ITW - Illinois Tool Works: A Dividend King Worth Buying

Summary

- In this article, we discuss one of the few dividend kings with more than 50 consecutive years of dividend hikes.

- Despite its age and status, Illinois Tool Works has an impressive dividend scorecard thanks to a good yield, high dividend growth, and satisfying dividend safety.

- The company is seeing rebounding growth thanks to fading supply chain issues and industry tailwinds. However, dark economic clouds are emerging, causing me to believe that buying on weakness is warranted.

Introduction

I haven't discussed Illinois Tool Works ( ITW ) since August of last year, which means it's time to dive into this dividend gem. In this article, we'll discuss several things. We'll start by diving into the company's ability to deliver consistent shareholder value through its dividends. While the company is a rather slow-growing industrial giant, it has an almost perfect dividend scorecard and a rare dividend king status. Unfortunately for potential investors, current investors have recognized the company's added value, pushing the stock price to a range that comes with a somewhat subdued risk/reward, given the tremendous pressure on the industrial sector. Hence, we'll also discuss how I would deal with this tricky situation, as I'm quite eager to add the ITW to my dividend growth portfolio or some of the portfolios I indirectly manage/advise.

So, let's dive into the details!

Royal Dividends

The definition of a dividend king is a company that has raised its dividend for at least 50 consecutive years. That's a tough thing to do, as it means a few things:

- A company needs to be able to pay a dividend in the first place. Meaning it needs to be profitable.

- That company needs to be profitable on a long-term basis and maintain strong capital discipline.

- It needs to consistently grow its net income and free cash flow to pay a steadily rising dividend.

These things sound straightforward. While that might be true, achieving these things on a long-term basis is very hard. In the US only 41 stocks are officially in the dividend king category.

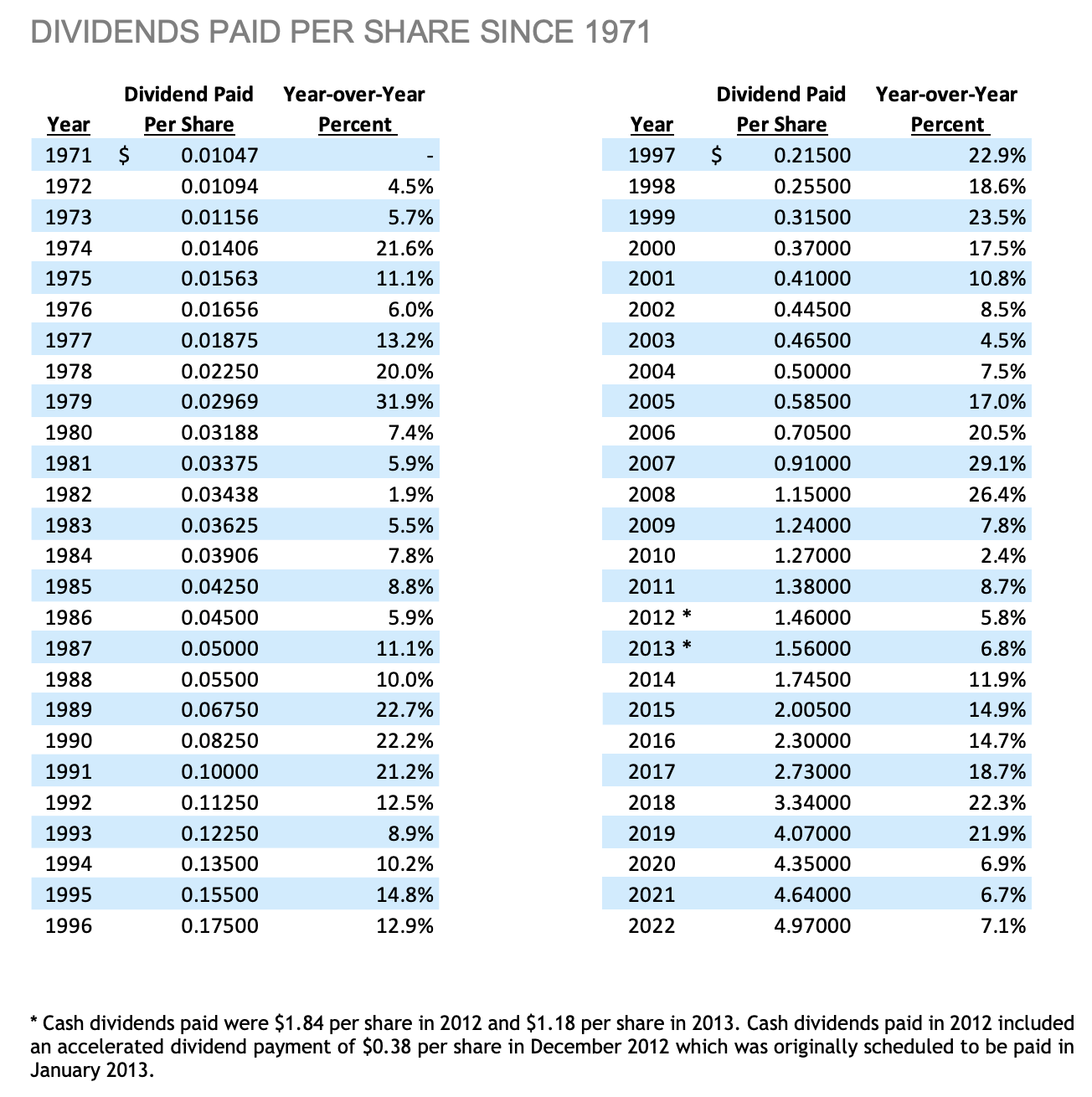

This Glenview, Illinois-based company became a dividend aristocrat before the start of the 21st century. In 1971, it started with an adjusted dividend per share of $0.01047, which has grown to almost $5 in 2022. This means that the company is now a dividend king, as the 2022 hike of 7.1% marked the 50th consecutive dividend hike.

{kind=link}

Also, as you may have noticed in the table above, the company's growth rates are everything but slow. Even after becoming a dividend aristocrat, the company's investors consistently enjoyed double-digit hikes.

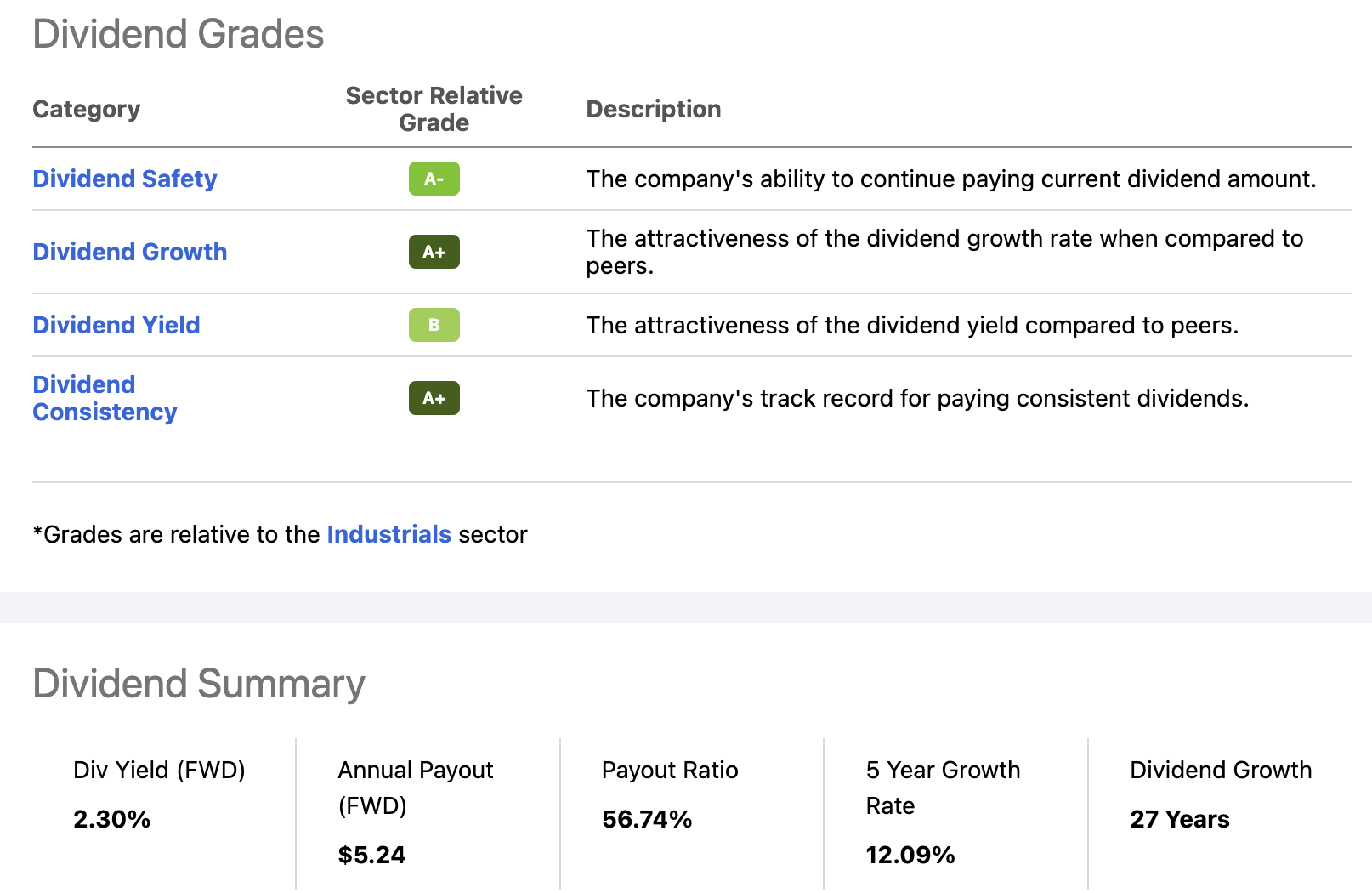

Using the Seeking Alpha dividend scorecard, we see that it is scoring extremely high compared to its industrial sector peers. The company scores very high on consistency (no surprise there), high on dividend safety, and relatively high on its dividend yield. Moreover, the company gets a top score for dividend growth, which is very unusual when also scoring high on dividend consistency. After all, consistent growers like aristocrats and kings are mature companies with, more often than not, subdued growth rates. However, before we continue, I need to address that the dividend growth number in the overview below (in years) is wrong. The data used includes a dividend decline in 1995. That is not the case, as the company's data shows. I believe there might have been a mistake due to a spin-off or stock split or something with a similar impact on dividends.

{kind=link}

With that said, the company is currently yielding 2.3%, which is based on a $1.31 per share per quarter dividend. This yield is close to the longer-term median.

The five-year average annual dividend growth rate is 12.1%. The payout ratio is 57%. Both are terrific numbers.

These are the most recent hikes (please note that the ITW table above shows average hikes per year, which explains the difference):

- September 2022: +7.4%

- August 2021: +7.0%

- August 2020: +6.5%

What we see here is that dividend growth has slowed, yet it is still at very acceptable levels.

This was caused by pressure on ITW due to post-pandemic issues like supply chain issues, which brings me to the next part of this article.

ITW Has Slow But Consistent Growth

When we talk about dividends, it's always key to assess the fundamentals that drive dividend growth: free cash flow and net income. In this case, I mainly care about free cash flow as it's hard to manipulate and it excludes capital investments.

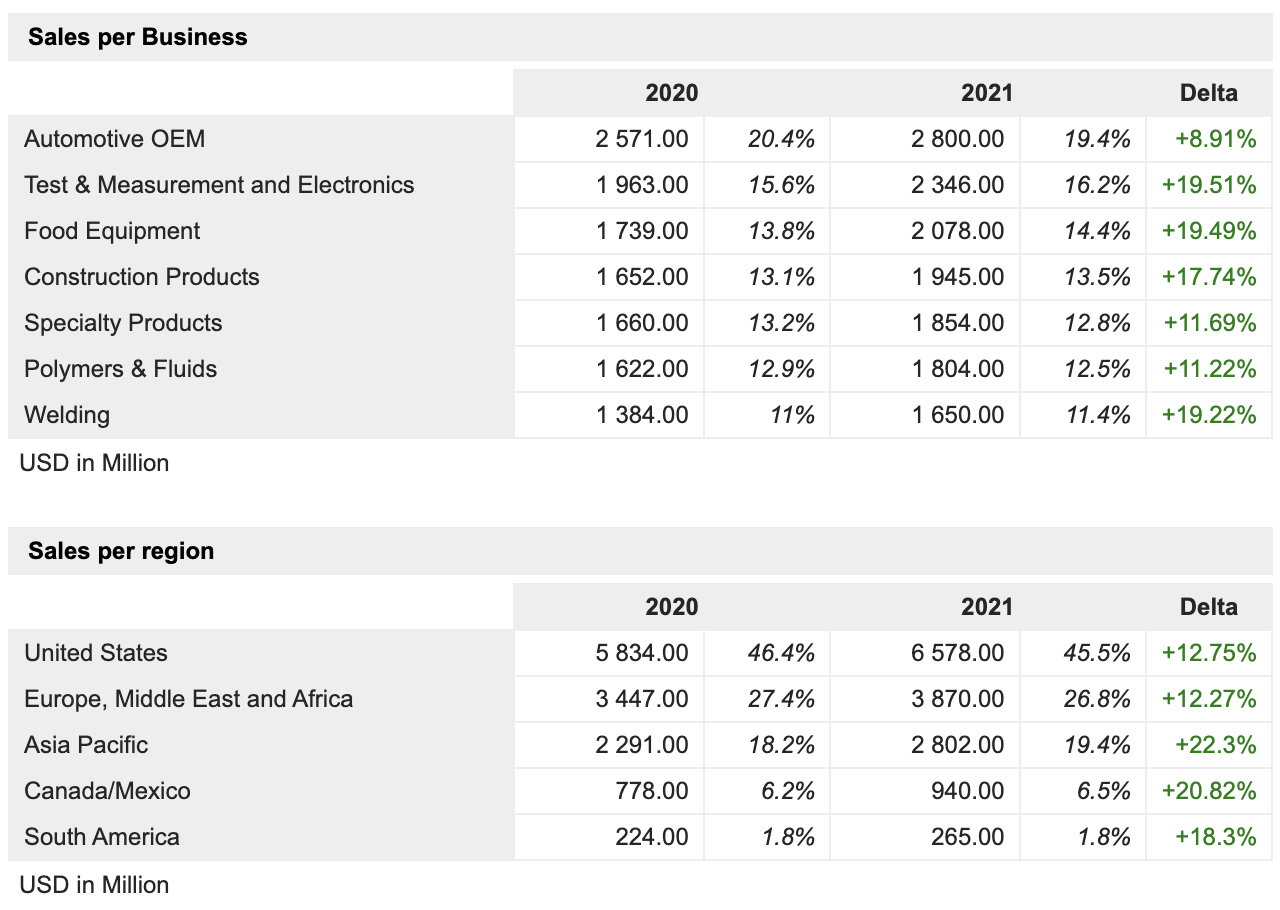

ITW was founded in 1912. Now, the company is an industrial conglomerate built around a differentiated and propriety business model, leading in seven industry segments. The company has high exposure in the automotive industry. It sells test & measurement and electronics, food equipment, construction products, and a wide range of tools used in various industrial processes.

{kind=link}

The company maintains a business model that is focused on value creation and customer relationships. Its 80/20 Front-to-Back process means that ITW focuses on the best 80% of business opportunities, cutting costs and complexity in the least promising 20% of endeavors. This allows the company to remain innovative without becoming a company with too much dead weight.

Moreover, the company innovates together with its 80% most important customers. This allows for accelerated innovation as it addresses customer needs directly. It also (indirectly) uses customer R&D capabilities and best practices.

One of the problems is that the company isn't growing rapidly. As the charts below show, a large number of industrial segments have shown little to no growth over the past 25ish years.

Federal Reserve

The same can be said about ITW's business. At least about the company's top line.

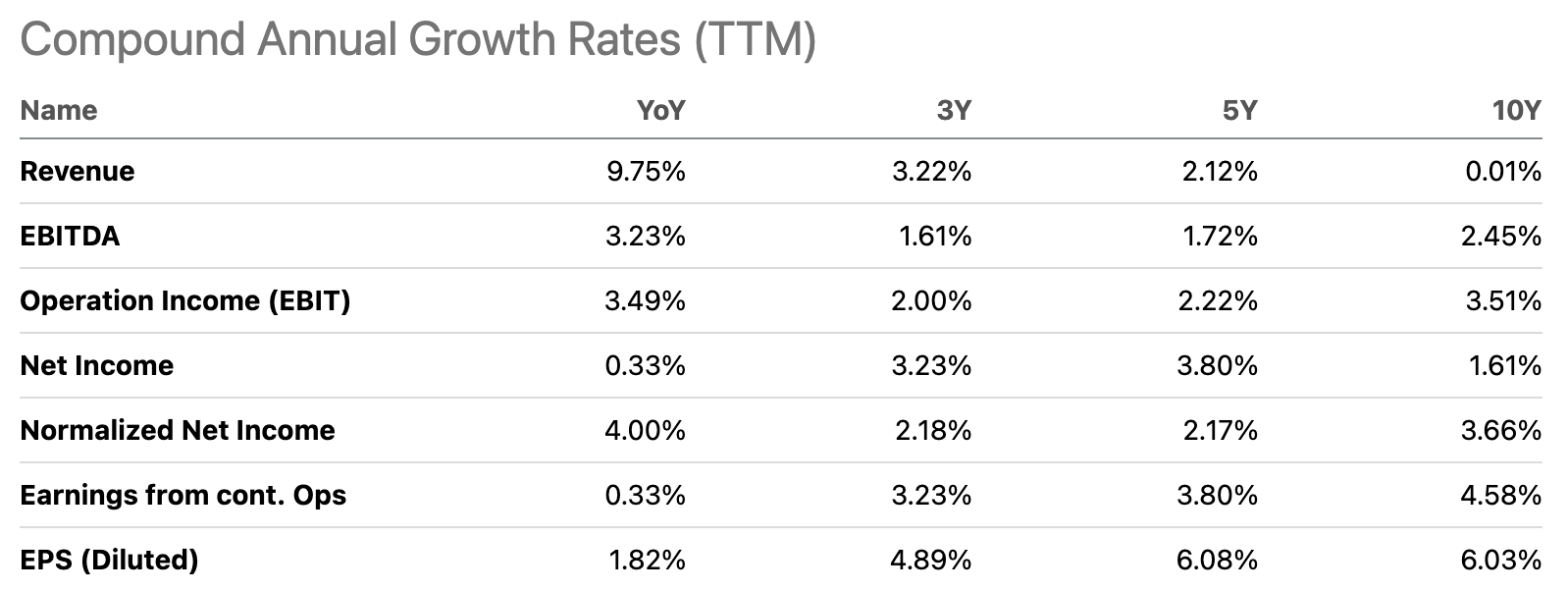

Using Seeking Alpha data, we see that revenue growth over the past ten years was 0.01% per year. That's not a lot. EBITDA growth was 2.5% per year. This beats the Fed's 2% inflation target. Yet, that's about it. Net income rose by 1.6% per year. Earnings per share rose by 6%. The difference is caused by buybacks. Between 2017 and 2021 alone, ITW bought back roughly 30 million shares, which translates to an 8% decline.

{kind=link}

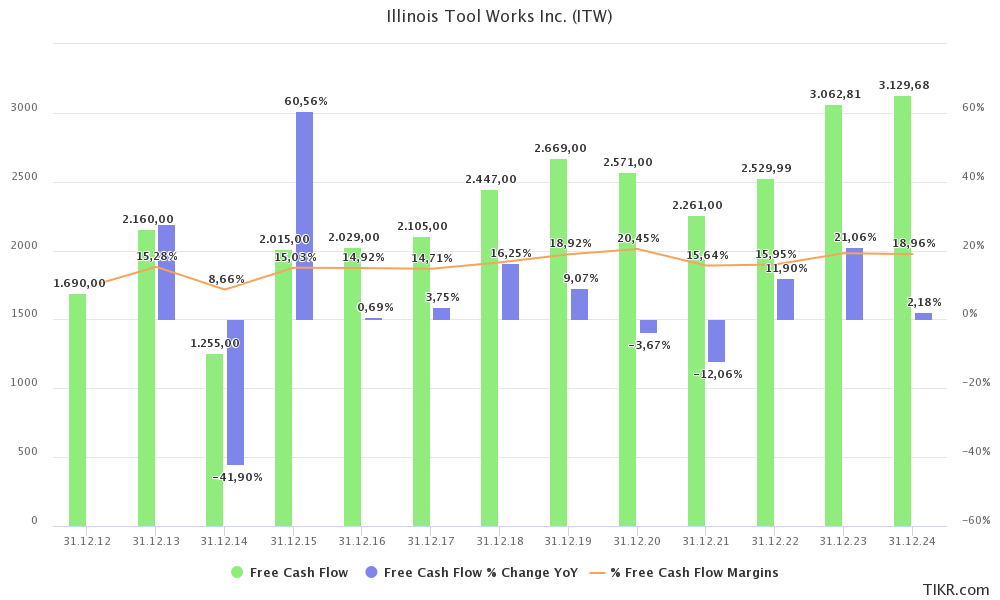

Even more important is that the company has done a tremendous job growing free cash flow. In 2012, the company had a free cash flow margin of 9.4.

{kind=link}

Speaking of 3Q22, in that quarter, the company had double-digit organic growth in all geographic regions. The company reported 16% organic revenue growth, boosting EPS growth by 16% despite currency headwinds (the strong dollar).

According to the company :

While we did see some softening in channel inventory reduction actions in our businesses serving the construction, auto aftermarket, commercial welding and appliance markets, five of our seven segments delivered double-digit organic growth, led by automotive OEM, up 25% and food equipment, up 23%.

Moreover, the company was positive that fading supply chains and a (related) return of higher automotive production might contribute to higher growth down the road.

[...] as supply chain issues eventually get resolved down the road, we remain confident that the automotive OEM segment is well positioned to be a very meaningful contributor to the overall organic growth rate of the enterprise for an extended period of time. And as that plays out, we also expect that the automotive OEM segment returns to its typical historical operating margin rates in the low to mid-20s.

The result is that ITW is expected to maintain positive free cash flow and EBITDA growth in 2022 (only one quarter remaining), 2023, and 2024.

- 2022: FCF +11.9%, EBITDA +7.2%

- 2023: FCF +21.1%, EBITDA +3.3%

- 2024: FCF +2.2%, EBITDA +6.2%

It also needs to be said that if the company can grow FCF to $3.1 billion in 2023. That would translate to a 4.4% FCF yield. This is another indication that the dividend is safe and supportive of longer-term growth.

So, what about the valuation?

Valuation

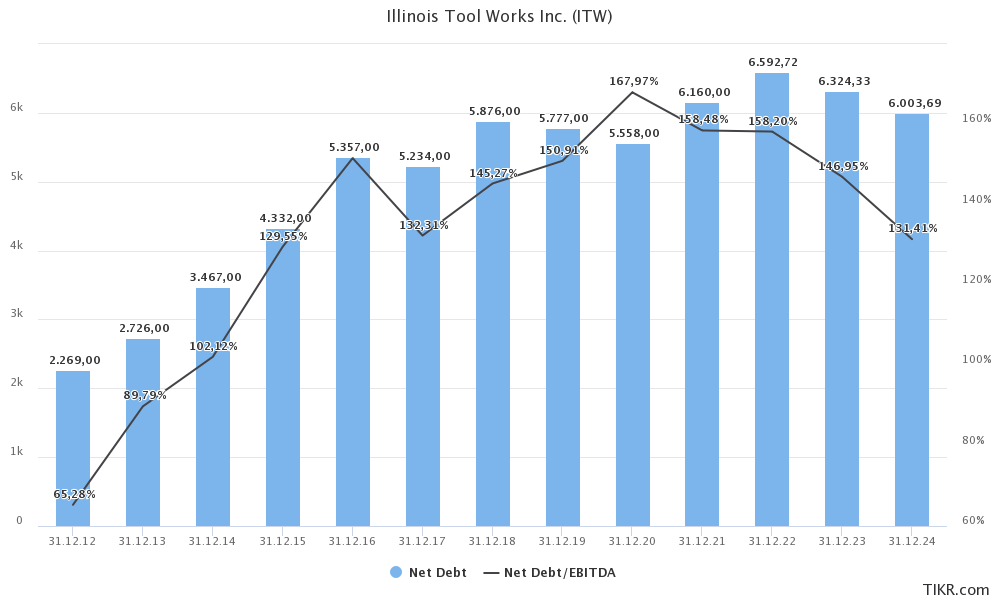

Illinois Tool Works has a very low debt load. This year, the company is expected to end up with $6.6 billion in net debt. That is more than it had in 2021, yet just 1.6x EBITDA. Next year, that number is expected to be below 1.5x EBITDA. The company's balance sheet has an A+ rating.

{kind=link}

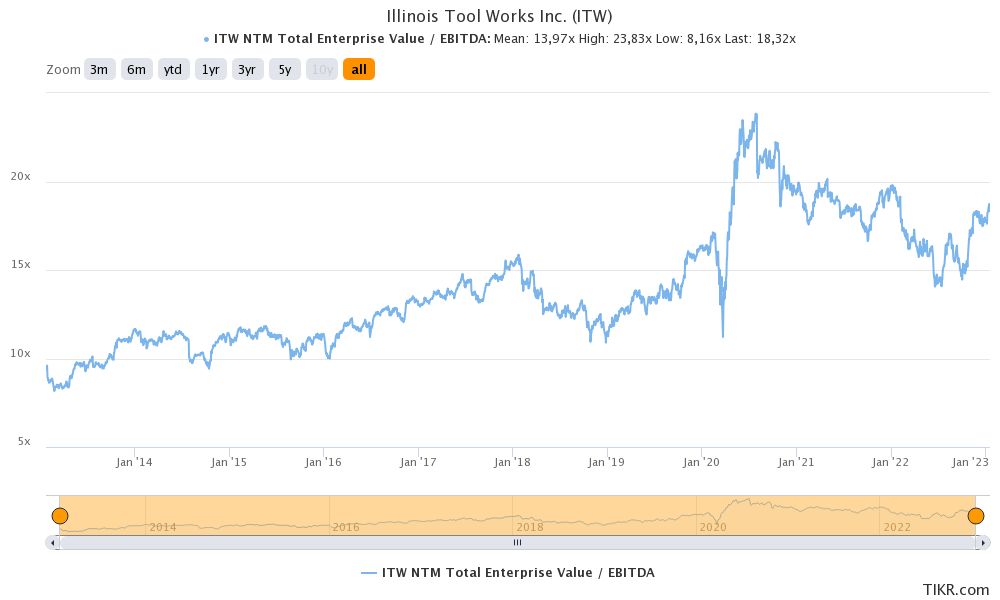

When adding $6.3 billion 2023E net debt to the company's $70.0 billion market cap, we get an enterprise value of $76.3 billion. That's 17.7x 2023E EBITDA of $4.3 billion.

That is a lofty valuation, and while I agree that ITW benefits from easing supply chain problems and a high automotive industry backlog, I do not like a forward EBITDA multiple this high in light of ongoing economic challenges.

{kind=link}

As I said in my prior article, I believe that ITW is a good buy close to $190. At that point, investors would be buying a dividend yield close to 2.8%, which does sweeten the risk/reward as well.

FINVIZ

With all of this in mind, here's my takeaway.

Takeaway

Illinois Tool Works is a fascinating company. The company is a dividend king with an impressive dividend scorecard. ITW has a satisfying dividend growth rate, a decent yield, and a business model providing stable free cash flow growth.

The only problem is the risk/reward. Thanks to its qualities, the company has done well, benefiting from the rotation from growth to value. Now, the company is seeing fading supply chain issues and related benefits while economic indicators are slowing.

Given the bigger picture, I believe that entries close to $190 per share offer a great risk/reward.

(Dis)agree? Let me know in the comments!

For further details see:

Illinois Tool Works: A Dividend King Worth Buying