SACH - If You Build It They Will Come

Summary

- I’m focusing on a niche sector in REIT-dom: housing finance.

- These REITs aren’t landlords, they’re specialty finance companies that provide capital to developers.

- These specialty REITs are yielding from 11.3% to 14.6%, and given the fact that the yields are elevated, so are the risks.

Don’t worry, the title to my article today is not click bait, it came from the 1989 movie, “Field of Dreams,” and the phrase was actually, “if you build it, he will come.”

If you saw the movie, it was about a farmer following his dream and building a baseball-playing field in his cornfield.

The construction of the baseball field would mean that he would need to sacrifice some of his corn yields; however, a voice came to him at night and said that quote.

After that point, he decided to put his fears aside and start building the baseball diamond, even though many people around him believed it was ridiculous and wasn’t going to work.

Now, I’m not going to write about the farming sector today, although I do own shares in Farmland Partners Inc. ( FPI ) and Gladstone Land Corporation ( LAND ).

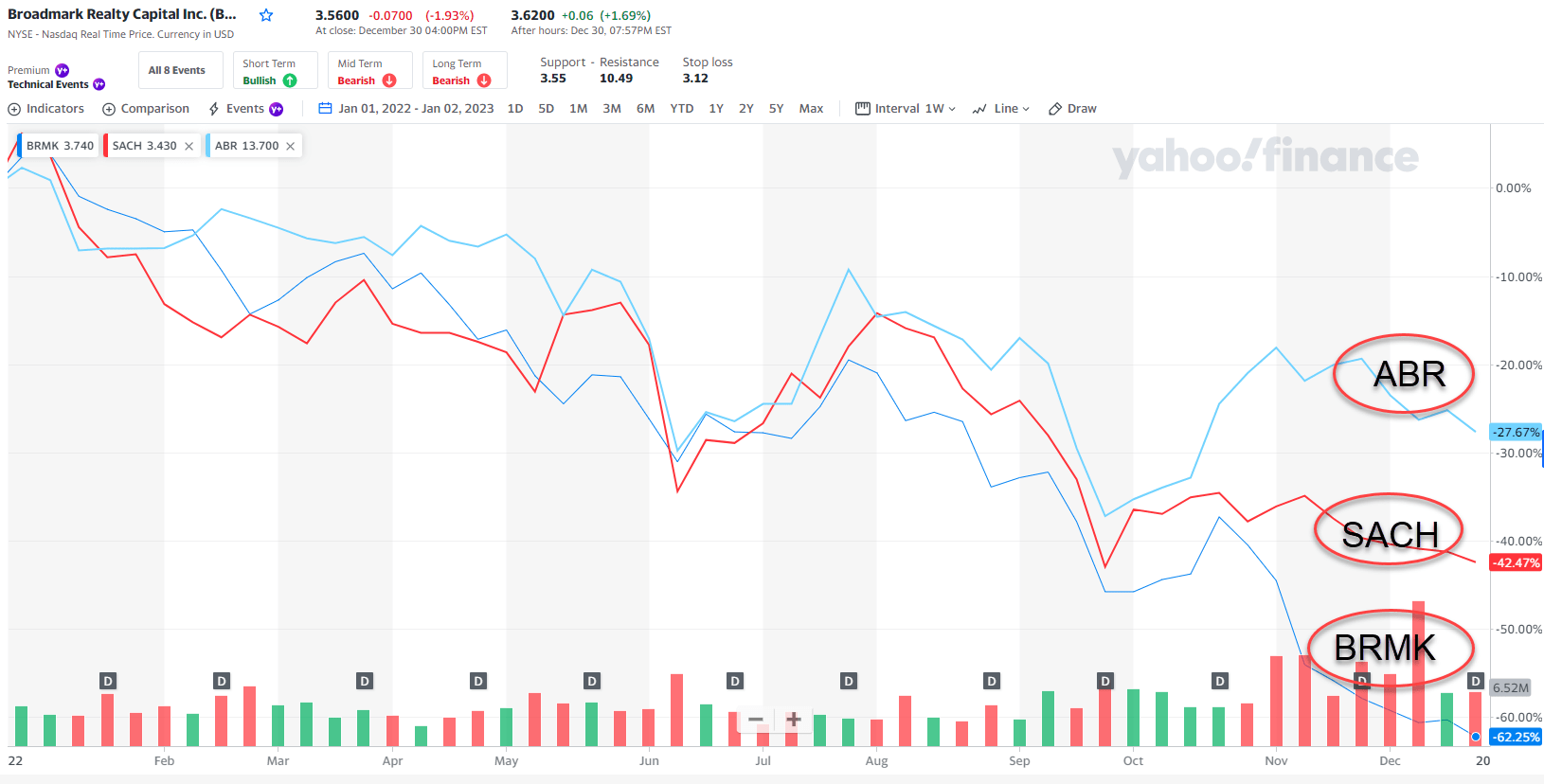

Instead, I’m focusing on a niche sector in REIT-dom: housing finance, a sub-sector within the commercial mREIT sector that has been crushed:

{kind=link}

As you can see, these three mREITs have been punished in 2022, and all three of them are focused on the residential sector, which is good reason for the underperformance.

However, these real estate investment trusts ("REITs") aren’t landlords, they’re specialty finance companies that provide capital to developers. And, as you know, the times when things look the worse are sometimes the best times to own…

Broadmark Realty Capital Inc. ( BRMK ): Yields 11.4%

Broadmark is a specialty real estate finance company investing in opportunities throughout the small to middle market. The company provides solutions across the entire debt capital stack, including senior fixed and floating rate loans, construction loans, bridge loans, as well as mezzanine and participating-preferred structures.

BRMK typically invests capital in the range of $5-$75M per transaction with investment terms in the range of 12 to 36 months. BRMK charges interest from 8% to 12% with fees ranging from 1% to 4%, which translates into annual gross yields of 9% to 16%. As you can see below, BRMK invests in residential (35%), multi-family (21%), and others:

BRMK Investor Presentation

The active loan portfolio includes 224 loans across 20 states plus the DC and targets states with favorable demographic trends and lending laws. This diverse borrower base and 46% repeat business provides the company with a highly level of predictability.

BRMK is well-positioned for rising rates, with current liquidity of $196 million and a conservative debt-to-equity ratio of 8.8% that support ongoing growth. Current pricing is expected to benefit when index-based competitors must raise prices in response to escalating interest rates and market uncertainties.

{kind=link}

BRMK recently cut its dividend by 50% back in November 2022, from $.70 to $.35 per share. We telegraphed this to members at iREIT on Alpha in advance, as we knew that the dividend wasn’t safe given the elevated payout ratio.

In addition, iREIT on Alpha has been monitoring defaults closely, with 41 loans in contractual default in Q3-22 ($286. Million). The weighted average loan to value of approximately 87.2% for loans in default, as a result of cost-overruns and collectible receivables.

BRMK Investor Presentation

During Q3-22 BRMK foreclosed on one small loan and received payoffs on six loans in contractual default status, representing $18 million in total commitment. At the end of the quarter BRMK owned 11 foreclosed properties with $93.5 million in carrying value.

BRMK’ CECL reserve was up in Q3 primarily due to a specific $9.1 million loan loss reserve associated with a loan collateralized by a hotel in Colorado with a borrower in bankruptcy. BRMK’s portfolio is less than 5% hotels and weighted towards single and multi-family collateral with substantially lower LTVs, and BRMK said,

“we do not believe this troubled loan is representative of our broader portfolio.”

BRMK also noted “ a 13% increase in aggregate CECL general reserve based on consideration of current macroeconomic factors .”

As a result of loans and non-accrual status and foreclosed properties BRMK saw a drag on earnings of approximately $0.05 per diluted common share for Q3-22.

BRMK has also seen a shakeup in leadership, as the company announced in November that Jeffrey Pyatt (previously CEO) assumed the role of interim CEO and Kevin Luebbers, a Director and Chair of the Audit Committee, was named Interim President.

The board is in the process of launching a search for a new CEO. Additionally, BRMK hired Jonathan Hermes as the Chief Financial Officer effective December 1, 2022.

Valuation

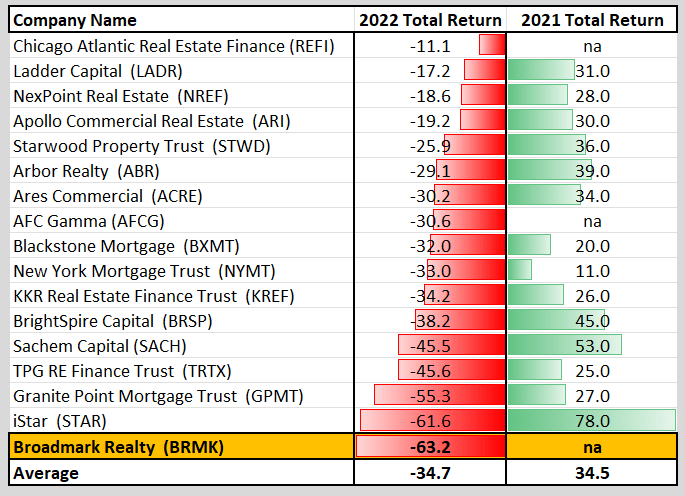

As you can see below, BRMK was the worst-performing mREIT in 2022:

{kind=link}

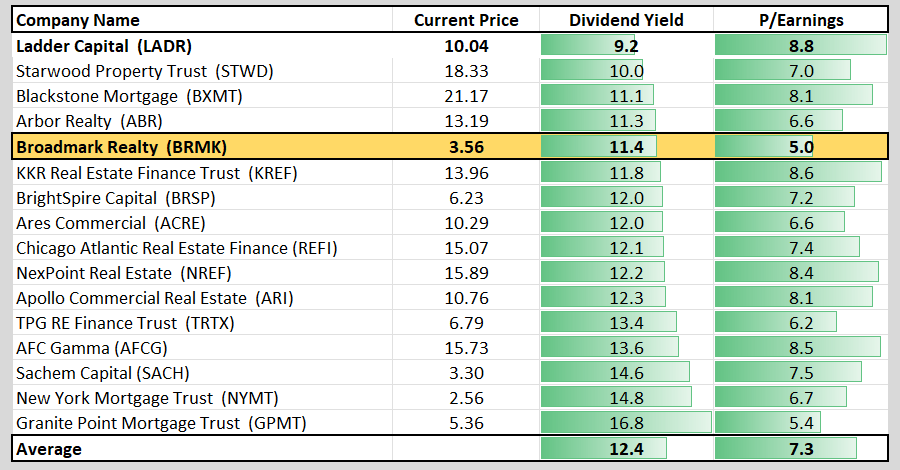

Even with a 50% dividend cut, shares are yielding 11.4%, with a P/E multiple of 5.0x (the lowest in the peer group).

{kind=link}

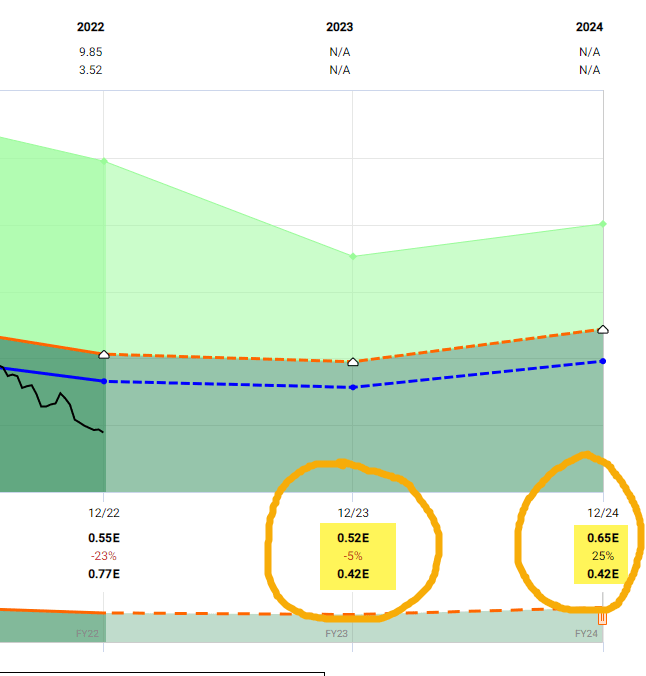

As you can see below, analysts are forecasting BRMK to grow by -5% in 2023 and +25% in 2024. These are simply consensus numbers, but based on this data point, the dividend appears to be safe – assuming defaults rates don’t escalate.

{kind=link}

Now that the dividend has been cut, we’re upgrading from a SELL to a HOLD and we will be reaching out to management for an interview. For the opportunistic investor, it may not be a bad time to cast a line (or nibble on some shares in BRMK). The valuation is extremely attractive, but expect a few more innings of choppy water.

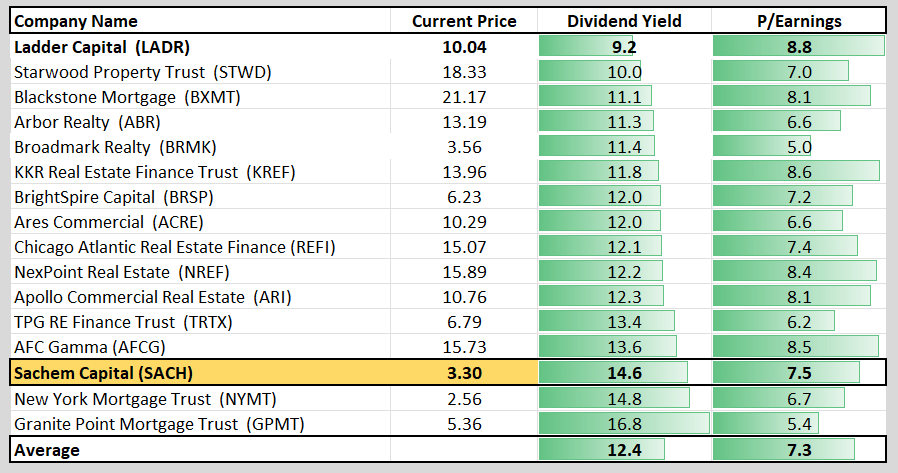

Sachem Capital Corp. ( SACH ): Yields 14.6%

Sachem Capital is a Mortgage REIT that went public in 2017. The company specializes in originating, investing, underwriting, funding, servicing, and managing a portfolio of short-term, high-yielding real estate loans, historically targeting the “fix-and-flip” market and real estate developers.

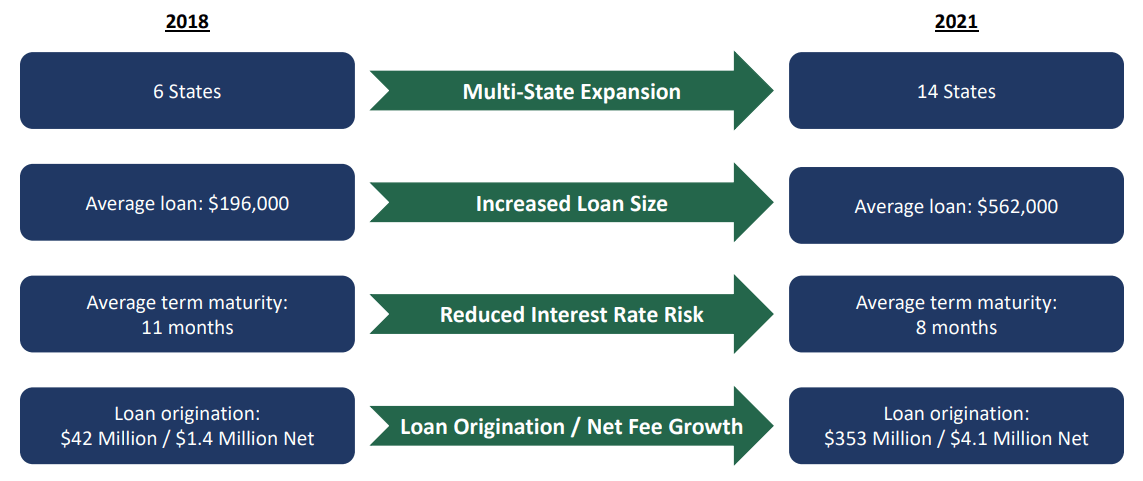

Originally founded in 2009 as a private partnership, SACH grew to 175 partners and approximately $30 million in partners’ capital up to the IPO in 2017. SACH’s loan portfolio has grown to $448.5 million as of Q3-22 from $33.8M at year-end 2016.

{kind=link}

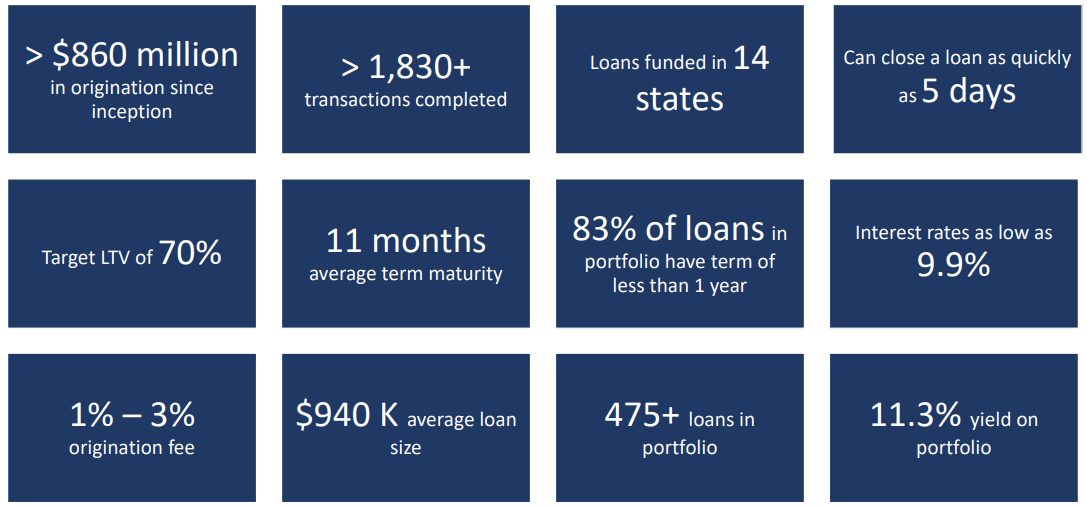

When originating a loan, SACH focuses on the collateral value more so than the property’s projected cash flow or the borrower’s credit, which enables them to close a loan in as quickly as 5 days. Their competitors typically take 3-6 months.

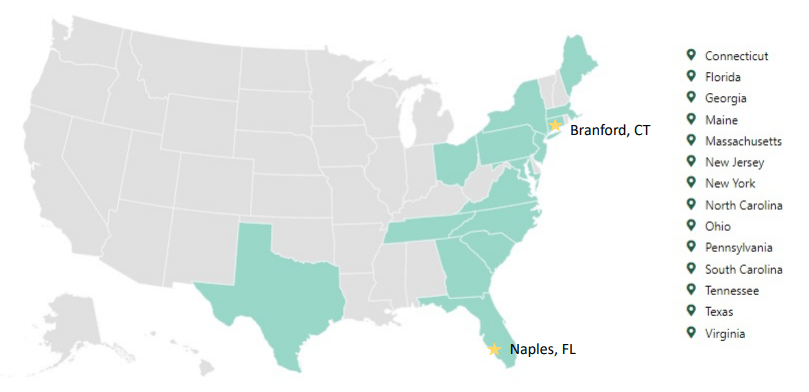

Sachem takes a conservative underwriting approach, as all their loans are secured by first lien mortgages with a target 70% Loan-to-Value ratio. SACH has a strong core Eastern Seaboard presence complemented by local lending capability, as viewed below:

{kind=link}

SACH has shifted to commercial real estate loans that provide a hedge on the residential market given its more typical reliance on cash flow and CAP rate calculations by borrowers/investor. Interest rates and loan-to-value ratios are consistent with historical targets.

SACH’s investment model is comparable to BRMK, as SACH seeks interest rates as low as 9.9% with origination fees of 1% to 3%. The average portfolio yield as of Q3-22 was 11.3% (as shown below):

{kind=link}

I recently interviewed Bill Haydon, the CIO and COO of SACH, and he explained,

“we basically overhauled our underwriting about a year and a quarter ago, really last summer, summer of 2021. And we felt at the end of 2021 that rates were going to go stratospheric in 2022 and we hedged around that.”

He added,

“The organic default rate or the incidents of a loan going sort of sideways and having some dysfunction has been fairly stable. What's increased the default rate in Q3 is our option to elect not to renew loans that don't currently meet the guidelines.”

He continued,

“So non-payment of insurance, non-payment of taxes, non-payment of the payment, any breach of a covenant. If we discover that they're, the developers living in one of the properties, that's a breach. It could be a myriad of anything, but it's not just payment, it's other default options.

Interestingly around that is that in many cases, it's paid in acceptable order, but there's some other factor that creates a breach like the insurance lapsed and we enforced place insurance. So then we take the option to not renew them, it becomes a default.”

As seen below, SACH had 16 loans in foreclosure in Q3-22 compared with a total of 520 active loans in the portfolio, a much lower number than BRMK.

SACH Investor Presentation

So why did SACH cut the dividend by 7% in October 2022 (from $.14 per share to $.13 per share)?

Once again, SACH’s CIO responded as follows,

“So we've always had a 12 cent to quarter dividend for a long time and every now and then, we true it up at the end of the year with a special dividend. We decided to do a special dividend and do the 14 cents.

And we do have an internal sort of ethic or desire to maintain or increase the dividend, kind of like your dividend aristocrats, right? If you can increase your dividend over time, then your price relative yield is very nice for long term holders.

So we reduced to 13, which is still over the 12, and what happened was we sort of, I wouldn't say we learned, but we did get some perspective that sometimes shareholders are like, hey, what have you done for me lately? We were like, hey, we've been giving you 12 for years.

And then we took it up to 14 and then we want to keep the dividend increase. We took it down to 13 and everyone was like, you had a reduction. We're like, wait, it's, we increased to 14, then took it to 13, but we've always been 12, so we're still increasing the dividend.”

Lesson learned: Don’t cut the dividend.

Valuation

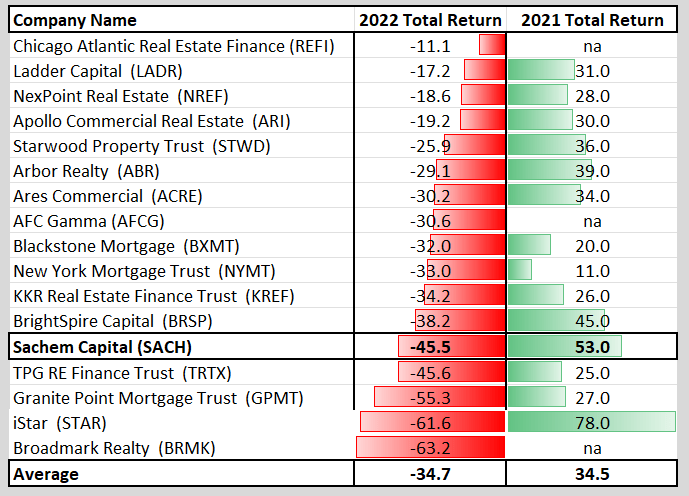

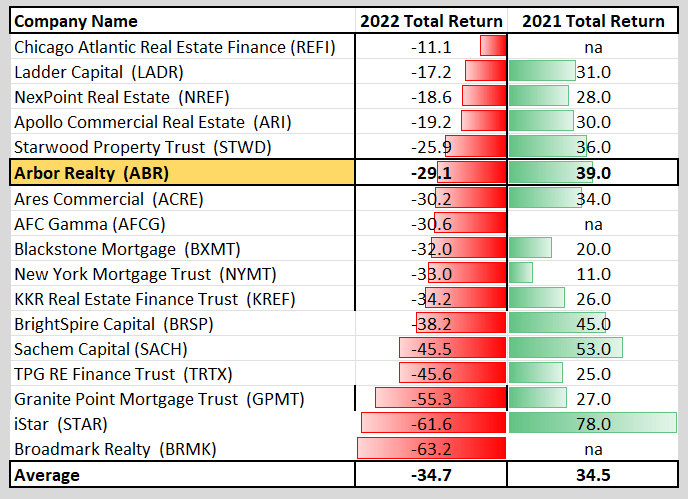

As you can see below, SACH returned 53% in 2021 and -45% in 2022:

{kind=link}

And with a 7% dividend cut, shares are now trading at 14.6% with a P/E multiple of 7.5x (BRMK trades at 7.3x).

{kind=link}

Now, in addition to lower defaults (than BRMK), SACH has another trick up its sleeve, and that’s the forward looking consensus model. As seen below, SACH is forecasted to grow EPS by 20% in 2023 (as opposed to -5% for BRMK). That tells me that SACH has the potential to boost its dividend by a healthy margin this year.

FAST Graphs

Although the dividend cut was unexpected (and unfortunate), it does look as though SACH has the potential to deliver the goods…and, of course, we’ll be speaking with management again soon. We believe this one could repeat 2021 performance and deliver 35% annualized returns…

One more plus, insiders own 5% of the shares outstanding.

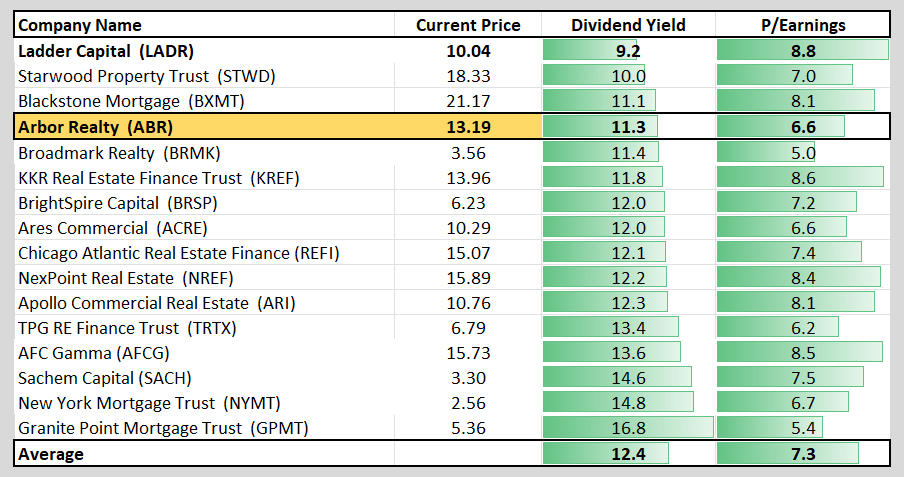

Arbor Realty Trust, Inc. ( ABR ): Yields 11.3%

Arbor Realty is different from the previously discussed mREITs, and we consider the company one of the most comprehensive lending platforms that specializes in customized financing and is most active in the multifamily sector.

Like the others, ABR is internally managed, and the company executes a highly flexible multifamily focused lending platform focusing on:

- Balance sheet loan origination – strong risk-adjusted returns; drives GSE/Agency/APL pipelines

- GSE/Agency & Private Label loan origination – capital light; significant earnings and cash flows with a high barrier to entry

- Servicing – ~$27B portfolio; generates significant prepayment protected annual income stream of ~$115M with 9-year w/a remaining life

- SFR – Proprietary single-family rental portfolio platform providing bridge, permanent and build-to-rent lending products, which also drives GSE/Agency/APL pipelines

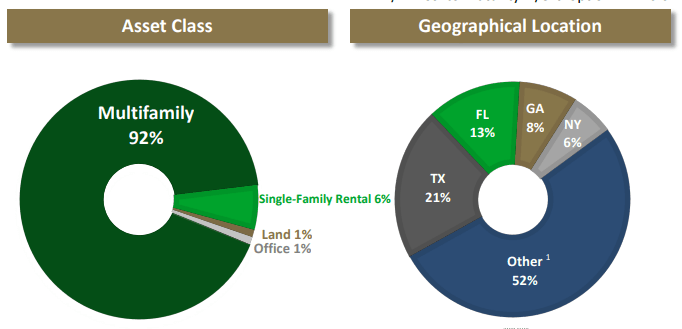

This mREIT primarily focuses on the multifamily asset class as the portfolio contains ~$8 billion in non-recourse, non-mark to market CLO (collateralized loan obligation) debt. Most of the loans (98%) are senior secured bridge loans, and the average loan size is $20.2 Million with an average loan to value of 76%.

{kind=link}

Importantly, interest rate increases tilt economics toward apartments and away from single-family homes (it hurts both, but individual buyers using 90% leverage are more sensitive to it). This is where ABR is a big beneficiary.

Much of Arbor’s business looks and pays like an annuity as it builds income streams from its lending activity. The REIT has generated distributable earnings of $0.56 per share in Q3 2022, which is $0.16 in excess of the current dividend, representing a payout ratio of 71%.

ABR has 10 straight years of dividend growth; 10 consecutive quarters, a 33% increase, with the lowest payout ratio in the industry – annualized dividend of $1.60.

ABR’s total debt on core assets in Q3-33 was approximately $13.9 billion, with all in debt costs of approximately 5.33%, which is up from a debt cost of around 4% at Q2-22. The overall net interest spreads in core assets decreased slightly to 2.08% compared to 2.16%.

Around 97% of balance sheet loan book is floating rate, while 88% of ABR’s debt contains variable rates, further enhancing the positive effect that interest income spreads as rates increase. All things remaining equal, a 1% increase in rates would produce approximately $0.10 a share and additional annual earnings.

Valuation

As viewed below, Arbor Realty yields 11.3% with a P/E multiple of 6.6x (BRMK yields 11.4% and SACH yields 14.6%).

{kind=link}

As mentioned, ABR’s dividend is much safer than the others, as the company has frequently increased it and the payout ratio is just 71%. ABR has returned -29% in 2022 versus +39% in 2021:

{kind=link}

As seen below, analysts are forecasting negative growth of -12% in 2023 and -3.5% in 2024. However, there’s ample cushion for the dividend:

FAST Graphs

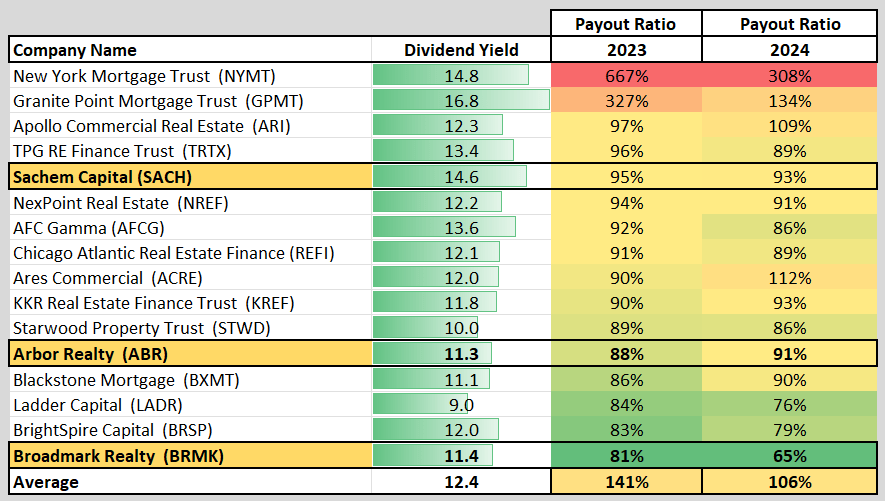

We put together an mREIT dividend safety chart (below) that illustrates the future payout ratios for these mREITs, using the analyst consensus data for 2023 and 2024. As you can see, BRMK screens the safest using this data set:

{kind=link}

We maintain a BUY on ABR, although we consider this an income play. Also, insiders own 12% of the shares outstanding

In Conclusion

All three of the above-referenced specialty REITs are yielding from 11.3% to 14.6% and given the fact that the yields are elevated, so are the risks. Remember that mortgage REITs do not generate the same predictable income as equity REITs, so the dividends can become more volatile.

We believe that the economic backdrop for housing is strong, based on the combination of aged housing stock, declining inventory, continued strong household creation, and consistent housing starts.

SACH Investor Presentation

However, the key to success (in this sub-sector) is to manage default risk, because that’s directly correlated to rising earnings and dividends. Perhaps I should have titled the article,

If You Loan It, You Could Own It

As always, thank you for reading and happy new year!

For further details see:

If You Build It, They Will Come