ITW - Illinois Tool Works: Still Not A Bargain

2023-09-18 07:02:55 ET

Summary

- Illinois Tool Works could not really grow its top line in the last ten years, but management could improve margins and use share buybacks to grow its bottom line.

- According to its Enterprise Strategy, management is expecting earnings per share to continue growing.

- We could make the case of ITW being slightly undervalued, but, in my opinion, it is not a great investment right now.

In my last article , I called Illinois Tool Works Inc. (ITW) and expensive dividend king. However, my last article was written more than 1.5 years ago. And although I would describe myself as long-term investors who does not pay much attention to information that might impact a stock in the short-term, an update after such a long time seems justified - even for potential "Buy and hold forever" stocks.

In the following article I will provide an update on Illinois Tools Works and try to answer the question if the business can continue the successful strategy of the last decade - leading to bottom line growth especially by share buybacks and improving margins. And we will update our intrinsic value calculation to determine if Illinois Tool Works is a good investment at this point or not.

How Did The Company Grow?

When looking at Illinois Tool Works, we see a great stock performance in the last ten years with Illinois Tools Works outperforming the S&P 500 ( SPY ).

In the last few quarters, Illinois Tool Works could grow its top line again, but when looking at the previous years the company was clearly struggling to grow its top line. And considering the struggles to grow the top line, the stock outperformance seems rather surprising.

Running up to the revenue peak in 2009, the company could grow its top line with the CAGR of 11.74% in the two decades leading to that peak and double-digit revenue growth rates for two decades are clearly impressive. However, in the years following 2009 the company started to struggle and could not grow its top line anymore and almost 15 years later, Illinois Tool Works is still reporting a revenue below its all-time high.

While revenue could not really grow in the last 15 years, earnings per share are showing a different picture. Earnings per share are growing with a high pace for several decades in a row and in the last ten years, Illinois Tool Works could grow earnings per share with a CAGR of 4.89%. And since 2009, revenue declined 9.5% in total while earnings per share increased 247% in the same timeframe.

When asking the question how Illinois Tool Works could grow its earnings per share with such a high pace, we can look at the company's expenses - or when looking at it from a different point of view: the company's margins. We see margins improving - and this improvement especially happened in the years after 2010. Gross margin improved from about 32% around 2010 to about 42% right now. And operating margin increased from a low of 10% in the quarters following the Great Financial Crisis to an operating margin of 24.5% right now.

Aside from improving margins, which contributed to bottom line growth in an impressive way, the company also used share buybacks to improve the bottom line. A little more than 15 years ago the company started buying back shares and these share-repurchases contributed to bottom line growth. Between 2008 and 2023, the company decreased the number of outstanding shares from 521 million to 304 million - resulting in a CAGR of 3.5% in the last 15 years.

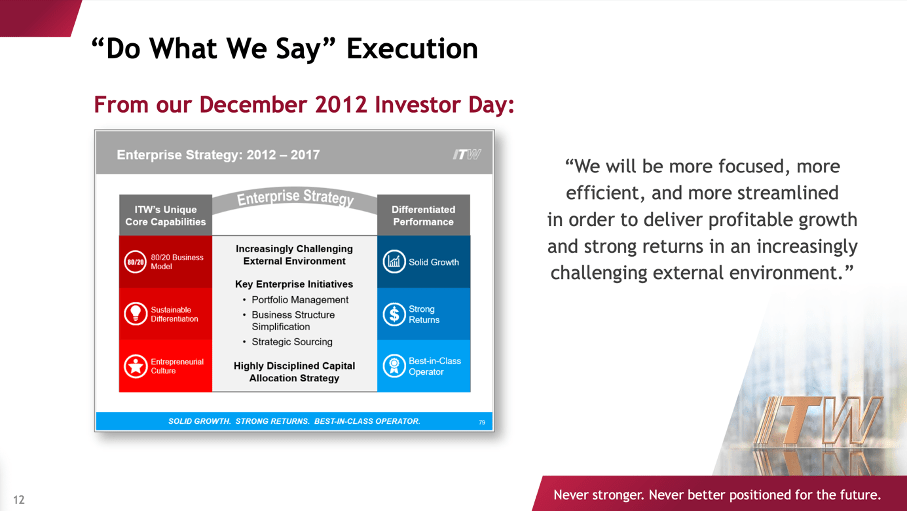

Management is attributing a big part of this growth to the enterprise strategy started in 2012. During the 2012 Investor Day, Illinois Tool Works promised investors to be more focused, more efficient, and more streamlined.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

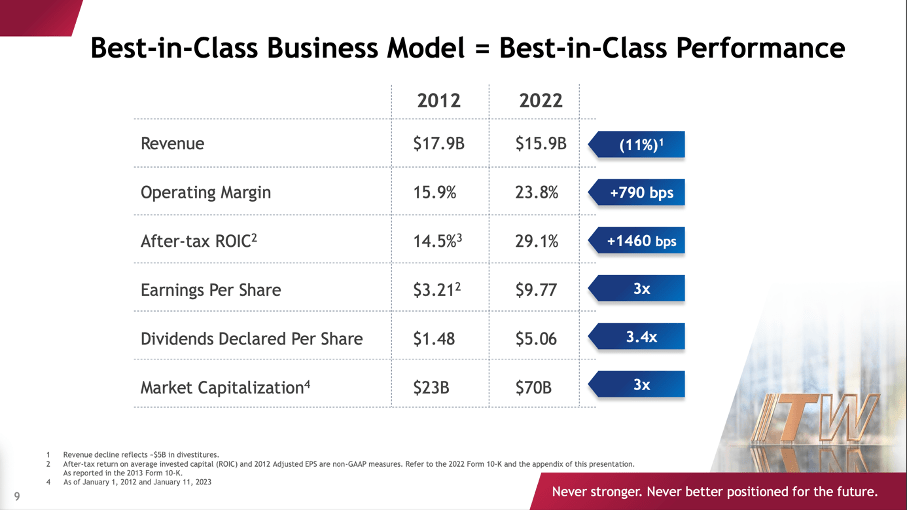

And as we can see the strategy was working although revenue between 2012 and 2022 declined about 11%. Earnings per share could increase 3x, operating margin improved 790bps and dividends per share could also be increased 3.4x during that timeframe.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

What About The Future?

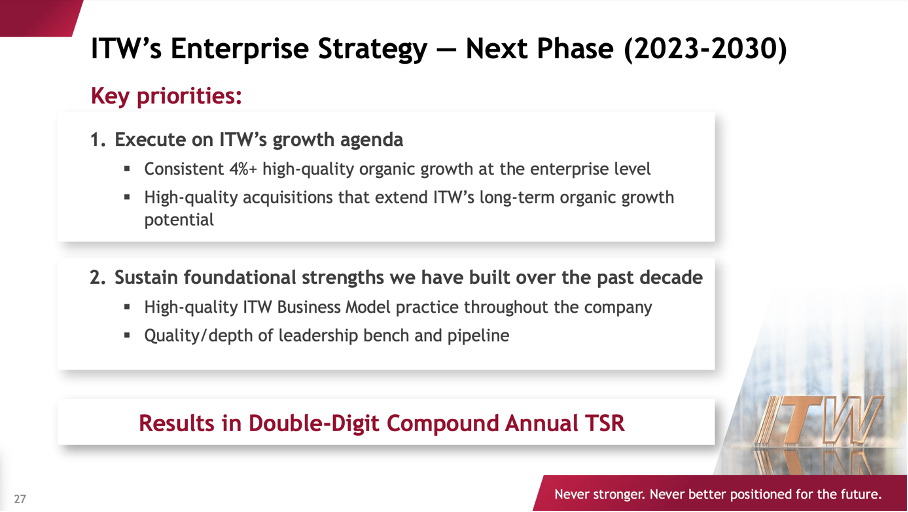

I am a big advocate of looking at past data and learning from history, but of course I can't ignore (or deny) that investing is about the future. And at this point we looked enough at past data and should focus on the expected future performance of Illinois Tool works. During the 2022 Investor Day, management presented its enterprise strategy for the next phase - the years between 2023 and 2030.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

For starters, we can assume Illinois Tool Works to continue share buybacks in the years to come. Although the balance sheet is not perfect, spending a certain amount of the generated free cash flow on share repurchases should not be a problem. On June 30, 2023, Illinois Tool Works had $1,275 million in short-term debt as well as $6,947 million in long-term debt. Compared to a total stockholder's equity of $3,094 million we get a debt-equity ratio of 2.66 - a rather high metric. However, when comparing the total debt to the operating income of the last four quarters it would take a little over two years to repay the outstanding debt - and this is acceptable. We can also mention $922 million in cash and cash equivalents on the balance sheet.

Another interesting question is if Illinois Tool Works can continue to improve its operating margin. In theory, higher margins are certainly possible and when only looking at the S&P 500, we currently see 140 companies with a higher operating margin than Illinois Tool Works (and when only looking at the "Industrials" segment we can still find 14 companies with a higher operating margin listed in the S&P 500).

{kind=link}

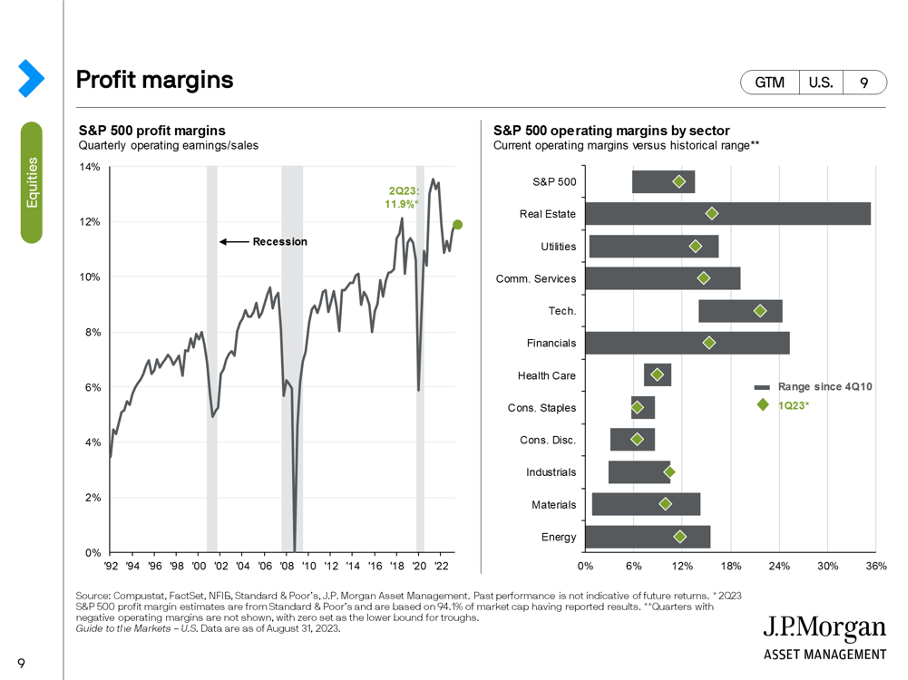

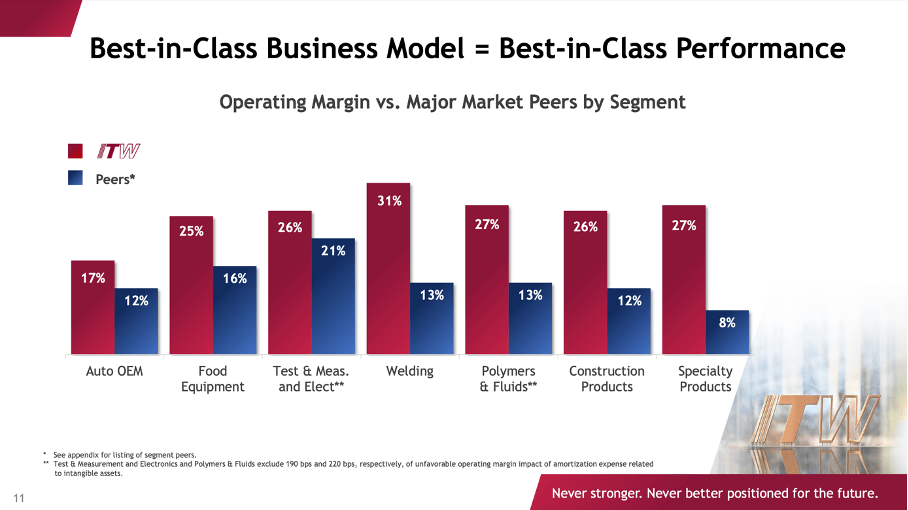

And when looking at profit margins since the early 1990s , we see constantly higher profit margins over time (only interrupted by the different recessions) and hence we can make the argument that Illinois Tools Works might also be able to improve its margins further (following that long-term trend). And management is optimistic that higher margins will contribute to growth in the years till 2030. On the other hand, Illinois Tool Works is already reporting much higher margins than its peers in every business segment - in some cases twice as high - and we must ask the question how much more room for improvement there is.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

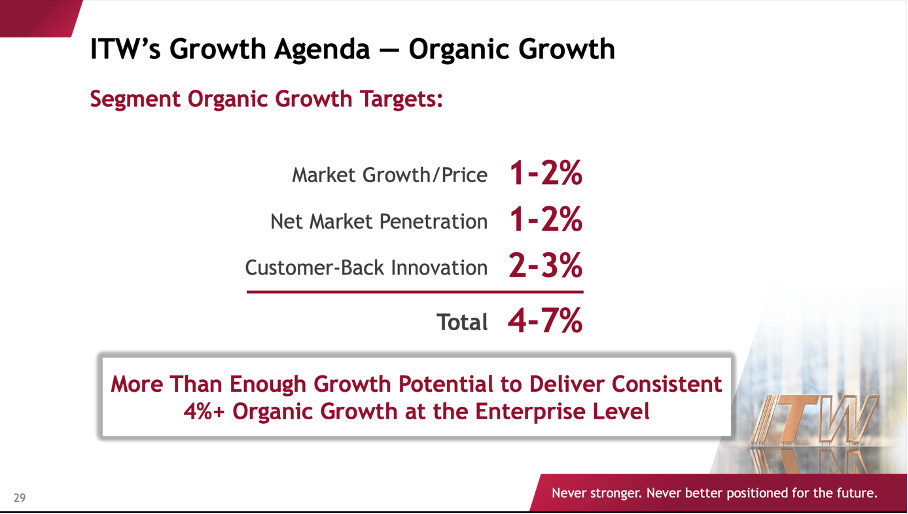

And one of the targets mentioned above for the next phase is 4% organic growth as well as acquisitions to drive the top line. And management is having several organic growth targets - including a growing market (being able to charge a higher price) or net market penetration.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

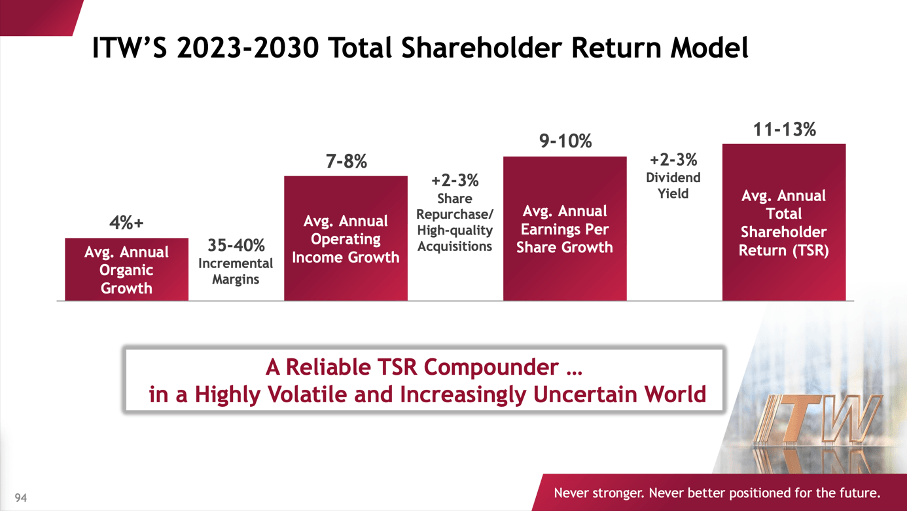

When summing up, Illinois Tool Works is expecting at least 4% organic growth and combined with higher margins and share buybacks (or acquisitions), the company is expecting earnings per share to grow about 9% to 10% annually.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

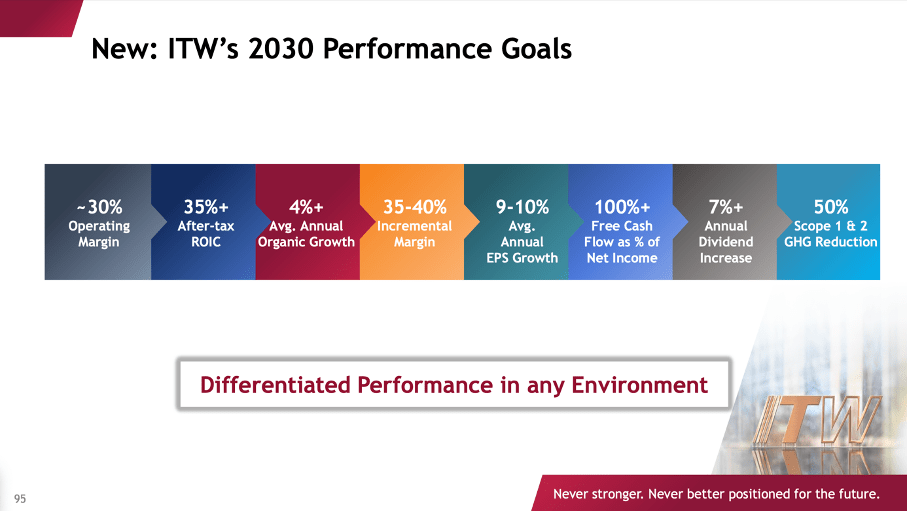

And management has even more very optimistic targets - including at least 100% free cash flow conversion rate and a 7% annual dividend increase for the years 2023 till 2030.

Illinois Tool Works 2022 Investor Day Presentation

{kind=link}

Intrinsic Value Calculation

And even when assuming that these targets are realistic, we still must ask the question if Illinois Tool Works is fairly valued at this point. As always, we can start by looking at simple valuation metrics. And right now, the stock is trading for 23.5 times earnings, which is in line with the 10-year average (22.53). When looking at the price-free-cash-flow ratio, Illinois Tool Works is trading for 28.2 times free cash flow - this is above the average 10-year P/FCF ratio (24.41).

So far, Illinois Tool Works cannot be seen as undervalued or a bargain. And a price-free-cash-flow ratio of 28.2 can only be justified by high growth rates.

Instead of looking at simple valuation metrics, we can use a discount cash flow calculation to determine an intrinsic value. As basis for our calculation, we can take the free cash flow of the last four quarters, which was $2,587 million. And when taking management's growth targets of 10% and assume Illinois Tool Works can grow with that pace for the next ten years followed by 6% growth till perpetuity, we get an intrinsic value of $ 282.19 (10% discount rate and 304.2 million outstanding shares).

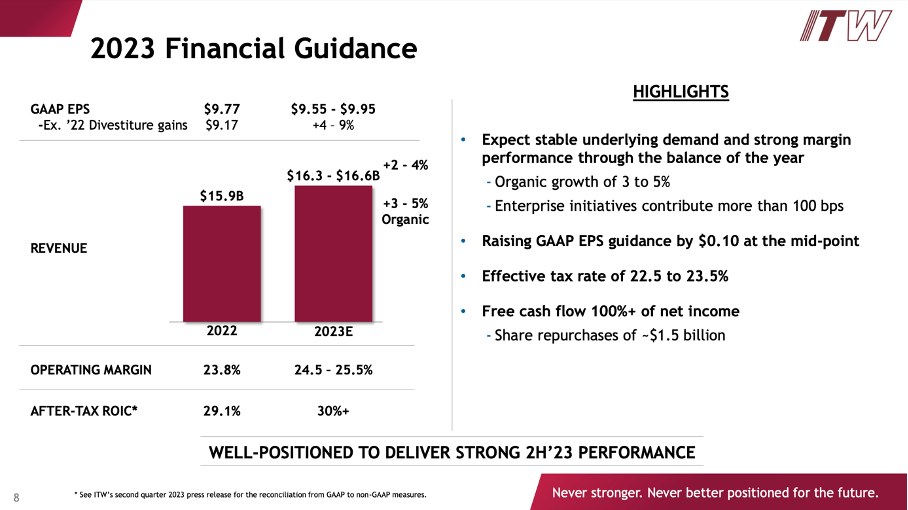

The free cash flow of the last four quarters is more or less in line with the free cash flow of the last five years (which was $2,401 million) and could certainly be seen as realistic assumption. We can even be a little more optimistic and calculate with the estimated free cash flow for fiscal 2023 as basis. Illinois Tool Works is expecting net income to be close to $3,000 million in fiscal 2023 (midpoint of the company's guidance). Management is also expecting free cash flow conversion to be at least 100% and free cash flow in fiscal 2023 should therefore be at least $3,000 million. When calculating with these assumptions we get an intrinsic value of $327.24 for the stock.

{kind=link}

And while assuming $3 billion in free cash flow for fiscal 2023 seems realistic, I don't know if we should calculate with 10% growth for the next ten years. I don't have doubts that Illinois Tool Works can in theory grow with such a high pace. On the other hand, we should always include a margin of safety. When calculating with only 8% growth for the next ten years followed by 6% growth till perpetuity, we get an intrinsic value of $284.08 for the stock.

Conclusion

Although we can calculate a slightly higher intrinsic value than the current stock price, I would see Illinois Tool Works as fairly valued at this point. We could make the argument that the stock is slightly undervalued, but in my opinion, we are not looking at a bargain and the company will only remain on my watchlist at this point. Especially as the business was not able to grow revenue in the last 10 to 15 years, I remain cautious if management is able to achieve 4% organic growth in the years to come.

For further details see:

Illinois Tool Works: Still Not A Bargain