SPG - If Howard Marks' Sea Change Memo Is Correct REITs And High Yield Stocks Look Unattractive

2023-03-08 13:23:14 ET

Summary

- Yesterday, Chairman Powell signaled more rate hikes are required to tame this stubborn spell of inflation. The entire yield curve has moved up, and notably, during FY 2023.

- On December 13, 2022, Howard Marks penned a compelling piece - Sea Change. His chief argument is the era of cheap money was the driver of the robust equity returns.

- If rates are higher for longer, then investment grade bonds are safer and more attractive than REITs and High Yield Dividend Stocks. Many of these REITs are highly leveraged.

- As the cost of both equity and debt has dramatically re-priced, and higher, the attractiveness of REITs and High Yield Dividend Stocks is less attractive.

Seeking Alpha has millions - yes plural - of highly engaged readers who are retired or are nearing retirement. They may have (or may not have) saved enough for retirement, but on almost a daily basis, and by many authors, these retirees have been told and continue to be told that buying REITs ( VNQ ) or High Yielding dividend stocks is the magic elixir. The leading argument, in favor of these strategies, boils down to retirees need for income. And given this unquenchable thirst for income, it has been argued, a portfolio of High Yield Dividend stocks or REITs, paying those shiny quarterly (or in some cases, monthly) dividends is the best way to generate that safe and reliable income.

At face value, these are persuasive arguments as the demand for safe and reliable income greatly outstrips the readily available supply of truly SWAN like income. Given this strong demand for income, by the millions of retirees (or people rapidly approaching retirement), the notion of being able to pay for daily living expenses and enjoying their golden years has such a strong magnetic pull. In other words, with tens of million of retirees facing this dilemma, 'how to not outlive their savings', as their ultimate lifespan and relative healthy, on an individual basis, during their retirement years, is unknowable. Therefore, given this huge captive audience that is highly engaged and receptive towards this strategy, writing on REITs and High Yield Dividend stocks has become a cottage industry. This fear of outliving your money is such a pressing problem for retirees and something that keeps them up at night, therefore a messenger carrying the 'goods news', cleverly packaged and delivered in a such simply and easily digestible manner is well received. That said, it doesn't mean it's sound or empirically proven.

Moreover, usually explicitly, champions of this strategy argue don't worry about the underlying value of the principal, that is 'money good' and portfolio diversification will wash away many of the risks. In fact, when retirees ask about the inherent volatility in the underlying stock prices, they are assured not to worry, and that inherent volatility associated with these strategies are normal (or par for the course) and their investment principal is 'money good'. Just focus on seeing those monthly or quarterly shiny dividend payments getting deposited to your account. Don't worry about any portfolio drawdowns - remember, you bought the cow for the milk (the dividends) - so go out and enjoy life, travel, spending time with family and friends - not to worry - your portfolio of REITs and High Yield Dividend stocks are money good.

In this day and age, I would argue a portfolio of REITs and especially High Yield Dividend Stocks is bad advice! Likewise, the elephant in the room is so many of these REITs and High Yield Dividend stocks are highly leveraged.

And don't just take my word for it, the well regarded Howard Marks, of Oaktree, a person that has moved (and still moves) in upper echelons of the investment world, for north of fifty years, is implicitly saying the same thing.

Just go read his December 13, 2022 Sea Change Memo......

{kind=link}

( Source: OakTree - December 13, 2022 )

Howard has written a thought provoking and in-depth piece. It is well reasoned, even though I don't take it as gospel and only view it as one input as part of my broader process. That said, it can't be ignored and contains well constructed arguments.

Enclosed below, let me share two direct quotes and poignant sections, from Howard's Sea Change memo:

Exhibit A

The long-term decline in interest rates began just a few years after the advent of risk/return thinking, and I view the combination of the two as having given rise to ((A)) the rebirth of optimism among investors, ((B)) the pursuit of profit through aggressive investment vehicles, and ( C ) an incredible four decades for the stock market. The S&P 500 Index rose from a low of 102 in August 1982 to 4,796 at the beginning of 2022, for a compound annual return of 10.3% per year. What a period! There can be no greater financial and investment career luck than to have participated in it.

Exhibit B

{kind=link}

Now, I could write upwards of a dozen articles on why I think REITs or especially a High Yield Dividend stock portfolio isn't the panacea, for retirees. That said, this is a complex topic and we need to tackle it in smaller pieces.

Therefore, today, I want to focus on only one aspect. I want to shine the light on the inherent leverage risk, in the capital structures of many of these REITs, notably in this higher absolute interest rate environment.

As a proxy for REITs, let's look at the top eight holdings of the highly popular Vanguard Real Estate Index Fund. And by the way, this ETF has $65 billion in AUM. And to be clear, these are all high quality companies. However, many of them are super reliant on access to cheap debt capital for growth and that debt capital has dramatically re-priced over the past six months!

1. American Tower Corporation ( AMT ) : As of December 31, 2022, AMT has $32 billion of net debt.

Enclosed below, you can clearly see that AMT has benefited immensely from access to cheap money. Look at the weighted average interest rate of its debt (we are talking about fixed yields ranging from 2.30% to 3.49%).

{kind=link}

The days of cheap money and issuing billions of dollars of debt, with a 'two' handle, as the first number of the yield, are over.

2. Crown Castle Inc. ( CCI ) : As of December 31, 2022, CCI has $21.6 billion of net debt.

Similar to AMT, the vast majority of CCI's fixed rate debt has coupons ranging from 1.5% to 4.1%.

{kind=link}

3. Equinix, Inc ( EQIX ) : As of December 31, 2022, EQIX only has $10 billion of net debt. I don't have an opinion of the business, but I'm not overly concerned about the balance sheet leverage here per se.

4. Prologis, Inc ( PLD ) : As of December 31, 2022, PLD has $23.5 billion of net debt.

Per PLD's FY 2022 10-K, its average weighted interest rate is 2.5%.

{kind=link}

5. Public Storage ( PSA ): As of December 31, 2022, PSA has $6 billion of net debt.

I'm not overly concerned about Public Storage's balance sheet or leverage. Again, though, the average effective fixed interest rate is very low and its interest expense will drift higher.

{kind=link}

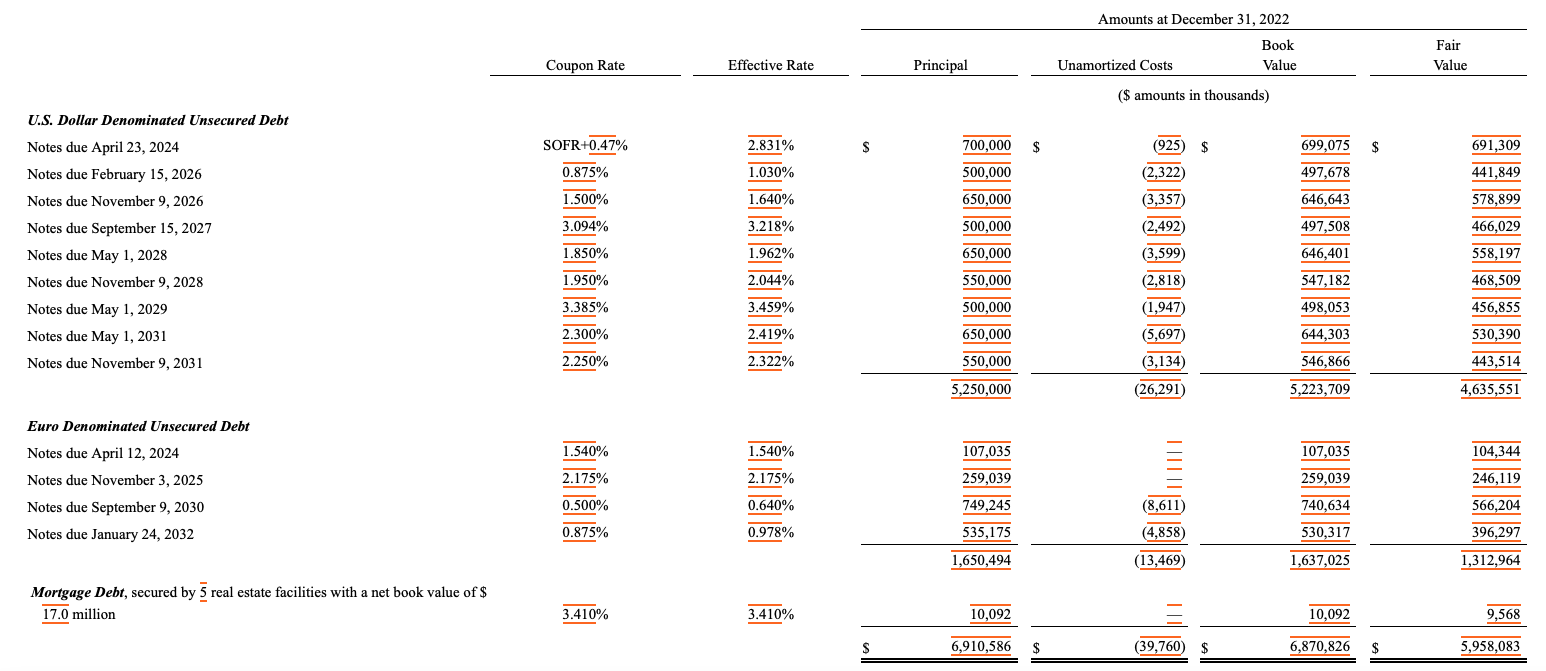

6. Realty Income Corporation ( O ) : As of December 31, 2022, O has $17 billion of net debt.

Per Realty Income's 10-K, its cost of debt has been extraordinarily low. Given the big move up in the yield curve and absolute rates, that is changing and its annual net interest expense will only increase from here.

{kind=link}

7. SBA Communications Corporation ( SBAC ) : As of December 31, 2022, SBAC has $12.7 billion of net debt.

As you can see, a very low cost of fixed rate debt.

{kind=link}

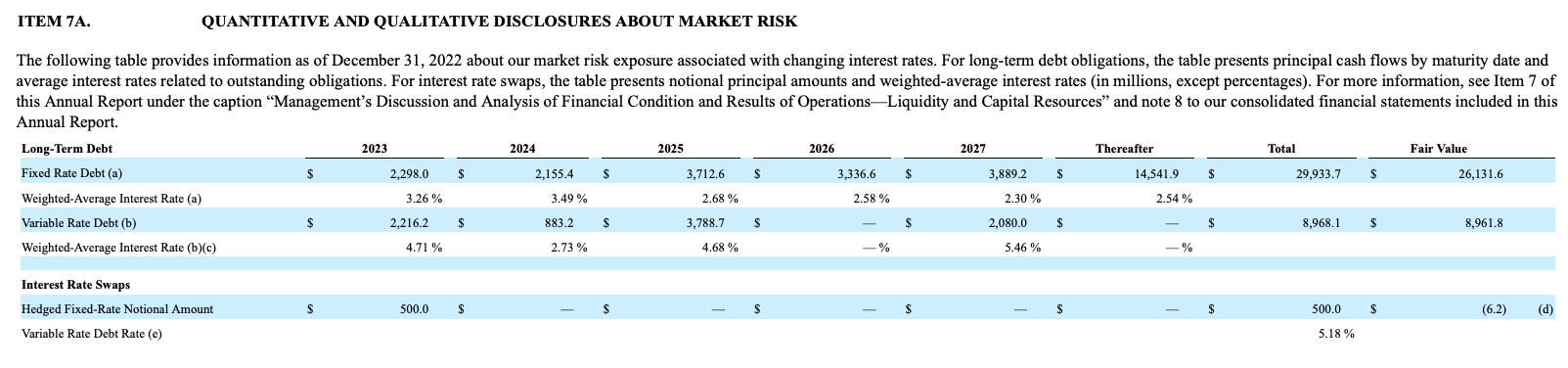

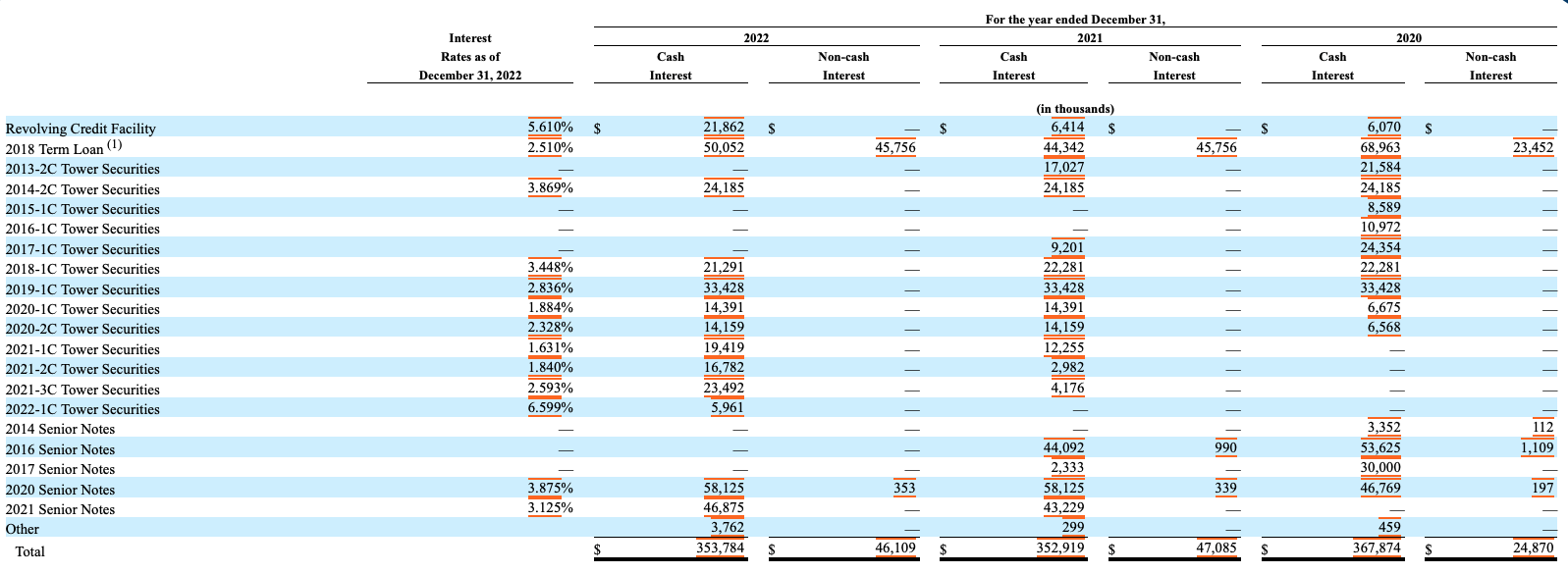

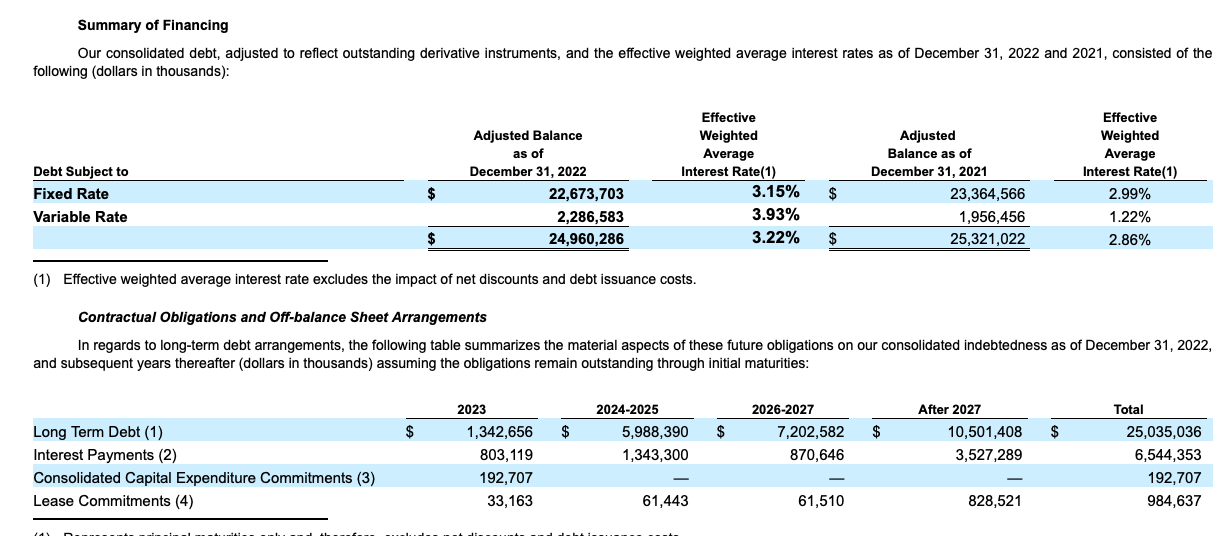

8. Simon Property Group, Inc. ( SPG ) : As of December 31, 2022, SPG has $24.3 billion of net debt.

Enclosed below, as you can see, Simon has enjoyed and benefited immensely from the era of cheap money. Simon's effective average interest, on the fixed side, was 3.15%, as of December 31, 2022.

{kind=link}

The issue:

So just to be clear, of course, I'm well aware that debt must be understood in relative terms to equity. In isolation, $20 billion of debt isn't problematic per se, especially if the underlying business's operating cash flow is robust and its equity value is much, much higher. That said, and again, all eight of these companies are high quality, but we can't lose sight of the fact that the cost of debt and equity has dramatically reset, given the big move up in rates and across the bond yield curve. Therefore, the relatively attractiveness of the yields, as in dividend yields, from an equity perspective is less attractive compared to bonds. These REITs, by design, are already paying a significant amount of their AFFO, in dividends. Higher rates mean higher interest expense and lower AFFO to pay out dividends. This leads to a double whammy of multiple compression and slower AFFO growth.

So I love seeing these cherry picked charts of how well REITs, as an asset class have performed, in the past. If we are keeping it real, and as Howard Marks might argue, one of the biggest drivers of the increase in the equity values has been the access to cheap debt capital. And if we following the logic, the relatively attractiveness of REIT yields, was then measured relative to the once extraordinarily low bond yields, due to a prolonged era of cheap money.

The era of cheap money is over!

Therefore, if you've telling retirees you have the solution to solve this incredibly hard issue of financial planning, and authors aren't rigorously stress testing the downside risks of permanent capital impairments, at the embryonic level (as in getting in the weeds and understanding the businesses) more so on the High Yield Dividend side of the house, then it starts to sound like magic beans.

On the high yield side of the house , in order to payout these juicy dividends, you have to understand how the sausage is made and where the yield is coming from. If it is from a (highly) leveraged balance sheet, or some exotic financial instruments, then as retirees, we should be very wary of the just how 'money good' your principal really is. It is fine to collect a year (or maybe even two years) of 9% annualized dividends, but if the dividend gets cut, in this much tougher macro backdrop, with slower growth rates and much higher costs of capital (both equity and debt), your principal can be at risk of permanent impairment.

A Better Alternative - Investment Grade Bonds

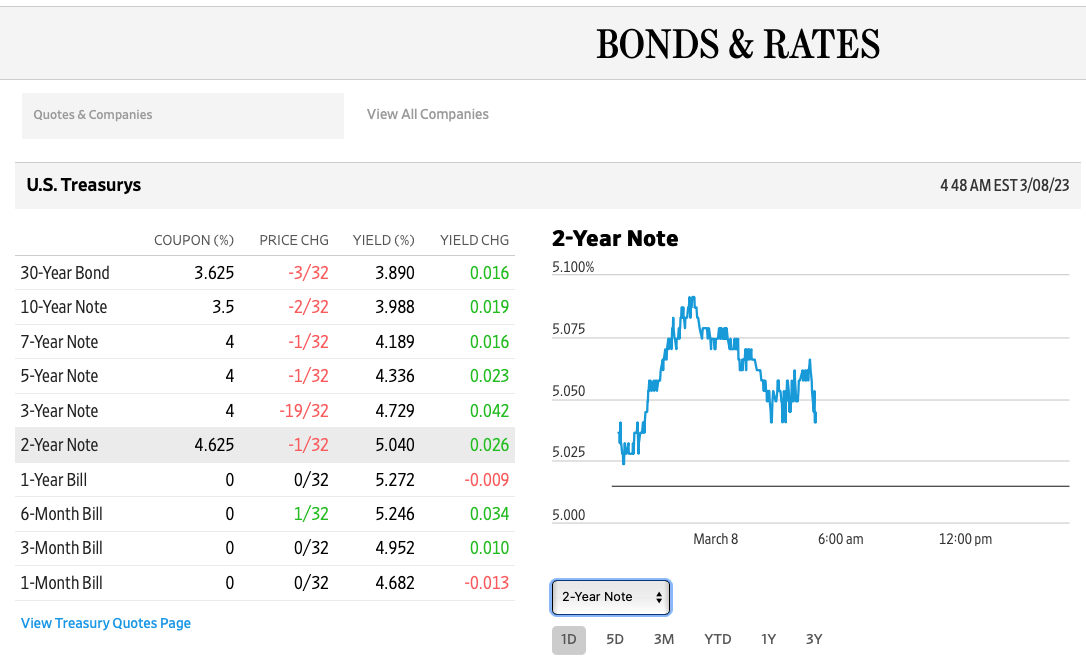

And if you look at the yield curve, given how much the Fund Funds rate has moved up, bonds are a much safer and better alternative.

{kind=link}

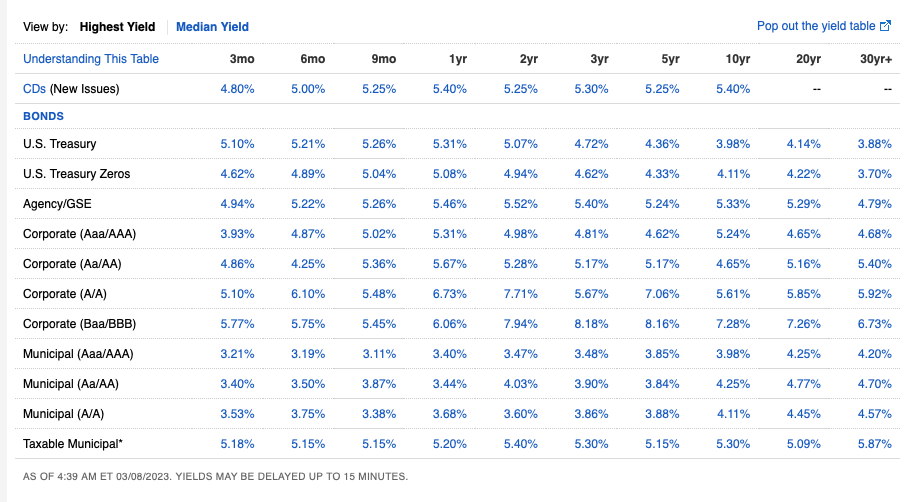

Secondly, and here is a snapshot, from Fidelity, displaying the Median Yields, as of March 7, 2023 (the close of business). This chart nicely captures Fidelity's actual inventory of bonds, in a moment in time, organized by maturity date, type of bond (Treasury, Agency, Corporate, Municipal, etc.), and 'median yield'.

{kind=link}

As you can clearly see, if you're willing to venture out five to ten years, on the maturity yield curve, there are plenty of high quality investment grade [IG] corporate bonds currently sporting yields of 5% to 7%.

And as the good steward of the vast majority of my parents' liquid financial wealth, back in late October 2022, I shared my specific IG bond portfolio that I created on their behalf, with a portion of their taxable retirement savings (see - My Gift To Retirees: Sharing My Recently Constructed $300K Investment Grade SWAN Portfolio ).

In a nutshell, and this portfolio is designed to be SWAN like, I didn't mess around with IG bonds of financial companies unless the underlying company is super high quality, such as a JPMorgan ( JPM ) or Bank of America ( BAC ). I would never, ever reach for yield and buy an IG bond of a questionable financial company, like a Credit Suisse ( CS ). And as I'm very risk averse, with this portion of the portfolio, as I only want exceptionally high quality companies.

Putting It All Together

If Howard Marks is correct that this is in fact the third 'Sea Change' of his 53 year (and counting) investment career then I'm not so sure REITs do so well. Secondly, and I plan to continue exploring this topic, albeit periodically, in future pieces, I would argue High Yield Dividend stocks could perform very poorly in this much more difficult market, as oceanic forces consisting of much higher costs of both debt and equity capital have dramatically re-priced, and higher. Trust me, I get the allure of collecting juicy quarterly dividends. On paper and at face value, it seems like a great strategy. That said, the market is relatively efficient and you must understand why equities are priced at such dividend high yields. Perhaps, more often than not, and I'm excluding intentionally excluding period of exogenous shock, such as Covid, in March 2020 and April 2020, and the 2008/09 housing crash, I would argue the downside risks are real and that is why the dividend yield are so high.

Therefore, if people are investing the vast majority of their retirement savings, in this strategy, I would argue it is paramount to rigorously stress test the underlying quality of the securities contained within a portfolio. Yes, collecting those shiny dividends is fine, but only if the principal is truly 'money good'. Once you are retired, unless you are extraordinarily talented or have some unique set of skills, more often than not, it is very difficult to go back into the labor force, if you had to, due to a bad financial setback or event. Simply put, retirees can't risk having a big reversal or a poorly constructed stock portfolio. Don't chase yield! It just isn't worth it.

In closing, I'm going to end this note with the timeless wisdom of Dr. Seuss:

Just never forget to be dexterous and deft. And never mix up your right foot with your left.

(Dr. Seuss - Oh, the Places You'll Go!)

For further details see:

If Howard Marks' Sea Change Memo Is Correct, REITs And High Yield Stocks Look Unattractive