IGD - IGD: Time To Divest This Financials Heavy Equity CEF

2023-09-22 16:18:40 ET

Summary

- Voya Global Equity Dividend and Premium Opportunity Fund is an equity closed-end fund with a 9.6% dividend yield.

- The fund has failed to produce meaningful total returns in 2023 due to the negative impact of higher rates on dividend-paying equities.

- The fund is currently utilizing over 70% ROC to pay its dividend due to the underperformance in the global equity portfolio it holds.

- IGD has a high concentration in financials, which could be negatively affected if stresses in the banking sector re-emerge.

- Investors now have alternative options in high-yielding, low-risk assets such as treasuries and AAA CLOs.

Thesis

Voya Global Equity Dividend and Premium Opportunity Fund ( IGD ) is an equity closed end fund. The closed end management company holds global equities and seeks a high level of current income. The fund currently sports a 9.6% dividend yield, but has failed to produce any meaningful total return since we covered this name earlier this year:

Prior Rating (Seeking Alpha)

In our original coverage article, we outlined the good risk/reward analytics for the fund and its low standard deviation. The vehicle sits more on the defensive side via its analytics, and it seemed a good choice at the start of a year that was supposed to be very tumultuous.

Things turned out differently in the equity markets. While defensive, dividend-paying equities have done very poorly, mega tech-oriented funds have excelled:

We are looking at a couple of names here - the S&P 500 via the SPDR S&P 500 ETF Trust ( SPY ), the Vanguard Total Stock Market ETF ( VTI ), and the Schwab U.S. Dividend Equity ETF ( SCHD ). There is a clear bifurcation in total returns here, and the reason behind this occurrence is the AI (artificial intelligence) revolution. While AI has benefited tech mega-caps, higher rates have weighed down on dividend-paying equities.

As they say, 'the trend is your friend', and until the Fed starts lowering rates, or the market starts pricing lower rates via the yield curve, expect the above performance discrepancy to persist.

Furthermore, IGD has a high concentration in financials, which is the top sector in the fund and accounts for 21.4% of the exposure. With the sudden spike in yields in the past week as the Fed reiterated its ' higher for longer ' message, we feel there will yet again be pressure on financials. An informed reader needs to remember the regional banking crisis earlier in the year, entirely driven by the spike in yields and the ballooning in unrealized losses for held-to-maturity and available-for-sale treasury bonds on banks' balance sheets. Well, things have gotten even worse as of late:

The above graph depicts the iShares 20+ Year Treasury Bond ETF ( TLT ) which we covered here , and for which we have a $90/share price target. As yields increase, the price of long-dated bonds comes down in value. We can see how bond prices have performed since the March regional banking crisis. They are in effect down another -9%! So a bank holding $1 billion in notional of long-dated bonds has just had paper losses for another $90 million.

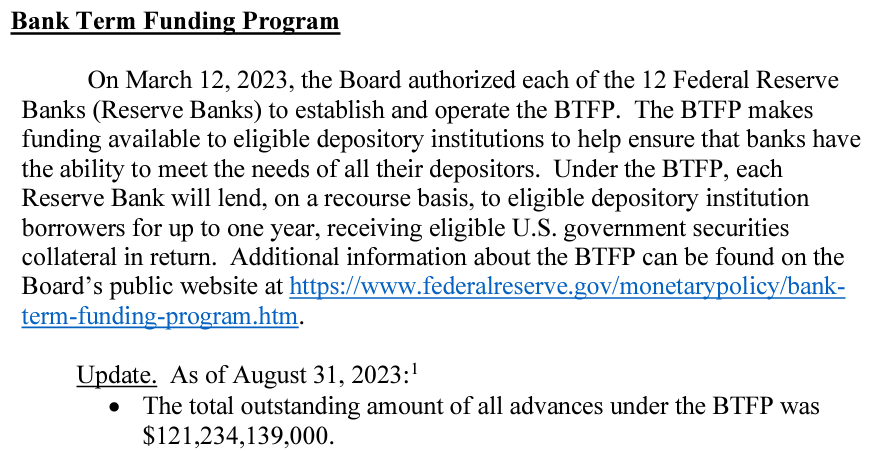

Do expect stresses to build again in the financial services industry, and watch closely the amounts borrowed under the Bank Term Funding Program (BTFP):

{kind=link}

Deposits have fled banks and gone into money market funds and short-dated treasuries, so in the case of financial stress, we expect to see the BTFP facility be drawn extensively.

IGD now warrants a rating downgrade because we do not see this fund outperforming until the Fed starts lowering rates, and furthermore its financials-heavy sectoral allocation is going to suffer if stresses in the banking sector re-emerge. Sell it now and revisit the name when the Fed starts cutting rates mid-next year.

Analytics

AUM: $0.39 billion

Sharpe Ratio: 0.52 (3Y)

Std. Deviation: 10.8 (3Y)

Yield: 9.6%

Z-stat: -1.76

Leverage Ratio: 0%

Composition: Global Dividend Stocks

Dividend Coverage

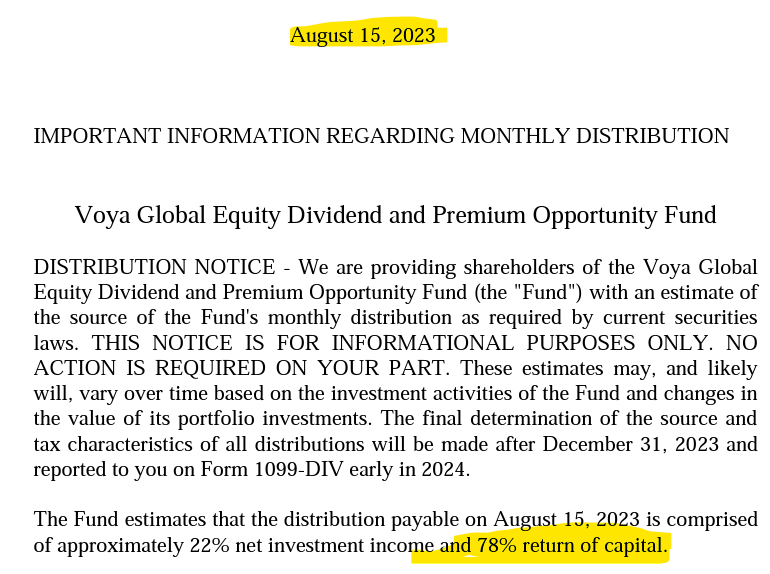

Equity CEFs need the underlying stocks to appreciate in value in order to cover their distributions. When equities do not perform (just like in IGD's case), the structure resorts to a high ROC utilization:

{kind=link}

As of its August 2023 payment date, the CEF utilized 78% of its own capital in order to pay the dividend. In essence, an investor is just getting their own money back. Do expect this set-up to continue as long as the underlying equities do not generate capital gains (i.e., appreciate in value).

A CEF structure is just a financial engineering vehicle to transform equity returns into monthly dividends. If there are no equity gains/returns then one cannot magically create dividends, so your own cash is being returned to you. Very long periods of ROC utilization result in quasi-permanent AUM decreases:

We can see how IGD has lost around 55% of its AUM in the past decade from that feature.

Portfolio Composition

The fund contains a portfolio of equities and is overweight the financials sector:

Sectoral Allocation (Fund Fact Sheet)

The sectoral composition is fairly conservative otherwise, with a high allocation to health care, industrials, and consumer staples.

From an individual name perspective, the top holdings are large multinational corporations:

Top Holdings (Fund Fact Sheet)

We do not think there is actual default risk associated with any of the names in the portfolio, however as large-cap value equities, many of these names will continue to have a subdued performance in today's interest rate environment, and furthermore, a new flare-up in bank balance sheet issues will further cut value here.

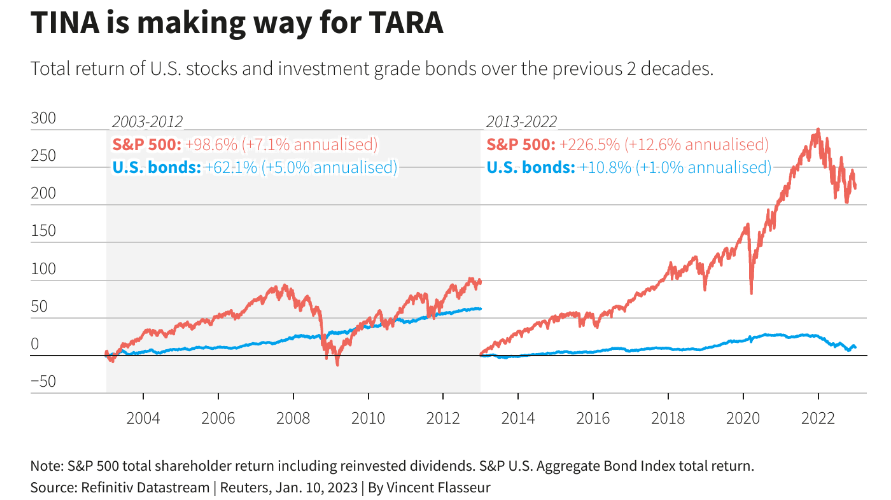

An Investor Now Has Alternatives - TARA Has Arrived

Prior to the Fed starting to move rates higher, it was said that investors had no alternatives to equities, hence the moniker TINA - there is no alternative. Well, TINA has left, and TARA has arrived (there are reasonable alternatives):

{kind=link}

With short-dated risk-free treasury bonds yielding well in excess of 5%, investors can choose not to be in equities and still receive hefty returns with no risk. IGD is down -2% this year, with downside risk. A pure treasury portfolio would have yielded close to 3%, hence a 5% gap.

If an investor does not see a lot of upside in the near-term, but actual downside, they can now just wait it out in cash and actually get compensated for doing so.

Furthermore, there are short-dated corporate bond funds which are yielding close to 6%, or even AAA CLO funds passing to investors yields above 6%. There are plenty of high-yielding, low-risk alternatives out there at the moment.

Conclusion

IGD is an equities CEF. The fund invests in global dividend-paying equities and has current income as its main goal. The CEF has a 9.6% yield which is currently unsupported, and the fund utilizes a 78% return of capital in order to cover its latest dividend. This is not unusual since the collateral pool has failed to perform, IGD being in a negative total return territory this year. Expect more of the same as long as the underlying stock portfolio fails to generate capital gains.

Our main issue with IGD at this stage lies with its large financials exposure, which could significantly drag it down in a scenario where a banking crisis flares up again. With yields up aggressively in the U.S. in September, we will see again pressure on banks' held to maturity and available-for-sale portfolios.

We do not see the large cap dividend-paying stocks that IGD holds performing extremely well until the Fed starts cutting rates, and actually, we think the CEF runs significant downside risk via its financials sleeve. With high-paying alternatives now in treasuries and AAA CLOs, a retail investor is best served to Sell here and revisit the name once the Fed starts cutting rates, in our view.

For further details see:

IGD: Time To Divest This Financials Heavy Equity CEF