SBKFF - IIF: Reasons To Pursue And Reasons To Avoid

2023-12-05 06:27:46 ET

Summary

- The Morgan Stanley India Investment Fund is a well-established closed-end fund that has been around for almost 3 decades.

- IIF has a good track record of delivering returns and witnessing lower volatility over time.

- We touch upon why IIF may represent a good investment at this juncture.

- We close with a contrarian take on why it may be avoided.

CEF Snapshot

The Morgan Stanley India Investment Fund ( IIF ), a $290m sized closed-end fund ((CEF)), is one of the financial stalwarts in the industry, with a near 30-year trading history. This actively managed product focuses on 40-odd Indian stocks that are believed to exhibit growing price and earnings momentum in underpenetrated industries, and run by quality management.

Strong Performance Backed By Diminishing Volatility

One would think that Amay Hattangadi , the manager of the fund is well-placed to engage in primary research, and exhibit good judgment calls on the management quotient as he is based in India, and has been involved with this fund for 26 years now.

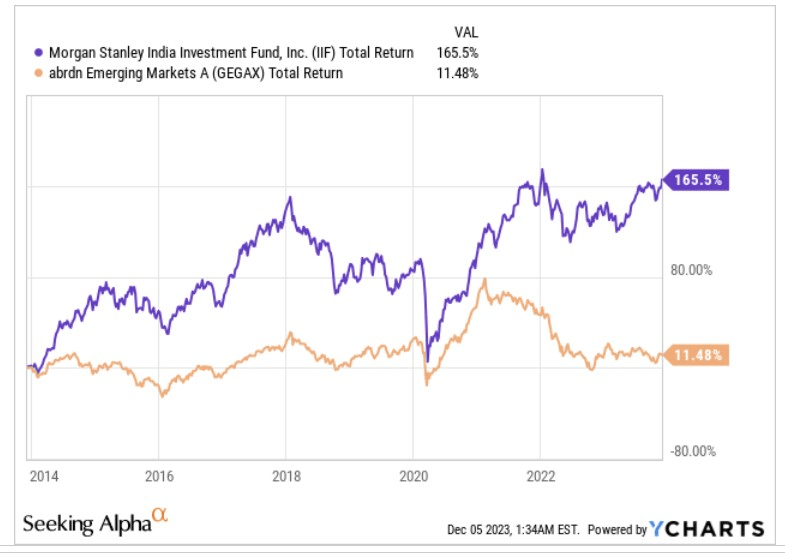

Regardless, it’s hard to argue with the results; for instance, if you look at the decade-long relative return differential of IIF and the abrdn Emerging Markets Fund A ( GEGAX ), the performance is quite stark. IIF has managed to deliver total returns of 165% at a time when GEGAX has just about managed to deliver double-digit returns.

{kind=link}

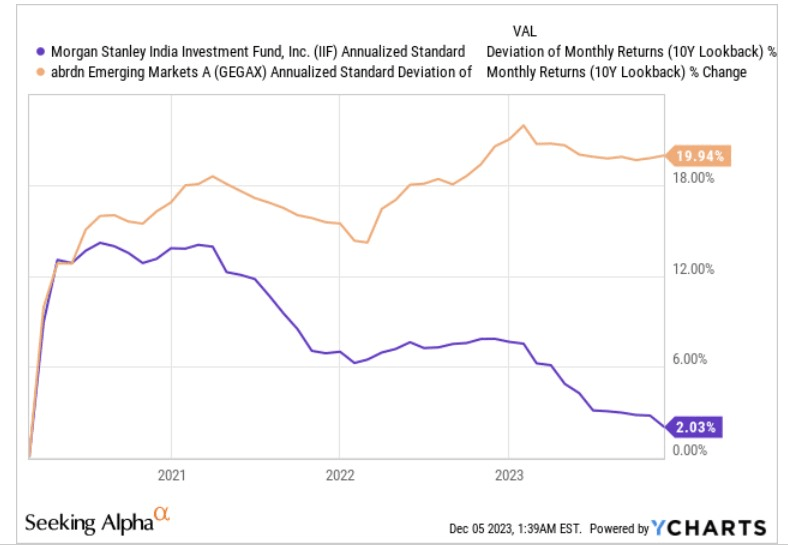

Besides the solid total return track record, you're also looking at a fund that has seen the variance of its monthly returns diminish over time. As things stand, the monthly standard deviation of returns (annualized) is at rather miserly levels of just 2%. Contrast that, with the diversified EM play whose volatility quotient has only grown over time, with the monthly standard deviation currently hovering around the 20% levels.

{kind=link}

Whilst IIF has done well so far, what about its outlook? Well on that front, we believe things are looking rather mixed. We’ll first summarize some of the tailwinds, followed by the headwinds.

Reasons to Pursue IIF

IIF has been rather generous with the pace at which it has been growing its annual dividends. Last year, one almost saw a 4x surge in the annual dividend, and despite a +15% growth in the market price this year, the yield still looks rather stunning at over 17%.

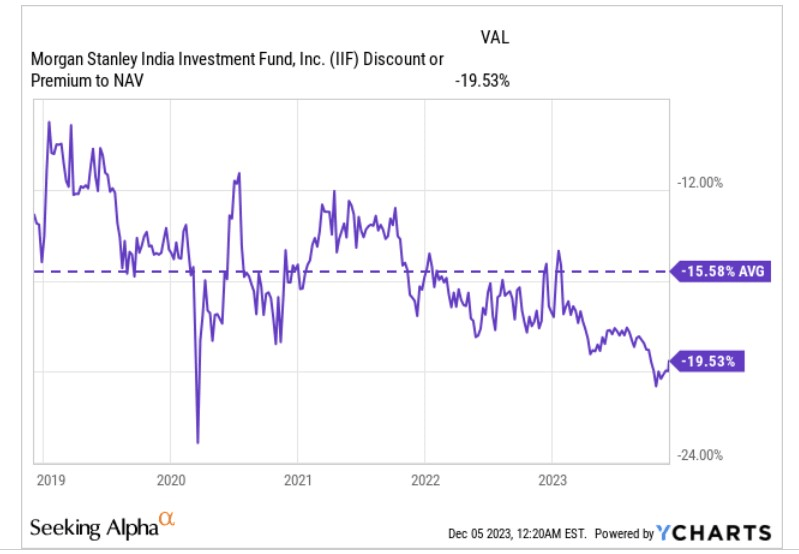

Then it's also well-known that CEFs typically tend to trade at a discount to the NAV, but currently one could say the discount is rather inordinate and could mean revert in the months ahead. Over the last 5 years, the average discount to NAV has worked out to over 15.5%, but right now that variance is a lot higher by around 400bps.

{kind=link}

What investors also need to note is that this is a product that tends to engage in healthy doses of buybacks every other month. As per the most recent data, we can see that it has been buying back a useful chunk of around 0.5% of the shares outstanding on a monthly basis.

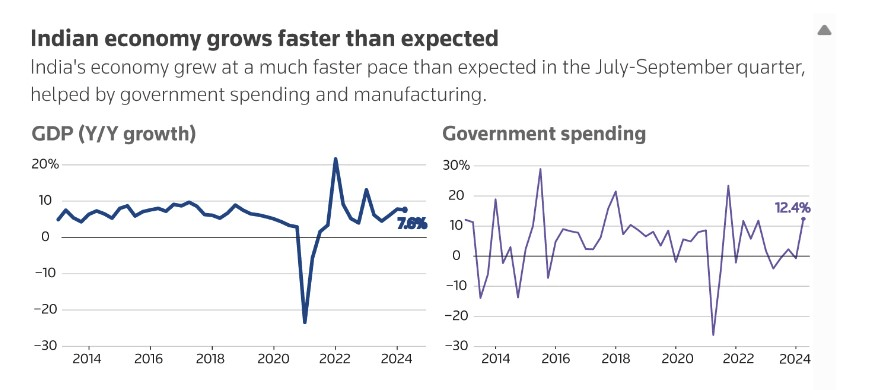

Then when it comes to the macros, India currently appears to be in fine fettle. In the September quarter, GDP growth came in at a resilient pace of 7.6%, comfortably beating street estimates of 6.8%. The IMF has already stated that India will be the fastest-growing economy in FY23, and it looks like that may be the case even in FY24 with the economy expected to deliver growth of 6.3% .

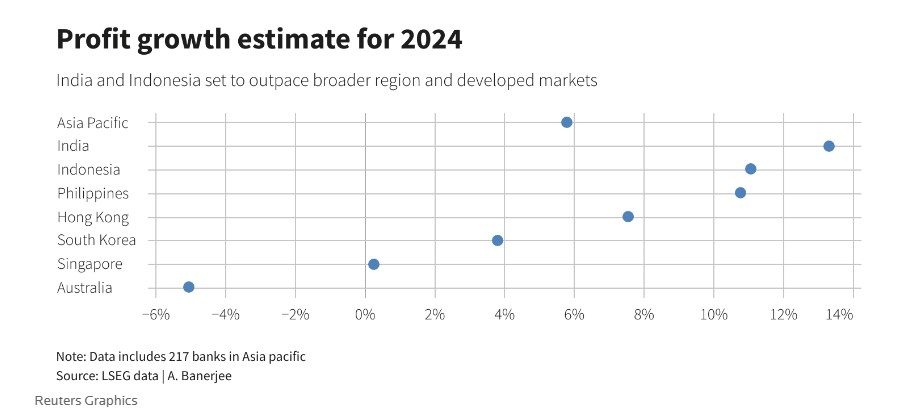

With a rather resilient growth runway, it pays to expose yourself to cyclical sectors such as financials which have typically benefitted from loan growth coming in at roughly 2x the pace of GDP growth. LSEG thinks that loan growth in India could be even more resilient next year and is currently budgeting for a 15% pace , around 500bps better than the expected pace for Asian banks as a whole. Meanwhile, a lot of Indian financials also benefit from ample low-cost deposits in their funding structure, and this could filter through to much better dynamics at the bottom line. Whilst Asia-Pacific banks are largely only expected to witness 6% profit growth in FY24, India banks could see a rate which is over 2x that figure at 13%.

{kind=link}

All in all, IIF looks well-poised to profit from these financial sector dynamics as close to half its portfolio consists of stocks from that sector alone.

Reasons to Avoid IIF

If you’re someone who attaches a lot of importance to the cost competitiveness of financial products, then this actively managed fund is probably not meant for you. Whilst most other Indian ETFs have expense ratios of less than 1%, this CEF’s net expense ratio is rather elevated at 1.32%, driven primarily by a steep management fee of 1.1%.

Then India’s growth story may well be trouncing the rest of the world, but if one were to focus on the country’s own high growth standards, it is questionable if the momentum will linger in the second half of the fiscal year (India follows a March year ending calendar). After delivering 7.7% real GDP growth in H1-24 (April 23 -Sep 2023), the FY expectation is for a slower pace of 6.7%-7%. Put another way, growth in H2 (Oct 23- March 24) now looks set to come in at a lower threshold of 5.7%-6.3%.

One of the reasons why growth has been so strong in H1, is because of strong impetus by the ruling government in front-loading its CAPEX initiatives. Government spending was particularly robust in Q2, growing by 12%, but with almost 80% of the budgeted CAPEX already likely used up, it’s reasonable to expect momentum to ebb.

{kind=link}

The other thing to note is that India goes to the polls next year, and thus the government’s focus will understandably tilt towards election-driven initiatives. In an election year, we've also previously seen that equities tend to see a spike in volatility which is not ideal.

Whilst Indian banks may be well-positioned to facilitate another year of strong credit growth and profits, one should also question if one will receive great bang for the buck at these valuation levels when there are cheaper opportunities elsewhere. MSCI’s all-country Asia banks index currently only trades at a multiple that is less than book value (P/BV of 0.9x ). However if one looks at the top financial stocks of IIF- ICICI Bank ( IBN ), Axis Bank, Bajaj Finance, and SBI ( OTCPK:SBKFF ), all of whom take up a sizeable chunk of the top 10, the valuations are off the charts.

Reuters, Moneycontrol

Leave aside the banks, even if you want to take a broader view and look at IIF's entire portfolio, it's hard to feel too excited about the rate at which this product is currently priced. Morningstar data shows that IIF is priced at a little less than 20x. In contrast, a diversified EM CEF can be picked up at a much lower multiple of 13x .

{kind=link}

Finally, it also looks like those fishing for suitable rotational opportunities in the EM space, are unlikely to gravitate to Indian stocks, as the current relative strength ratio of Indian equities to EM equities is not far from hitting record highs. Towards the end of last year, and a few months back, we’ve seen this ratio recoil from similar levels, so don’t be surprised to see this pan out yet again.

For further details see:

IIF: Reasons To Pursue, And Reasons To Avoid