IHS - IHS Holding Limited: Buy Forget And Compound Capital

2023-05-25 10:25:33 ET

Summary

- Telecom tower operators have the ability to compound capital faster than the market.

- IHS, with a presence in lucrative Africa, is poised to take advantage of demographic growth and demand, on top of an already excellent business.

- IHS stock trades at 7.5x P/FFO, which makes it undervalued compared to both larger comps with less attractive investments and smaller comps with less scale.

Introduction

One of my favorite investment tricks is to look at companies that have compounded like gangbusters in the US or Europe and invest in copycat companies in the rest of the world. One such firm, IHS Holding ( IHS ), is the fourth largest telecom tower operator in the world with most of its operations in Africa and a reminder in South America - all fast-growing and high IRR jurisdictions. As I show below, IHS is positioned to take advantage of demographic tailwinds, operates a great business, and has a long runway to grow. For these reasons, I have a bullish view of IHS.

IHS is a towerco, a company that builds and manages towers for telecom firms. IHS is the industry leader towerco in Nigeria and concentrates much of its business in Africa. Recently it has also expanded the business to Kuwait and some of Latin America.

Industry Economics

In order to illustrate the economics of the industry, here is a slide from an Industry Presentation by American Tower Corporation (AMT).

{kind=link}

Tower IRRs given location and number of tenants (AMTs Introduction to the Tower Industry Presentation)

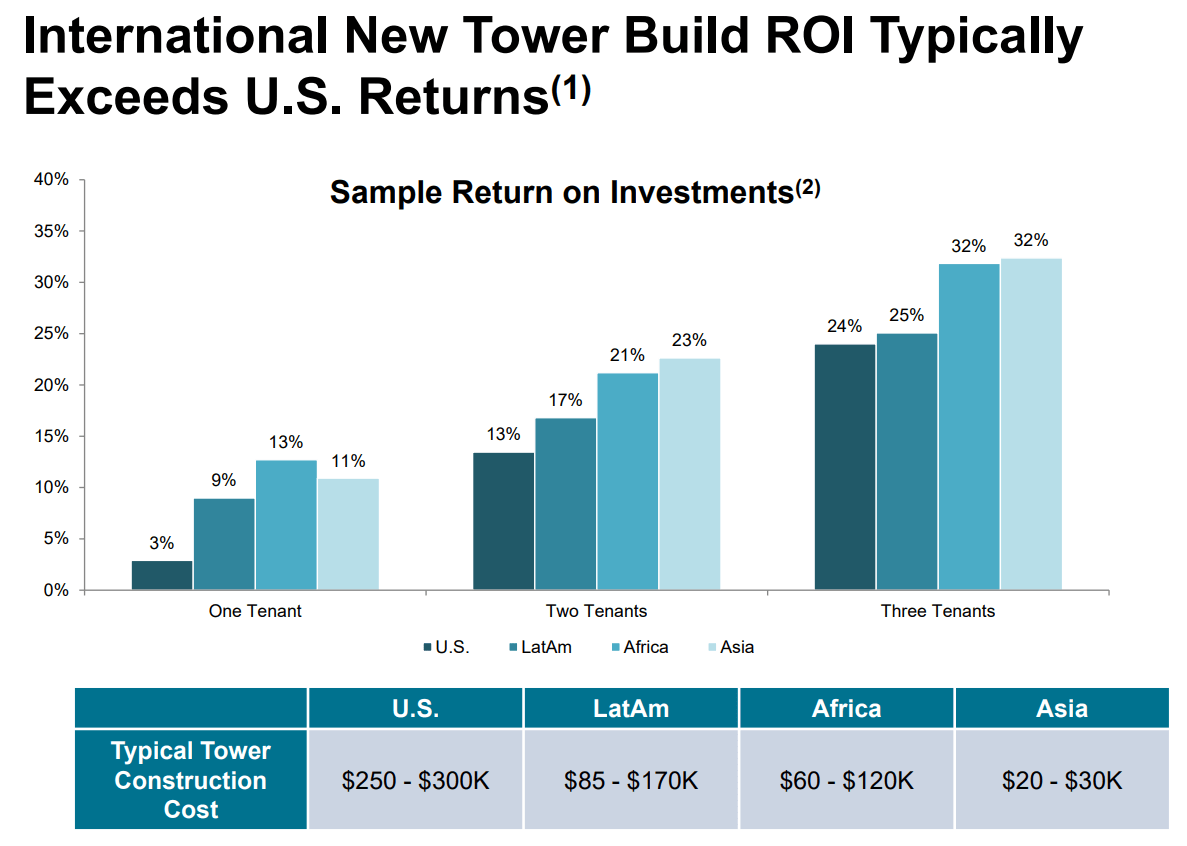

AMT illustrates internal rates of return (IRRs) in developing countries that are significantly better than US tower IRRs. Investors often argue that the US is the tower REITs best market due to zoning restrictions that make it difficult to build more towers, an effective power grid to provide energy, and the combination of many mobile operators who are willing tenants. But this graph, provided by the largest towerco in the US, clearly shows that the bottleneck in supply in the developed world, combined with cheaper construction costs, makes the US one of the worst places for a tower REIT from an IRR perspective, and yet AMT and SBA Communications Corporation (SBAC) have compounded capital excellently - returning a CAGR between 12% and 15% since inception.

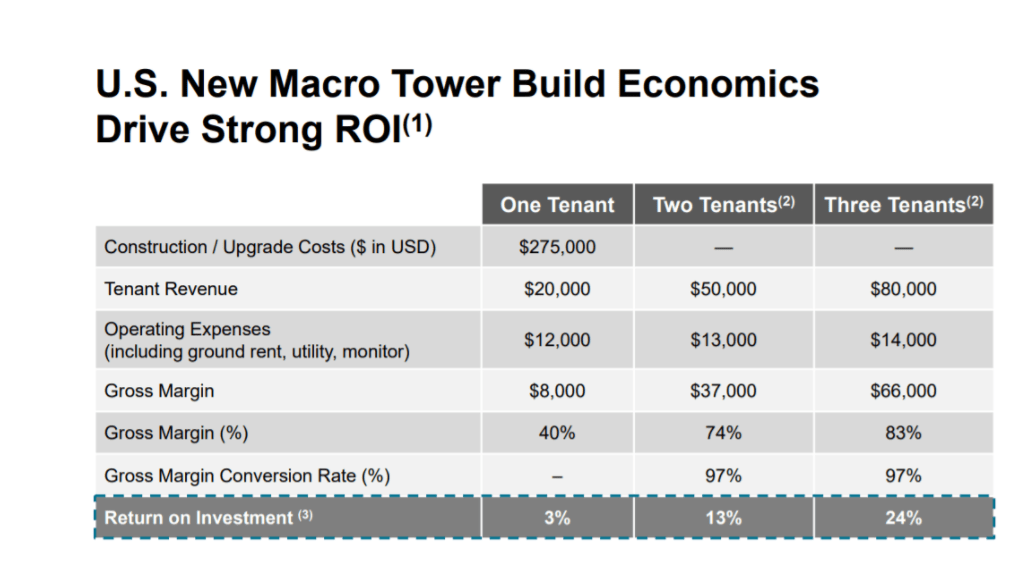

In every jurisdiction, increasing IRR comes from additional telcos tenants per tower . A tower operator builds a tower and then rents space for mobile network operators to send phone and data signals to a large geographic area covered by the tower. Thus, building the tower is a fixed cost, but renting to additional network operators is almost 100% gross margin. AMT illustrates the economics here:

{kind=link}

Returns given number of tenants in a Tower (AMTs Introduction to the Tower Industry Presentation)

By AMT's own admission, if you can get more than one tenant in a tower, towercos have excellent business economics. However in places like Africa and Latin America, even if you only have one tenant, economics are pretty good, however, a second or third tenant is gravy. Since IHS has a presence mainly in Africa, I will discuss the demographic tailwinds that make Africa such an attractive place for a towerco.

Demographic Tailwinds

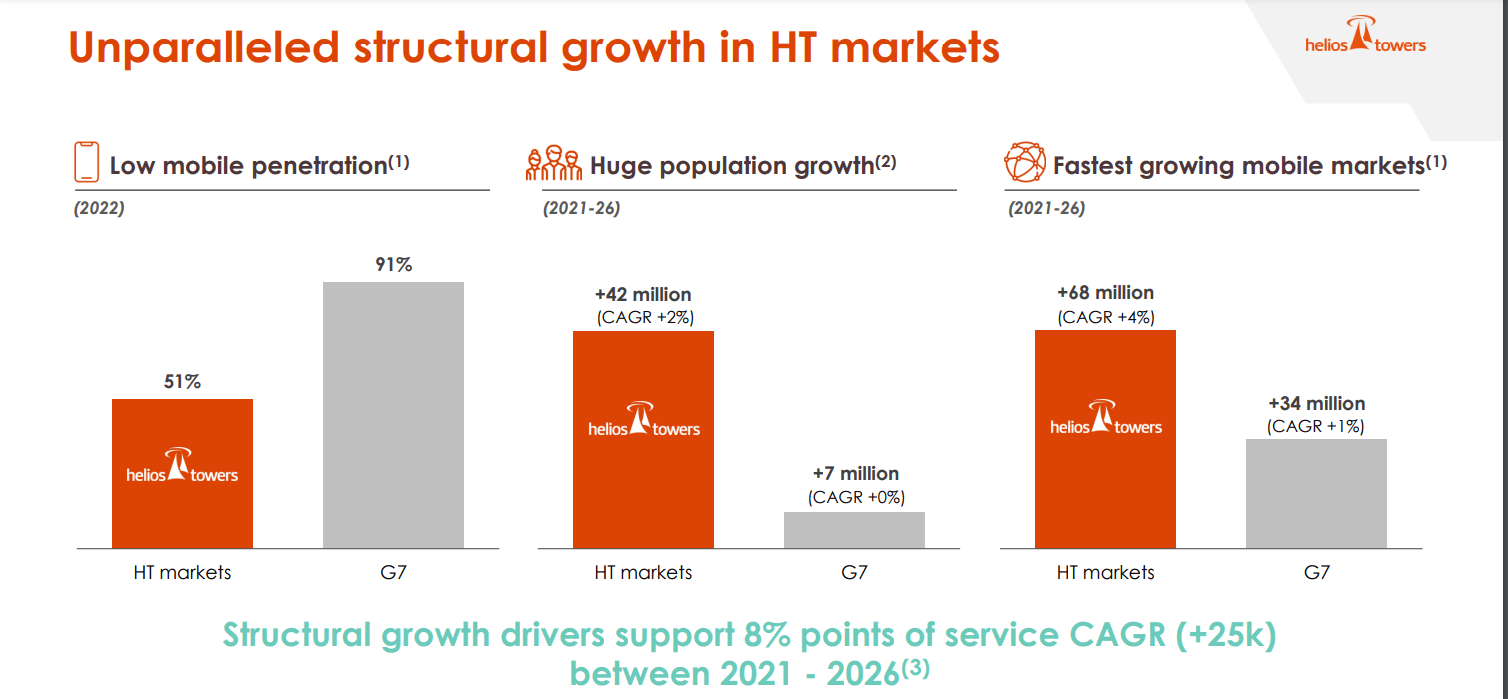

Demand for towers depends on the growth of mobile markets and the increasing wealth of a populace willing to pay for data. Here is competitor Helios Towers' ( OTCPK:HTWSF ) argument for the attractiveness of the African market :

{kind=link}

Helios Presentation of Attractiveness of Africa for Tower Operators (Helios FY 2022 presentation)

Compared to the Group of 7 (G7) developed countries, African countries have almost half the mobile penetration as G7. The population is slated to grow by 2% CAGR compared to stagnant growth in the G7. The combination of low mobile penetration and fast population growth leads to some of the fastest-growing mobile markets in the world.

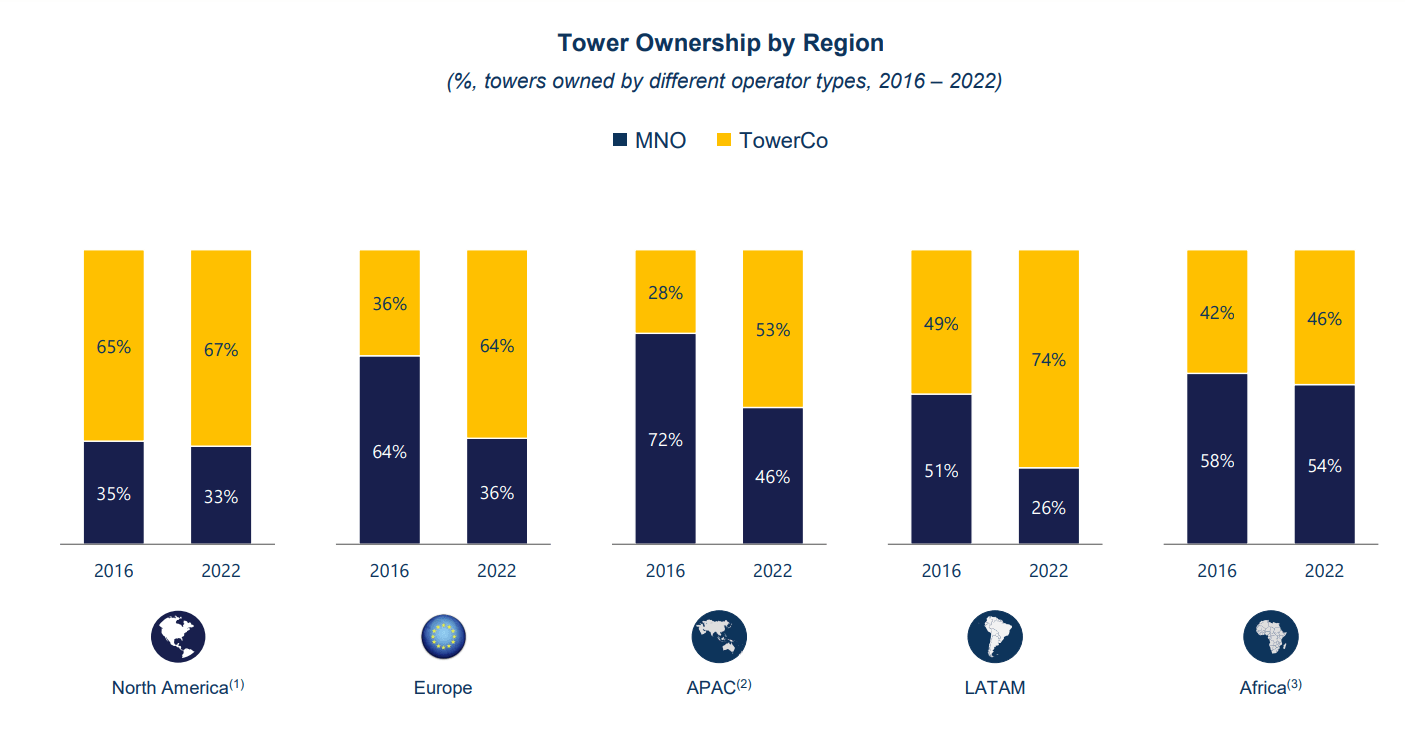

Towerco-owned towers also have an advantage over telco-owned towers. If a telco owns a tower, they are incentivized to stay as the sole tenant. Despite 100% gross margins when renting out space to competitors, the presence of another telco could lead to increased churn. Thus you will see situations of telcos building towers in areas where another is already present. Thus, tower operators have a competitive advantage in terms of profitability compared to telco-owned towers, as having a tower with additional tenants is more profitable than a single tenant. According to Ernst and Young : “A typical location of a wireless network operator (also point of presence) managed by a TowerCo is circa 40 percent more efficient than one managed by an [Mobile Network Operator](MNO)..." With this fact in mind, this is another area where towerco operators are uniquely positioned in Africa. According to the AMT's International Market Overview Q4 2022 :

{kind=link}

MNOs versus TowerCos in a given geography (AMTs International Market Overview Q4)

Mobile network operators (telcos) have the largest market share in terms of tower ownership in Africa. As mentioned above, this gives operators like IHS a pricing and profitability advantage over a larger number of incumbents than almost anywhere else in the world as IHS increases return on investment ((ROI)) by signing multiple tenants to a tower.

Although Africa has many advantages when it comes to tower operators, it also has some disadvantages. Due to the unreliable electric grid, most African towers need to use diesel generators. This means that maintenance costs per site are about $2000-7000 a year compared to $500 in Latin America and in the US. IHS is attempting to install solar and grid connections for many of their cell sites, a capital expense program they call Project Green. According to management, this will lead to an ROI of around 30%. The high cost makes the IRR less attractive, but these costs are baked into both AMT's and IHS's IRR numbers.

Business Quality

Next, I will more thoroughly discuss the quality of IHS' business. IRRs look attractive given AMT's presentation and supported by IHS' work as well. In addition, there are three important qualities I look for: 1) Low capital expenditures, 2) essential service at a price point that is small compared to customer expenses, and 3) Low churn.

Low capital expenditure is important because this makes the business less volatile on the cost side. Businesses with high capital expenditures and high cyclicality cannot plan for market downturns and commiserate high operating leverage. This is good when the market is growing, but difficult to manage over the whole cycle. If capex is low, even mediocre management can grow profitability. Latin American maintenance and capex costs are extremely low at $500 per tower which can generate $20000-80000 a year in revenue. The costs in Africa are much higher, however, Project Green should lower the total capex a significant amount. As the company invests in lower-cost tech and the African electrical grid develops, there is no reason why costs can’t trend down to Latin America maintenance and capex costs.

The second point is stickiness. The lower the overall cost and the higher the overall value a product delivers, the stickier it will be and the easier it is to raise prices. This is especially important in high-inflation jurisdictions like Nigeria. From the AMT presentation cited above, the average annual cost a telco pays for a tower is $25000. There are 307,000 cell towers in the US which suggest the average tower covers 1000 people. At a phone plan cost of $10 per month, the average revenue per tower is $100,000 per month or $1.2 million per year. A cost of $25000 is about 2% of total revenues. Furthermore, having wireless coverage is one of the most important services a telco needs to provide for people living in that area. If the telco stops paying for tower service, it will likely lose most of those 1000 customers.

This is also reinforced by the low churn number. The lower your churn, the easier it is to raise prices, as churn is evidence that the customer needs your service. Additionally, churn increases the lifetime value (LTV) of a customer in a hyperbolic manner. Going for 10% churn to 9% increases LTV by roughly 1x. Going from 3% churn to 2% churn increases LTV by 16x. This can be seen by comparing the fact that at 3% churn, a customer leaves every 33 years, but at 2% churn that number is every 50 years. Thus companies that have extremely low churn reap a significantly larger LTV. According to IHS Towers' annual report for 2021, churn averages around 2% annually. Among key accounts (i.e., large telcos) the churn is basically 0%. One benefit of this low churn is as IHS signs up more tenants, the tenant-to-tower ratio will improve as few are churning, leading to the economics of scale illustrated by AMT.

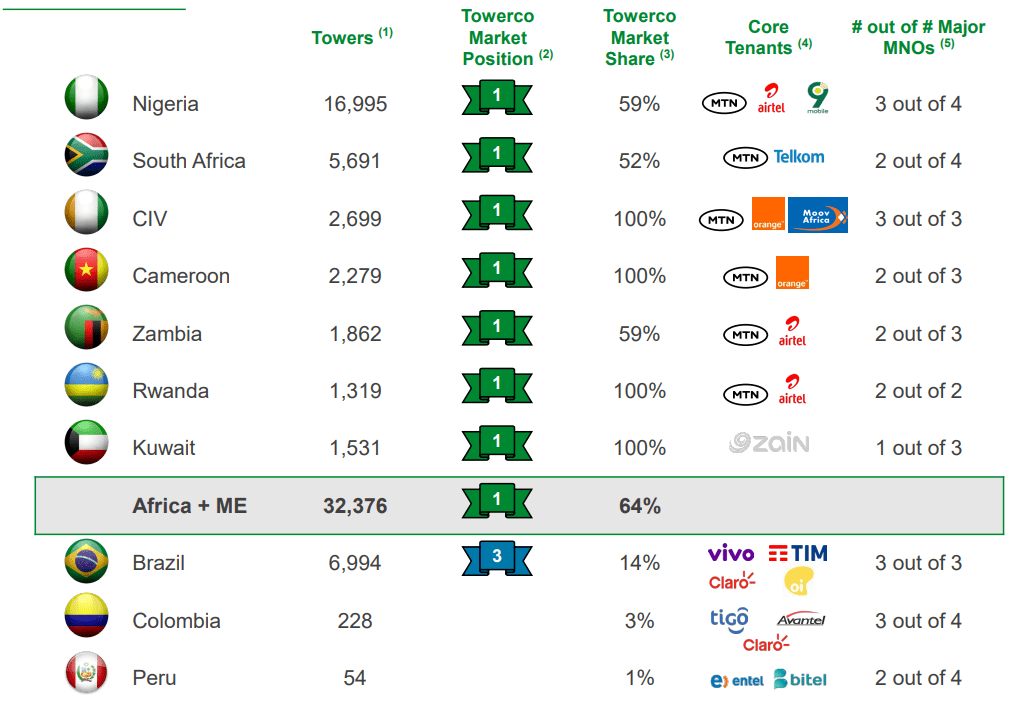

Despite having a smaller scale than the American tower companies, IHS is often the largest tower operator in a given country:

{kind=link}

IHS Market Share (IHS Q4 2022 Presentation)

IHS has the number 1 market share in all their Middle East and Africa locations, often with 100% towerco market share.

Runway for Growth

In Africa, according to the AMT Tower Industry Presentation, one can reach a 20% return on equity given a single tenant and moderate amounts of debt. This is important because IHS has 1.48x tenants per tower on average, which is lower than most other players. This means current ROIs will be lower than other players. However, this will likely improve over time as IHS' 2012 tower cohort now has a tenancy ratio of 2.24x, and the decrease in tenancy is based on their acquisition strategy. AMT has a 2.6x tenancy ratio and a 1.81x tenancy ratio for Helios. Given IHS' scale in the markets it operates in, its historical path to cohort growth, and its low churn, it is not hard to imagine that current towers will increase tenant ratio to 2x or higher.

Additionally, the growth in smartphone access and usage will require more tower infrastructure. According to IHS, while Africa has 170,000 towers, it will need 60,000 more to meet demand, which comes out to be $12 billion in capex which IHS, Helios, and other towercos are better positioned to build compared to legacy telco operators, for reasons discussed above. Assuming these capital expenditures have a 20% return on equity--which probably represents building a tower with little more than one tenant--this leads to a long runway of organic growth for towercos.

Valuation and Comps

After analyzing the business dynamics, I would like to examine valuation. Revenue for IHS has been compounding at almost 14% a year over the last 4 years, with last year's revenue growth, both organic and inorganic, at 24%. With Project Green and operating leverage, the bottom line should compound faster after the increased Project Green capex has been digested. Below is a table listing P/FFO and Net Debt/EBITDA:

| P/FFO |

| Debt/EBITDA |

| IHS |

| 7.5 |

| 4 |

| AMT |

| 20.7 |

| 5.5 |

| SBAC |

| 23.2 |

| 7.3 |

| Helios |

| 11.7 |

| 5.1 |

Sources IHS, AMT, SBAC, Helios Annual Reports and Tikr.com

Looking at all this together, IHS is the lowest leverage player with the lowest price to funds from operations. Even Helios, which is a smaller company with a main listing on the UK markets, has a higher valuation than IHS. IHS is better positioned than AMT and SBAC, by nature of its concentration in countries with higher IRRs than the United States so one could argue that IHS should have a higher multiple. However, it seems people like the familiarity and scale that the big towercos have.

Risks

The first risk is the developing country risk. There is a reason why the US is arguably the richest large country for the past 70 years, and also one of the best-performing markets even from that high water mark. Having good institutions and norms made us an economic superpower in the 1940s, and continues to provide tailwinds for our growth. However, it seems like enough developing countries like the BRICs and Asian Tigers have joined the West as developed nations, that many other countries--and more importantly their citizens--are more educated on the types of policies that will help them grow. Nigeria, a country responsible for almost 50% of IHS towers, had an oil-induced recession last year but grew at 1.4% over the past 4 years. These are not the groundbreaking numbers you see in China or, lately, India. However, they do suggest government policies are not solely rent-seeking but aiming at improving national wealth.

Inflation at 22% in Nigeria, is also a problem. However inflation has always been a problem, and it hasn't stopped IHS from compounding USD EBITDA at 17% a year for the last 5 years. 51% of IHS revenue is in Euro or USD. Additionally, most tenant contracts have quarterly forex resets. Low oil prices can become a problem for the Nigerian economy, however, since diesel fuel is required to power many of IHS' towers and telcos are unlikely to lapse on their leases, a decline in oil prices will likely be a net positive to IHS' bottom line.

A final risk is the advent of satellite-based data and telephony. At most, this is a long-term risk as a couple of thousand low earth orbit satellites don't have the bandwidth to connect the world's urban and suburban populace to each other and the internet. Additionally, satellite launches are still expensive--SpaceX's cost savings notwithstanding. At this point, satellites are only cost-competitive for rural and low-population-density locations. There are also issues with diffraction that come with propagating light waves through clouds and rain and latency issues with geosynchronous orbit satellites.

I would reconsider my investment in IHS if it looked like the IRRs for towers showed a pronounced decrease below my IRR hurdle rate of about 10%. If it seemed like new towers couldn't increase tenant ratios above 1.5, this would be cause for some concern. Additionally, if the stock price grows into a rich valuation perhaps around the levels of AMT and SBAC, I would be happy to sell.

Conclusion

The historical results of AMT and SBAC indicate that the towerco sector may be in the early innings in Africa. Using this information, it is likely that IHS will compound capital at high rates. Additionally, its position as the market leader in most of the countries it has a presence in, and the growth of demand in Africa suggests that IHS may compound capital faster than its American counterparts. If that's true then, IHS will likely compound capital in the mid-teens, well ahead of the market. As a company currently trading at a P/FCF of 7.5x—well below peers—IHS seems like a good long-term buy.

For further details see:

IHS Holding Limited: Buy, Forget, And Compound Capital