IHIT - IHIT: You Could Get An 8% Risk-Free Return Here In 2023

Summary

- Invesco High Income 2023 Target Term Fund is a CMBS closed end fund.

- The CEF has a December 1, 2023 target liquidation date.

- The fund is trading with a 4.25% discount to NAV, which will be realized upon liquidation.

- The current dividend yield for the vehicle is above 5%, with the collateral composed of mostly investment grade CMBS bonds.

- This article covers CEFs.

Thesis

Invesco High Income 2023 Target Term Fund ( IHIT ) is a closed end fund from a premier asset manager. What is particular about this vehicle is its term structure:

The Fund’s investment objectives are to provide a high level of current income and to return $9.835 per share (the original net asset value (the “NAV”) per common share before deducting offering costs of $0.02 per share) (“Original NAV”) to common shareholders on or about December 1, 2023 (the “Termination Date ”). The objective to return the Fund’s Original NAV is not an express or implied guarantee obligation of the Fund or any other entity. The Fund intends, on or about the Termination Date, to cease its investment operations, liquidate its portfolio (to the extent possible), retire or redeem its leverage facilities, if any, and distribute all its liquidated net assets to common shareholders of record unless the term is extended for one period of up to six months by a vote of the Fund’s Board of Trustees. The Fund’s ability to successfully return the Original NAV to holders of common shares on or about the Termination Date will depend on market conditions at that time and the success of various portfolio and cash flow management techniques.

Source: Annual Report

So under the current format, IHIT is supposed to liquidate on or about December 1, 2023. The liquidation date is subject to a six months extension by the Board of Trustees. A retail investor needs to note that the fund's collateral is NOT maturity matched - this means that the underlying bonds are not set to mature in the next 12 months, and the manager will take market risk by holding on to the collateral until the end of the year. That can be good or bad, depending on how this bear market develops. The collateral is made up of mostly investment grade CMBS securities, but there are junk rated CMBS bonds in there as well. The underlying assets can move around quite a bit, depending on how volatile the market gets.

Currently the fund has a 5% distribution yield and a 4.25% discount to NAV. The yield is achieved via leverage, with the fund sporting a 28% leverage ratio.

There are two ways the fund can move forward here in 2023:

1) Doing what is right by Shareholders

The vehicle has a distinct maturity date; hence it will have to liquidate its collateral, be it December 1, 2023 or six months later. By most analysts' consensus, we are going to experience a recession in 2023. That translates into volatility and potentially lower prices for some securities. When you add leverage on top, it could be a rough ride.

What is right by shareholders in our opinion, is a risk-free yield of above 8%. Is that achievable? Yes. The fund is trading at a 4.25% discount now, which is going to be realized upon maturity and liquidation. If the vehicle were to liquidate most of its longer dated assets now and only keep the bonds which would pay down by December while reinvesting the proceeds in 1-year Treasuries, it could achieve a yield in excess of 4% risk free. Coupled with the discount to NAV that would ensure a current shareholder would get 8%+ by the end of the year with de-minimis volatility and no headaches.

The funny thing about term funds is that they are set to liquidate around a certain date, so unless there is a massive bull market going on in risky assets (CMBS in our case), then the upside is fairly capped. We are actually looking at the flip scenario, where we are entering a recession and things could get really ugly. In our opinion what is right by shareholders is to ensure an 8%+ return by the end of the year by doing a lot of de-risking now.

2) What the CEF will probably end up doing

However, what the CEF will end up doing is not what is right by shareholders. A retail investor needs to realize that shareholder interests and asset manager interests are not always aligned. An asset manager always compares a portfolio's performance versus a benchmark, and mostly cares about relative value:

{kind=link}

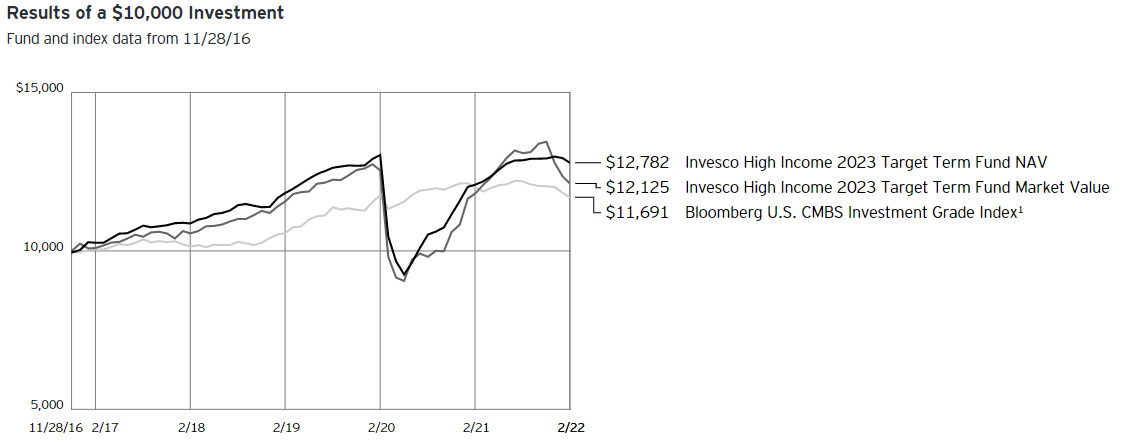

In this case the benchmark is the Bloomberg U.S. CMBS Investment Grade Index. The fund is currently trading below the $9.835 per share it aims to return to shareholders per its literature. Will it get to that level? We doubt it.

Most likely than not the managers are going to run the portfolio into the storm that 2023 will prove to be, and if things get really ugly by Q4 2023, they will extend the fund's duration. That is going to translate into volatility, and a net result that could be below the 8% outlined above. Why? Because the fund will take market risk. If we get a severe recession and asset prices plummet, the NAV could be down -10%. When factoring in the discount and yield an investor would be looking at a net small negative result. That is just a possibility of course, not a certainty. But we would prefer the certainty of a deleveraged term fund that would ensure we get more than 8% by the end of the year, irrespective of what risky assets do.

Conclusion

Invesco High Income 2023 Target Term Fund is a fixed income CEF. The vehicle is currently overweight investment grade CMBS bonds, with a sleeve containing junk CMBS securities (25% of the holdings). What is specific about this CEF is its term structure, with the fund set to liquidate on or about December 1, 2023. The liquidation date is subject to a six months extension by the Board of Trustees. A retail investor needs to note that the underlying collateral is not maturity matched, meaning the bonds in the portfolio have much longer maturity dates. The fund thus takes liquidation risk if it holds the portfolio until December - by liquidation risk we mean the risk of a significant market sell-off that results in lower bond prices and lower NAV for the fund heading into Q4 2023.

From our viewpoint, the fund can choose to de-risk now and liquidate the collateral that does not pay-down principal by December, and re-invest said proceeds in Treasuries. By doing so, the vehicle can offer shareholders an 8%+ return, coming from the discount to NAV of -4.25% which will go to zero, and the substantial yield offered by risk free securities such as Treasuries (in excess of 4% for that maturity ladder). De-risking now would ensure a less volatile, well defined return for the rest of the year.

Unfortunately shareholder interests and management interests are not always aligned, and we believe the fund will continue to run its portfolio and clip its fees until the termination date, with dubitable results in terms of obtaining net total returns in excess of 8% for the remainder of the life of the fund. What is certain is that the volatility is going to be much higher.

For further details see:

IHIT: You Could Get An 8% Risk-Free Return Here In 2023