BTAFF - If I Could Only Buy 2 Dividend Stocks In April 2023

2023-04-11 13:00:00 ET

Summary

- In today’s article, I will introduce you to my two top dividend picks of the month, which I currently consider attractive due to various factors.

- Both companies have strong financial health, possess important competitive advantages and their valuation is currently attractive.

- One of the picks can contribute to raising the Average Dividend Yield [FWD] of your portfolio, the other one to increase its Average Dividend Growth Rate.

Investment Thesis

When building an investment portfolio, I consider it crucial that you reach a balance regarding achieving an attractive Dividend Yield while, at the same time, reaching an attractive Dividend Growth Rate. This allows you to gain a significant additional income today, which could increase at an attractive growth rate over the long term.

In order to help you to reach this, I will present you in today’s article with my two top picks of the month, which I would select in case I could only choose two dividend paying companies.

One of the picks provides your investment portfolio with a high Dividend Yield and the other one with significant Dividend Growth.

My two top picks of the month fulfill the following requirements:

- Strong competitive advantages over its competitors

- Economic Moat

- Strong financial health

- Relatively low Payout Ratio

- Attractive Average Dividend Growth Rate over the past 5 years

- Dividend Yield [FWD] > 0%

- Attractive Valuation

These are the two companies I have selected for this month of April:

Altria

Altria manufactures tobacco products and was founded in 1822. The company currently has 6,300 employees and a Market Capitalization of $79.33B.

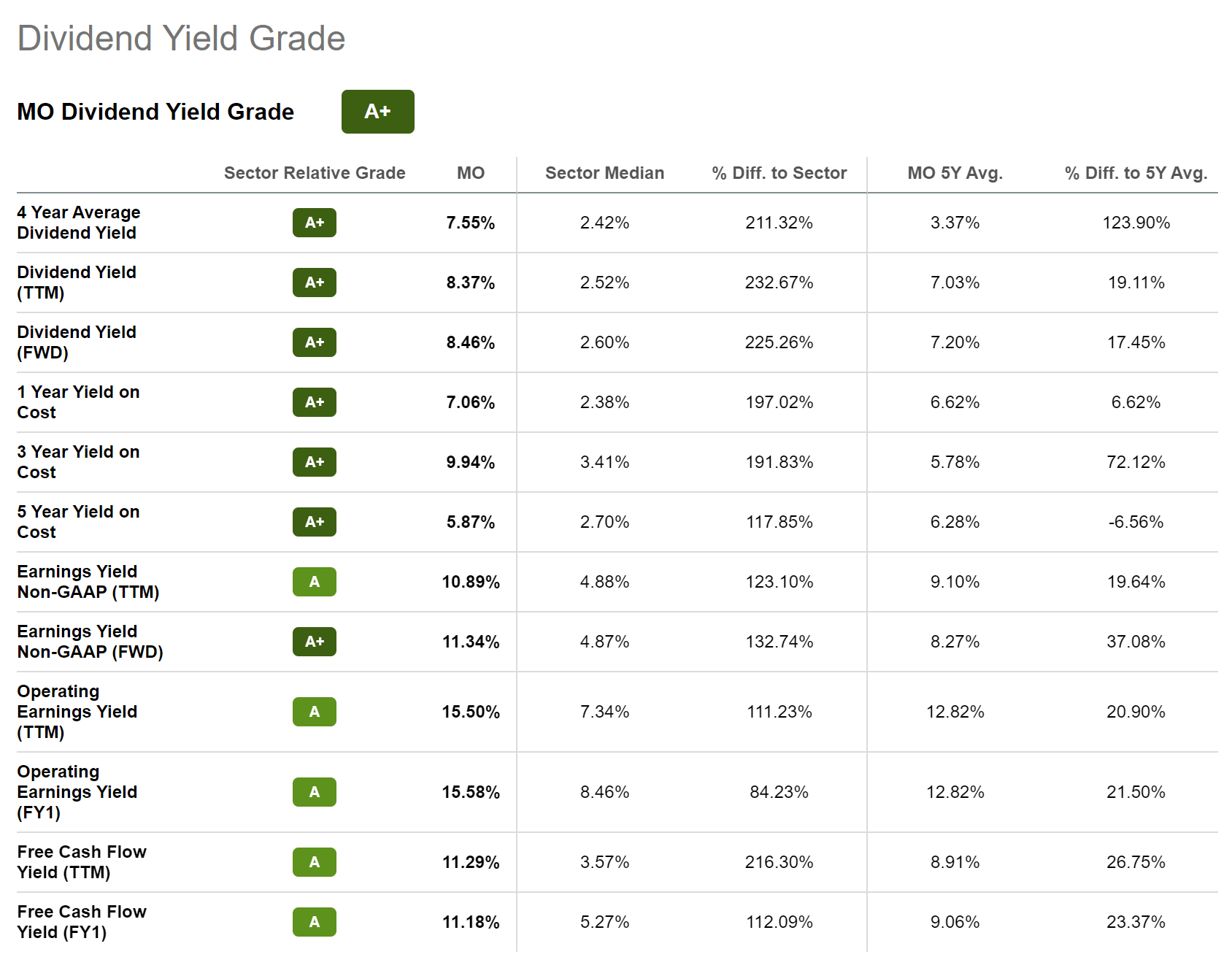

At its current share price, Altria pays shareholders a Dividend Yield [FWD] of 8.46%. This is an attractive Dividend Yield for investors, particularly considering that the company’s Payout Ratio only stands at 76.03%.

At present, the company boasts a Free Cash Flow Yield [TTM] of 11.29%, which lies 216.30% above the Sector Median of 3.57%. At the same time, its current Free Cash Flow stands 26.75% above its Average Free Cash Flow Yield [TTM] over the past 5 years. Below you can find the Seeking Alpha Dividend Yield Grade, which strengthens my belief that Altria is currently an attractive pick for investors, particularly due to the company’s attractive Dividend Yield.

{kind=link}

On top of that, the company has shown significant Dividend Growth over the past decade and this is what makes Altria particularly attractive from my point of view: the company combines a high Dividend Yield with an attractive Dividend Growth Rate. Altria’s Dividend Growth Rate 10Y [CAGR] has been 7.96%, which lies 27.73% above the Sector Median (6.23%).

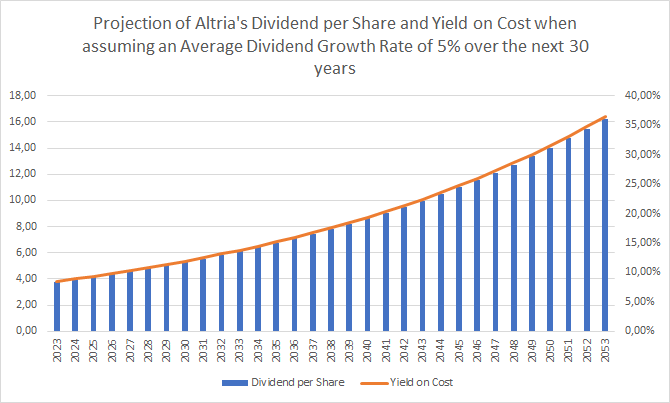

The graphic below shows how you could benefit from an investment in Altria assuming that the company would be able to provide shareholders with a Dividend Growth Rate of 5% over the next 30 years. The graphic shows the company’s Dividend per Share and the Yield on Cost assuming that you would invest at the company’s current stock price of $44.45. The graphic shows that you would reach a Yield on Cost of 13.78% in 2033, of 22.44% in 2043 and of 36.56% in 2053.

{kind=link}

Atria’s Valuation

In terms of Valuation, it can be highlighted that the company currently has a P/E GAAP [FWD] Ratio of 8.82, which stands 57.41% below the Sector Median, serving as a first indicator that the company is currently undervalued.

The same is confirmed when we compare the company’s current P/E [FWD] Ratio with its Average over the past 5 years: the company’s current P/E [FWD] Ratio stands 32.47% below its Average from the past 5 years (13.06).

In addition to that, Altria’s current Dividend Yield [TTM] of 8.37% stands 232.67% above the Dividend Yield [TTM] of the Sector Median (which is 2.52%) and 19.11% above its Average Dividend Yield [TTM] over the past 5 years (7.03%), further indicating that Altria is very attractive at its current Valuation.

Taking into account the company’s Price / Cash Flow Ratio [TTM], the same is confirmed: the company’s current Price / Cash Flow Ratio [TTM] of 9.61 stands 39.97% below the Sector Median (16.01) and 17.30% below its Average over the past 5 years (11.62). All these metrics, once again, confirm that Altria is currently undervalued.

When compared to its peer group, Altria’s low Valuation is again confirmed, further strengthening my current buy rating for the company: while Altria has a P/E [FWD] Ratio of 8.82, British American Tobacco’s (NYSE: BTI ) is 9.26 and Philip Morris International’s (NYSE: PM ) is 15.54.

In addition to that, I see Altria in front of its competitors when it comes to Profitability: while Altria has an EBIT Margin [TTM] of 59.46%, British American Tobacco’s is 42.17%, Japan Tobacco’s ([[JAPAY]], [[JAPAF]]) is 23.95%, Imperial Brands’ ([[IMBBY]]) is 19.00% and Philip Morris International’s is 39.03%, indicating that Altria is the most attractive choice when it comes to Profitability.

Mastercard

I consider Mastercard to be an excellent pick at this moment in time due to many reasons.

First, Mastercard has strong competitive advantages over its competitors: among its competitive advantages are, for example, the company’s enormous financial health, its large number of debit and credit cards, its strong brand image, and the company’s worldwide financial network.

Mastercard has shown strong results in terms of Dividend Growth over the past decade, which is proven by its Dividend Growth Rate 10Y [CAGR] of 30.32%, standing 273.73% above the Sector Median. The company has shown 11 Consecutive Years of Dividend Growth.

I see Mastercard ahead of its competitors in regards to Growth: this is underlined by the company’s Revenue Growth Rate [FWD] of 14.77%. Mastercard’s Growth Rate [FWD] is superior when compared to Visa (NYSE: V ) (Revenue Growth Rate [FWD] of 14.22%), PayPal (NASDAQ: PYPL ) (8.16%), Fiserv (NASDAQ: FISV ) (5.94%), Block (NYSE: SQ ) (9.28%) and Fidelity National Information Services (NYSE: FIS ) (2.72%).

In terms of Profitability, Mastercard is also ahead of most of its competitors: while Mastercard has an EBIT Margin [TTM] of 56.77%, PayPal’s is 14.88%, Fiserv’s is 20.86%, Block’s is -3.30% and Fidelity National Information Services’ is 11.62%. Mastercard also has a significantly higher Return on Equity (144.03%) when compared to Visa (Return on Equity of 41.51%), American Express (NYSE: AXP ) (32.05%), PayPal (11.52%), Fiserv (8.11%), Block (-5.38%) and Fidelity National Information Services (-44.59%), which demonstrates Mastercard’s strength in terms of Profitability.

When it comes to Profitability, Mastercard is even ahead of Apple (NASDAQ: AAPL ) (even though they are not direct competitors, Mastercard competes with Apple Pay within the Mobile Payments Industry): Apple’s EBIT Margin [TTM] of 29.41% is significantly lower than the one of Mastercard. However, it should also be highlighted that Visa has an even higher EBIT Margin [TTM] (67.14%) than Mastercard.

Mastercard’s Valuation

Mastercard’s current P/E GAAP [FWD] Ratio stands at 29.83, which is 20.88% below its Average over the past 5 years (which is 37.70). This can serve as a first indicator that Mastercard is currently undervalued.

This is also confirmed when we have a look at the company’s Price / Sales [FWD] Ratio: while the company’s Price / Sales [FWD] Ratio currently stands at 13.82, its Average Price / Sales [FWD] Ratio over the past 5 years has been 16.58, further strengthening my theory that the company is currently undervalued.

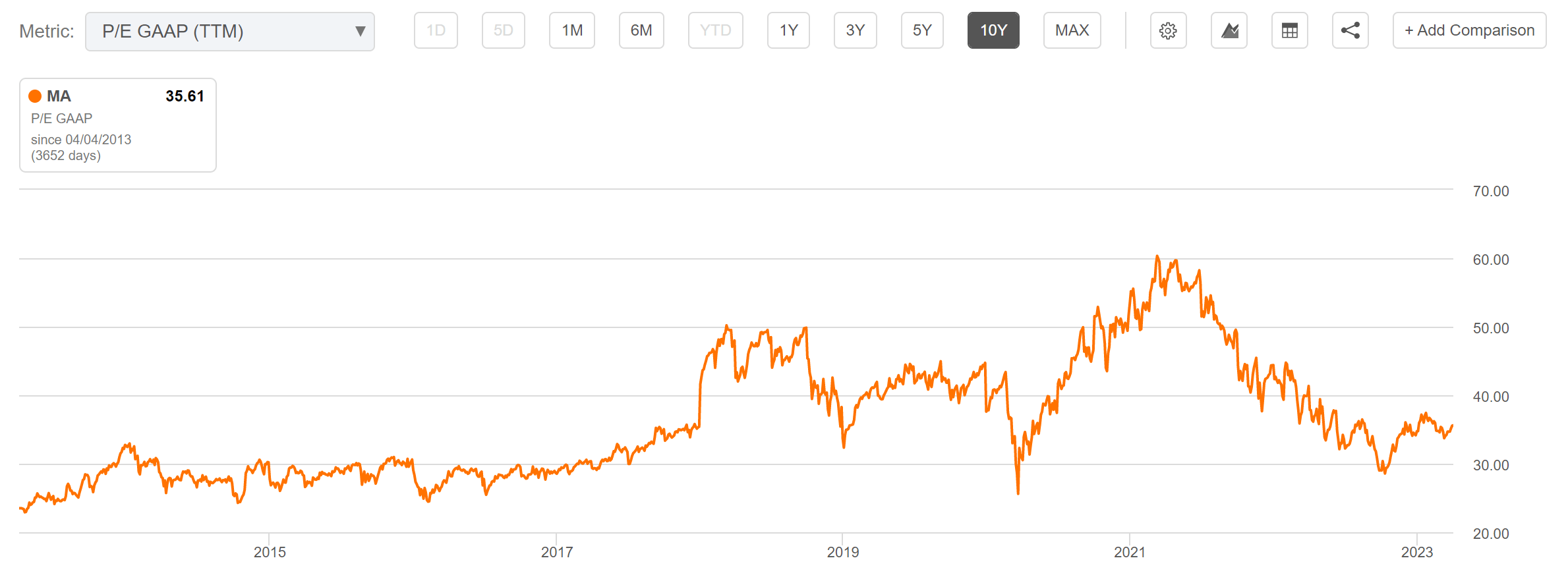

In the graphic below you can further see that Mastercard’s P/E GAAP [TTM] Ratio is currently relatively low compared to its P/E GAAP Ratio of the past 10 years, further strengthening my theory that the company currently has an attractive Valuation.

{kind=link}

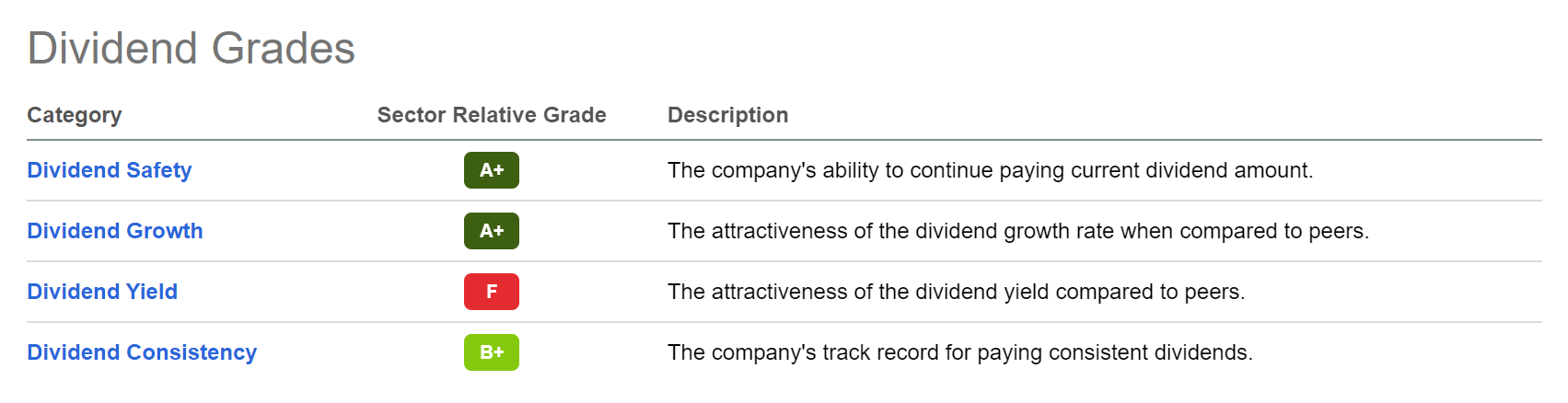

Moreover, the Seeking Alpha Dividend Grades demonstrate that Mastercard is an excellent pick, particularly for dividend growth investors: the company receives an A+ rating for Dividend Safety and for Dividend Growth.

{kind=link}

Conclusion

When constructing an investment portfolio, achieving a mix between an attractive Dividend Yield [FWD] and a relatively high Dividend Growth Rate is crucial in my opinion. Through the combination of both, investors can be able to achieve a significant Dividend Income today while increasing this amount to a relatively high level over time.

In order to help you to reach this objective, I have selected for you two stocks that I currently consider to be very attractive: one of the picks is a company that pays a high Dividend Yield [FWD] of 8.46% ( Altria ) and the other pick is one that provides your portfolio with significant Dividend Growth (Mastercard).

I consider both companies to be excellent long-term investments, since both have substantial competitive advantages and enormous financial health. In addition to that, both companies currently have an attractive Valuation, which has additionally contributed to selecting them as my top of the month dividend paying stocks.

Moreover, I would like to highlight that I consider both Altria and Mastercard as excellent picks in terms of risk and reward, which makes me conclude that you could overweight both in an investment portfolio build with a long investment-horizon.

Assuming that you would invest an equal amount in both companies, their Average Dividend Yield [FWD] would be 4.55% (Altria’s Dividend Yield [FWD] is 8.46% while Mastercard’s is 0.63%). At the same time, both would have shown an Average Dividend Growth Rate of 12.42% over the past 5 years (Altria’s 5 Year Dividend Growth Rate is 7.18% and Mastercard’s is 17.66%). This makes both the perfect selection for your portfolio to combine dividend income with dividend growth.

I would love to hear your opinion on this article and which dividend companies you would select during this month of April in case you could only choose two?

For further details see:

If I Could Only Buy 2 Dividend Stocks In April 2023