PLDGP - IGR: 3 Reasons This REIT Fund Gets An Upgrade

2023-09-28 09:00:00 ET

Summary

- CBRE Global Real Estate Income Fund held a Sell rating from us since September 2022.

- That has been the correct call as the REIT CEF has delivered massively negative returns.

- We give you 3 reasons why we are upgrading this to a hold.

It has been rough. REIT investors have been taken to the cleaners. Even though our own portfolio was just around 11% in REITs, and all of that was buffered with covered calls, we felt the tremors and are down on several positions. In most cases our cost basis was pretty good, or so we thought. While the market decline took no prisoners, it did bring opportunities and chances to wrap up trade ideas. That is what we are doing today with CBRE Global Real Estate Income Fund ( IGR ).

The Fund

IGR is one which we have covered a few times before. The fund is of the closed end variety and as the name suggests, invests in real estate around the world. The fund definitely knows what it likes as evidenced by the heavy weighting to its top holdings.

CEF Connect

Familiar names such Prologis Inc. ( PLD ), Simon Property Group Inc. ( SPG ) and Sun Communities Inc. ( SUI ) grace the top of the list. While the fund may love what it owns, it also does not stay in love for long. The turnover is high and on last check it was close to 58%.

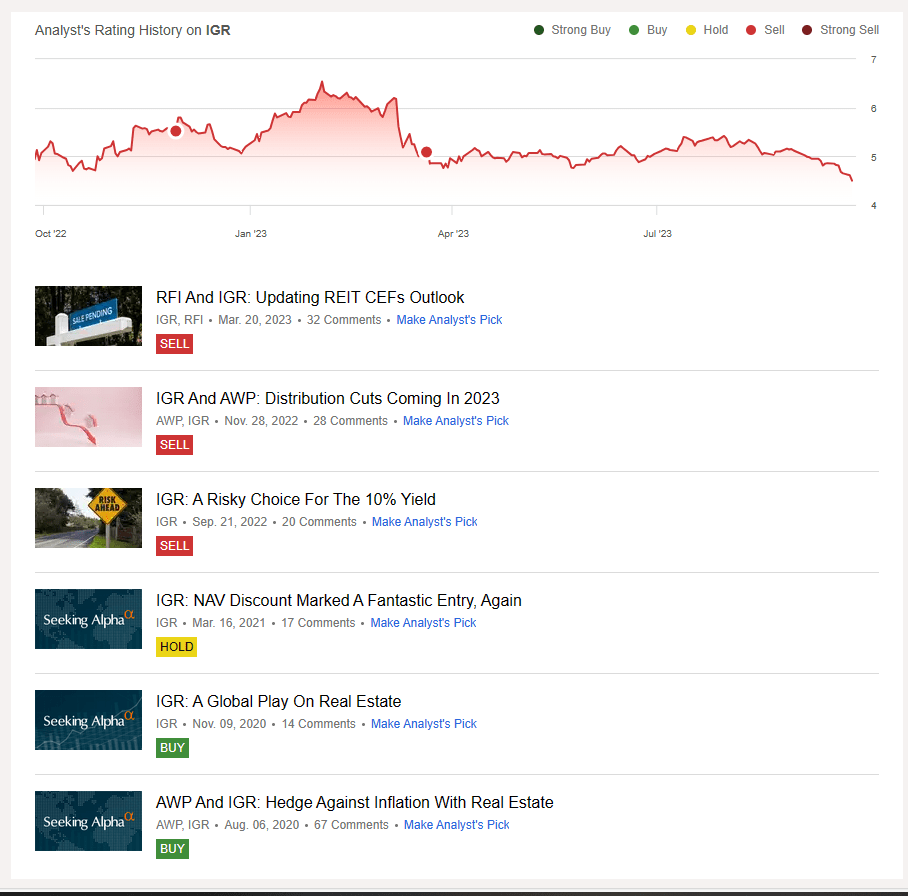

Our coverage here has varied based on the setups. Too many readers are quick to label our views as bearish and nothing could be further from the truth. Below you can see the bull and bear calls on IGR.

{kind=link}

In this particular case, all the trade ideas were profitable. The stock went up between August 6, 2020 and March 16, 2021 and is down substantially since the first of our trinity of bearish articles.

Seeking Alpha

The point of that history lesson is that it is best to trade these funds, as there is no real money to be made with a buy and hold strategy. IGR's total returns have been negative 2.56% over the last 5 years.

That gets us to our main course for today and we give you three reasons why we are ending our Sell rating.

1) Second Lowest Relative Strength Index In 10 Years

IGR's 14 day RSI is 14.06. That is the second lowest in the last decade. That kind of feat is hard to accomplish for funds and shows system wide unrelenting selling pressure. Even getting the second place was close as it almost overtook the COVID-19 selling numbers.

Can it go lower? Of course. Can it crash into the sub $4.00 level? It is possible. But no one in their right mind should push the "Sell" into those readings.

2) A Solid Discount

The fund trades at a nice double digit discount to its NAV.

CEF Connect

We would prefer this metric to be stronger but it is in the middle of its range. The Z-score is nice but it could be better.

CEF Connect

Nonetheless, it is an improvement from where it was some time back. The fund as recently as August, traded at just a 6% discount. These changes reflect better pricing for a fund that has delivered poor long term returns.

3) REITs Are Getting Cheap

We don't have a lot of nice things to say about the fund's top holdings, but on the whole REITs have now discounted a rather aggressive Federal Reserve. As an asset class they are not exactly bombed out, but setup to deliver modest returns even if the interest rates cuts don't come. Sure there are challenges in this sector and office might not normalize this decade. Even the office-adjacent REITs like Alexandria Real Estate Equities, Inc. ( ARE ) might take a few years to absorb the office conversions into Lab spaces . But REITs as a whole, have given up the hope of lower rates and even some big bulls are looking hopelessly defeated. Would we want to press on the downside in this scenario? No.

Verdict

It is an upgrade but it is not a signal to buy. CEFs remain a dangerous area to tread and our biggest gripe here is the leverage. This amplifies both your upside and downside.

CEF Connect

Combined with large distributions that have to be paid monthly, it forces the fund to "sell-low". That is why over the last decade the fund has not beaten Vanguard Real Estate ETF ( VNQ ), despite using leverage. That is about 2.5% compounded.

So while we think this can bounce, the leverage hangs over its head like a Damocles sword. Also hanging over its head is the upcoming distribution cut. Yes, we know, we know. Investors will believe that a fund that has delivered 2.5% annual returns over the last decade can fund a 14.5% distribution yield (that's on NAV, yield is 16.14% on price). We think that might happen in the fifth season of Stranger Things , but not in real life. That distribution will go down at some point. Possibly by 50%. So if you want to hang around with two swords over your head, that is your call. We are ending the "Sell" rating, moving to "Hold" and moving on.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

IGR: 3 Reasons This REIT Fund Gets An Upgrade