IMVT - Immunovant Could Be Poised For A Breakout In H2 2023

2023-05-24 13:14:23 ET

Summary

- Rating: Buy-rating maintained based on IMVT-1402's unique potential and impending Phase 1 catalyst in 2H 2023.

- Stock Upswing: Anticipate over 200% rise if Phase 1 MAD data showcases clean safety and broad autoimmune disease applicability.

- Argenx Readthrough: CIDP results from Argenx in July 2023 are expected to fuel further interest in Immunovant.

- Sound Financials: Comfortable cash position and attractive valuation underpin upside potential, given the scalability of the anti-FcRn platform.

Key catalyst update: IMVT-1402 data is expected in 2H

We maintain a non-consensus buy rating on Immunovant (IMVT) based on our confidence in IMVT-1402's differentiation optionality compared to other anti-FcRN classes and a clear phase 1 catalyst that is expected in 2H 2023. Especially the recent IND acceptance from the FDA adds to our thesis.

We believe the stock can go up meaningfully if the phase 1 MAD data expected in late 2023 demonstrates clean safety, defined as LDL, and no symptomatic reductions in albumin while providing some level of pharmacodynamic evidence. This would position IMVT-1402 as the only 2 low-dose subcutaneous FcRN agents besides JNJ's ( JNJ ) agent. We believe that provided that IMVT-1402 satisfies the aforementioned bar, it should provide a high degree of attractive opportunity for it to be used in multiple autoimmune diseases such as MG, CIDP, PV, ITP, and RA.

Our diligence suggests 20-90% of patients with 'traditional' autoimmune diseases such as ulcerative colitis, Crohn's disease, multiple sclerosis, lupus and others could have disease driven partly or entirely by auto-antibodies where anti-FcRn therapies could be developed...

Wells Fargo wrote recently.

In terms of safety, we anticipate minimal safety risks associated considering that fewer/lower doses are going to be used and (so far) anti-FcRn antibodies showed clean safety across the board, except for some LDL, head-aches, and albumin-related issues, which tend to be manageable and mild. Furthermore, if IMVT-1402's doses in Phase 1 come out clean, we do not expect any safety-related surprises in later-stage trials, as evidenced by argenx and UCB's trials.

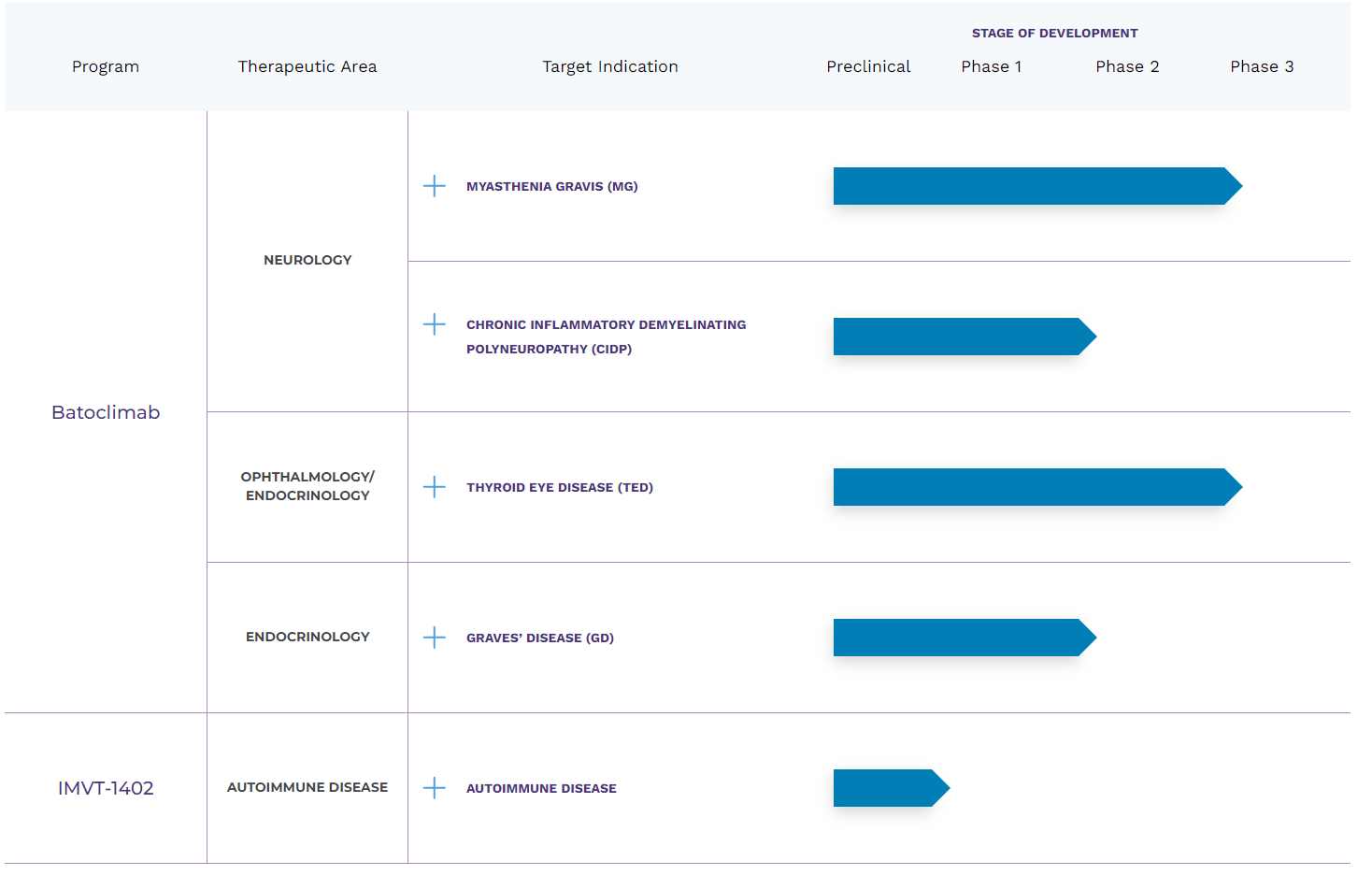

IMVT pipeline overview (Company source)

{kind=link}

Argenx July CIDP readout should be net positive for IMVT

Furthermore, we believe Argenx's CIDP readout expected in July 2023, should be a net positive catalyst for Immunovant because a) positive results of efgar should have a positive readthrough to IMVT as both efgartigimod and IMVT-1402 share the similar mechanism of action targeting CIDP and some investors may pile into IMVT as a potential hedge against argenx, and b) if argenx's CIDP readout does not come out to be positive, it should be net positive as one of the biggest competitors of IMVT got eliminated.

Catalysts on the horizon for the FcRn mechanism

Setting Trial details/event Timing Argenx and Vyvgart (IV approved, subcutaneous under review) CIDP Phase 3 Adhere trial (subcu) Q2'23 MG US approval of subcutaneous formulation Pdufa Jun 20, 2023 PV Phase 3 Address trial (subcu) H2'23 ITP Phase 3 Advance-SC H2'23 PC-POTS Proof of concept phase 2 Q4'23 J&J and nipcocalimab (IV in ph3, subcutaneous in early development) HDFN Open-label phase 2 Toplined positive Feb 2023 RA Proof-of-concept phase 2 H2'23 SLE Proof-of-concept phase 2 H2'23 wAIHA Phase 2/3 Q4'23 MG Phase 3 Q4'23 UCB and rozanolixizumab (subcutaneous infusion under review) MG Potential US/EU approvals Q2'23 Immunovant and batoclimab (subcutaneous in ph3) Graves' disease Initial phase 2 results (trial not started) H2'23 MG China phase 3 (run by Harbour Biomed) H2'23 Immunovant and IMVT-1402 (subcutaneous in preclinical) TBC Initial phase 1 data Mid-2023 Note: CIDP = chronic inflammatory demyelinating polyneuropathy; HDFN = haemolytic disease of the foetus and newborn; ITP = immune thrombocytopenia; MG = myasthenia gravis; PC-POTS = post-COVID-19 postural orthostatic tachycardia syndrome; PV = pemphigus vulgaris; RA = rheumatoid arthritis; SLE = systemic lupus erythematosus; wAIHA = warm autoimmune haemolytic anaemia. Source: Evaluate Pharma, clinicaltrials.gov & company communications, Evaluate Pharma

Strong financials and valuation

The company has an enterprise value of ~$2.7Bn and a cash balance of $380m, which we believe should provide a comfortable runway for 1-2 years (considering a $40-60m quarterly burn). We believe the current valuation is attractive considering Argenx is trading above $21Bn, albeit their platform is significantly ahead of IMVT in terms of the developmental process and showed superior safety; if IMVT-1402 shows some degree of positive readout (mentioned above) in phase 1, that alone should justify 200-300% rise in IMVT's valuation considering highly scalable nature of the anti-FcRN platform.

Risks

-

Clinical Trial Outcomes : Immunovant's lead candidate, IMVT-1402, is still in the experimental stage. Any negative or inconclusive results from ongoing or future trials, specifically regarding its LDL or albumin profile, could have a severe impact on the company's prospects and stock valuation.

-

Regulatory Approval Risk : IMVT-1402's success depends on obtaining necessary regulatory approvals from bodies like the FDA and EMA. If Immunovant fails to meet its stringent standards, it could face delays or rejection, adversely affecting the investment proposition.

-

Market Competition : Immunovant is developing one of only a few low-dose subcutaneous injectable FcRn drugs, but it's not alone. Other competitors, like Johnson & Johnson, are working on similar treatments. If competitors reach the market first or deliver more effective drugs, it could significantly undermine Immunovant's market position.

-

Execution Risk for Phase 1 Trials : Immunovant's decision to potentially run Phase 1 trials outside the US introduces unique risks, including navigating different regulatory environments, logistical challenges, or public perception. A failure to smoothly execute these trials could hamper progress and investor confidence.

Conclusion

We reaffirm our non-consensus buy rating on Immunovant, bolstered by our trust in IMVT-1402's unique market position and an upcoming Phase 1 catalyst expected in 2H 2023. We forecast a potential 200%+ stock surge if late 2023 Phase 1 MAD data demonstrate clean safety (i.e., no LDL and albumin issues), leading to potential use in multiple autoimmune diseases. Further bolstering our thesis is the FDA's recent IND acceptance, and we expect Argenx's CIDP readout in July 2023 to prove net positive for Immunovant. Despite inherent risks-like trial outcomes, regulatory approval, market competition, and trial execution-Immunovant's robust financials and attractive valuation ($2.7Bn EV, $380m cash), along with the scalable nature of the anti-FcRn platform, justify our bullish stance.

For further details see:

Immunovant Could Be Poised For A Breakout In H2 2023