IMGN - ImmunoGen: Shares Take Flight On Ovarian Cancer Survival Data - What Happens Next?

2023-05-04 10:31:45 ET

Summary

- ImmunoGen released some outstanding Phase 3 data in relation to its only approved asset ELAHERE yesterday.

- In its MIRASOL study, ELAHERE met its primary endpoint of Progression Free Survival, as well as the key secondary endpoint of Overall Survival in Platinum Resistant Ovarian Cancer.

- The drug has already received an accelerated approval in the US in PROC - full approval - and approval in Europe now looks a formality.

- Nevertheless, and despite stellar triple-digit percentage gains for the stock price, the MIRASOL data does not necessarily increase the peak sales number for ELAHERE of ~$210m.

- IMGN is chasing approval in Platinum Sensitive Ovarian Cancer - a larger market opportunity - and data from a study in that field will arrive before the end of the year.

Investment Overview

ImmunoGen (IMGN) - an under the radar, Waltham, Massachusetts based biotech founded in 1981 sent its shareholders into raptures yesterday after publishing new data from its Phase 3 MIRASOL study of its drug ELAHERE, in patients with FR?-Positive, Platinum-Resistant Ovarian Cancer ("PROC").

Prior to yesterday's news, ImmunoGen stock had been trading at a value of ~$4 - which is about the average across the past 5 year period. Shares ended the day trading at $12.2 - their highest value since the end of 2015. Across the past 5 years the stock is now up just 8.4%, although across the past year, it is +142%.

ELAHERE Overview And Why Yesterday's Data Is So Important

ImmunoGen's business is focused on the development of next-generation antibody drug conjugates ("ADCs"), a class of drug the company describes as follows in its Q1'23 10-Q submission (quarterly earnings and updates):

An ADC with our proprietary technology comprises an antibody that binds to a target found on tumor cells and is conjugated to one of our potent anti-cancer agents as a "payload" to kill the tumor cell once the ADC has bound to its target. ADCs are an expanding class of anticancer therapeutics, with twelve approved products and the number of agents in development growing significantly in recent years.

4 of the 12 approvals mentioned above were secured by the Seattle based, oncology focused drug developer Seagen (SGEN), a business that was recently acquired for $43bn by Pharma giant Pfizer ( PFE ), which helps to underline the promise the industry sees in ADCs.

ELAHERE - or Mirvetuximab Soravtansine, to give it its chemical name, is, according to ImmunoGen:

a first-in-class ADC targeting folate receptor alpha (FR?), a cell-surface protein over-expressed in a number of epithelial tumors, including ovarian, endometrial, and non-small-cell lung cancers.

In November last year the FDA agreed to award ELAHERE an accelerated approval for the drug, as a therapy for adult patients with FR? positive, platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal cancer, who have received one to three prior systemic treatment regimens.

This was based on data from a single arm SORAYA study of 33 patients that showed an Objective Response Rate ("ORR") of 31.7%, and a Duration of Response ("DOR") of 6.9 months. Analysts offered peak sales estimates around the $170m per annum mark, although due to a previous failed Phase 3 study in which ELAHERE failed to extend progress free survival ("PFS") by more than chemotherapy, were skeptical of the impact the drug could have in a real world setting.

ELAHERE is not the first FRA-targeting drug to have flunked a late stage trial - Japanese Pharma Eisai saw its drug farletuzumab fail to meet endpoints in a Phase 3 ovarian cancer study, whilst Merck ( MRK ) and partner Endocyte abandoned a Phase 3 study of FRA-targeting candidate vintafolide in ovarian cancer.

Yesterday's data from Immunogen however apparently turns the thesis that targeting FRA does not work well in Ovarian Cancer therapy on its head. The Phase 3 MIRASOL study, which enrolled 453 patients, demonstrated "a statistically significant and clinically meaningful improvement in OS compared to IC chemotherapy", according to a press release . The release goes on:

With 204 OS events reported as of March 6, 2023, the median OS was 16.46 months in the ELAHERE arm, compared to 12.75 months in the IC chemotherapy arm, with a hazard ratio ("HR") of 0.67, p=0.0046. This represents a 33% reduction in the risk of death in the ELAHERE arm in comparison to the IC chemotherapy arm.

ELAHERE demonstrated a statistically significant and clinically meaningful improvement in PFS by investigator assessment compared to IC chemotherapy, with a hazard ratio of 0.65 (p<0.0001), which represents a 35% reduction in the risk of tumor progression or death in the ELAHERE arm compared to the IC chemotherapy arm. The median PFS in the ELAHERE arm was 5.62 months, compared to 3.98 months in the IC chemotherapy arm.

ORR by investigator assessment in the ELAHERE arm was 42.3%, including 12 complete responses (CRs), compared to 15.9%, with no CRs, in the IC chemotherapy arm.

Anna Berkenblit, MD, Senior Vice President and Chief Medical Officer of ImmunoGen added that:

Importantly, ELAHERE is the first drug to show an overall survival benefit in this patient population.

In short, these results had a genuine "wow factor" about them. When ImmunoGen had announced the accelerated approval of ELAHERE back in November, its share price hardly budged, again based on doubts about the drug's profile, its planned $6k per vial (with patients expecting to receive 3-4 vials per course of treatment) price point, and competition in the form of already approved PROC drugs such as AstraZeneca's ( AZN ) Lynparza, and vascular endothelial growth factor ("VEGF") targeting Avastin.

Perhaps strangely, however, as good as the MIRASOL results are, some analysts have not noticeably raised their peak sales expectations for the drug. SVB Securities apparently raised expectations from $170m per annum, to $210m, on the basis that chances for success in platinum sensitive ovarian cancer remained low, and also pointing to 55% of patients who receive AstraZeneca's PARP inhibitor Lynparza during the MIRASOL study.

On the other hand, Piper Sandler upgraded ImmunoGen stock, noting the outperformance in Overall Survival, and raising its price target to $16 per share, from $6 per share.

ELAHERE - What Happens Now?

It might seem odd that such an important, share price needle moving data win may not translate to a revenue opportunity that supports ImmunoGen's new market cap valuation of $2.8bn. Based on peak sales expectations of $210m per annum, we have a forward price to sales ratio of ~13.3x, which either means that ImmunoGen stock is now significantly overvalued, or that the market believes there is much to come from this drug, this company, and this company's pipeline.

Certainly, ImmunoGen will now be able to submit a supplemental Biologics License Application ("sBLA") and almost certainly receive a full approval for ELAHERE, likely this year. This is the first new PROC drug to be approved since 2014, and ELAHERE revenues in Q1'23 were $29.5m, which seems like an impressive start, plus management says it has coverage policies in place for ~55% of Medicare and ~70% of commercial lives.

According to ScienceDirect :

Platinum-resistant ovarian cancer, generally defined as progression occurring within 6 months after completing platinum-based therapy, occur in about 20 % of the patients after first-line platinum-based therapy

If my understanding is correct that therefore makes platinum sensitive ovarian cancer ("PSOC") the much larger market, and despite analysts' skepticism, it is a target market for ImmunoGen, with ELAHERE being evaluated as a monotherapy in this indication.

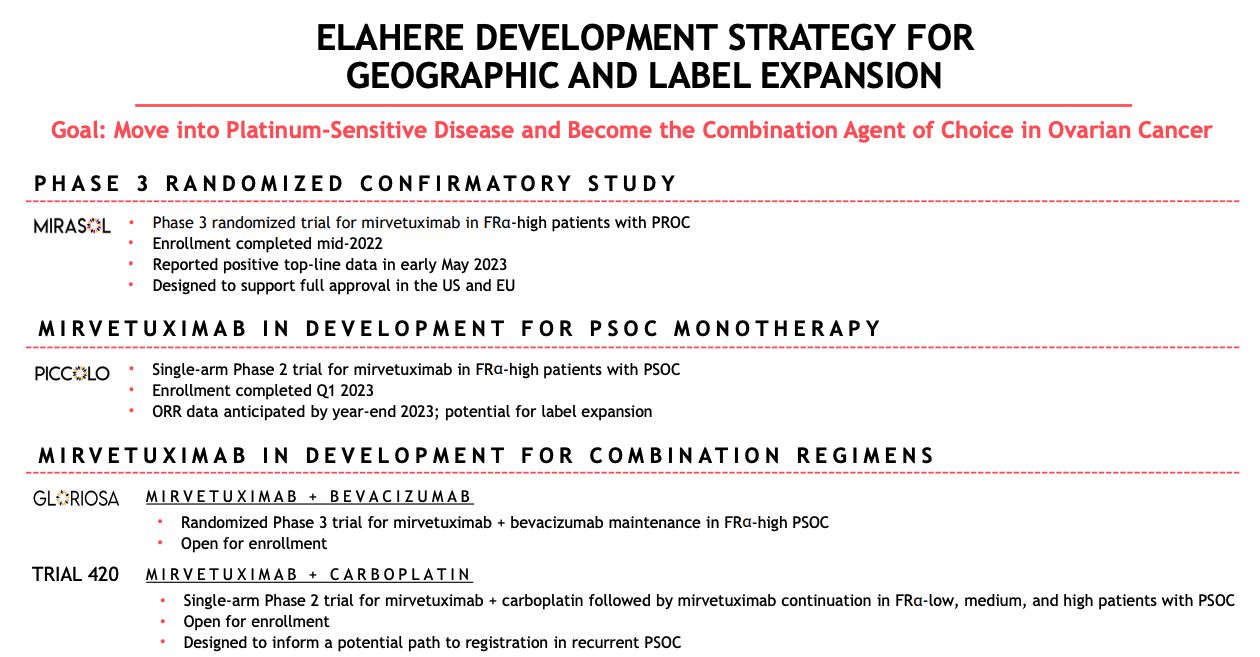

ELAHERE development strategy (ImmunoGen presentation)

{kind=link}

As we can see above, besides MIRASOL, there is a Phase 2 PICCOLO study evaluating ELAHERE as a monotherapy in PSOC ongoing, with data expected this year, and 2 further studies, GLORIOSA and TRIAL 420, evaluating the drug in combo with Swiss Pharma Roche's (RHHBY) Avastin, and chemo drug Carboplatin.

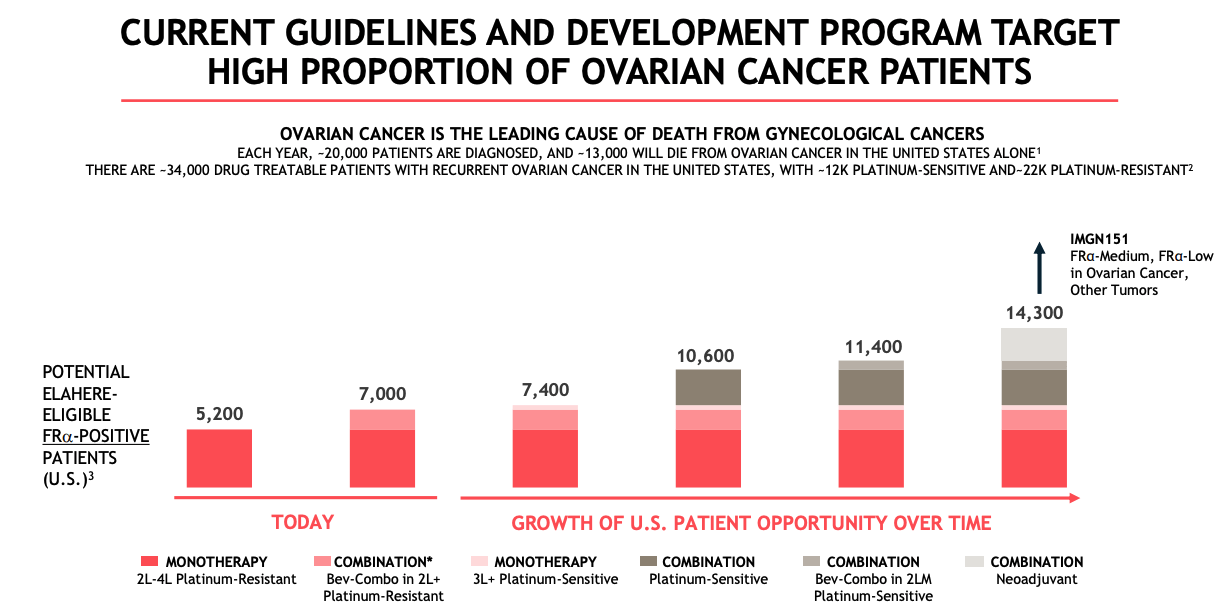

ImmunoGen patient opportunity forecast for ELAHERE (ImmunoGen presentation)

{kind=link}

As we can see above, if all studies were to be successful - and that is far from guaranteed, it should be stressed - then ELAHERE's target market may increase from 5k patients today, to >14k if all label expansions are approved. Based on the near 3x increase in patients, an optimistic scenario might suggest that ELAHERE could go on to achieve blockbuster (>$1bn per annum) sales in Ovarian Cancer alone.

ELAHERE has not yet secured approval in Europe and the UK, although this seems likely to happen soon based on the data, which increases the total addressable market ("TAM") still further, whilst ImmunoGen also has a Chinese partner - Huadong Medicine - who could pay ImmunoGen up to $265m more if development and approval milestones are met.

Plus, ELAHERE is not ImmunoGen's only ADC candidate. Pivekimab Sunirine is being evaluated in 2 Phase 2 studies, in patients suffering from Blastic plasmacytoid dendritic cell neoplasm ("BPDCN"), and Acute Myeloid Lymphoma (in combo with chemo drugs), whilst IMGC936 is in Phase 1 studies in various solid tumor cancers, and IMGN151 in a Phase 1 study looking at endometrial cancers.

ImmunoGen reported a cash position of $201m as of Q1'23, and total revenues of $49m, although total costs and operating expenses amounted to $92.3m, resulting in a loss from operations of $42.4m. As so many biotechs do on the back of a good date release, the company has immediately moved to raise $200m via a share offering, which means current shareholders will suffer some dilution, although they will doubtless be expecting a good return on the $200m raised.

Some Risks Around ImmunoGen To Consider

With close to $400m in cash, despite making a net loss of $223m in 2022 ImmunoGen ought to have sufficient funding for the next couple of years, especially now that the company is generating revenues. FY23 guidance is for $45 - $50m of non-ELAHERE revenues, and OPEX of $320 - $335m. No forecast for ELAHERE revenues is provided, but if we assume sales in later quarters match Q1, that figure would be ~$120m, and net loss would come in at around $160m for the year.

As such, ImmunoGen will remain a loss-making company in 2023, and considering its current market cap of nearly $2.8bn, that does make the current share price look a little high.

Although ImmunoGen is enjoying a first mover advantage for an ADC in PROC, a statement in the company's 2022 10K submission discusses its competition as follows:

Mersana Therapeutics ( MRSN ), Eisai ( ESAIY ), and Sutro BioPharma have clinical-stage ADCs targeting platinum resistant ovarian cancer, and Pfizer, Seattle Genetics, Roche, Astellas, AstraZeneca, Daiichi Sankyo, GlaxoSmithKline ( GSK ), AbbVie ( ABBV ), and the Menarini Group have programs to attach a cell-killing small molecule to an antibody for targeted delivery to cancer cells.

With competition coming in the form of major Pharmas with massive R&D and marketing budgets such as Eisai in PROC and AbbVie (ABBV) and Pfizer in the ADC space, it is possible that ImmunoGen and ELAHERE could be overwhelmed, whilst the current competition against e.g. Lynparza and chemotherapies will continue. In short, ImmunoGen may not have the upper hand in, or exclusive access to its target markets and the company has very limited commercial experience.

Concluding Thoughts: Outstanding Results Enhance ImmunoGen's Reputation - Although The Road Ahead Remains Somewhat Unclear

When a biotech company released data as impressive as ImmunoGen did yesterday with the announcement of its MIRASOL Phase 3 data, it deserves to be rewarded as such conclusive data readouts are rare. As such, I am not surprised to see the company's share price spike overnight - however the next question is whether the gains are sustainable.

The low peak sales forecasts for ELAHERE are a concern, in my view, although an approval in Europe and the UK may increase expectations from ~$210m, to ~$350m. That's still not enough to support a $2.8bn market cap, therefore it does seem important that ImmunoGen can penetrate the PSOC market, and that it continues to work on its other ADC assets.

Another value enhancing event that I would not rule out is a large Pharma offering to buyout ImmunoGen - this could be done for >$10bn, in my view. A Pharma would have few qualms about paying ~$7.5bn for a drug generating the kind of data that ELAHERE has, plus 3 other candidates and a technology platform that also helped develop KADCYLA - a marketed ADC resulting from a development and commercialization license with Roche. Obviously, ImmunoGen shareholders would be delighted to make a ~270% further gain on their investment - after yesterday's gains.

Roche could in fact be the buyer, or perhaps Eli Lilly (LLY), given the 2 companies are already working together on developing assets in a program that has the "potential for up to $1.7 billion in development and sales-based milestone payments if all targets are selected and all milestones are realized", according to ImmunoGen's 10K submission.

Nevertheless, in the short term ImmunoGen still has a lot of work to do, and a key data readout to come at the end of this year when PSOC monotherapy data is shared. Since biotech valuations tend to drift downward when there are no notable near-term catalysts in play, I'd be prepared to wait and see if ImmunoGen's shares lose a little of their value in the coming months as share offerings and the realities of trying to grow market share in a presently tough trading environment hit home.

As a biotech stock watcher I wish I had paid more attention to ImmunoGen - especially in the wake of Pfizer's buyout of Seagen - and invested ahead of yesterday's results, although the risk may well have looked too high back then owing to the prior Phase 3 fail. There could be much more to come from ImmunoGen stock, however, and if I see the share price slip back into the single digits while the current upside catalysts are still in play, I'd be tempted to buy.

For further details see:

ImmunoGen: Shares Take Flight On Ovarian Cancer Survival Data - What Happens Next?