ARGNF - Immunovant: argenx At A 10% Valuation Initiating With A Buy Rating

Summary

- Immunovant is developing a similar drug to argenx, but at 10% of argenx’s valuation, offering a good option value and a hedge against owning argenx.

- Immunovant has a new generation anti-FcRn IMVT-1402, and recent pre-clinical data showed that it does not impact albumin levels (which was the key overhang for batoclimab).

- Any positive data from IMVT-1402 can work as an inflection point for the stock, as the market expectation is close to rock bottom.

- IMVT has a robust cash runway until 2025 (cash of ~USD400M) and an EV of 2.14Bn at the moment.

Pipeline, argenx copay-cat

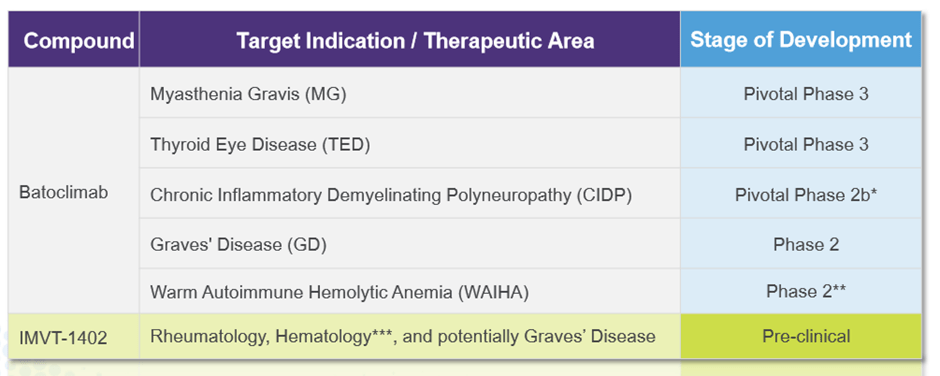

Immunovant (IMVT) is developing an anti-FcRn similar to argenx's (ARGX) efgartigimod. Although their mechanism of action is similar, there are some differences; argenx's efgartigimod is an anti-FcRn fragment, whereas IMVT's batoclimab is a full anti-FcRn and there is some evidence that the full anti-FcRn leads to some cardiovascular issue due to its impact on albumin. This could be due to the fact that efgartigimod has a smaller size, and that is why it can avoid albumin interactions. We believe this "safety overhang" and argenx's launch showing impressive close to USD300M sales during 2022 (beating consensus) in gMG have driven IMVT's stock price down with many investors thinking the pipeline is dead.

IMVT Pipeline summary (Company)

{kind=link}

We are neutral on batoclimab's potential in MG but positive on CIDP as a potential tradable option value.

Currently, the company has an ongoing phase 3 study in myasthenia gravis, where the management is confident that batoclimab's overall efficacy and safety profile. However, with efgartigimod's approval and UCB's (UCBJF) rozanolixizumab joining the party , how much potential there will be for batoclimab in MG is still murky. Only way to really position batoclimab is that it shows somehow outlandishly superior efficacy profile over efgartigimod, which may or may not be possible due to the safety and convenience disadvantage (argenx is the only company that can use Halozyme's technology). However, we find batoclimab's pursuit in CIDP interesting; the management noted that 2 doses in OLE will inform dose response and if batoclimab's low dose will be sufficient for CIDP. Also, we expect argenx's upcoming CIDP data from ADHERE trial to offer more insight into anti-FcRn's role in CIDP. CIDP is a highly heterogeneous disease that is driven by likely multimodal pathophysiologies, not only driven by autoantibodies. As the disease can be driven by complement and T cells, we are unsure if efgartigimod will be effective broadly like IVIgs that use a shotgun approach with many unknown mechanisms of action offering an attractive first-line treatment option. Therefore, we believe it is hard to speculate whether the anti-FcRn will work across all CIDP patients and we will need to wait until argenx's ADHERE data to build conviction in CIDP. Our base-case view is that argenx will show some level of (stat sig) efficacy during part B portion of the ADHERE trial but don't show non-inferiority to IVIgs (ICE trial that showed ~33% placebo-adjusted reduction in relapse) due to a high placebo rate and robust multimodal mechanism of action of IVIg (unlike efgartigimod that only reduce IgG). We believe this can still position anti-FcRn as a 3rd or 4th line option for the refractory population who fail steroids or IVIg/SCIgs.

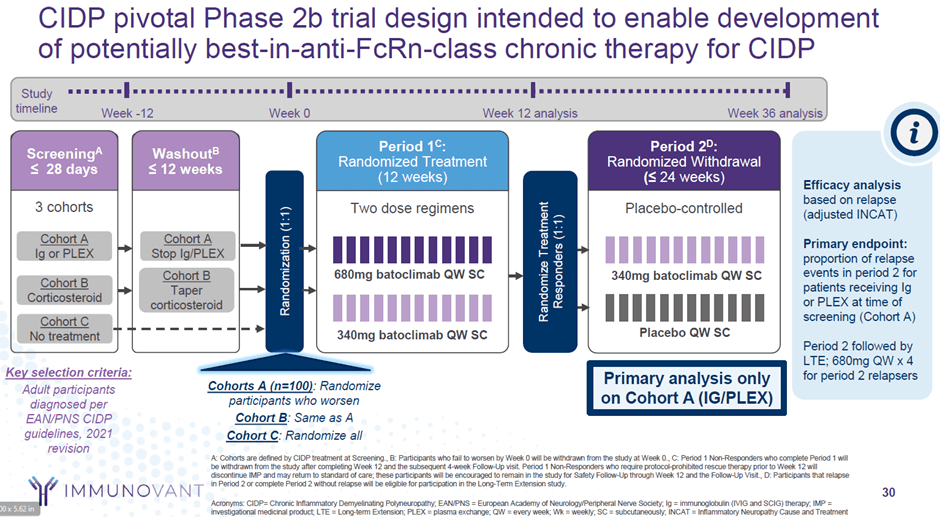

IMVT CIDP phase 2b trial (IMVT)

{kind=link}

The trial design of Immunovant seems comparable to argenx's ADHERE trial with robust washout and period 1 that can be eliminated potential non-active CIDP patients entering the trial and increase the placebo rate. We note that the only difference would be that period 2 seems shorter than argenx's 44 weeks which can be concerning as some patients in the placebo group may not relapse on time. Net net, if argenx's ADHERE trial comes out positively, we believe the IMVT's CIDP trial should show similar results to efgartigimod in terms of efficacy as both batoclimab and efgartigimod are anti-FcRn that reduce IgG levels after all. However, batoclimab's impact on albumin and CVD can be a key safety overhang and a disadvantage vs. efgartigimod as in CIDP; both anti-FcRn will be used as a chronic therapy (continuous dosing every weekly), unlike anti-FcRn's usage as a cyclical therapy in MG. Safety impact can compound with chronic long-term usage.

New generation anti-FcRn IMVT-1402 potentially has superior safety over batoclimab

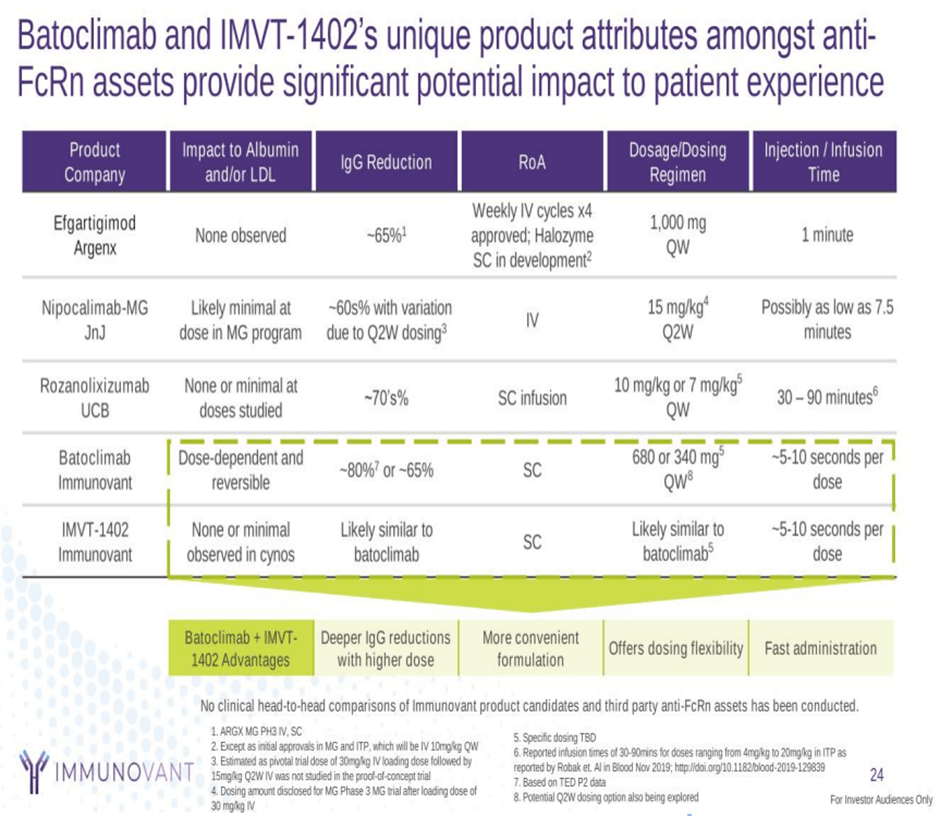

Interestingly, Immunovant is developing a new generation anti-FcRn that can perhaps avoid this albumin overhang. IMVT has recently presented head-to-head data from a monkey trial (cynos) that demonstrated comparable albumin/LDL interactions between IMVT-1402 vs. placebo. The data was promising as this was shown at a super-saturated dose. Although, it is unsure if cynos data can be fully translated into human data and whether clinical results will show significantly different safety profiles vs. batoclimab. Though, net-net, we find the recent publication highly promising for IMVT. We believe there is a chance that IMVT will forgo batoclimab and just pursue the development of IMVT-1402, which can create an inflection point for IMVT's stock price.

{kind=link}

Risks

The biggest risk revolves around IMVT-1402's clinical data; if it is inferior to efgartigimod, we expect Immunovant to sell off. Regulatory and commercial risk remains as the company is a first-time launcher without any drug approval. Financing risk is a concern as the company is not cash flow positive and may have to raise additional capital if they run out of cash which can lead to dilution of shareholder value.

Conclusion

In conclusion, we initiate Immunovant as a BUY due to i) modest valuation compared to argenx potentially offering a hedge against owning argenx, ii) optionality of the new generation IMVT-1402 that seems to show comparable impact to albumin vs. placebo, and iii) argenx's CIDP catalyst that can be a net-net positive to Immunovant either way. We believe the anti-FcRn class will be analogous to anti-TNF, where it can be used in numerous indications and will be a multi-billion dollar indication. This may be the reason why so many sponsors are trying to develop their own version of anti-FcRns and we see multiple anti-FcRn players sharing the market and newer generation anti-FcRn may show superior clinical profile over efgartigimod. Although argenx is significantly further into clinical development, especially in MG, and has a superior safety profile vs. batoclimab, we find it may make sense to long IMVT as a potential hedge as there is a probability that IMVT-1402 can be a better drug than efgartigimod or at least comparable to efgartigimod potentially competing in certain indications. Also, we find the upcoming argenx's CIDP readout can be net-net positive for IMVT, considering the fact that Immunovant is starting a pivotal phase 2b on CIDP shortly. If argenx's CIDP succeeds, Immunovant will pop, considering that Immunovant is the only other anti-FcRn being studied in CIDP except for Johnson & Johnson (JNJ); if efgartigimod fails in CIDP, it can also benefit Immunovant as its biggest competitor has been eliminated. Furthermore, we like the low valuation of IMVT (market cap: 2.5Bn/EV: 2Bn) vs. argenx (market cap: ~20Bn/ EV: 18Bn).

For further details see:

Immunovant: argenx At A 10% Valuation, Initiating With A Buy Rating