ONTTF - Illumina: Grail's Divestment Could Unlock Significant Shareholder Value

2023-12-12 14:16:54 ET

Summary

- Illumina's market cap has fallen 80% from its all-time highs in 2021, but the divestment of Grail could bring it back on track.

- Illumina's competitive advantage lies in its scalable DNA sequencing platform and highly integrated system, which makes it difficult for customers to switch to competitors.

- The sale of Grail could unlock shareholder value, improve operating margins, and provide fresh liquidity for Illumina to invest in R&D and strengthen its core business.

Illumina ( ILMN ) has been one of the worst performers in the S&P Health Care Select Fund ( XLV ), falling 40% in 2023 alone. Illumina's market cap has fallen from over $75 billion to just $18 billion at the time of this writing, representing an 80% decline from all-time highs in 2021. While the market's pessimism surrounding Illumina can be understood, the divestment of Grail could bring Illumina back on track and lead to shareholder appreciation in the future.

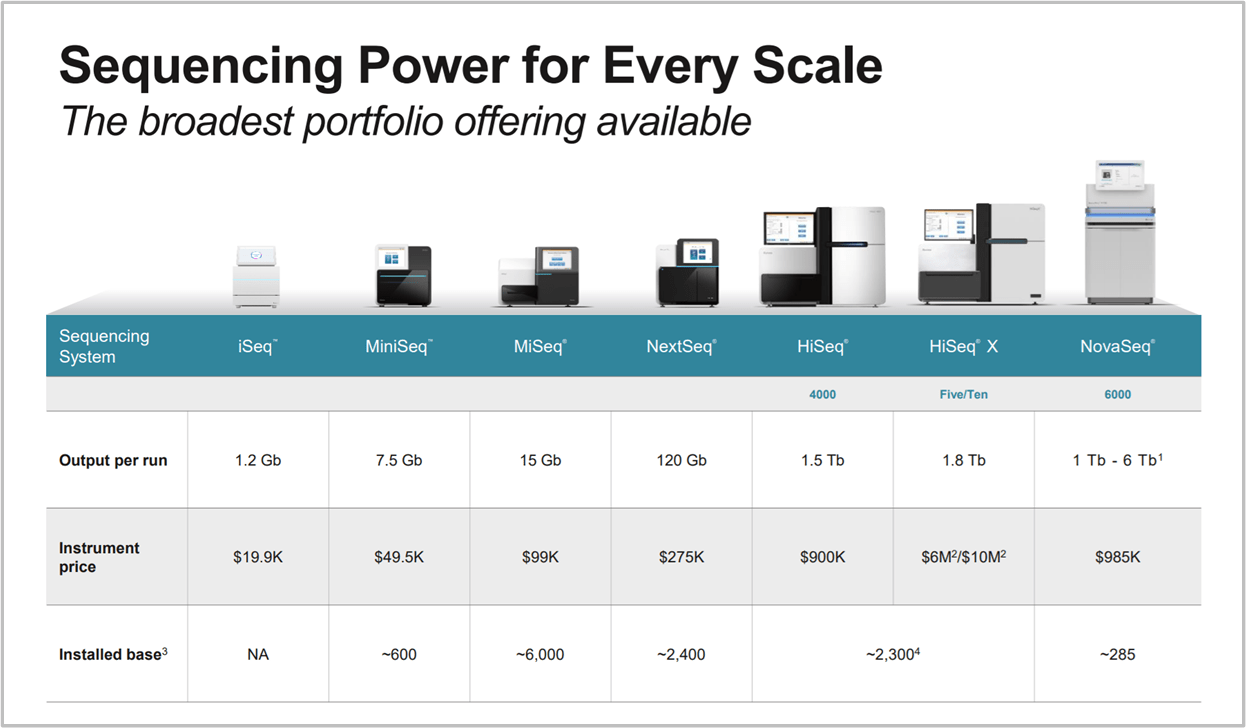

Illumina stands at the forefront of producing advanced genomic sequencing systems. These systems are capable of analyzing DNA fragments present in blood or various other samples. This technology is widely employed in diverse fields, including criminal investigations and pharmaceutical research.

Illumina's competitive advantage lies in two key areas. First, the scalability of its DNA sequencing platform is a major strength. The company's proprietary sequencing by synthesis ((SBS)) technology tracks the addition of labeled nucleotides as the DNA chain is copied, enabling the sequencing of more than 20,000 human genomes per year. The recent introduction of the NovaSeq X production-scale sequencing systems has significantly reduced the cost of reading a human genome to as low as $200??.

{kind=link}

Compounder Fund

Secondly, Illumina offers a highly integrated and scalable system that provides a lower cost of ownership to customers. The company provides comprehensive support for sample preparation, instrument control/management, and post-run analysis. This integration, along with their informatics suite, bio-IT platform, and connected analytics, makes it difficult for customers to switch to competitors once they start using Illumina's solutions. This integration positions Illumina as a cornerstone of the broader sequencing and multi-omics ecosystem??.

Illumina holds an impressive 80% market share with around 90% of all DNA sequencing being completed with Illumina's instruments.

Grail Divestment Could Unlock Shareholder Value

Illumina originally spun off Grail in 2016 but retained a 12% stake. Later, in 2021, it reacquired Grail despite opposition from European and U.S. regulators. Through Grail's comprehensive cancer test, Galleri, which can detect multiple types of cancer from a single blood sample, Illumina aimed to increase its total addressable market. Executives claimed that by reacquiring Grail, Illumina could increase its potential market by $60 billion, given that the liquid biopsy market is projected to reach over $75 billion by 2035.

Despite pending regulatory approvals, Illumina completed the acquisition, leading to substantial fines and allegations of anti-competitive behavior. Thus, the EU Antitrust Fine and Regulatory Opposition, Illumina was fined a record €432 million ($476 million) by the European Union for closing its takeover of Grail before securing EU antitrust approval. The deal, which was initially opposed by both the European Union and the U.S. Federal Trade Commission ((FTC)), was seen as potentially anti-competitive.

Regulators were concerned that Illumina, upon acquiring Grail, might prevent Grail's rivals from accessing the technology needed to develop competing blood-based cancer detection tests. On the flip side, Illumina and researchers claimed that Illumina could broaden the accessibility and reduce the cost of Grail's Galleri test. Through early cancer detection, thousands of lives could be saved every year.

Nevertheless, EU antitrust officials ordered Illumina ((ILMN)) to sell its Grail unit, and Illumina followed suit by filing an SEC filing for a potential divestiture of its GRAIL unit. Illumina stated that the company has already been contacted by interested parties. Although it did not disclose further details, potential suitors are likely large pharmaceuticals.

While Grail is one of the only companies with a blood test designed to detect multiple early-stage cancers on the market, it does not have regulatory approval and likely needs a lot more data to prove it works. Thus, the company has been a money pit for Illumina so far and has not contributed to its top-line earnings.

{kind=link}

Illumina

A large part of Illumina's losses over the past two years can be attributed to the Grail acquisition, including legal costs. This is despite Grail only generating $21 million in revenue in the last quarter and still potentially years from commercial approval.

{kind=link}

Illumina

Illumina's core revenue, however, comprised of its sequencing machines, remains rock solid with strong operating margins. If Illumina divests Grail, overall operating margins will jump back to around 25%, allowing the market to value Illumina based on its core earnings. More importantly, the divestment will open up billions in fresh liquidity for Illumina, which will help bolster its balance sheet, which has deteriorated as a result of its acquisition-related losses over the past two years. The company could use the cash to further strengthen its competitive advantages in its core business and focus on innovations by investing in Research and Development.

Valuation

At an $18 billion market cap, Grail's market value of $7-$10 billion, represents roughly half of its entire value. Until just recently, shares were trading at levels similar to 2011, when Illumina had just $1 billion in annual revenues.

Since its all-time highs in 2021, Illumina's multiple contracted from over 17 times Price to Sales (P/S) to just under 4 times annual revenues as of the latest. Arguably, that valuation was too high, even for a monopoly with over 30% net profit margins, yet Illumina's core fundamentals have not changed, in my opinion. Even before the Grail acquisition, Illumina had a 13-year median Price to Sales Ratio of 12.3, due to its high profit margins, growth, and overall strong competitive position.

Therefore, I believe its valuation should be compared to Intuitive Surgical ( ISRG ), which has a comparable competitive position and comparable margins. Similar to Intuitive Surgical, Illumina also benefits from growing recurring revenues and economies of scale. Around 80% of its revenue comes from higher-margin consumables and services, with each new instrument sold creating a recurring revenue stream. As genome sequencing costs decrease, demand for their services increases, allowing Illumina to maintain a competitive edge by keeping the total cost of ownership lower for their clients compared to competitors.

Before the Grail Acquisition, Illumina's net profit margins hovered around 20-30%, which was among the highest within the medical devices and diagnostics industry. In the latest Q3 earnings, Illumina highlighted its goal to return to 25% core profit margins by 2025 and 27% by 2030. Assuming that Illumina does not further grow revenues (which appears unlikely), this would translate into roughly $1 billion in operating income by 2025. At the current market cap, this would translate into just 18 times Price to Earnings (P/E). In contrast, Intuitive Surgical trades at 72 times P/E, IDEXX Laboratories ( IDXX ) at 54 times P/E and Stryker ( SYK ) at 43 times P/E.

Illumina's core market for genetic sequencing is expected to reach between $15 billion and $25 billion, depending on the estimate. If Illumina's market share drops to 50% due to increased competition, it could still grow revenues to around $10 billion by 2030. Given the fact that Illumina nearly doubled its revenues over the past seven years, this estimate isn't unrealistic, in my opinion. If Illumina reaches 27% profit margins by 2030, this would translate into $2.7 billion in operating income. At a 30 times P/E ratio, or 8.1 Price to Sales, Illumina's market cap could then stand at just over $80 billion, which represents a potential upside of over 300%.

Of course, these are very rough estimates and the exact revenue numbers and valuation figures are difficult to predict. Nevertheless, its current valuation certainly leaves potential for upside in the future. Also, Illumina could face growing competition from newer players such as Oxford Nanopore Technologies ( ONTTF ) and Pacific Biosciences ( PACB ), which could hinder its growth and margin plans. However, Illumina's newest most powerful sequencer of its NovaSeq X Series, outperforms all competing sequencing platforms based on the Cost per Gigabase. Furthermore, companies such as Exact Sciences Corp ( EXAS ) and six other companies testified in the U.S. that they relied on Illumina's system and stated that it is more advanced than others and switching is too costly.

Therefore, I believe Illumina's competitive edges are likely to be sustained as the company remains technologically ahead of its competitors and has substantially higher R&D spent compared to smaller companies such as Pacific Biosciences.

Takeaways

While Illumina's acquisition of Grail has cast a shadow of pessimism over the company, the strength and resilience of its core business may be undervalued. The potential funds from the sale of Grail could enable Illumina to refocus on its areas of expertise—innovation, and growth. Additionally, Illumina stands to benefit from substantial tailwinds provided by the rapidly expanding global healthcare market.

However, the thesis comes with risks. The company faces increased competition and regulatory challenges, particularly in emerging markets like China, where rivals are gaining ground. There's also the inherent uncertainty in the biotechnology sector, where technological advancements can rapidly change the competitive landscape. Furthermore, the ongoing legal and regulatory challenges related to the Grail acquisition could continue to impact the company's financials and stock performance in the short term. Nevertheless, in the long term Illumina's stock could present a compelling opportunity.

For further details see:

Illumina: Grail's Divestment Could Unlock Significant Shareholder Value