WPC - If I Could Only Own 7 REITs It Would Be These

2023-07-31 13:41:18 ET

Summary

- I own 18 individual REITs and believe that all of them are great real estate businesses with strong growth prospects.

- I'd argue that diversification is not the main goal of owning multiple REITs, but rather conviction in each individual company.

- That said, if I could only own a handful of REITs, there are some truly top-tier, best-in-class names that I could narrow it down to if I had to.

- I highlight the 7 REITs that I would choose if I could only own that many, articulating what gives them unique qualities and competitive advantages.

I own a lot of real estate investment trusts ("REITs"). As of the end of July, I own 18 individual REITs.

Some would say that 18 REITs is too many -- that I would still be able to achieve all the benefits of diversification in this stock sector by owning far fewer REITs. After all, there aren't even that many sectors of real estate or basic property types. Clearly, I own multiple REITs in some of the same sub-sectors.

To this I would respond that all 18 of the REITs I own are great businesses with fantastic real estate, smart investment philosophies, skilled and shareholder-aligned management teams, modest or low leverage, strong costs of capital, and bright future growth prospects.

The "over-diversification" criticism may make sense in theory, but not when one has a sufficient level of knowledge and conviction about the companies they own.

Besides, the point in owning 18 REITs is not diversification per se. It's conviction in each individual company . As Warren Buffett has wisely said:

Diversification is protection against ignorance. It makes little sense if you know what you are doing.

If diversification is your goal, it would probably be better simply to own an ETF or mutual fund rather than individual stocks.

For example, if you'd like real estate exposure, consider buying the Vanguard Real Estate ETF ( VNQ ). It has quite a good history of generating total returns. From the mid-2000s until COVID-19, it even outperformed the S&P 500 ( SPY ):

But I would not recommend buying individual stocks, REITs, or assets simply for diversification's sake.

Imagine the silliness of someone saying, "You know, I'm not particularly bullish on _____ (gold, bitcoin, emerging market bonds, private equity companies, commercial real estate, etc.), but I'd better own some anyway for the sake of diversification." If that is your thinking, I would urge you to seek the counsel of a registered investment advisor.

With all of the preceding said, I have been asked in the past by REIT newcomers where to start looking for great REITs. Sometimes the question is phrased as which handful of top-tier REITs they should research first. Other times, it's phrased as, "Austin, if you could only own five REITs, what would they be?"

That's a great question. I've tried to narrow it down to five in the past and simply haven't been able to distill it to that nice, round number without feeling like I've excluded other, equally high-quality names.

But I do think that seven of my 18 REITs are a tier above the others -- true best-in-class businesses in their respective sub-sectors.

In what follows, I'll give a brief pitch for each of these seven REIT all-stars and try to articulate what gives them their own respective competitive advantages.

Agree Realty Corporation ( ADC )

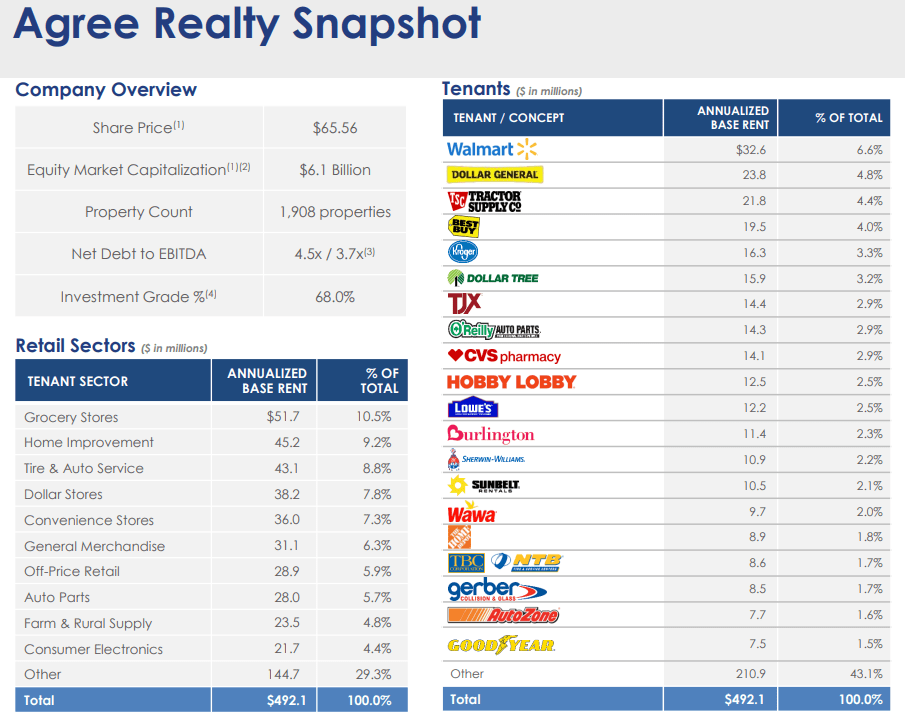

ADC is a net lease REIT specializing in single-tenant, primarily freestanding properties leased to the nation's largest, strongest, and fastest growing retailers. In fact, ADC is one of the largest landlords to retailers like Walmart ( WMT ), Tractor Supply Company ( TSCO ), Dollar General ( DG ), and Best Buy ( BBY ).

{kind=link}

ADC June Presentation

These are companies that are not only able to survive the growth in e-commerce, they are themselves at the leading edge of technologically enabled retail commerce through mobile ordering, home delivery, curbside pickup, and so on.

And Walmart's swiftly advancing drone delivery capabilities look like they are progressing even faster than those of Amazon ( AMZN ).

ADC owns prime real estate leased to the cream of the crop in the retail world.

{kind=link}

ADC June Presentation

But that's only one aspect of ADC's best-in-class character. Another is the balance sheet and cost of capital advantage.

ADC constantly maintains a relatively low leverage ratio (net debt to EBITDA almost always under 5x, which is quite low for real estate investments) as well as pool of forward equity to tap for investments. These multi-hundred-million dollar forward equity deals are locked in at a certain price, allowing ADC to go out and find investments that will be accretive to that price.

In addition, ADC enjoys a BBB credit rating, and the debt it has secured in recent years is often priced as if the REIT had an even higher credit rating than that. With this low cost of capital, ADC is able to bid competitively for the best real estate. Well-located properties leased to top-tier retailers naturally bear higher pricing and lower yields, and ADC is now one of the few players in its space that is still able to invest accretively.

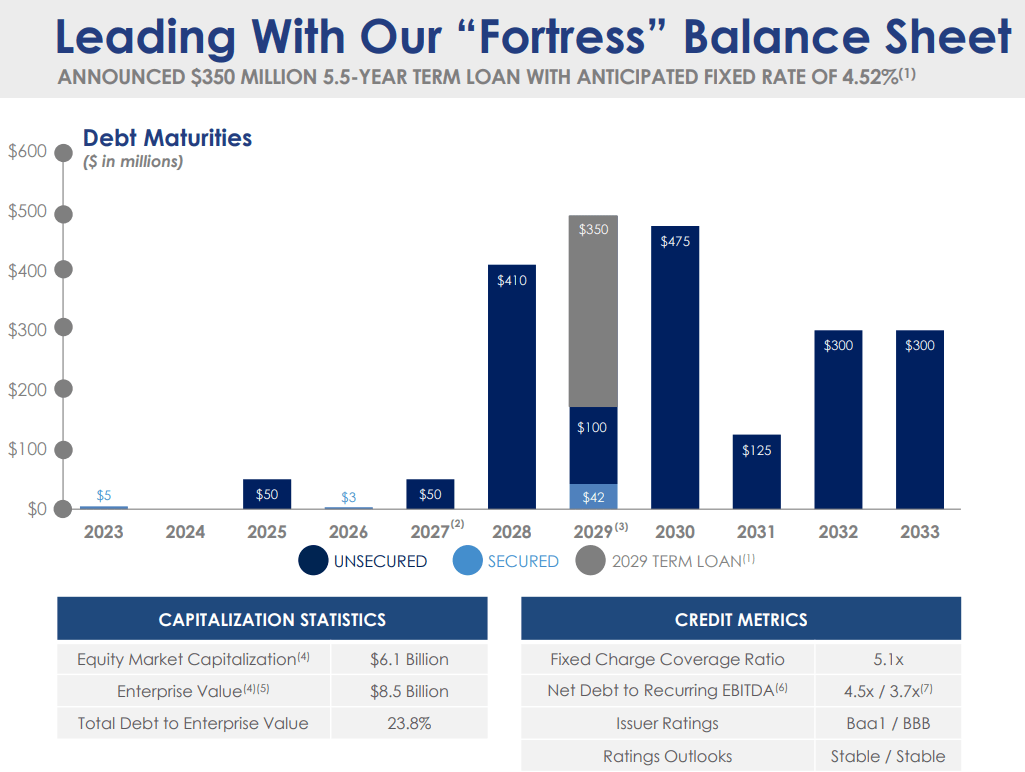

Moreover, amid elevated interest rates, ADC's fortress balance sheet is a massive strength. Almost no debt matures until 2028.

{kind=link}

ADC June Presentation

Lastly, it's noteworthy that ADC is led by its forward-thinking and outspoken CEO, Joey Agree, whose interests are about as aligned with shareholders as a chief executive's possibly could be.

Alexandria Real Estate Equities ( ARE )

Named after the Egyptian city that was once a center of knowledge and science, exemplified by the Library of Alexandria, ARE's buildings are a modern-day facilitator of the advancement of knowledge and science.

ARE is the only pure-play owner and developer of state-of-the-art, Class A life science (laboratory research) facilities on the public markets. These beautiful and technologically advanced buildings are located in the most productive and innovative research clusters in the nation such as Boston, San Francisco, San Diego, Seattle, and the Research Triangle in North Carolina.

{kind=link}

ARE Q2 Earnings Report

Amid an oncoming wave of new life science supply coming online in the next few years as owners of older office buildings convert space from traditional office use to laboratories, it's important to recognize ARE's competitive advantages in this industry.

- ARE has been a major player in this space for three decades, honing its investment philosophy and strengthening its tenant relationships.

- The REIT focuses on innovation clusters, or mega-campuses wherein multiple biotech companies gather in relatively close proximity for purposes of networking and compounding of knowledge. Much research has demonstrated the superior productivity of these clusters over standalone facilities.

- ARE specializes in the highest quality, most state-of-the-art building designs, many of which were developed in-house, for maximum appeal to the world's best biotech companies.

- ARE has a small venture capital arm, which exists in part to bring up and establish relationships with the next generation of biotech innovators.

- ARE's triple-net leases obligate the tenant to pay for all building maintenance, insurance, and taxes while also providing 3% annual rent escalators. This makes for a very high margin, low ongoing capex business model.

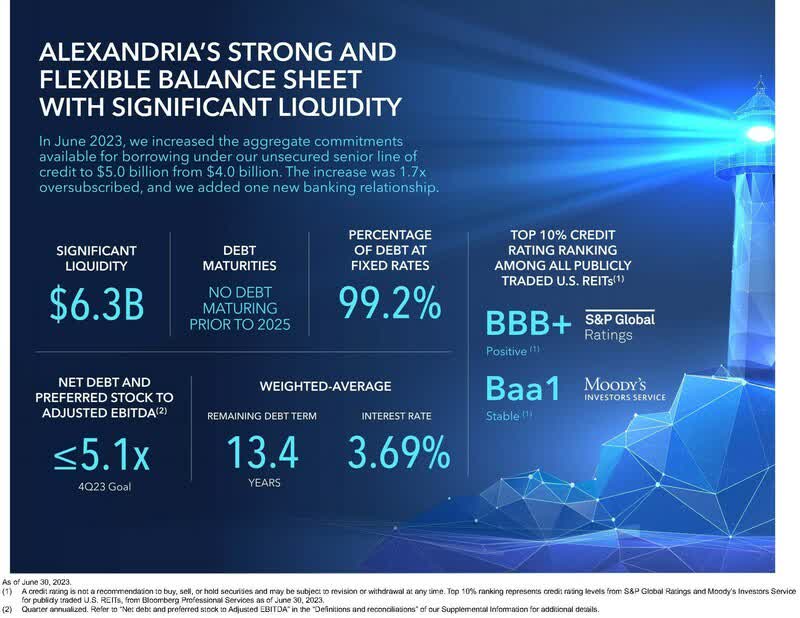

- The REIT's balance sheet and cost of capital, illustrated by its BBB+ credit rating, are among the strongest in the public real estate space.

{kind=link}

ARE Q2 Earnings Report

With a weighted average debt maturity over 13 years, no debt maturing before 2025, and substantially all (>99%) of debt at fixed interest rates, ARE's balance sheet is enviably strong.

Finally, ARE continues to be led by Chairman and co-founder Joel Marcus, who oversees a top-notch management team with a stellar history of generating shareholder value.

Crown Castle ( CCI )

CCI owns and operates one of the most extensive networks of telecommunications infrastructure in the United States, including over 40,000 towers, about 120,000 small cell nodes, and 85,000 route miles of fiber.

CCI Presentation

While demand for and supply of towers might be growing faster in certain developing markets, I like CCI's exclusive focus on the US, for several reasons:

- The US market is extraordinarily stable and safe, and mobile data demand growth should remain strong well into the future.

- CCI has no geopolitical or currency fluctuation risks to think about from presence in foreign markets.

- Zoning regulations and NIMBYism ("not in my backyard") ensure that the supply of cell towers stays stagnant, preventing the normal real estate cycle of overdevelopment and oversupply leading to periods of poor performance.

- CCI is a leader in the small cell space (mini-cell towers used to boost capacity in high traffic areas), wherein its primary competitors are the mobile carriers themselves. CCI can pitch itself as an "infrastructure-as-a-service" provider to lighten the capital load for the carriers, earning a nice spread in the process.

As I explained in my last full article on CCI :

CCI has a uniquely attractive business model that allows it to add multiple "tenants" onto its infrastructure for little to no incremental cost, which pushes up its yields on invested capital over time.

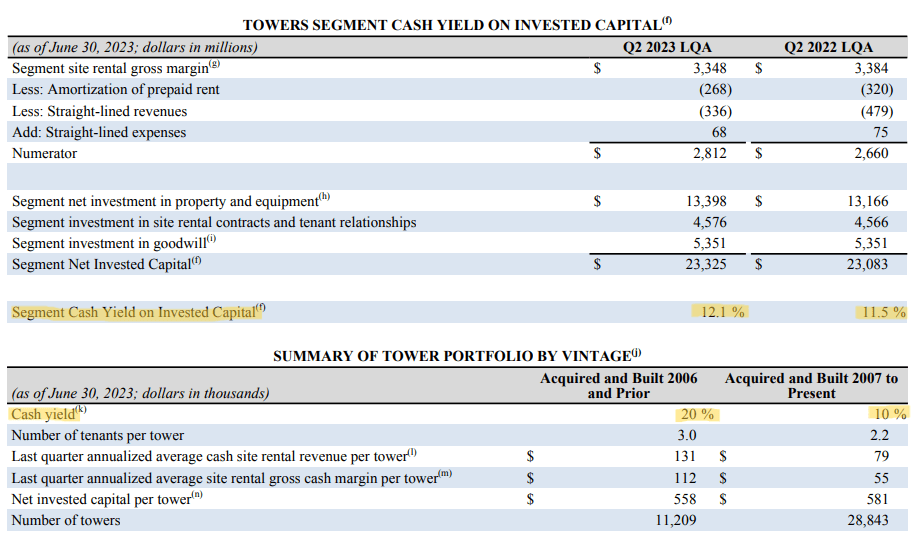

Each tower or small cell has an initial cash yield on invested capital, and that will slowly rise over time as the annual rent escalations take effect. But CCI can also co-locate multiple tenants on the same infrastructure asset for little to no incremental cost, which significantly pushes up its yield on investment.

{kind=link}

CCI Q2 Supplemental

Notice above how CCI's tower segment has grown its cash YOI year-over-year. This is from densifying its towers with multiple tenants. CCI's average number of tenants per tower is currently 2.5, but there's room for that to go up as the four largest carriers (including Dish Mobile ( DISH )) continue to invest in their networks.

With mobile data usage projected to grow at a double-digit pace over the next decade from increased video streaming, ridesharing, mobile gaming, Internet of Things, self-driving cars, etc., I believe CCI's irreplaceable infrastructure portfolio has many years of growth still ahead of it.

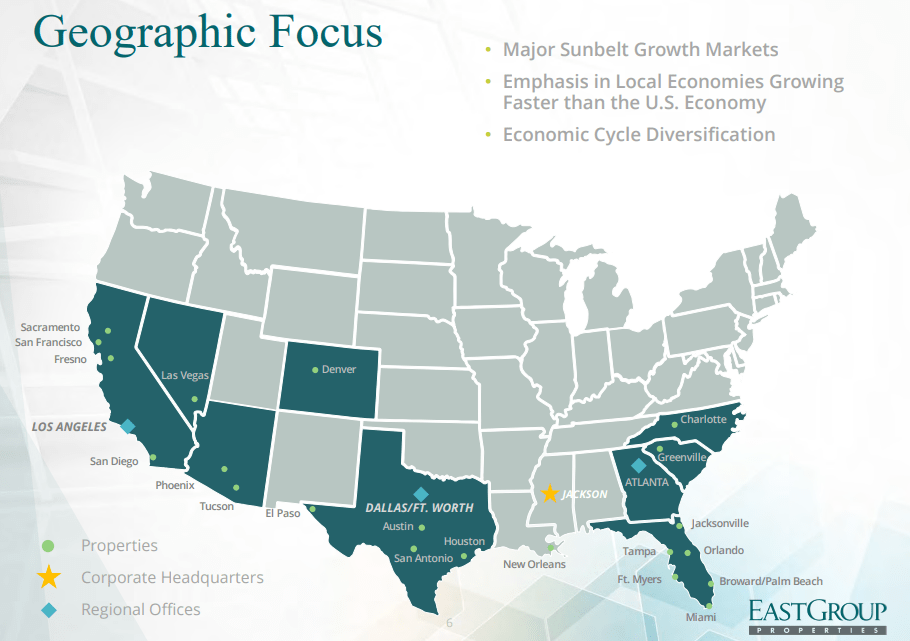

EastGroup Properties ( EGP )

EGP owns and develops multi-tenant, shallow-bay logistics and distribution facilities in multi-building industrial campuses located in infill locations of Sunbelt markets.

EastGroup Properties

What does all that terminology gobbledygook mean? Let's break it down:

- "Shallow-bay" means smaller buildings (15,000-50,000 square feet) best suited for last-mile warehousing and distribution logistics. Two-day and next-day shipping wouldn't be possible without these buildings.

- Industrial campuses/parks are the properties with several relatively small buildings instead of the giant big box distribution facilities typically located outside of population centers.

- "Infill" refers to buildings that "fill in" the limited unused space in a mostly built-out market, as opposed to the big box industrial facilities typically located outside cities where land is more abundant.

- "Sunbelt" refers, of course, to states in the sunny Southern region of the US that enjoy above-average population and job growth.

{kind=link}

EGP July Presentation

EGP boasts great locations in fast-growing cities in Texas, Florida, Georgia, Arizona, and the Carolinas, as well as a strong presence in extremely supply-constrained, low-vacancy California markets. Texas, Arizona, and Southern California also have the added benefit of proximity to Mexico, as recent government policies have spurred a wave of near-shoring to countries like our Southern neighbor.

As I explained in a recent article on EGP ,

EGP's tenants compete for this space based on location , not price, which means that rent growth is generally higher. EGP's properties are mission-critical for tenants, whereas the typical exurban industrial building is more of a commodity product subject to price sensitivity.

In order to fulfill their promises of quick delivery times, e-commerce players and business-to-business companies alike need to have logistical facilities located within the city itself, which is what makes EGP's infill locations so valuable.

Like the other REITs in this list, EGP also enjoys a strong balance sheet and cost of capital. Only 18% of its total capitalization is in the form of debt, with 100% of that being fixed-rate debt. The debt-to-EBITDA ratio sits comfortably at 4.4x, and that should fall further as the company plans to issue more equity than debt for growth investments this year.

Mid-America Apartment Communities ( MAA )

MAA owns and develops a diversified portfolio of apartment complexes across the Sunbelt. Its communities span from downtowns to the suburbs and satellite cities. In terms of amenities and price points, its assets range from high-end luxury (Class A+) to affordable workforce housing (Class B-). And in terms of building types, its portfolio is heavily weighted towards low-rise, garden-style communities with exposure to mid-rise and some high-rise buildings.

{kind=link}

MAA June Presentation

Which will offer superior returns going forward, supply-constrained coastal markets with stagnant or slightly falling populations, or fast-growing Sunbelt markets where supply growth is robust?

I would rather own real estate in growing markets. Yes, developers are building lots of new supply in these markets, but that new supply corresponds to the population and job growth. It isn't the result of a speculative bubble. All signs, including MAA's Q2 2023 results , point to the idea that robust population inflows should easily absorb the oncoming supply being delivered. To quote MAA's CEO Eric Bolton from the Q2 conference call :

While we are working through a higher level of new supply deliveries across our markets for the next few quarters, with the demand trends holding up as they are, we expect to continue to drive top line results that will exceed our long-term historical averages.

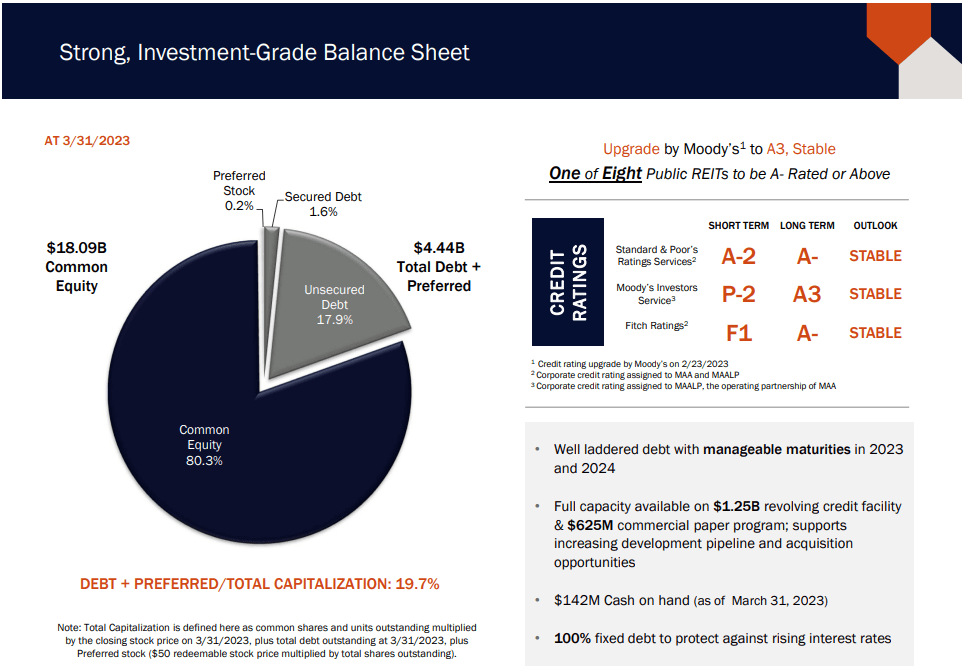

On top of the strong positioning of its apartment assets, MAA enjoys one of the strongest, if not the strongest, balance sheets in its apartment REIT peer group. Its credit ratings of A-/A3 make it part of an elite group of REITs with A-ratings.

{kind=link}

MAA June Presentation

Moreover, 100% of its debt is fixed-rate (no floating-rate exposure) with a weighted average interest rate of 3.4% and weighted average maturity of 7.7 years. Net debt to EBITDA sits at just 3.5x, giving MAA plenty of room to opportunistically use debt-financing for acquisitions in the near future.

The combination of well-located apartment assets, a fortress balance sheet, and skilled, conservative management makes MAA a strong long-term performer.

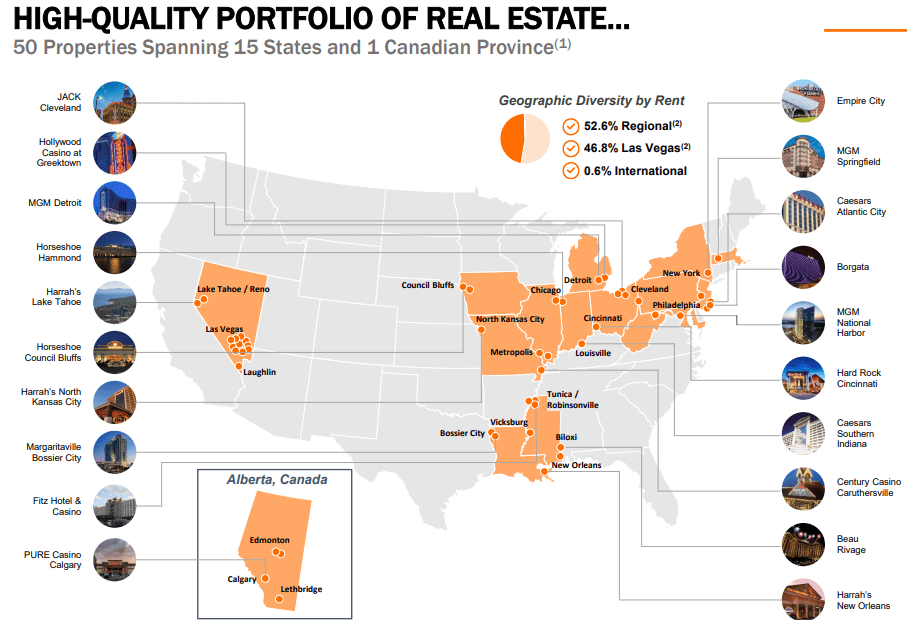

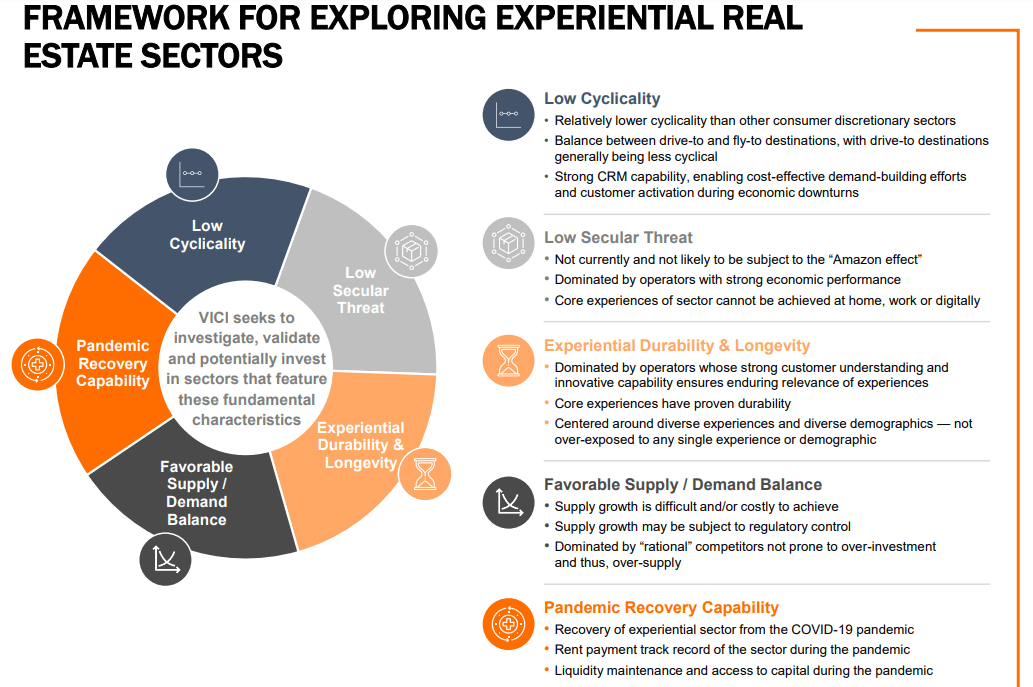

VICI Properties ( VICI )

In the past, I've called VICI the "Landlord of Las Vegas," because it owns many of the most iconic casino resorts on the Las Vegas strip, such as Caesar's Palace and The Venetian.

{kind=link}

Begas Vaby

These are some of the most economically dynamic and profitable properties on the planet. The buildings are built like fortresses, with the tenant-operators contractually obligated to reinvest in them regularly to maintain desirability and functionality.

These truly are trophy pieces of real estate and one-of-a-kind buildings, leased to the nation's leading gaming operators under multi-decade, triple-net leases featuring 1.9% average annual rent escalations.

Aside from gambling, these operators have multiple streams of revenue, such as hotel rooms, restaurants, bars, convention centers, entertainment venues, retail stores, and even gondola rides (at The Venetian). This makes VICI more than just a casino REIT. It is more of an "experiential" REIT.

In addition to its irreplaceable Las Vegas properties, VICI also owns high-quality casino real estate in regional gaming hotspots around the US as well as in Alberta, Canada.

{kind=link}

VICI May Presentation

But VICI is in the process of becoming much more than just the Landlord of Las Vegas. Management is exploring other opportunities in one-of-a-kind, experiential real estate to grow the portfolio.

{kind=link}

VICI May Presentation

For example, VICI recently agreed to provide financing for the expansion of the luxury wellness resort brand, Canyon Ranch. Part of this agreement included rights for VICI to provide mortgage financing and eventually acquire the real estate of future Canyon Ranch locations.

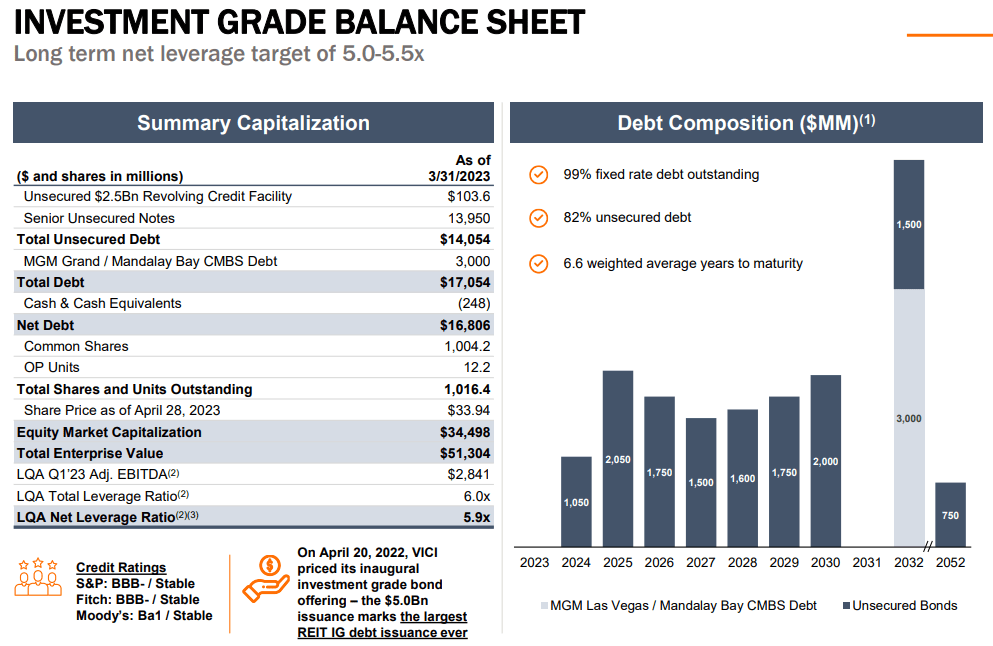

While VICI's 5.9x net debt to EBITDA ratio is higher and BBB- credit rating is lower than the other names in this list...

{kind=link}

VICI May Presentation

...it's important to note that 99% of VICI's debt has fixed interest rates, and only 6.2% of total debt matures prior to 2025. Moreover, VICI aims to reduce its net leverage ratio from 5.9x to the 5-5.5x range, which would put it in line with other blue chip REITs.

W.P. Carey Inc. ( WPC )

Finally, if I could only own seven REITs, the last one would be WPC, a triple-net lease REIT specializing in sale-leasebacks of large industrial facilities in North America and retail stores in Europe.

{kind=link}

WPC Q2 Presentation

WPC targets strong real estate that is highly critical to the operations of its tenants, which are typically just barely sub-investment grade in creditworthiness. This is where WPC sees the best deals.

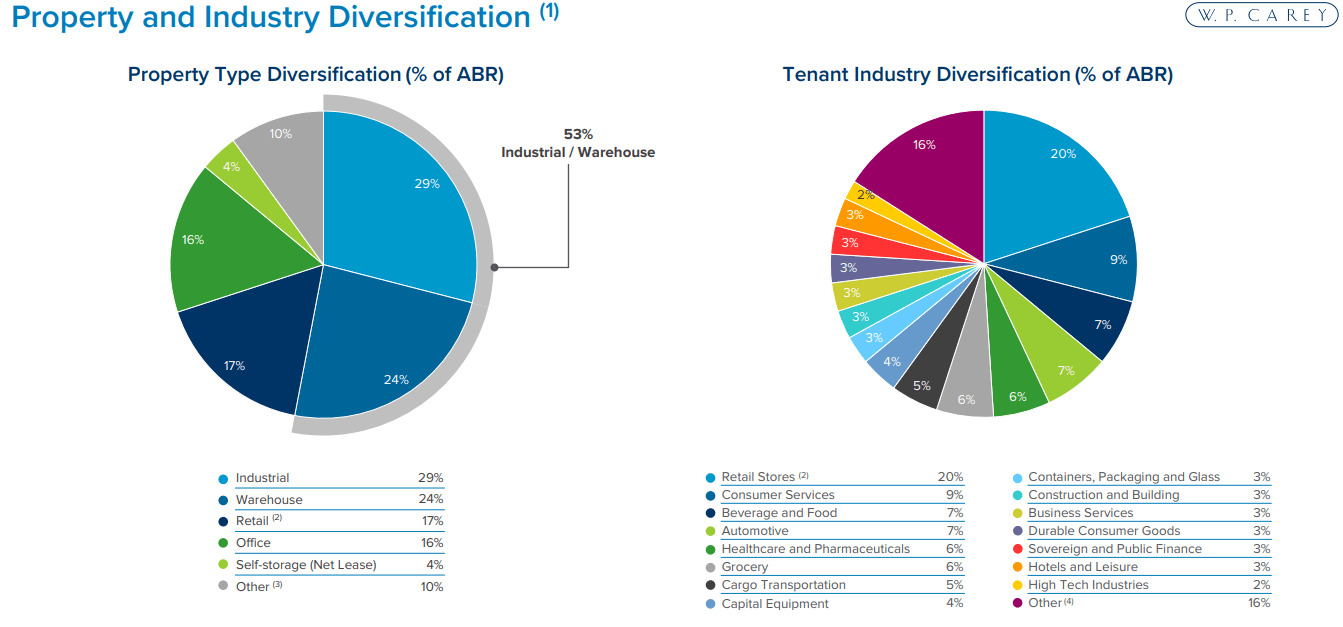

Slightly over half of its portfolio is in industrial/manufacturing or warehouse/distribution properties, with 17% in retail stores and 16% in office. Much of this office exposure is in Europe, where worker utilization of offices is higher than the US.

{kind=link}

WPC Q2 Presentation

As a perk of performing sale-leasebacks, WPC negotiates landlord-friendly lease terms such as multi-decade terms, relatively high annual rent escalations (usually linked to the local country CPI), and master leases. About 99% of leases by rent feature some sort of contractual rent escalation, and over half (54%) features inflation-based bumps.

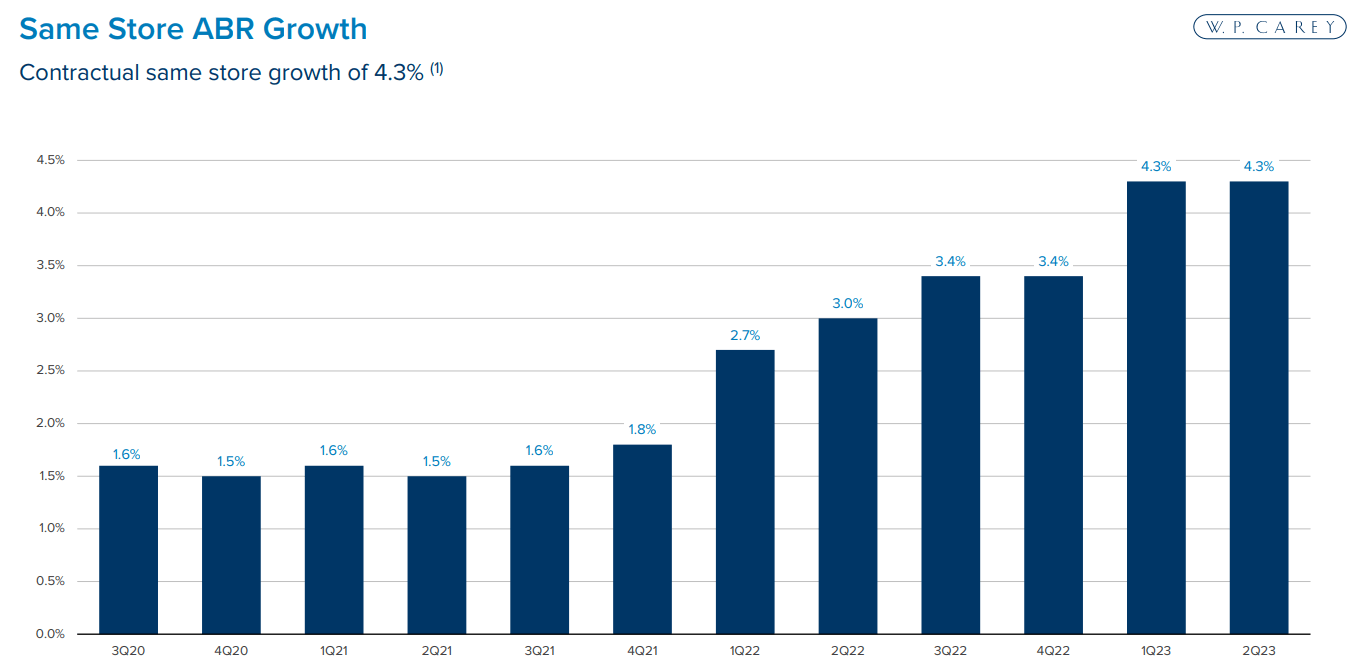

Strikingly, 37% of WPC's rent roll has uncapped CPI-based escalators. That's a big reason why WPC's same-store rent growth has surged from about 1.5% in 2021 to 4.3% in the last two quarters.

{kind=link}

WPC Q2 Presentation

This is an incredible level of organic rent growth for a net lease REIT!

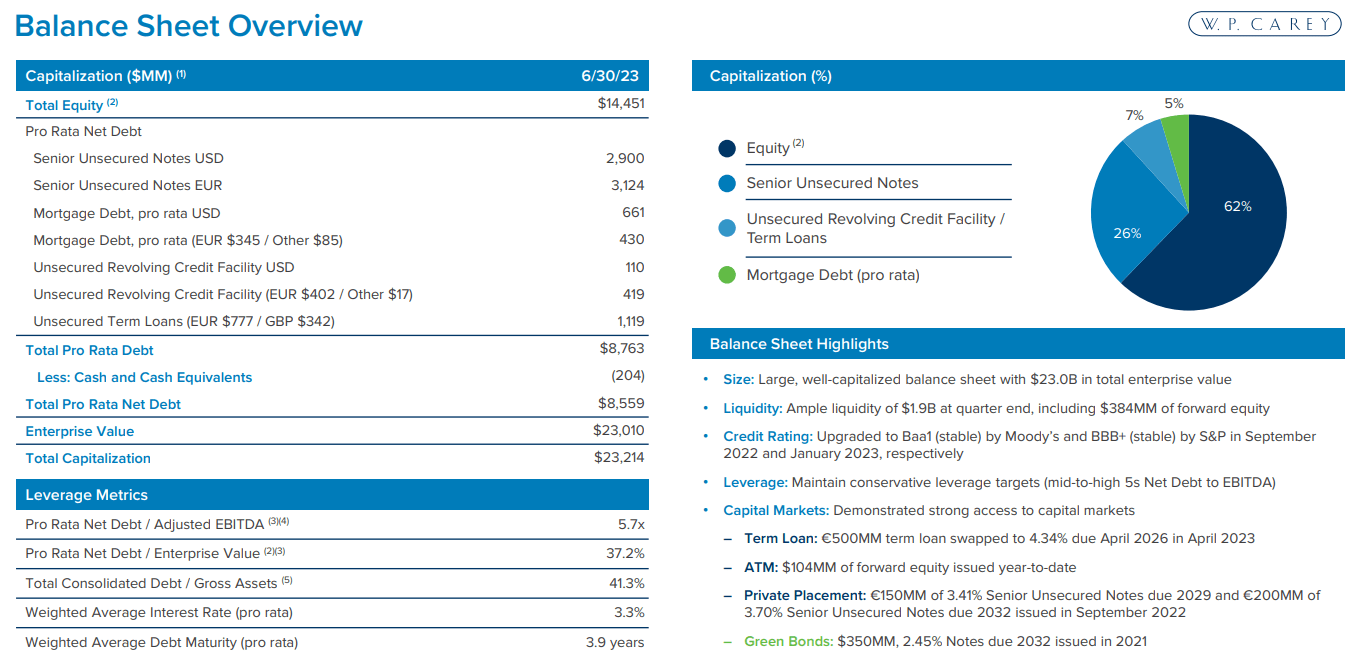

Although WPC does have ~15% of its total debt maturing in 2024 and another 3% maturing in the balance of this year, the REIT's strong BBB+ credit rating should ensure that its borrowing costs don't surge too much.

{kind=link}

WPC Q2 Presentation

At a net debt to EBITDA ratio of 5.7x, WPC's leverage is a bit on the high side, but by no means worrisomely so. This is especially true given its strong organic rent growth.

CEO Jason Fox has done a great job of transforming WPC into a pure-play net lease REIT with a simple story, strong cost of capital, and renewed capacity to grow.

Bottom Line

You'll notice I didn't discuss valuations, dividend yields, or dividend growth track records above. Those are topics for another article, and I've written other articles about almost all of these REITs.

The point of this article was to articulate why these seven REITs are best-in-class businesses with phenomenal real estate, strong balance sheets, and enduring competitive advantages.

While I fully intend on holding all 18 of the REITs I currently own, if I had to only own seven, or if someone asked me which are the seven highest quality REITs that they can look into, it would be these.

For further details see:

If I Could Only Own 7 REITs, It Would Be These