BTAFF - Igniting Alpha: A Value-Driven Dive Into British American Tobacco

2023-11-09 02:51:36 ET

Summary

- British American Tobacco is a compelling value play with low price to book, price to earnings, and price to cash flows ratios.

- The tobacco industry has been subject to overreaction by investors, and BTI is undervalued compared to its competitors.

- Despite regulatory and health concerns, the perceived magnitude of risks to BTI are far greater than the intrinsic risks, making it a strong investment opportunity.

Investment Thesis

Since Benjamin Graham first proved that value-based strategies could produce abnormal returns investors and academics alike have flocked to the strategy. Value in nature implies a quantitative lens where intrinsic price exceeds current price. Our analysis reveals British American Tobacco as a compelling value play, embodying the essence of value as defined by Lakonishok, Shleifer, and Vishny (1994) . British American Tobacco ( BTI ) falls well in the value category with its enticing low Price to Book (0.75), Price to Earnings (6.61), and Price to Cash Flows (4.99) ratios. From here we will identify additional qualitative and quantitative factors to show investors that the Tobacco Industry is currently undervalued and that BTI is the best value play amongst them. Lastly we believe the reasoning behind this opportunity of mispricing is consistent with the behavior theory, the value premium is derived not from increased systematic or firm-specific risk but market wide overreaction. We believe with strong conviction that this is precisely the case for BTI and we will prove this in our valuation section.

Company Background/Description

British American Tobacco, a legacy that spans over a century, is a multination conglomerate with a stronghold in the tobacco industry. With a diversified product portfolio encompassing cigarettes, smokeless tobacco, and modern nicotine delivery systems, BTI holds a robust market presence in over 200 countries. Its notable brands, such as Dunhill, Lucky Strike, American Spirit, and Pall Mall, continue to be consumer favorites, symbolizing a blend of tradition and innovation.

We can also take an opportunity to apply qualitative factors to the company here. Using this lens we consider the Economic Moat derived from value principles of Warren Buffet. For the moat, BTI has a long-standing presence and substantial market share in over 175 markets globally, coupled with a well-established brand portfolio. We can break this down further by utilizing Porters Five Factors.

Bargaining Power of Buyers :

The bargaining power of buyers in the tobacco and nicotine industry is relatively low due to the nature of the products.

Bargaining Power of Suppliers :

Suppliers, primarily farmers providing raw materials, possess high negotiation power. Some farmers are transitioning from tobacco to fast-moving agricultural items, reducing competition among tobacco growers. Maintaining good relationships with suppliers is crucial for BTI to mitigate the impact of supplier negotiation power on profitability??.

Threat of New Entrants :

The threat of new entrants is low due to high barriers to entry at the global or national level. The restrictions on advertisement and marketing on tobacco products, along with the challenge of achieving economies of scale, deter new entrants. Well-established companies like BTI present formidable competition to new entrants?.

Threat of Substitute Products :

The threat from substitute products is moderate as consumers demand for non-combustible? has risen in the past decade. However, heavy regulation of non-combustibles has quelled substitute products.

Rivalry Among Existing Competitors :

The tobacco industry is fiercely competitive. BTI faces stiff competition from other tobacco giants like Philip Morris (PM), Altria (MO), Japan Tobacco (JAPAF), and China Tobacco National Company (CTOBF). However, this competition is concentrated as there are only a few top companies.

Review Of Competitive Environment

Let's look more closely at the rivalry and substitute product categories. Throughout our analysis we will look most closely at Philip Morris and Altria as their sizes and markets are almost similar. Currently Philip Morris is priced as the winner in the industry trading at an EV / EBITDA nearly double the industry median. This is due to their lead in next generation tobacco substitutes. PM currently derives 35% of their revenue from next gen products, which is their leading differentiating factor. Currently BTI's revenue consists of 10.5% next gen products. Although at first glance this is not nearly as good one must consider that this is nearly double the 5.5% it was only just 2 years ago. Revenue has grown in this category by over 40% in the past two years. This clearly indicates that BTI is having success with their new product lines while PM has seemed to slow down growing revenue 9% in the category. Lastly looking at Altria they are in the most trouble in this segment due to the heavy regulation of JUUL over the past years. Their next gen product segment shrunk slightly year over year and they have an uphill battle to get new product lines to market.

Overall Economic Moat for BTI is strong due to their advantages in the power of buyers, and low threat of new entrants mixed with their current large market share and diversified product line helping them in the other categories. Looking at TTM figures BTI currently leads in revenue with 35.85B to PM's 34.28B and in EBITDA with 18.24B to PM's 13.54B. Considering their current fundamental strength with their growth in next gen products it's clear BTI is a leader here and is severely underpriced at its current $69.5B market cap relative to PM's $135.8B.

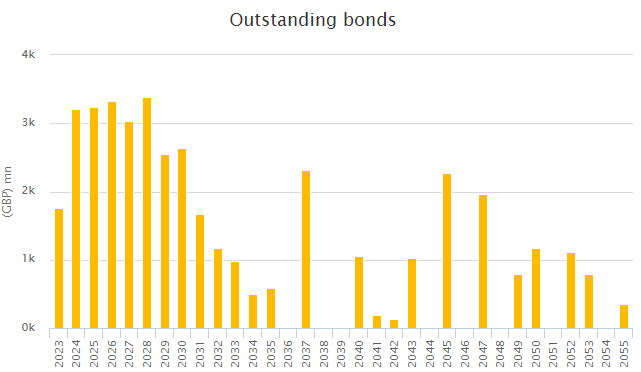

Outlook on Debt

Beyond the competitive landscape of next gen product lines a significant factor at hand is BTI's debt. BTI currently has a total debt of $53.55B with a D/E of 58.06%, the highest total debt in the industry. 41% of the outstanding bonds will become due between 2024 and the end of 2028.

{kind=link}

We can also break this out in USD millions as:

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| $3906 |

| $3947 |

| $4059 |

| $3709 |

| $4127 |

With interest rates much higher and the outlook being they will stay here this may be a concern to investors. Currently the average coupon is 4.1% across all of their bonds while new issuances would likely average between 6.5% and 7%. Although this seems alarming the magnitude of these bonds due are a stark decrease from the prior 5 year average, $8.04B per year. With BTI's robust free cash flow they are actually positioned to pay off these bonds without rolling them forward while continuing to grow its strong dividend.

QOE Capital

As you can see the forecasted payback table shows dividends continuing to increase and a positive Net Change in Cash much greater than their 5 year average of $147M. Additionally they maintain the ability to issued new debt in smaller amounts than they have historically should opportunities arise. With an after tax cost of debt being around 5.3% although higher than what they have paid historically this won't prevent them from taking up strong projects.

So Why Has BTI Fallen Out of Favor?

BTI shares have experienced a notable decline, reflecting broader investor concerns about the tobacco industry's future amid shifts in consumer behavior and regulatory pressures. The stock has witnessed a 23% drop in price year-to-date, with a reported decrease to $31.09 from the start of the year at $39.98?1??2?. This fall out of favor can be partly attributed to BTI's relative valuation to competitors like Altria Group and Philip Morris International, particularly as the market is increasingly factoring in the potential of next-generation products and the challenges of a higher debt load.

Looking at relative valuation the argument that BTI is behind PM in next gen products is valid but as discussed before ground is being made up rapidly. Beyond that we have shown that BTI is financial sound and supported by their strong cash flows. Taking total debt as a negative factor at face value is a naïve approach. BTI can lever up more because of their robust business. This was an advantage of theirs when rates were low and it's still an advantage now because they are uniquely able to continue raising dividends without rolling debt forward.

Lastly the concerns regarding the long-term strength of the tobacco industry are valid, given the global trend towards smoking cessation and stricter regulatory environments. However, BTI's strategic focus and robust growth in next-gen products indicate a potential to outpace the overall industry's issues. With the New Categories segment expected to achieve profitability by 2024 and a target of £5B by 2025, BTI is on pace to adapt effectively to the evolving landscape. Overall, investors are guilty of overreaction to these factors stated above and has caused BTI to have increased upside. We are able to see through these overreactions and utilize the behavioral theory as our edge.

Main Points Supporting Thesis

Our thesis is rooted in two major points, the terminal value of the Tobacco industry being over discounted and undervalued as a whole and BTI itself being undervalued relative to the industry. During our analysis a glaring figure we noticed is that median EV / EBITDA of comparable companies when used to calculate Terminal Value through the Multiples Method implies a Free Cash Flow growth rate of (-4.69%). Although governments worldwide are making efforts to regulate the industry and decrease future consumption amongst younger generations this still seems extreme as there is no data to back this stark decline. According to Statista , the expected CAGR over the next 5 years is expected to be 2.55% with developing countries expanding consumption.

BTI specifically has posted CAGR in revenue over the past 5 years of 3.49% while its EV/EBITDA of 6.90x implies -5.44% terminal FCF growth. Yes eventually regulation efforts will likely create earnings impact but the magnitude currently priced by the market is farfetched. This alarming, implied growth rate may however be related to low WACC due to BTI's beta of 0.405. Which again would mean the market is over discounting the cash flows into perpetuity. We identified its value ratios of P/E, EV/EBITDA, B/M, P/CF all on the lower end of the industry despite its robust growth against competitors in revenue, EBITDA, and free cash flow.

Valuation Analysis

Employing a disciplined DCF model, we scrutinized the industry and BTI's stance within. First of all, BTI has posted a strong year so far and 3.5% growth YoY on revenue looks likely. Beyond this we used a conservative 1.75% growth rate tapering down to .75% in 2028. The result is the following Free Cash Flow to Firm:

| Stub |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 7,165 |

| 14,190 |

| 14,403 |

| 14,583 |

| 14,729 |

| 14,839 |

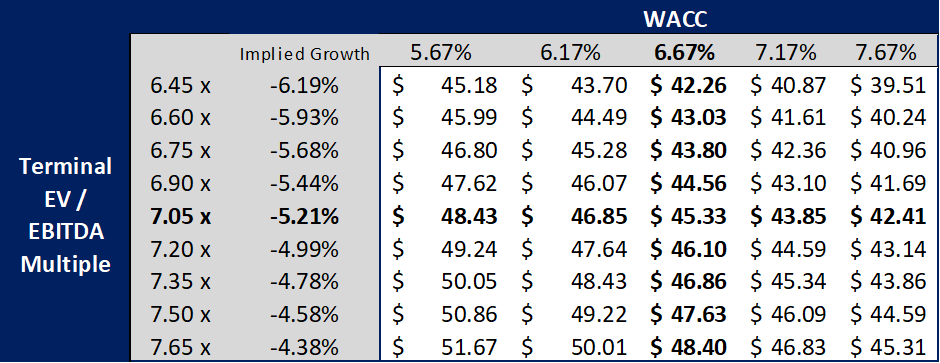

To properly calculate WACC we ran a regression over the past 500 trading days to get a beta of 0.405. This low beta leads to our low WACC. Outside of beta we were generous with Market Return and Cost of Debt to get a more conservative WACC figure, and in addition we have provided a sensitivity table.

QOE Capital

Looking back at our terminal value approaches in our Multiples Method we believe BTI will move toward the industry median and even with the heavily negative implied FCF Growth there is a healthy implied price of $45.36. In our Perpetuity Growth Method, we choose what we believe is a much more reasonable -2% Growth rate giving us an implied share price of $58.10.

QOE Capital

Lastly, for our DCF, we have our sensitivity table. Currently, industry multiples are tight within 8x but considering the implied growth there is definitely a case to be made that over the long run we could see multiples move towards 9x+ as shown in our Perpetuity Growth Model at -2% growth.

{kind=link}

Overall, our takeaway from our valuation is that BTI is strong value play and the implied growth rates really shine light on this beyond just their strong value ratios. It's important for us to remember that value plays have longer timeframes to correct to their intrinsic value. Value stocks shine over 5-year periods. As obscene as some of these implied growth rates are it is just as obscene as to think that the market will price BTI correctly over the course of one year. Simply put the overreaction to qualitative factors such as regulation efforts and expected changes in consumer behavior will take time to overcome. For this reason, we will be conservative, stick to the Multiples Method and issue our $46 price target and leave extra upside on the table.

Possible Catalysts

So why is the value good now? What could reverse the trend in share price? We have shown BTI is relatively undervalued to competitors and the industry is discounted as a whole. Additionally we believe this is due to common overextrapolation and overreaction of investors consistent with behavioral theory. Price will reverse when the leading factors investors are concerned by subside or are overcome.

- Next Gen Products:

- New Categories segment expected to achieve profitability by 2024 and a target of £5B by 2025

- New Categories are expected to continue growing at 20%+ YoY in 2024 while competitors are stalling

- Paying Down Debt:

- As BTI continues to pay down debt in 2024 their financial strength will become more clear

- Concerns about persistent rates impacting financials will subside

- Sustained Revenue Growth:

- Over the long run revenue growth persisting will be major driver of upside as the current expectation is for cash flows to shrink into perpetuity.

Discussion of Risks

Despite the compelling narrative, certain risks could thwart our thesis. The overwhelming issue here is the qualitative risks of regulatory escalation and systematic decrease of tobacco usage due to health concerns. Yes we see these as real risks to BTI. However, our stance is that the perceived magnitude of risk by investors is far greater than the intrinsic risk here. For reference, looking at our target implied FCF growth of -5.1%, this rate implies that FCF will drop 93% over the next 50 years. The first reports tying tobacco to health issues came out of German in the 1920s. The Surgeon General's scientific study group declared the relationship in 1956. Over the past 65 years, we have not seen any indication in earnings that would suggest such a strong drop in cash flows over the next 50 years. The last qualitative risk would be competitive pressure. This is a real risk and especially with younger generations turning away from traditional tobacco there is the possibility of losing ground to innovative competitors. That being said, BTI has continued to diversify its product offerings as well as shown better than average revenue growth over the past 5 years.

We have also touched on the risks of high debt and sustained higher rates. BTI undoubtedly has a large sum of debt to be paid with a large portion coming due in the next 5 years. As we discussed above they are more than capable of meeting their debt obligations without rolling it forward and while continuing to provide their favorable dividends. Moreover the perceived cost of debt by investors seems to be misplaced. The after-tax cost of issuing new debt would be around 5.3% as opposed to their current average cost after-tax of 3.1%. This difference would have minor impact on their bottom line and is not significant enough to prevent them from investing in good projects. Lastly, a more traditional quantitative risk measure, BTI has an exceptionally low beta of 0.405. This will provide for less intense swings in value during volatile markets and along with its high dividend yield provide dampening for a portfolio. .

Conclusion and Actionable Takeaway

British American Tobacco, with its blend of undervalued metrics and resilient growth, stands as a beacon of value in a market clouded by undue pessimism towards the tobacco industry. While acknowledging the entailed risks, the compelling valuation juxtaposed with a conservative price target of $46/share, warrants a 'buy' stance for the discerning investor. In the labyrinth of market misjudgments, BTI emerges as a pathway to value-driven growth, rewarding those with the foresight to see through the smoke of market myopia.

British American Tobacco shares have experienced a notable decline, reflecting broader investor concerns about the tobacco industry's future amid shifts in consumer behavior and regulatory pressures. The stock has witnessed a 23% drop in price year-to-date, with a reported decrease to $31.09 from the start of the year at $39.98??. This fall out of favor can be partly attributed to BTI's relative valuation to competitors like Altria Group and Philip Morris International, particularly as the market is increasingly factoring in the potential of next-generation products and the challenges of a higher debt load.

For further details see:

Igniting Alpha: A Value-Driven Dive Into British American Tobacco