VICI - If You Like BlackRock You'll Love These 2 High-Yielding Stocks

2024-01-14 07:40:00 ET

Summary

- BlackRock is the most dominant asset manager on the planet, again surpassing $10 trillion in assets under management in Q4 2023.

- Since I upgraded BlackRock to a strong buy last October, its shares have doubled the S&P.

- Despite a slight premium valuation, BlackRock could still be positioned to generate 170%+ cumulative total returns over the coming 10 years.

- A blue-chip MLP and a blue-chip REIT yield an average of 7.2%, boast an average 10.7% annual growth consensus, and could be 13% undervalued.

- Together, the duo could deliver 500%+ cumulative total returns in the next 10 years.

To argue that the S&P 500 ( SP500 ) has sharply rallied since its dip last October would be an understatement. Since that time, the index has gained approximately 15%.

There has been perhaps no bigger beneficiary of this rally and the overall rally in 2023 than asset managers. As has been the case for many years now, BlackRock ( BLK ) has been the undisputed king of the asset management industry. Overall, this is an exceptional business. An overview of the fundamentals can confirm this to be true.

{kind=link}

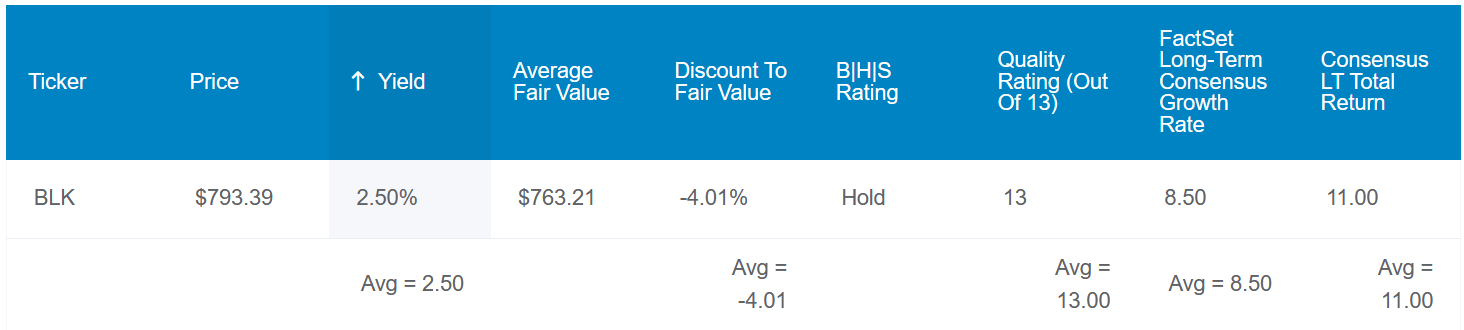

BlackRock's 2.5% dividend yield is reasonably higher than the 1.5% yield of the S&P. The company's payout also appears to be quite safe moving forward.

At first glance, that may seem like a contradictory statement. After all, BlackRock's 57% EPS payout ratio clocked in above the 50% EPS payout ratio that rating agencies prefer from the asset management industry. But the only reason this payout ratio was elevated beyond the rating agency guideline is because BlackRock's earnings in 2023 were still down from their peak set in 2021.

As earnings recover further in 2024 and are expected to surpass 2021 levels in 2025 per FAST Graphs' analyst estimates, the payout ratio should come back down to safer levels.

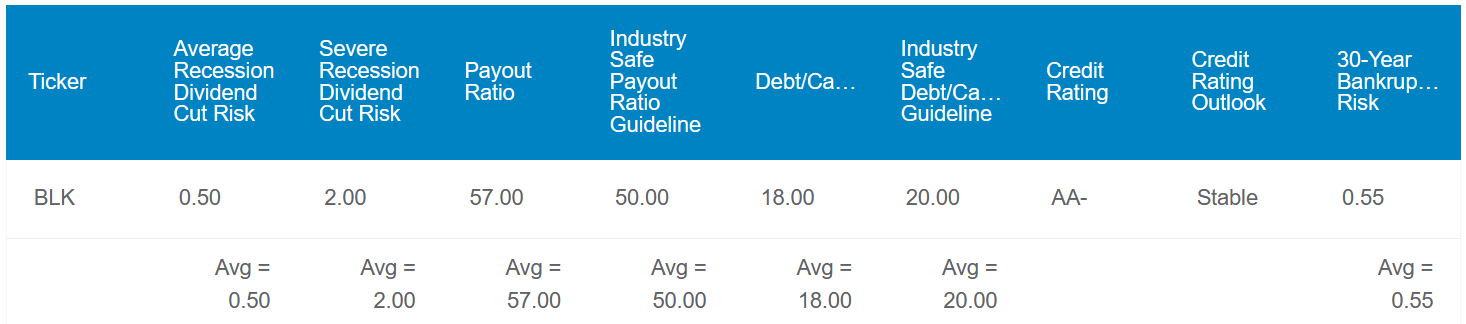

BlackRock's 18% debt-to-capital ratio registers just below the 20% that rating agencies like to see from the asset management industry. Thus, the company enjoys an AA- credit rating from S&P on a stable outlook. That implies the risk of BlackRock closing its doors in the next 30 years is just 0.55%.

What's more, the estimated probability of the company cutting its dividend in the next average recession is only 0.5%. Even if a severe recession were on the horizon, that risk would still be just 2%.

{kind=link}

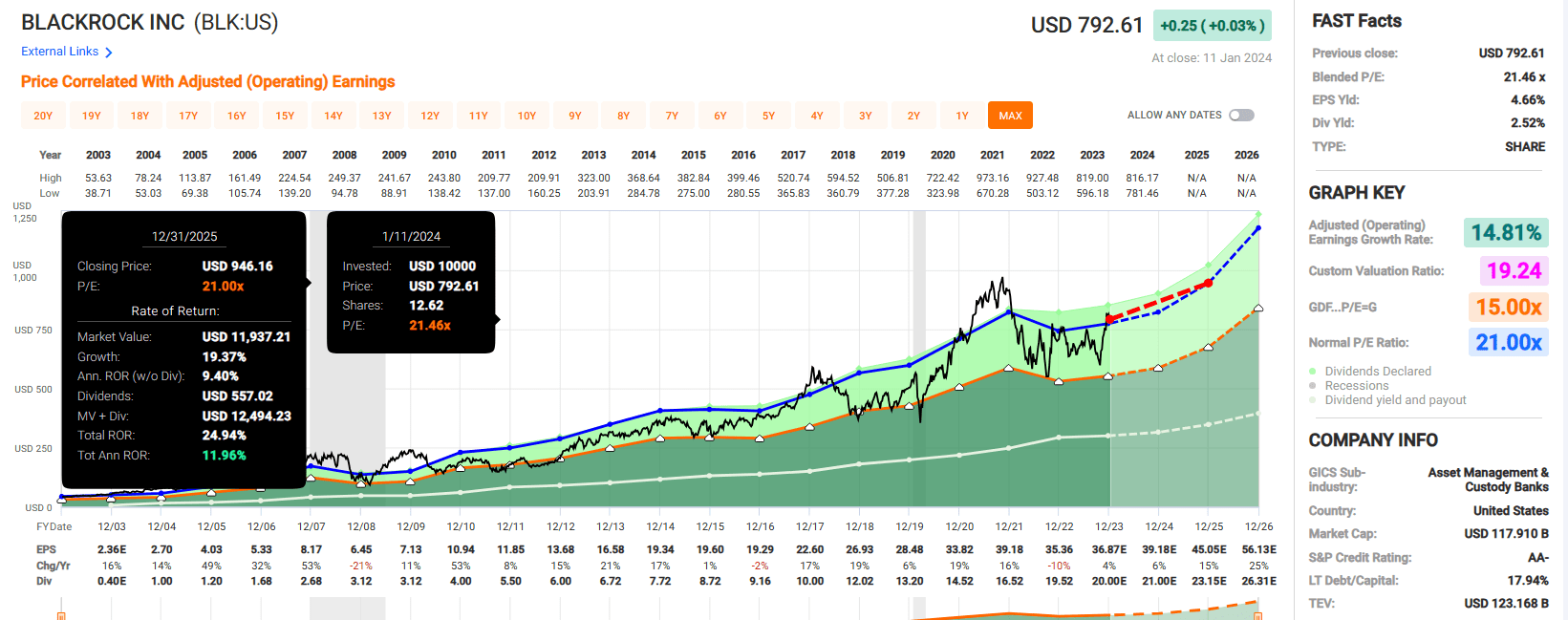

Unsurprisingly, the market rally appears to have overextended shares of BlackRock. Since my previous article in late October , shares have soared by over 30%, doubling the S&P. Relative to a $763 fair value estimate, BlackRock's current $798 share price (as of January 12, 2024) implies that it is trading at a 5% premium to fair value.

If the company can match the analyst growth consensus and reverts to its mean valuation, here are the total returns that it could generate in the next 10 years:

- 2.5% yield + 8.5% FactSet Research annual growth consensus - 0.5% annual valuation multiple contraction = 10.5% annual total return potential or a 171% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

{kind=link}

{kind=link}

Due to my preference for a margin of safety, I am now rating shares of BlackRock a hold until they settle back into the lower $700 range (or become more valuable over time). I will now elaborate on the company's recent operating results and developments, as well as highlight two higher-yielding, undervalued alternatives to BlackRock until shares again enter a more attractive range.

BlackRock Is Firing On All Cylinders

{kind=link}

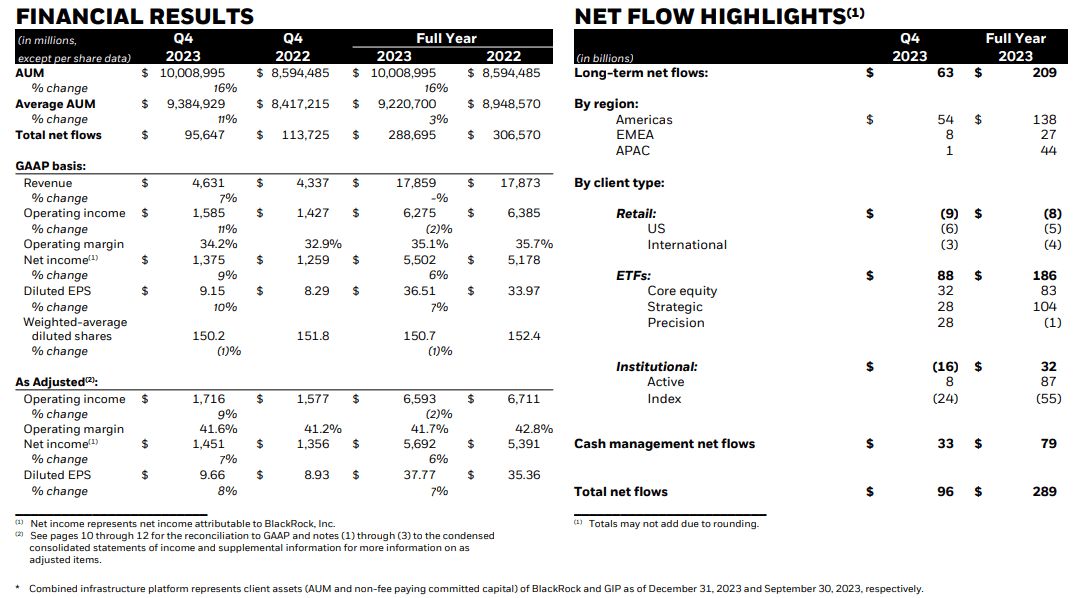

BlackRock delivered the goods to shareholders in its fourth quarter ended December 31. The company's net revenue grew by 6.8% year-over-year to $4.6 billion during the quarter, which met the analyst consensus .

This bounce-back was driven by two components. For one, the broader market has rallied in recent months. That had a positive effect in bringing BlackRock's assets under management back above $10 trillion for the first time since Q4 2021 . Additionally, the company benefited from $289 billion in net inflows in 2023. This shouldn't come as a shock considering the trust that many retail and institutional investors place in the company. Paraphrasing Chairman and CEO Larry Fink, when investors are ready to put money to work in the markets, they do it with BlackRock.

The company's adjusted diluted EPS surged 8.2% higher over the year-ago period to $9.66 for the fourth quarter. That was $0.82 ahead of the analyst consensus. Besides the higher net revenue base, BlackRock's non-GAAP net profit margin expanded by nearly 10 basis points to 31.3% during the quarter. Along with a 1.1% lower share count, that's how the company's adjusted diluted EPS grew faster than net revenue in the quarter.

Looking ahead, there are reasons to be optimistic. For one, BlackRock is buying Global Infrastructure Partners for $3 billion in cash and 12 million shares of BlackRock stock. As my fellow SA analyst Tradevestor put it, this could help the company to become a more balanced asset manager, with both conventional assets and hard assets.

Additionally, the recovery in its net inflows suggests BlackRock remains the go-to asset manager. Along with equity markets that should move higher with corporate earnings over time, this should help the company's AUM base, net revenue, and adjusted diluted EPS climb further.

BlackRock's 2% increase in its quarterly dividend per share to $5.10 was exactly what I forecasted. For the circumstances, that's not a bad raise. As I alluded to, dividend growth should accelerate again when earnings are predicted to reach a new all-time high in 2025. If the $45.05 2025 EPS analyst consensus from FAST Graphs proves to be correct, I could see the quarterly dividend per share moving up to $5.60 in the next couple of years. That would put BlackRock back around a 50% payout ratio. After that point, I would expect annual dividend growth to be in the high-single-digit range.

After over a decade of zero interest rate policy, there aren't many companies whose balance sheets are still conservatively capitalized. However, BlackRock is one of them. Thanks to its robust balance sheet, the company generated $181 million in net interest income in 2023.

MPLX LP ( MPLX ): An MLP That I'm Glad To Own

With shares of BlackRock looking a bit overstretched, the first high-yielding option that I like right now is the MLP, MPLX LP. The company's network of crude oil, refined products, and natural gas pipelines extends throughout much of the U.S. MPLX's primary customer and supermajority owner is Marathon Petroleum Corporation ( MPC ), comprising nearly half of its revenue in 2022.

{kind=link}

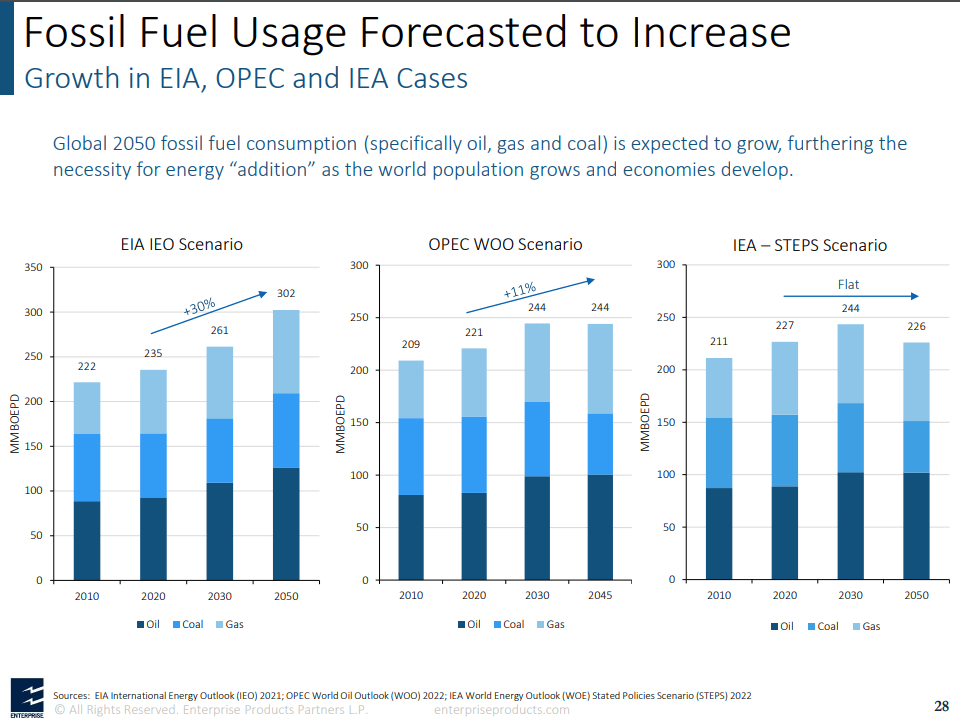

The core investment thesis is that, like it or not, the aggregate demand for fossil fuel products is going to be moving up in the next few decades or steady at the very least. Population growth and global economic growth (especially in emerging markets) will be the two factors underpinning demand for fossil fuels. This is how in various scenarios, global fossil fuel usage will be flat to up 30% between 2020 and 2050.

As a result of this demand, MPLX is committed to investing billions in expansion projects in the years to come. As I noted in my previous article, these include the Whistler natural gas pipeline expansion in the Permian and the Preakness II natural gas processing plant. For these reasons, the FactSet Research consensus is that DCF will rise by 4% annually long term.

{kind=link}

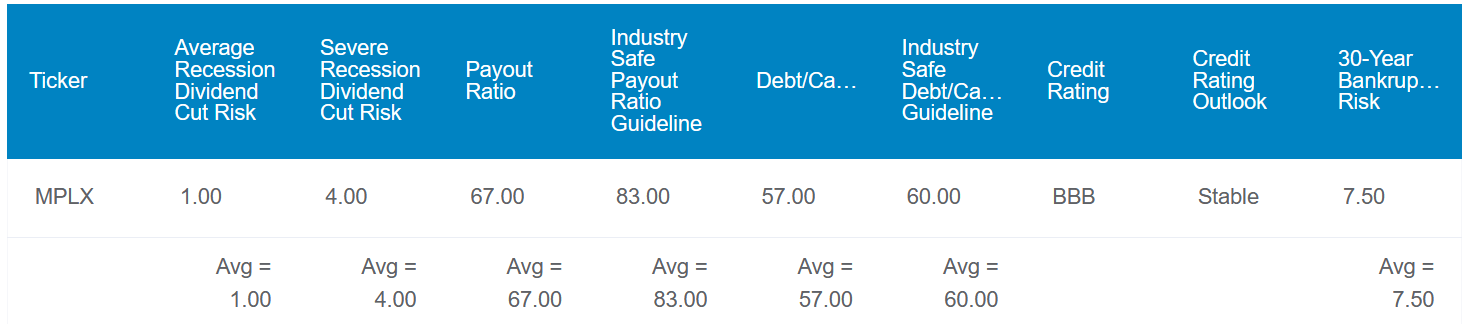

In tandem with its solid growth prospects, MPLX's 9.1% distribution yield is also well covered. The company's 67% DCF payout ratio is comfortably lower than the 83% that rating agencies prefer from the midstream industry. Also, the 57% debt-to-capital ratio is less than the 60% that is considered ideal for the industry by rating agencies. Thus, MPLX enjoys a BBB credit rating from S&P on a stable outlook.

{kind=link}

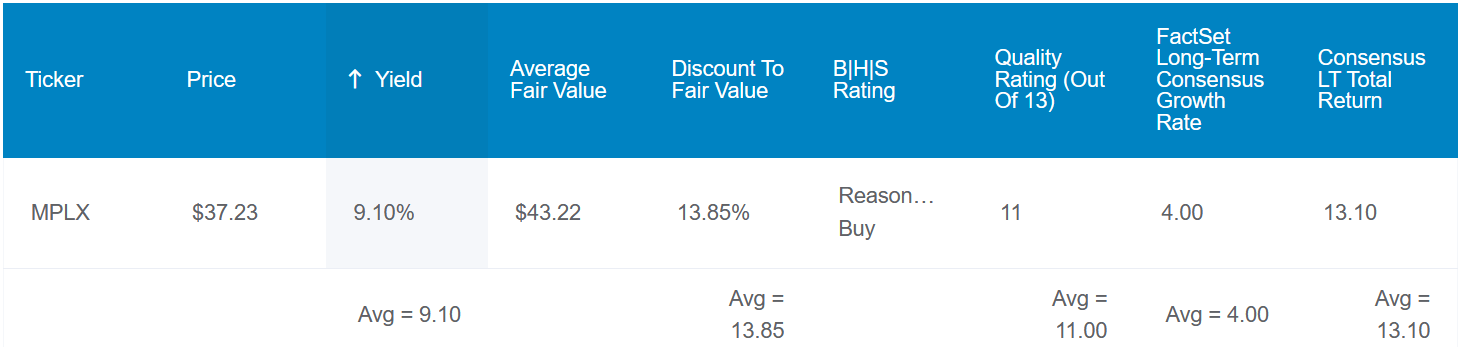

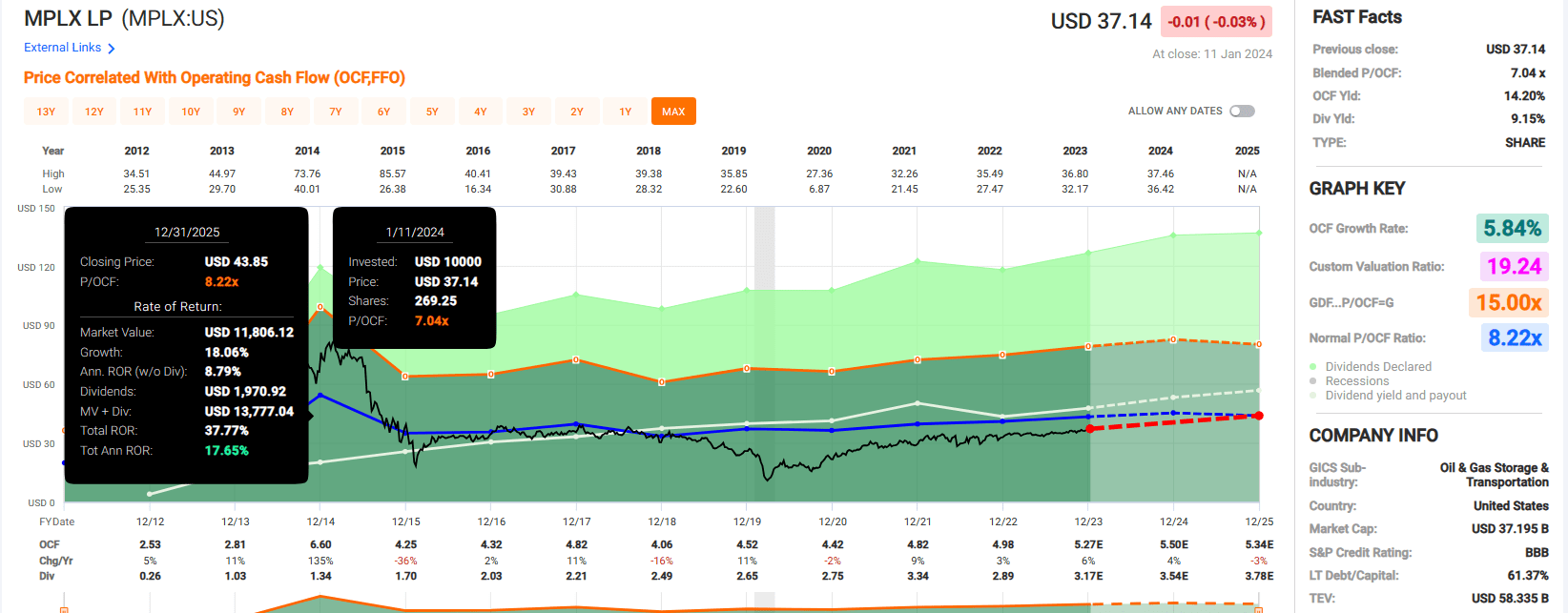

Best of all, MPLX could be 14% undervalued. That's because historical valuation metrics point to its fair value being $43 a unit versus its current $37 unit price.

If MPLX returns to fair value and grows as anticipated, here are the total returns that it could produce in the next 10 years:

- 9.1% yield + 4% FactSet Research annual growth consensus + 1.5% annual valuation multiple upside = 14.6% annual total return potential or a 291% 10-year cumulative total return

{kind=link}

VICI Properties ( VICI ): A Real Estate Play On The House Always Wins

Similar to the lottery, casinos use basic statistics to their advantage to make money over time - - lots of it. That explains the adage that the house always wins. Well, I'd take that one step further. As long as the house wins, so do their landlords.

Owning 54 gaming properties in the U.S. and Canada with over 60,000 hotel rooms and hundreds of retail outlets, 38 Bowlero ( BOWL ) bowling centers, and four championship golf courses, VICI Properties is the leading experiential REIT. Its most world-renowned properties include Caesars Palace, Harrah's Las Vegas, and The Mirage.

{kind=link}

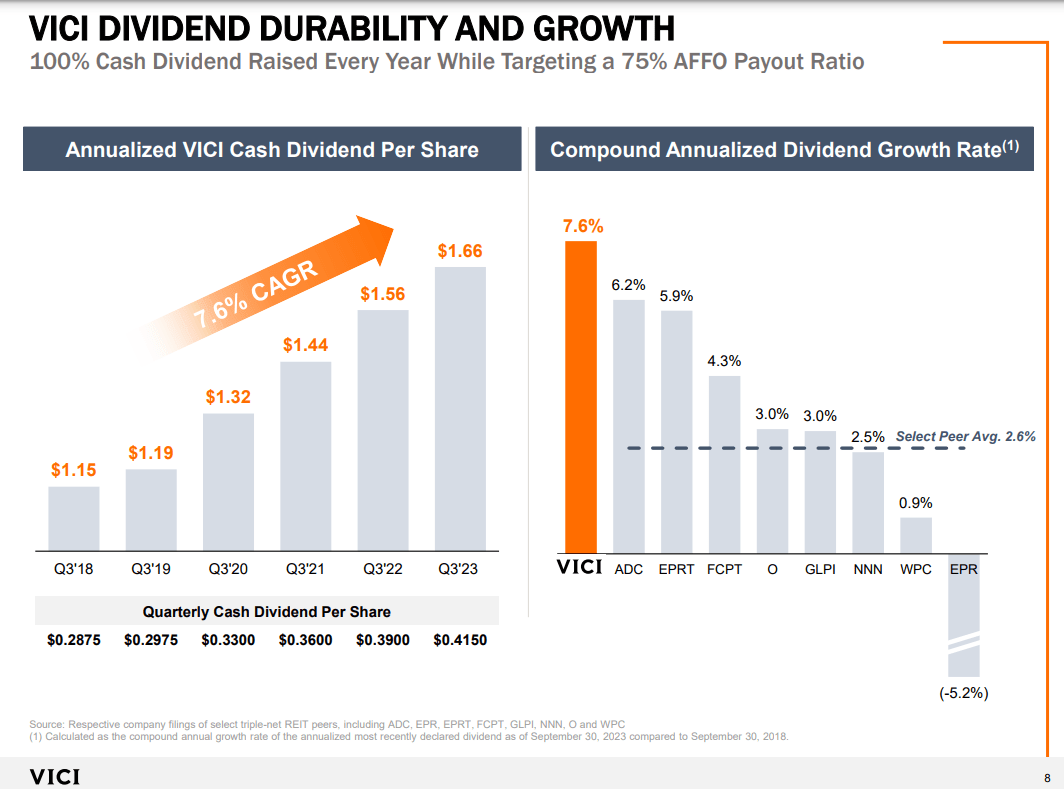

Owing to tens of millions of annual visitors to Las Vegas and its unmatched property portfolio, VICI has collected 100% of cumulative rent from tenants since its formation in 2017. Coupled with steady rent escalators that are built into its decades-long contracts with tenants, that's how VICI was able to compound its dividend by 7.6% annually from 2018 to 2023.

{kind=link}

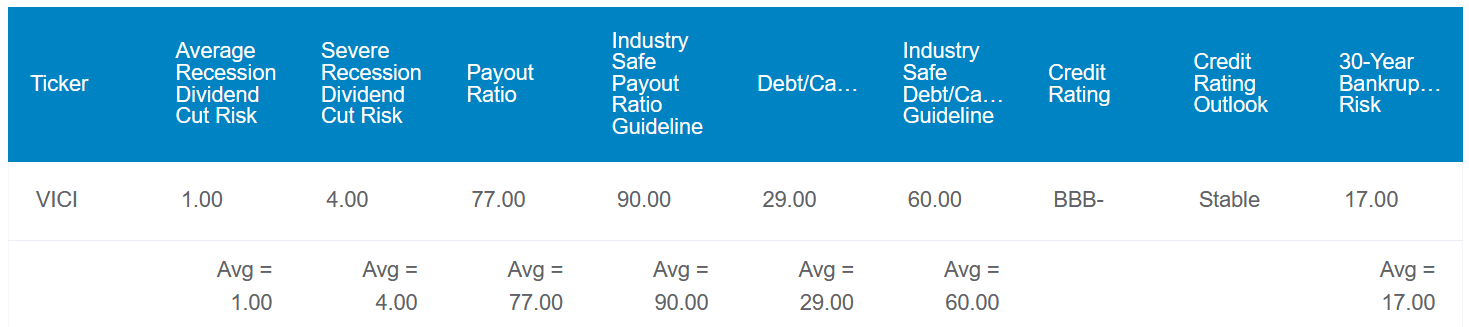

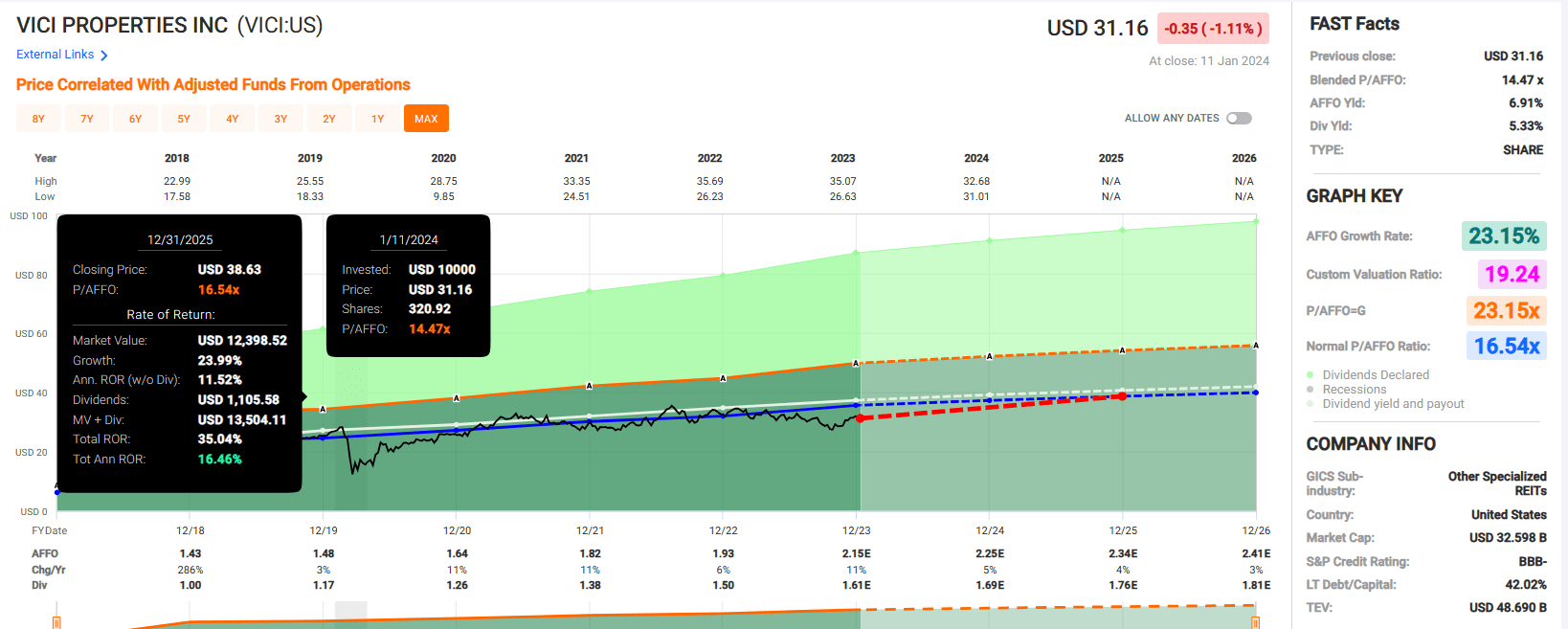

VICI's 5.3% dividend yield is also sustainable, with its 77% AFFO payout ratio coming in below the 90% that rating agencies desire. The company's 29% debt-to-capital ratio is also much better than the 60% debt-to-capital ratio that rating agencies prefer. That's why VICI's credit rating from S&P currently stands at BBB- on a stable outlook.

Moving forward, the company's dividend should keep growing at a healthy rate. That's because, besides rent escalators, VICI also can expand its non-gaming portfolio to drive additional growth.

{kind=link}

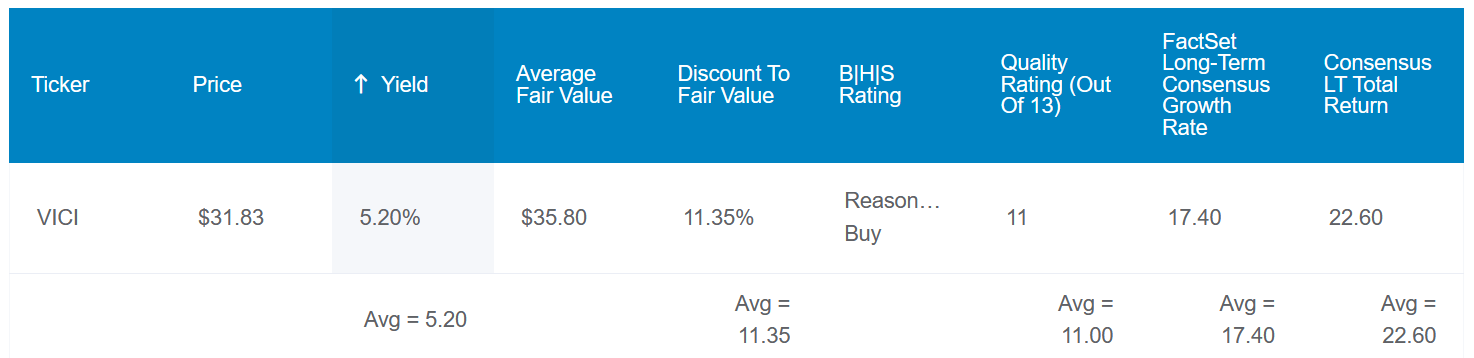

Like MPLX, the biggest risk to VICI is concentration risk. The company derived about 74% of its annualized base rent from Caesars Entertainment ( CZR ) and MGM Resorts International ( MGM ) as of November 2023 per its November 2023 Investor Presentation. The good news is that with shares potentially worth $36 each, the current $31 share price implies a 13% discount to fair value. In my opinion, this is a reasonable margin of safety.

If VICI were to revert to fair value and grow as expected, it could deliver the following total returns over the coming 10 years:

- 5.3% yield + 17.4% FactSet Research annual growth consensus + a 1.4% annual valuation multiple boost = 24.1% annual total return potential or a 766% 10-year cumulative total return

{kind=link}

Summary: Smart Investments Are Always Available

No matter what is going on in the world, I would contend that there are always opportunities in the investment universe. Even with the S&P 500's soft-landing forward P/E ratio of 19.6 coming in 17% above its historical multiple of 16.8, I believe this to be true.

BlackRock isn't quite at the point where I would add to my position. But as I hope to have demonstrated in this article, MPLX and VICI appear to be two opportunities that merit further consideration and research.

For further details see:

If You Like BlackRock, You'll Love These 2 High-Yielding Stocks