AFMC - Immaculate Disinflation Arrives

2023-10-26 21:11:15 ET

Summary

- Inflation is rapidly declining and is likely to continue to decrease further as shelter is declining, but enters the CPI with a considerable lag.

- The balance of the evidence points to pandemic-related factors as the main cause of the surge in inflation post-pandemic, which now looks like a temporal flare up after all.

- Monetary policy and fiscal stimulus were not the main drivers of the post-pandemic inflation.

- With inflation already declining, the Fed risks over-tightening, although residual risks remain.

Now that the dust is settling as inflation is coming down rapidly and will likely come down further (due to a delayed effect of shelter in the official figures), we can now make up the balance of what was behind this surge in inflation. We do this with the help of the following stylized facts:

- Inflation was a ubiquitous phenomenon in the developed world and the decline in US inflation has been as pronounced as in much of the developed world, if not more so, despite fiscal policy being much more expansionary in the US.

- The rapid rise in inflation didn't set off a wage-price spiral, despite record unemployment.

- The rapid rise in inflation hasn't caused a lasting major uptick in inflationary expectations.

- Immaculate disinflation; the rapid decline in inflation has not caused any major uptick in unemployment or job creation despite rapid monetary policy tightening.

The fourth stylized fact is especially noteworthy as nothing like this has happened before. We will argue that the inflationary surge was mostly a pandemic-related phenomenon, which means it is temporary and the Fed risks overtightening.

Inflation is coming down rapidly

The big inflation scare is rapidly declining, here is the headline CPI :

Tradingeconomics

And here is the core CPI, stripped of volatile food and energy:

Tradingeconomics

While 4% is still double the Fed target one could argue that we're highly premature calling inflation essentially conquered.

However, one should realize that the biggest component of the core CPI is shelter, which enters the CPI with a lag of about a year while rents are already falling , and what's more (our emphasis):

The latest Consumer Price Index shows that shelter costs contributed 90% of total inflation last month — but there’s a sharp turnaround ahead, say economic researchers at the Federal Reserve Bank of San Francisco...

But forecasts from the San Francisco Fed researchers suggest we could see the most severe contraction in shelter inflation since the Global Financial Crisis of 2007 to 2009, they say.

“Our baseline forecast suggests that year-over-year shelter inflation will continue to slow through late 2024 and may even turn negative by mid-2024,” the researchers wrote. “This would represent a sharp turnaround in shelter inflation, with important implications for the behavior of overall inflation.”

According to Moody Analytics (our emphasis):

Taking shelter out of the equation, core CPI rose just 0.1% for the month and is up 2% year over year , according to the report. That’s the lowest annual increase that index has recorded since March 2021.

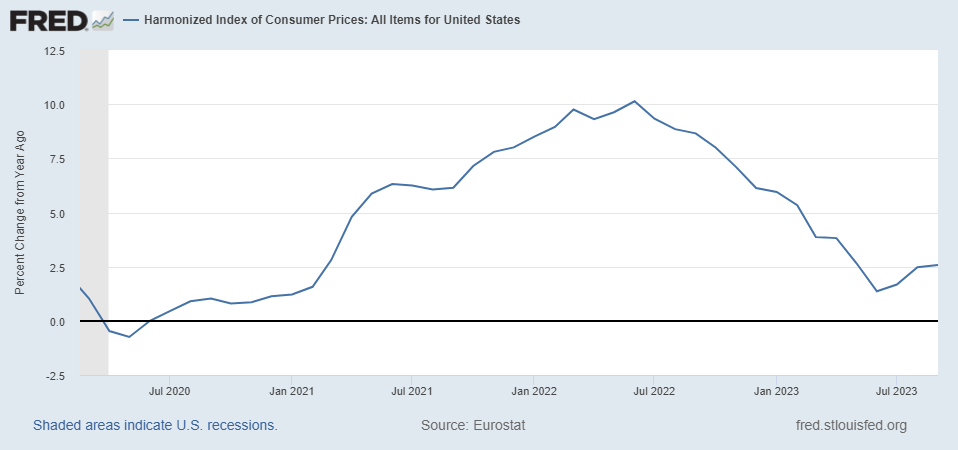

Indeed, the so-called Harmonized Index of Consumer Prices leaves owners' equivalent rent (which is a substantial part of shelter) out, and hey presto, inflation is almost back to the Fed target (2%) already:

{kind=link}

Basically, it has fallen almost as fast as it has risen and without causing any major damage to the labor market, at least so far despite dire warnings from the likes of Larry Summer.

There are other signs of rapidly decreasing inflation in producer prices, most dramatically in China, which, apart from illustrating deflationary forces in the world economy also means the US is importing deflation from them:

Tradingeconomics

The eurozone PPI has become very negative (the German PPI even reached -14.7% in September):

Tradingeconomics

Producer prices in the US are still in positive territory but have also come down rapidly:

Tradingeconomics

Then there are the PMIs (purchaser management index, a forward-looking indicator), in the eurozone it's already in negative territory.

Tradingeconomics

In the US the PMI is still in positive territory (above 50%) but barely:

Tradingeconomics

Lessons

There were three possible causes for the surge in inflation, highly expansionary fiscal and monetary policies, as well as pandemic distortions. Let's briefly discuss each.

Monetary policy

The past decade's experience should produce pause for thought for those who point to the Fed's "money printing" as the cause of the post-pandemic surge in inflation. We've heard these arguments before.

There was an open letter to the Fed in 2010 warning of accelerating inflation and other dire consequences of its asset-buying program (QE). This is somewhat curious as no less a figure like Milton Friedman advised Japan to embark on QE in comparable circumstances and argued that the Fed could have prevented the 1930s depression (by bailing out banks and boosting their reserves, preventing a fall in the money supply).

Reality proved a lot harder. Despite multiple rounds of QE and ultra-low interest rates, inflation didn't show any significant uptick during the decade.

This isn't a surprise. Monetary policy is an enabling factor, not usually a cause of inflation (apart from relatively rare circumstances like directly financing public spending, war, or crisis).

Money largely ends the economy through banks, which create deposits (part of the money supply) through lending. If there is no great increase in credit demand inflation is unlikely to take off.

One might retort that inflation showed up in asset prices, we would simply say that low-interest rates (that is, longer rates which are more important for the economy) would do that without any money printing. Low interest rates were largely the result of structural forces, the Fed's QE had a marginal effect on these.

It doesn't mean we are fans of QE, we're not. We think the post-financial recovery could have been much better handled with fiscal policy, as it's highly effective and essentially free at very low interest rates, but that's another matter.

Fiscal stimulus

As it happens, these lessons have been learned post-pandemic when the US (under both the previous as well as the present administration) went in big. This is why the post-pandemic recovery was much more vigorous even if money is no longer free.

But did the supersized fiscal stimulus produce the post-pandemic surge in inflation? It is likely to have contributed, but we don't think it was a major factor:

- The fiscal stimulus in the eurozone was much smaller , yet they experienced an even worse bout of inflation compared to the US.

- Fiscal policy remained highly expansionary yet this hasn't prevented inflation from falling rapidly.

Immaculate disinflation

Against the latter one could argue that it's the Fed's policy tightening that caused the rapid decline in inflation. However, apart from wealth effects, Fed tightening works mostly through cooling the economy, that is, higher interest rates cause interest-sensitive expenditures to decline, reducing growth and job creation.

This has happened in every other tightening Fed cycle, often throwing the economy into a recession, but not this time, growth and job creation remain vigorous and unemployment remains at 40-year lows, this has already been called the immaculate disinflation for these reasons.

We seem to have busted the usual trade-off between inflation and unemployment, confounding almost everybody, this isn't the 1970s, it's almost the opposite (even if both Larry Fink and Jamie Dimon still make comparisons to the 1970s)

A year ago expectations for a recession were widespread (see here and here ) and many (like Larry Summers ) argued that it would take a prolonged period of high unemployment to bring inflation down.

That isn't to say no recession and higher unemployment will ensue. The Fed can overdo it, and bond yields are rising considerably (material for upcoming articles), but so far the thesis of immaculate disinflation holds. Something else seemed to have caused the post-pandemic inflationary surge.

Pandemic

We think this is a no-brainer, it was the pandemic after all, reinforced by the Russian invasion of Ukraine, the reasons are simple:

- It caused a strong shift in demand from services to goods at the same time as creating all sorts of bottlenecks in production and logistics made it more difficult to fulfill that increase in demand.

- It produced increased demand and significant shifts in housing at the same time as hampering construction, creating a large rise in rents that came into the official figures with a lag (and will disappear from the officials with the same lag).

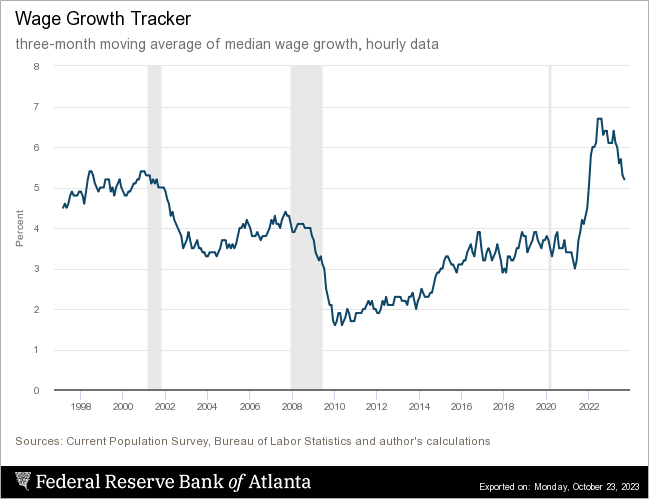

- Wage growth (while actually above inflation) is already declining quite significantly so there is little risk of a wage-price spiral and inflation expectations never caused alarm, suggesting what caused inflation was a one-off.

{kind=link}

Conclusion

- If tremendous monetary expansion in the 2010s didn't cause inflation and monetary tightening post-pandemic isn't responsible for the recent decline of inflation and inflation fell rapidly even in the face of very expansionary fiscal policy, the logical conclusion is that these policies weren't the prime driver of the post-pandemic inflation in the first place.

- This is corroborated by experiences abroad where inflation was every bit as serious as in the US but policy was much less extreme.

- The lack of a wage-price spiral and well-behaved inflationary expectations also point to one-off causes.

- That inflation lasted as long as it has can largely be explained by the reinforcement of pandemic distortions by the Ukraine invasion and the lag in the data for shelter, the biggest component in the CPI and core CPI.

And perhaps best for investors, with inflation mostly the product of one of pandemic distortions, the Fed could, and probably should stop raising rates. Whether they do is another matter, although they finally seem to have gotten the message .

But we are not entirely out of the woods. The Fed can still overdo it (in order to recover their lost credibility), inflation can flare up due to other causes (like international tensions producing an oil price surge) and bond yields have been rising significantly, doing much of the tightening for the Fed.

For further details see:

Immaculate Disinflation Arrives