SAFE - If I Had To Name The Biggest Risk For REITs It Would Be This One

2023-10-01 06:48:28 ET

Summary

- REITs have underperformed the S&P 500 due to the Fed's restrictive monetary policy and increased interest rates.

- The market is pricing in a higher for longer scenario, causing concern for REITs with fixed rate financing and upcoming debt maturities.

- REITs with longer debt maturity profiles and locked-in financing at below-market rates are better positioned to withstand higher interest rates.

As many of my followers know, the bulk of my analysis gravitates towards publicly traded U.S. equity REITs. These instruments account for roughly 30% of my portfolio, which is rather significant.

The characteristics of REITs connect well with my bias towards receiving safe and predictable dividends that are subject to a long-term growth component.

However, since the Fed started to apply a restrictive monetary policy by increasing the interest rates, the real estate sector in general has delivered subpar results.

{kind=link}

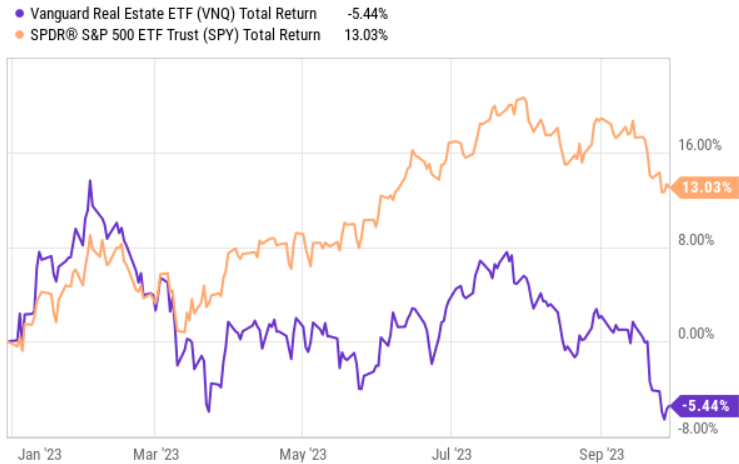

Lately (on a YTD basis), REITs have decreased in value by ~5.5%, while the S&P 500 has gone up by 13%.

{kind=link}

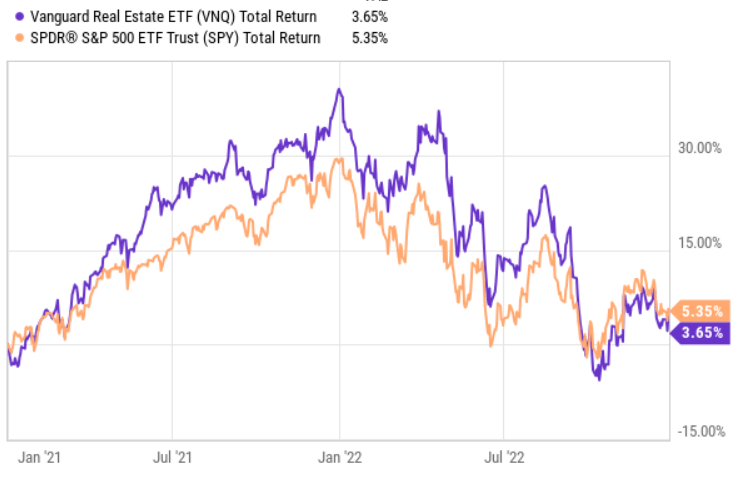

Interestingly, that starting from early 2022 when everybody already knew that the interest rates were going up until mid 2023, REITs have moved more or less in tandem with the S&P 500.

So, what has changed or what is now being priced in by the market that has put a downward pressure on the overall REIT sector?

The answer is an increased probability of higher for longer scenario.

{kind=link}

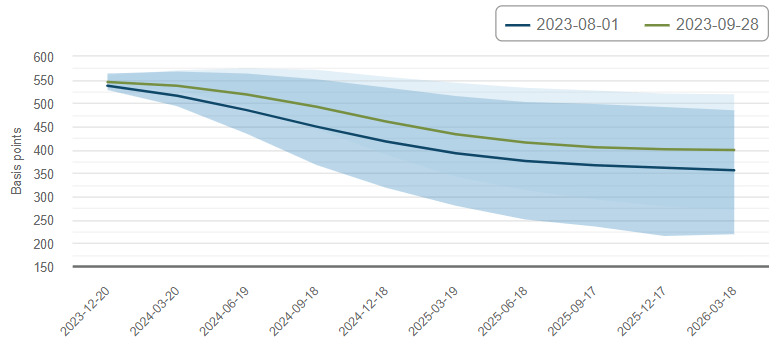

In the past month, the Vanguard Real Estate Index Fund ETF Shares (NYSEARCA: VNQ ), representing most of the U.S. equity REITs universe, has dropped by ~8%. At the same time, as we can see in the chart above, the consensus estimate for the Fed funds rate until early 2026 has increased across the entire curve.

One might wonder why just now the market reacts so negatively to the higher interest rates and why previously there was not so considerable divergence taking place between VNQ and the S&P 500.

Here the explanation lies in the duration of the higher for longer scenario.

Almost all of the U.S. equity REITs have historically relied on fixed rate financing that is locked in for on average 3 - 5 years in the future. What this does is it protects the cash flows from the volatility in the market interest rates.

Hence, the fact that currently or even starting from early 2022 we have much higher interest rates than what has been assumed via financing by REITs previously does not impact the underlying cash flows too much. Similarly, REITs (or their multiples) with fixed rate debt do not in general care about higher interest rates in, say, 1 year from now as long as (a) the interest rates will be lower after 1 year and (b) the refinancing event will take place in the environment when the interest rates have already decreased.

Granted, usually the debt exposure part that is associated with credit revolvers is based on SOFR, which has, in turn, allowed for at least some part of the prevailing interest rates to percolate through the books. But still, the lion's share of total REIT borrowings is still being priced at relatively low interest rates.

{kind=link}

Now, the market is increasingly getting more worried about the duration of the higher interest rates. Elevated interests are being projected to last over longer period of time.

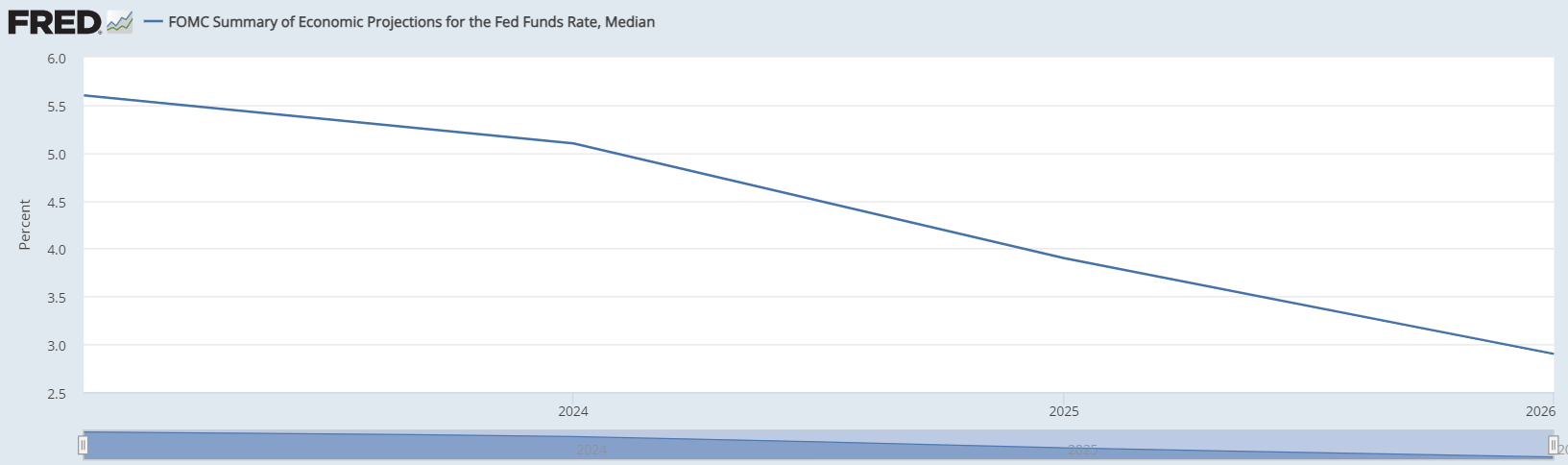

Currently, the market is pricing in Fed funds rate of ~5.1%, 3.9% and 2.9% in 2024, 2025 and 2026, respectively.

If we assume that the market is correct, then many REITs have a problem.

Large scale expensive refinancings

While I am still long REITs, I have selectively avoided and divested REITs with unfavourable debt maturity profiles.

In my opinion, this is the single biggest risk for REITs and I think that many analysts have not taken this into account enough.

Personally, I do not believe that the aforementioned FOMC forecast for the Fed funds rate will hold true. The chart has been wrong since the Fed started to hike in 2022. In fact, the curve has been extended meeting by meeting. There has been a considerable underestimation of the level of future interest rates.

At the same time, I do not believe in other or personal macroeconomic forecasts. Namely, I think it is overly risky to base an investment allocation strategy on the macroeconomic forecasts.

So, in the context of my portfolio, I structure the investments so that the downside is limited in case the negative scenario plays out. The key is long-term returns with extremely limited probability of value-destruction (e.g., massive equity dilution, structurally lower cash flows).

In this case, the negative scenario for REITs, which certainly is not of a low probability, is that the interest rates remain this high for longer period of time than what is currently baked into the cake.

Let me depict the consequences (via back of the envelope calculus) of high interest rates, which are extended over several years in the future.

#1 Realty Income (NYSE: O )

O is one of the safest REITs out there with an upper investment grade credit rating, diversified portfolio and over 25 years of dividend success.

O's current cost of financing embedded in the books is 3.7%.

{kind=link}

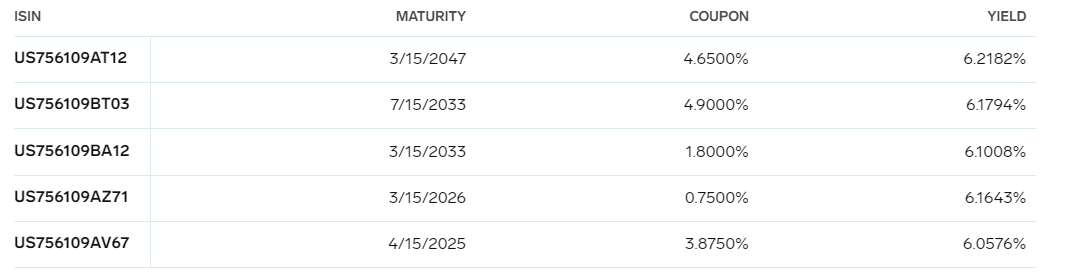

Yet, the market level financing for O is around 6.1% - based on its outstanding bonds.

{kind=link}

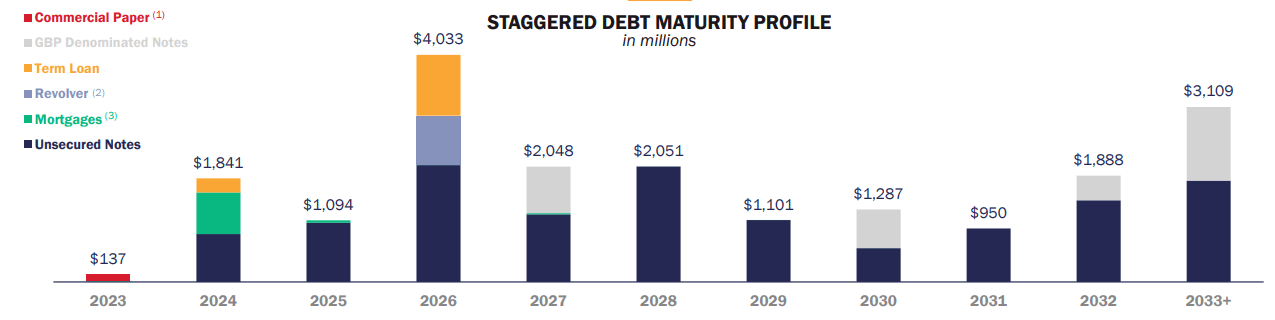

Looking at the existing debt maturity profile, year 2026 is when significant refinancing will have to be conducted.

Let's now plot a scenario in which the interest rates remain elevated until 2026 (included) and on average auxilierate around 5% over this time period.

By 2026, there is circa $6.5 billion of borrowings adjusted for the revolver that O has to rollover. We can be conservative here and reduce this amount by ~ $1 billion provided that O redirects a significant part of its undistributed FFO for the deleveraging. The current FFO payout ratio is around 74% so the remaining amount of internal cash flows is not that considerable, especially given the need of maintenance CapEx and further dividend increases to keep the "Dividend king" story alive.

So, if O had to reprice ~ $5.5 billion of its debt to 5% by 2026, it would imply additional ~ $165 million of interest cost, which destroys ~ 24% of the undistributed FFO. This is a significant amount, which consumes a part of the O's growth potential.

However, if we took the entire chunk of O's existing debt and aligned it to the market level interest rate (or 6.1% as per current YTM), the rate of change in the underlying interest cost would land at ~64% (or incremental $375 million interest costs). In such case, the FFO payout would increase to just below 90%, which inherently introduces more financial risk and impairs the growth prospects, thereby making lower valuations justified.

As we can see, there is a huge risk exposure to the higher for longer scenario, even for one of the (commonly deemed) safest REITs with A rated balance sheet.

#2 Medical Properties Trust (NYSE: MPW )

Let's now take a more extreme example.

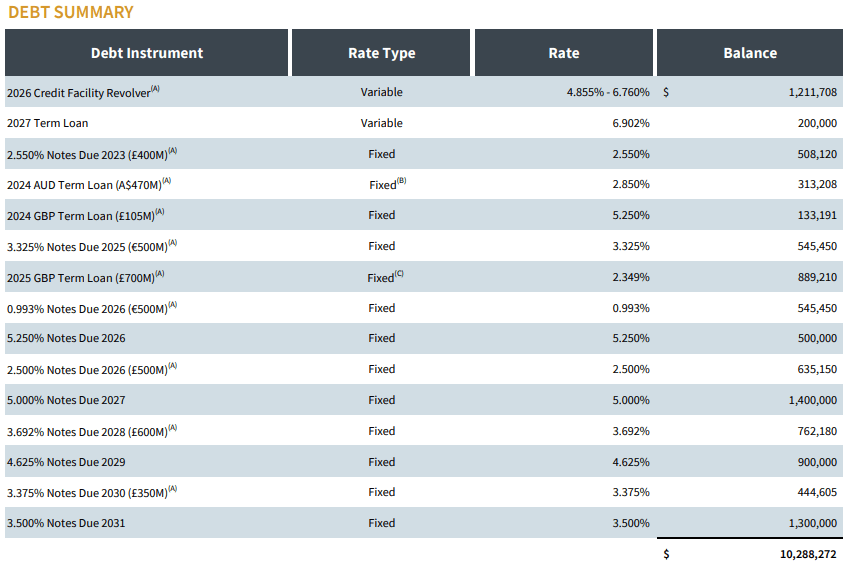

MPW's outstanding bond YTM trades at 14.4% , while the weighted average cost of financing in the Company's books is 3.9%. A huge gap, which is mostly explained by a huge credit risk premium on top of the increased SOFR.

{kind=link}

By year 2026 there is roughly $3.9 billion (excluding variable debt, which already reflects higher interest costs) of fixed rate debt that has to be refinanced.

In MPW's situation we can make no additional assumption pertaining to the retained FFO proceeds since the payout ratio is already fully exhausted. What we can do is we can quickly adjust for the ~$300 million of cash and some property sales (most notably the communicated sale of Australian portfolio), which together provide roughly $1.3 billion.

Again, we are generous here.

Yet, even with that, the interest rate item would inflate by additional ~ $280 million (or by 73% in relative terms based on TTM net interest expense), destroying about one third of the TTM FFO figure (excluding the effects of property sales).

#3 Two REIT examples with extremely long debt maturity profiles

My preference is to stick to REITs, which have well-laddered debt maturity profiles with a weighted average maturity of close to 10 years. This, in my opinion, gives REITs a sufficient time to accumulate internal cash flows and adjust the capital allocation strategy to optimize the balance sheet.

Most importantly, it should be a combination of locked in cost of financing, which is below the market level and a long maturity term.

It does not have to be necessarily 10 years, but sufficient to avoid unfavourable repricing of debt at a large scale during high interest rate environment.

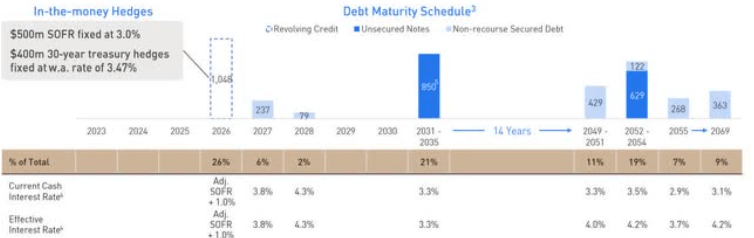

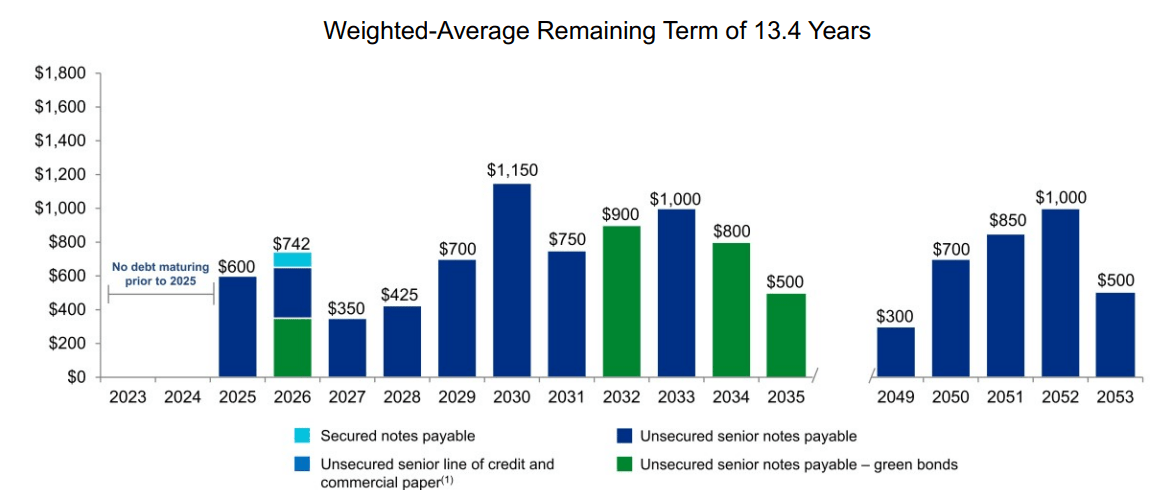

For example, Safehold (NYSE: SAFE ) has a weighted average debt maturity of close to 23 years with an average pricing of 3.6%.

{kind=link}

Alexandria Real Estate (NYSE: ARE ), which is one of the widely recognized office REITs has also structured its debt very well. It has about 13 years of the weighted average remaining term for its existing debt.

{kind=link}

The bottom line

In my opinion, the recent drop in REIT valuations is justified. It seems that the higher for longer scenario will last for a longer period of time, which will at some point trigger expensive refinancings.

Many REITs will experience notable debt maturities within 3 years causing the relevant cost of financing to double. In cases of elevated credit risk or some other idiosyncratic aspects, the new cost of financing is even higher.

As a result, interest expense items will balloon and destroy considerable portions of the existing FFO results. For some REITs it will imply weaker growth prospects due to reduced amount of capital that can be deployed for incremental cash generation. But for some it might require additional equity issuances.

In any case, if the interest rates remain this high for several years ahead (or worst go even higher), REIT investors have to be ready to experience negative alpha returns.

To decrease the gap of underperformance under a higher for longer scenario and mitigate the risk of unfavourable equity dilution, having a very long weighted average debt maturity term is critical.

For further details see:

If I Had To Name The Biggest Risk For REITs It Would Be This One