TAK - ImmunoGen: Takeda Swoops For Slice Of Elahere - Adding To Valuation Uncertainty?

2023-08-29 13:45:03 ET

Summary

- Yesterday, ImmunoGen, Inc. announced it has entered an exclusive licensing agreement with Takeda for the rights to develop and commercialize Mirvetuximab Soravtansine in the Japanese market.

- ImmunoGen's antibody drug conjugate - marketed and sold as Elahere -is indicated for platinum resistant ovarian cancer.

- The drug won accelerated approval in November last year - but outstanding data from its MIRASOL study virtually guarantees a full approval.

- Analysts were initially unsure about the drug's sales potential, but in Q2 2023 alone, Elahere generated $77.4 million in net product revenues.

- The Takeda deal is good news - although it raises questions about the true worth of Elahere and ImmunoGen - given doubts around patent protection, competition, and peak sales.

Investment Overview

I last covered ImmunoGen, Inc. ( IMGN ) for Seeking Alpha back in May, after the company's share price had leaped from ~$4, to ~$14/ The catalyst for gains was outstanding data released from the company's Phase 3 MIRASOL study of its lead candidate - the antibody drug conjugate ("ADC") Mirvetuximab Soravtansine.

Mirvetuximab Soravtansine had already been handed an accelerated approval by the FDA for the treatment of adult patients with FR? positive, platinum-resistant ovarian cancer ("PROC"), in November 2022, based on data from the single arm SORAYA study showing the drug shrank tumors in 32% of patients, but the new data was even more impressive, and virtually guarantees a full approval for the drug - which is marketed and sold under the brand name Elahere.

Drugs handed an accelerated approval - based on promising early data and a significant unmet need amongst the patient population - can still have that approval revoked if subsequent (required) studies do not support the original data. In the MIRASOL study, however, Elahere showed a 35% reduction in the risk of tumor progression or death compared to the chemotherapy arm, and the chemo drug in question was paclitaxel, which is regarded as the gold standard.

Median Overall Survival ("OS") was 16.46 months in the mirvetuximab arm, compared to 12.75 months in the IC chemotherapy arm (data from ImmunoGen's latest quarterly report ), and Elahere's Objective Response Rate ("ORR") was 42.3%, including 12 complete responses ("CRs"), compared to 15.9%, with no CRs, in the paclitaxel arm.

ImmunoGen's CEO Mark Enyedy called the data a "home run," noting that Elahere is the first drug to show an overall survival advantage in PROC. There was a slight catch, however - analysts were not sure how well the drug would sell.

Because Elahere had previously failed a Phase 3 study in PROC patients expressing high levels of Folate receptor alpha ("FR?") - a tumor associated antigen whose expression is often associated with more aggressive tumors, there were doubts about how widely the drug may have been adopted. The consensus seemed to be that the drug would struggle to drive peak sales of much more than $200m.

Perhaps analysts needn't have worried, however, because in Q2 2023 alone, Elahere generated $77.4m of net product revenues - on track to shatter analyst's estimates in its first full year on the market. Net loss for the quarter was reduced to just $(4.2m), versus $(62m) in the prior year quarter.

Takeda Buys Into The Elahere Success Story

Elahere is the first drug for which ImmunoGen has secured a commercial approval in more than 40 years, so arguably, analysts may have been right to question how easily management could turn the drug - which has a reported list price of ~$18k - $25k per annum - into a commercial success, with no prior experience. After all, no fewer than 30 drugs have been approved to treat Ovarian cancer, plus, there are safety concerns to consider, such as high instances of ocular toxicities - visual impairment, keratopathy, dry eye, photophobia, eye pain, and uveitis, for example.

One region the company no longer needs to worry about, at least, is Japan - a substantial Pharma market. Yesterday, the ~$48bn market cap Japanese Pharma giant Takeda ( TAK ) announced that it had entered an exclusive licensing agreement with ImmunoGen to:

Develop and commercialize mirvetuximab soravtansine-gynx (Hereinafter referred to as MIRV) for the Japanese market.

In Japan, ~13k cases of ovarian cancer are reported annually, with 40-50% of those cases advanced stage III and IV cancer, according to Takeda. Takeda's Head of Oncology Satoshi Uchida commented in the release:

Ovarian cancer is diagnosed in advanced stages in many patients, is considered to be the most lethal tumor among female reproductive organ tumors, and is the ninth most common cause of cancer death in Japanese women. We sincerely hope that MIRV, an innovative treatment developed by ImmunoGen, will be a new treatment option in this area with high unmet needs,

By the terms of the deal, ImmunoGen will receive $34m:

"in upfront and near-term milestone payments," and further, unspecified commercial and regulatory milestone payments, as well as double-digit royalties on future sales of the drug. ImmunoGen says it "has retained exclusive production rights and will supply product for development and commercial use in Japan". This may have been a wise move, as it gives the company ongoing control of drug product, but importantly, Takeda now has the rights to develop the drug "in all indications."

{kind=link}

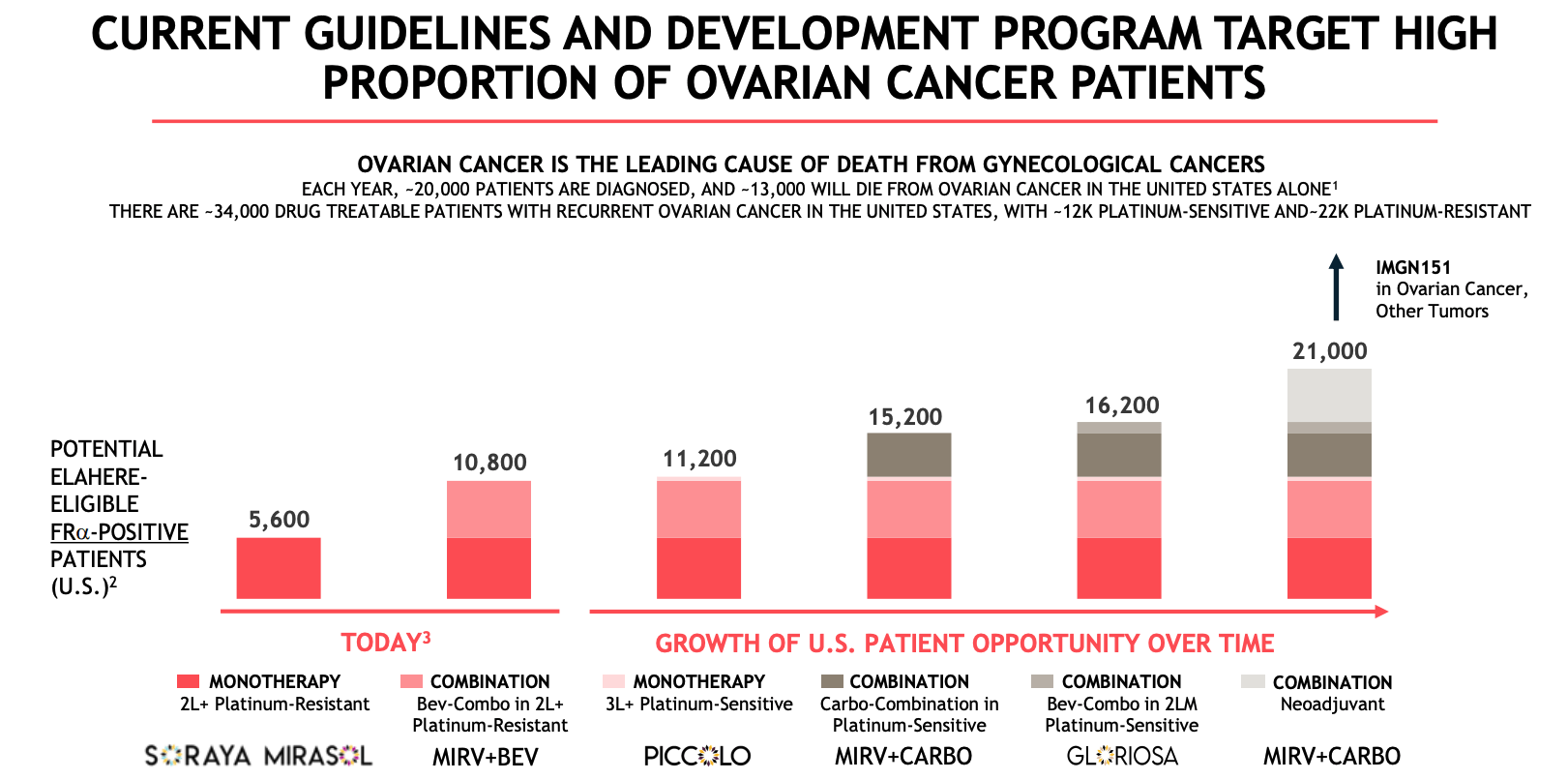

As we can see in the slide above - taken from a recent ImmunoGen presentation - the company has no plans to rest on its laurels, or rely on its current 5.2k patient market opportunity - which, multiplied by the midpoint of the quoted list price range implies a total addressable market of only ~$120m.

ImmunoGen is looking at developing Elahere in combo with bevacizumab - Swiss Pharma Roche's ( RHHBY ) Avastin - in platinum sensitive ovarian cancer - a phase 3 study is underway - as a monotherapy in later line platinum sensitive OC - at the Phase 2 stage - and as a doublet with chemotherapy carboplatin - also at the Phase 2 stage.

All of these larger target markets are presumably in play for Takeda also, and as we can see, in the U.S., these markets together represent a near 5x larger market opportunity than the monotherapy in PROC.

Questions Persist Around Revenue Opportunity

ImmunoGen's current market cap valuation is $3.9bn, and while there is no question that Elahere represents a major breakthrough for PROC treatment, and perhaps platinum resistant ovarian cancer also, even when we consider a best possible scenario in which the drug is approved for all the indications discussed above, the addressable market still appears to be below $500m.

That's arguably problematic for a company with a market cap valuation that is already ~40x larger than its current U.S. peak sales opportunity, and ~10x its future market opportunity. ImmunoGen says it will submit for European approval in the fourth quarter of this year, and given the chances of approval, based on data to date, are very strong, we could arguably double the market opportunity, and bolt on, let's say for argument's sake, ~$100m of royalties from Takeda per annum.

If we do this, then we start to see a blockbuster (>$1bn per annum) revenue opportunity for Elahere, and if we use a rule of thumb that a commercial stage Pharma may typically trade at ~5x sales, we can make the case that ImmunoGen's stock is as much as 28% undervalued.

Nevertheless, a lot has to go right for Elahere to succeed in all of the above indications - will the drug prove as effective in platinum sensitive OC as it is in platinum resistant? Plus, if the peak sales expectation was >$1bn per annum, wouldn't Takeda have had to pay far more to grab the rights to market and sell the drug in Japan than $34m plus royalties?

Furthermore, there is another issue that needs to be taken into account.

Intensifying Competition In ADC Space May Catch Up With Elahere

In some ways, by delivering such an impressive set of data from its MIRASOL study, ImmunoGen has created a problem for itself, by reviving a field of research, i.e., targeting of the folate receptor alpha, that many other companies were ready to abandon.

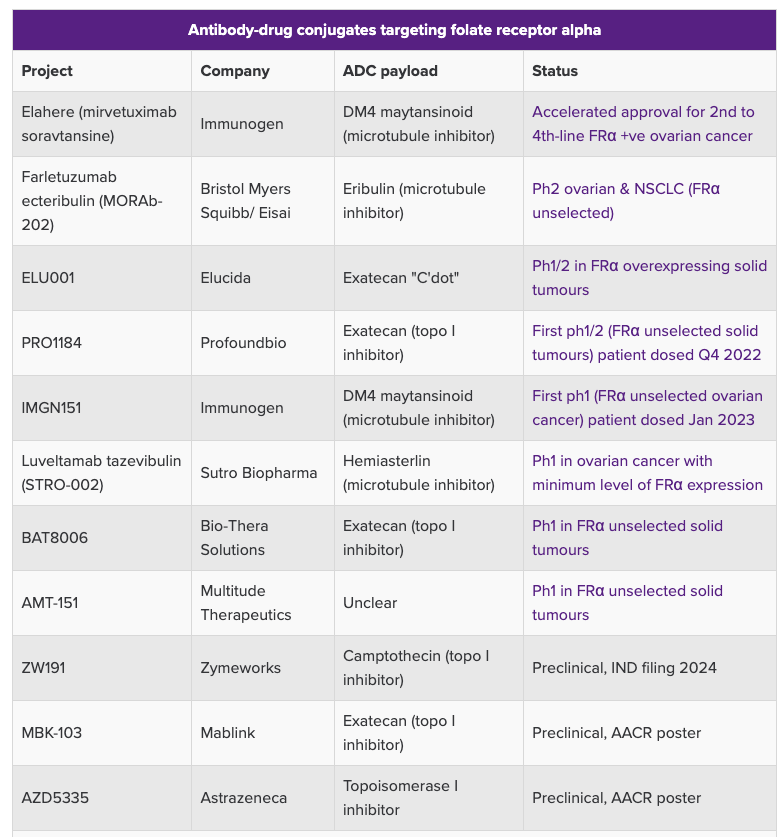

{kind=link}

As we can see from the above table (put together by Evaluate Pharma ) a large number of companies are also developing ADC's targeting FR? . Granted, not all of them will target ovarian cancer, but, as we can see, Bristol-Myers Squibb ( BMY ) has already reached the Phase 2 stage in this indication with a drug candidate purchased from Japanese Pharma Eisai for $650m upfront.

Perhaps ImmunoGen can take comfort from the fact that BMY was prepared to pay such a large sum for the asset - were ImmunoGen itself to become an M&A target, how much would a Pharma pay for an already approved asset with data as good as Elahere's? When we consider that Pfizer ( PFE ) was prepared to bid ~$43bn for Seagen ( SGEN ), a company boasting 4 approved ADC drugs, surely any buyout of ImmunoGen would take place at a value in the double-digit billions?

That may be the case, but it may also be worth considering the level of patent protection that ImmunoGen enjoys, in relation to Elahere and its pipeline of ADC assets, including Pivekimab Sunirine, which is in a Phase 2 study in myeloid malignancies.

Based on what I have found in the company's submissions to the SEC, I am not sure that Elahere enjoys a period of exclusivity in the market, i.e., it does not have "Orphan Drug Designation" from the FDA, so my understanding would be that, if, say, BMY successfully brings its ADC to market in ovarian, its superior marketing and sales infrastructure could blow ImmunoGen and Elahere out of the water.

ImmunoGen reported a cash position of $572m as of Q2 2023 - up from $275m in the prior year quarter - so money for SG&A purposes is not exactly scare, but then there is the safety aspect to consider and the fact that the company may not be well-positioned to protect the "secret sauce" in its ADC from copycat drug developers.

Concluding Thoughts - Takeda Deal Further Validation Of A Breakthrough ADC - But Does It Justify ImmunoGen's Upwardly Mobile Valuation?

When a Pharma of global repute such as Takeda swoops for the rights to your drug, as a biotech, you can be sure you have developed a good drug. In my last note on ImmunoGen, in May, I shared the company's definition of an ADC as follows:

An ADC with our proprietary technology comprises an antibody that binds to a target found on tumor cells and is conjugated to one of our potent anti-cancer agents as a "payload" to kill the tumor cell once the ADC has bound to its target.

The very precise nature of the drug's mechanism of action ("MoA") may restrict the range of indications it can target - unlike an immune checkpoint inhibitor like Merck's >$20bn per annum selling Keytruda, which has secured approvals in multiple indications, it may be the case that a new ADC must be developed for each new indication.

That could be restrictive to ImmunoGen's commercial ambitions, although as discussed, Elahere, if proven to be effective in platinum sensitive ovarian cancer, could target blockbuster sales - but for how long?

If there is no protection in place preventing rivals from bringing ADC's with a similar MoA to market, the first mover advantage that Elahere currently enjoys could be swiftly eroded. On its Q2 2023 earnings call, ImmunoGen management declined to provide FY23 revenues guidance, so we do not know what revenue target management has in mind.

In summary, whilst ImmunoGen has unquestionably developed an exciting new drug, that has gotten off to an excellent start commercially, many questions remain to be answered. Can Elahere expand its label? Can ImmunoGen develop another effective ADC to target other indications (we already know there is a next generation ovarian drug in development)? What kind of patent protection does Elahere have? Could safety be the drug's Achilles heel?

Each question adds an additional layer of risk to the Elahere story, and arguably detracts from the overall company valuation, as does, perhaps, the lack of forward guidance. As such, it is a little trickier to make the bull case for ImmunoGen stock than it may look at first glance. M&A activity would undoubtedly send the valuation soaring, but with so many companies believing they already have an Elahere rival in-house, will any larger Pharma take the plunge?

ImmunoGen secured another notable win yesterday with the Takeda deal - could the Japanese Pharma be the one to pull the trigger on an acquisition bid? Takeda may respond that it is more than satisfied with a $34m upfront payment plus royalties for the Japanese rights. All things considered, coming up with an appropriate valuation for ImmunoGen is a head-scratcher. If I were a shareholder I'd simply be happy the company is about to end it's 40-year wait for an approved drug.

That, and a European approval, could push ImmunoGen, Inc.'s valuation beyond $5bn in my view, but there are multiple risks to consider. It may be worth remembering that as recently as February this year, shares traded <$4.

For further details see:

ImmunoGen: Takeda Swoops For Slice Of Elahere - Adding To Valuation Uncertainty?