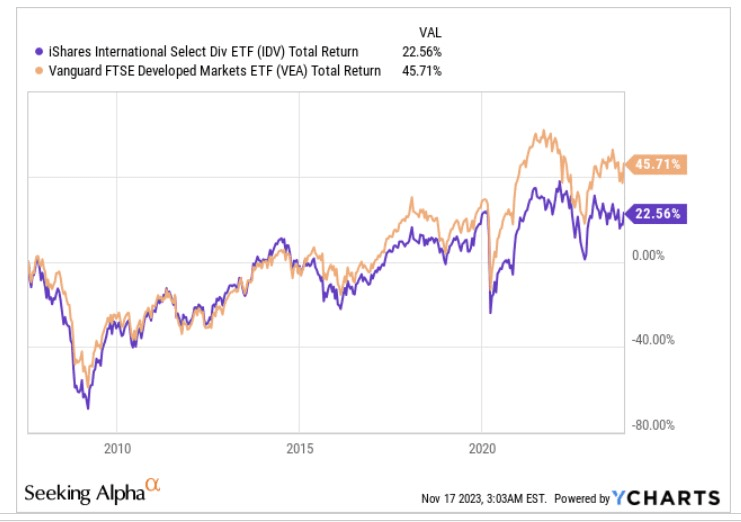

Then, as a long-term wealth compounder, it's also hard to be too chuffed with what IDV has delivered so far. Since its inception in 2007, it has only delivered returns of 22%, only half as much as what the Vanguard FTSE Developed Markets ETF has delivered.

{kind=link}

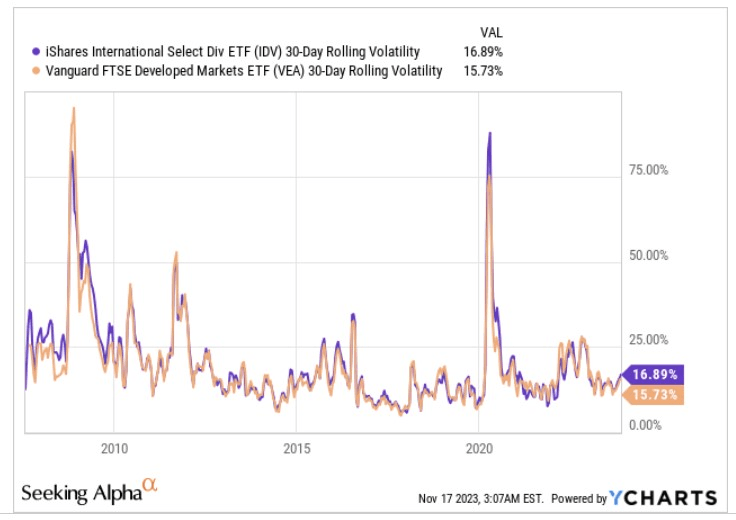

Even from a risk perspective, despite offering a more pronounced dividend tilt, note that IDV comes across as the more volatile option.

{kind=link}

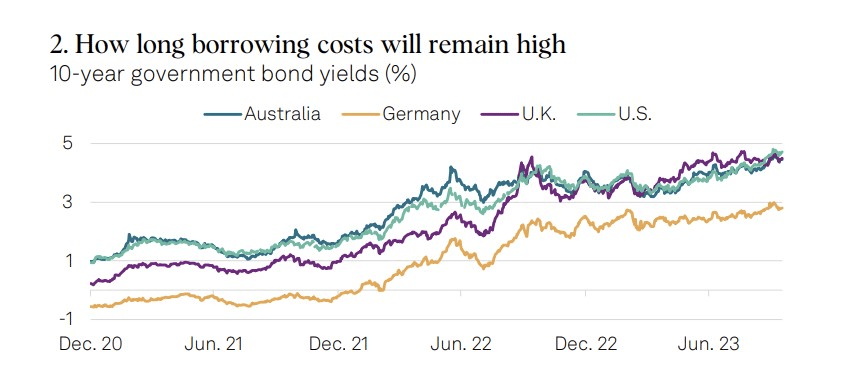

Coming back to the dividend narrative, one ought to question if conditions for dividend growth look particularly resilient. Compared to where they were a few years back, benchmark yields and the associated borrowing costs in some of the key developed markets have risen by large margins.

{kind=link}

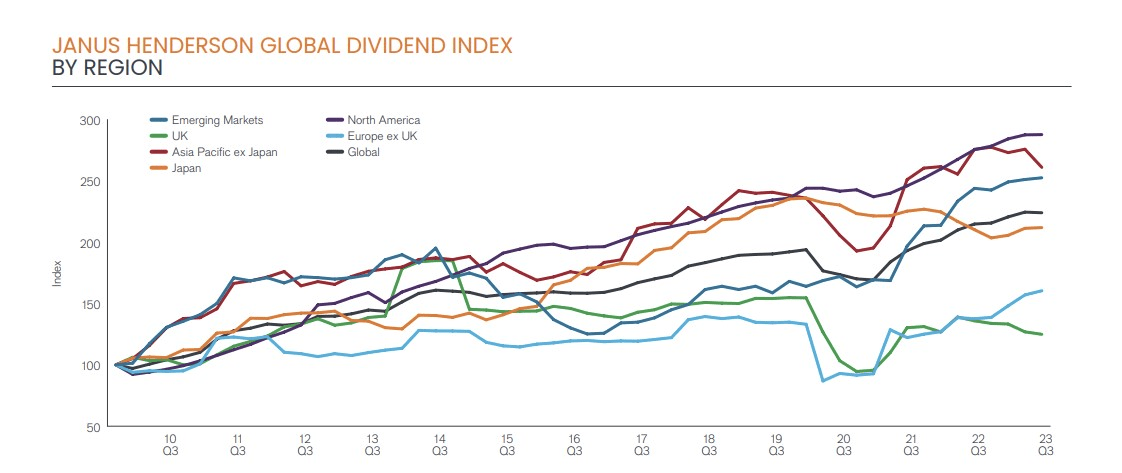

To mitigate the risk of higher borrowing costs, you could see developed market corporations focus on diverting any free cash flow towards delevering their balance sheets, rather than growing shareholder distributions. We believe one can already see the impact of this. A study by the asset management firm - Janus Henderson which specializes in analyzing global dividend trends shows that dividends in Q3 fell by 1%, prompting the firm to cut its FY global dividend forecast to $1.63 trillion from previous estimates of $1.64 trillion.

Janus Henderson

Also note that UK-based stocks take up the largest share of IDV's portfolio (~15%), and it appears that this is the region that is currently witnessing the weakest momentum in dividend growth.

{kind=link}

The IDV portfolio is also dominated by banking stocks (~27%), and we can't say the outlook here looks the most resplendent. Over the last 12-18 months developed market banks have seen their net interest margins ((NIM)) expand as policy rates get adjusted upward, but at this stage of the cycle, when central banks are draining excess liquidity from the system, funding costs will spike, limiting further NIM progression. Higher rates will also likely dampen business volume and potentially also lead to a spike in credit costs, as asset quality worsens in a higher rate regime. All in all, the flow through to the bottom line could be limited. Given, all these difficult considerations, investors shouldn't expect banks to be overly generous with their dividend distributions going forward, dampening the case for IDV even further.

Closing Thoughts - Technical Considerations

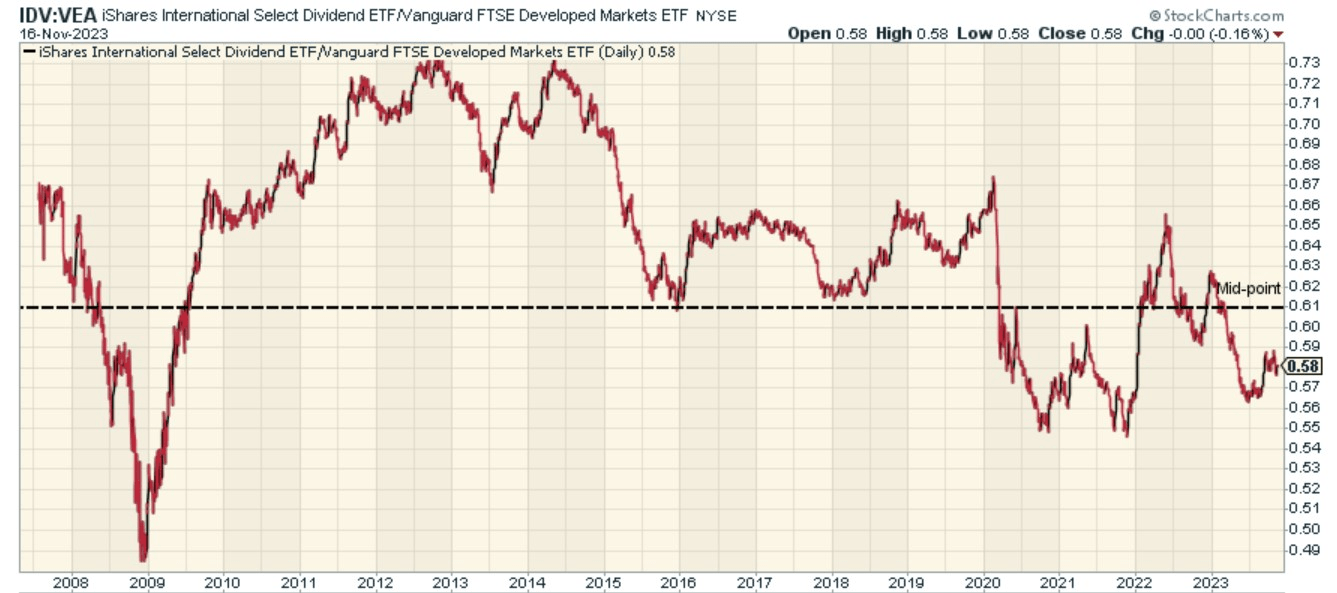

Those fishing for suitable mean-reversion opportunities in the developed market space may be open to considering IDV, given that the relative strength ratio is currently trading below the mid-point of the long-term range. However, that opportunity isn't overly compelling with a differential of just 5% or so.

{kind=link}

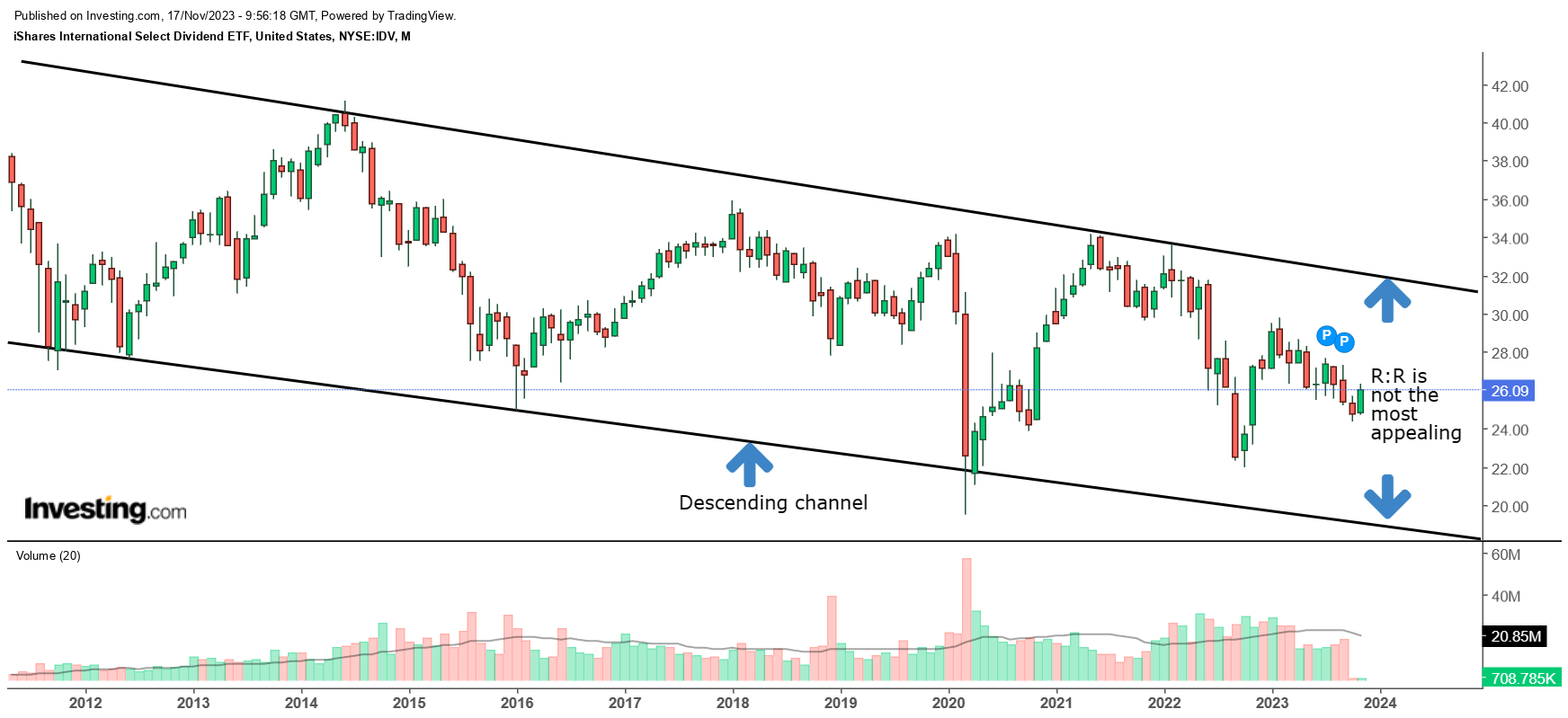

When it comes to IDV's price imprints, we can see that over the last decade, this ETF has steadily eroded investor wealth, in the shape of a descending channel. Within this channel, there have been trading opportunities to profit from the price movement, but history has shown that the most opportune period is when the price is trading closer to the lower boundary of the channel. Clearly, that's not where the price is currently; in fact, it is closer to the upper boundary of the channel, implying suboptimal reward to risk at this juncture.

{kind=link}

For further details see:

IDV ETF: Tasty Yield, But Not Too Comforting Otherwise