EQIX - IGR: REITs At A Tempting Discount But There Are Concerns

2023-05-16 11:12:40 ET

Summary

- After completing its rights offering last month, the fund continues to trade at what would appear to be an attractive discount.

- The fund offers exposure to global real estate when most other CEFs focus more specifically on U.S. allocations.

- IGR could be added for further diversification in one's portfolio at a fairly appealing discount; however, there are some concerns to consider.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 1st, 2023.

CBRE Global Real Estate Income Fund (IGR) recently finished up its rights offering earlier in April. Stanford Chemist wrote up more of the details of the offering beforehand, then provided a follow-up with the results. This offering was guaranteed to allow investors a discount since it was 95% of the closing market price. However, that also meant that since the fund was trading at a discount, it was guaranteed to be dilutive to shareholders.

Oftentimes rights offerings cause funds to drop quite sharply. That's why we often sidestep all rights offerings and revisit after the dust settles. In this case, since it had the guaranteed discount, participating if you held shares always made sense. For IGR, this was certainly the case, but it was also a lot of volatility going through March. So there was some unfortunate timing for this offering too.

Ycharts

For the most part, the biggest beneficiary for rights offerings tends to be the fund manager and not the shareholders. Occasionally, they can benefit both shareholders and management if designed to be such as the Cornerstone offerings. They design their offerings in a way that guarantees issuance above NAV.

Still, it seemed the CBRE here did somewhat of the right thing because, after being oversubscribed, they chose not to exercise this privilege. That meant they limited the dilution by not choosing to allow the additional shares to be issued. New shares were issued at $5.03, and the share price never breached this level, which is a positive for those that took new shares.

It has been a while since we last took a look at IGR, but since that time, the fund has been underperforming significantly. This rights offering plunge certainly played a role, but the overall weaker market also contributed to this.

IGR Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -1.91

- Discount: -12.23%

- Distribution Yield: 13.36%

- Expense Ratio: 1.24%

- Leverage: 28.55%

- Managed Assets: $1.208 billion

- Structure: Perpetual

IGR invests with an objective of "high current income, and its secondary objective is capital appreciation." They do this by investing "globally with an emphasis on the income-producing common equity and preferred stocks of real estate companies." They mention that "up to 25% of its assets in preferred shares of global real estate companies."

The fund is leveraged, and it was only moderately leveraged previously. However, a natural result of declines meant that the fund's leverage had climbed to a higher level. That being said, the fund's website shows a 31.09% leverage ratio at the end of March; it's actually a bit lower due to the new shares being issued through the rights offering.

IGR Portfolio Stats (CBRE Investments)

At least, that is assuming they didn't immediately increase their borrowings on the back of these new shares. This fund has shown that anytime they can, they will increase borrowings. Going from around $74 million in borrowings at the end of 2018 to now $345.2 million. That's even while the fund's total net assets shrunk to the lowest point in the last five years. Worth noting that the net assets would be higher now due to the new shares issued.

{kind=link}

With the leverage in this fund comes greater risks. Leverage means more volatility on both the upside but also the downside. It also means their borrowing costs have been rising with rising interest rates. They pay at the federal funds rate plus 75 basis points. The latest report showed an average rate of 2.44% for the prior fiscal year. According to their last report, unlike some REIT CEFs (Cohen & Steers,) IGR has not entered into anyways to hedge against the rising interest rates.

Performance - Attractive Discount

Now that the offering is over, the fund also looks to be providing a tempting discount. As we saw above, the fund's share price has underperformed the fund's NAV significantly. Of course, the main push for this would have been the rights offering, but overall the weaker results in the fund should also be considered. The plunge put the fund's discount near its longer-term average.

Ycharts

This is one of only a couple CEFs that focus more on a global allocation to real estate and REITs. So it can make it more unique. However, U.S. investments have been outperforming that of international markets for most of the last decade. That helped contribute to IGR's weaker relative results.

{kind=link}

Going forward, one would have to not only find the discount more attractive at this time but have a positive outlook on global REITs. REITs overall have been an area of the market that has remained challenged with higher interest rates. We aren't in a reversal stage for interest rates just yet, as the Fed is looking to put through at least one possibly more hikes. On the other hand, that also means rates pausing or being cut in the future could benefit this fund.

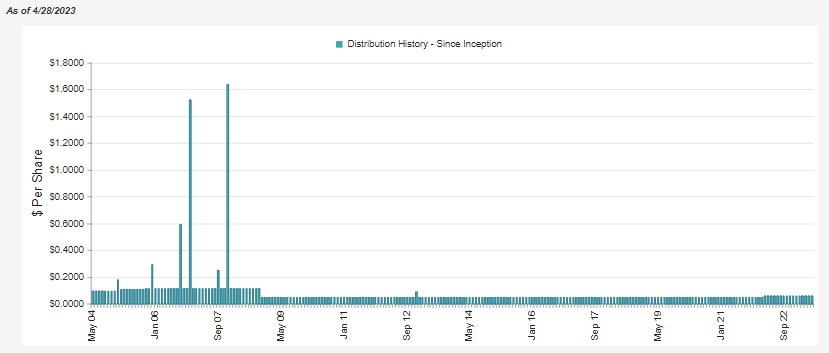

Distribution - A Cut Seems Likely

One of the more attractive features of IGR is likely its 13.36% distribution rate. Based on the NAV distribution yield, it's actually a bit more modest at 11.67% due to the significant discount. However, even that appears to be quite extended at this time, and a cut is likely. That could be a reason why the fund could stay stuck nearer its current valuation as well.

The fund, like many in the GFC, cut big. However, it's otherwise been fairly steady, with a couple of raises since.

{kind=link}

What could make the fund's current rate increasingly difficult is the higher interest rate costs on its leverage. Leverage doesn't bring the same benefits that it used to when you could get away with paying sub-1% rates. At between 5 and 6%, it is much more difficult for borrowings to provide an added boost.

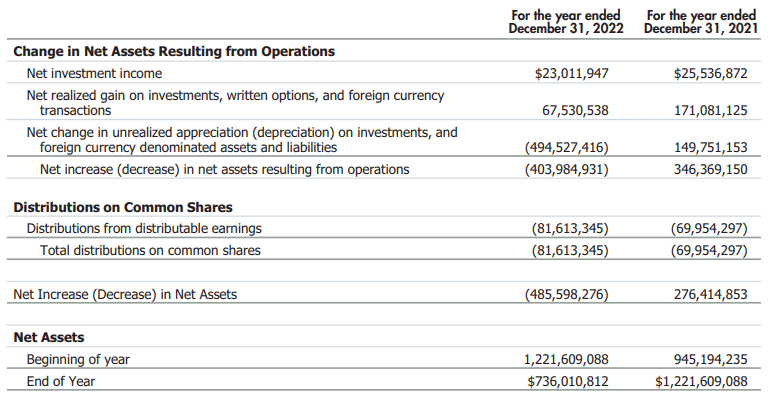

The fund also invests heavily in equities, with only a small sleeve of preferreds. Therefore, the majority of the fund's distribution will be covered through capital gains. They write options, and that helped contribute around $1.365 million in the prior year, so not exactly a massive gain.

{kind=link}

Additionally, going forward, the fund will now be paying more out to shareholders due to the rights offering issuing new shares. The net investment income may increase year-over-year. However, since it was a dilutive offering, the NII per share is likely to take a hit. NII per share went from $0.22 in 2021 to $0.20 in 2022.

Overall, unless we get some swift recovery from global REITs, this fund's distribution could become increasingly uncertain. Still, they just recently announced another three months at the same rate despite this elevated level and lack of coverage.

IGR's Portfolio

The portfolio data available is listed as of the end of March. That means the new capital that they are putting to work isn't reflected yet. Keeping that in mind, here's a breakdown of their portfolio.

IGR Geographic Allocation (CBRE Investments)

Being that the portfolio looks like it did just over a year ago in our last update, I suspect they won't make massive changes going forward. The largest allocation is in U.S. companies, but they also had material exposure outside the U.S. Last year, they listed 59.66% of U.S. common exposure. Japan's exposure was listed at 8.34%, and continental Europe was 7.42%, which is close to what we see today.

Where we have seen some shifting was in the fund's subsector exposure.

IGR Sector Allocation (CBRE Investments)

A year ago, the residential sector was just over 19% of the fund, which has now shifted to 13.44%. The top exposure now comes in with retail at 16.61% and industrials at 14.61%. The office is an important area to focus on as its one of the areas with the gloomiest outlook. At 5.48%, it isn't necessarily an overly large exposure, but it is something to watch.

Residential and retail REITs are also another area to focus on should there be a recession. We always know that there will be a recession, but it is always a matter of when. Those are other areas that could be hit particularly hard, even in REITs that generally have been laggards in sector performance overall.

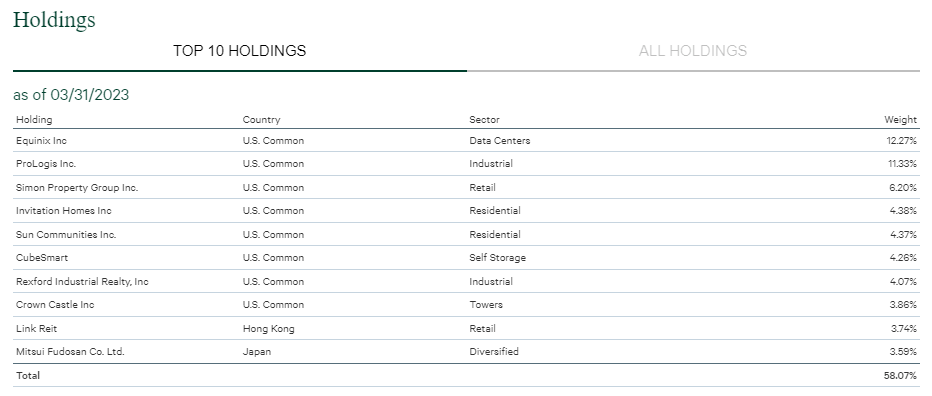

The fund's top ten holdings show us that IGR is highly concentrated for a CEF. They list a total of 76 holdings, but over 56% of the portfolio is in the top ten. In fact, the top two holdings make up nearly a quarter of the overall portfolio.

{kind=link}

That would mean an investor better be very comfortable with Equinix (EQIX) and Prologis ( PLD ) to be holding this fund. PLD last year was the largest holding, but it only came to a 7.04% allocation. EQIX was the sixth largest holding so that one really ramped up from the 3.83% weighting.

The fund's top ten at the end of February 2022 was 46.12%, so we've seen a narrowing overall. The percentage allocations to EQIX and PLD were a significant driver of this.

In the last year, all the fund's top ten holdings have performed fairly poorly except for EQIX. That could account for some of the growing allocations. PLD also saw a fairly weak performance, suggesting that the fund would have had to add to the holding in PLD to get it to the allocation it is today.

Ycharts

This was the case as of the end of March 2022 . According to their N-PORT, they held 415,385 shares of PLD. At the end of December 2022 , this was up to 718,154 shares. For EQIX, we see that they increased that position as well, as the results sort of indicated was the case. They held 67,059 EQIX shares in March 2022, and that had moved up to 126,080 by the end of 2022. Of course, that doesn't tell us exactly what happened between December 2022 and March 2023. It still gives us a good idea of what sorts of moves they made through the prior year. Given the larger allocations, it's probably safe to assume they at least didn't reduce these positions to a sizeable degree.

IGR Vs. Other REIT CEFs

IGR remains an interesting global REIT fund. There really is only abrdn Global Premier Properties Fund ( AWP ) that competes in the space. However, with the help of strong U.S. investments beating out global investments, Cohen & Steers has historically delivered superior results.

Ycharts

Past performance is no guarantee of future results, but in the case of Cohen&Steers Quality Income Realty Fund ( RQI ) and Cohen & Steers REIT and Preferred and Income Fund ( RNP ), it's a bit hard to get over just how much the results have diverged. You then have Cohen & Steers Real Estate Opportunities and Income Fund ( RLTY ) trading at a similar discount to IGR, and it becomes a tougher option to choose IGR. As C&S has tended to provide significantly superior results, and they have a fund that is just as attractively discounted.

RLTY isn't that old of a fund, so it actually only goes back to early 2022. Basically, right when REITs started to get destroyed due to higher interest rates.

Ycharts

However, even despite the short history of a terrible time for REITs, even RLTY showed they lost a bit less than IGR during this period.

Conclusion

The fund's rights offering recently crashed it to a deep discount, putting it closer to its longer-term average. On the other hand, RLTY is another beaten-down REIT name from the C&S suite. C&S has a more appealing longer-term and short-term track record. Being at around the same valuation, RLTY would continue to get my interest instead. A large portion of RLTY's leverage is also hedged through interest-rate swaps or fixed-rate financing. All REITs are getting hammered due to rising rates, but that's definitely a benefit for RLTY and the other C&S funds at this time.

In summary, I can see why investors would want to invest in IGR. It can make sense if one has a positive outlook on REITs and, specifically, global REIT exposure. That can add a bit of diversification to an investor's portfolio. With no hedging in place for their borrowings, they are more susceptible to continuing rising rates. I also wouldn't bank on that distribution rate in the future unless we see some serious recovery. So it comes down to one's own outlook in the future.

For further details see:

IGR: REITs At A Tempting Discount, But There Are Concerns