IMVT - Immunovant: Data Sizzles But The Steak Isn't Done Yet (Rating Upgrade)

2023-09-26 11:10:50 ET

Summary

- Immunovant's IMVT-1402 shows early promise with dose-dependent IgG reduction and a decent safety profile, rejuvenating the company's drug pipeline.

- Despite a solid 20.9-month cash runway, escalating R&D expenses and liquidity concerns necessitate vigilant financial monitoring.

- Investment recommendation on IMVT stock: Shift from "Strong Sell" to "Hold," given the nascent promise in IMVT-1402 and remaining uncertainties in batoclimab and financials.

At a Glance

In this update on Immunovant, Inc. (IMVT), I dial back on my previous "Strong Sell" stance , invigorated by early-stage yet promising data on IMVT-1402-a drug showing dose-dependent IgG reduction with an acceptable safety profile. Concurrently, batoclimab, the company's lead candidate, still navigates a fierce competitive landscape and unsettled safety questions. Financially, a rising R&D burn rate is juxtaposed with a solid 20.9-month cash runway, requiring vigilant monitoring. While investor sentiment has propelled the stock, evidenced by a 70% intraday uptick and outperformance relative to SPY, underlying uncertainties mandate caution.

Given these mixed signals, I'm revising my recommendation to "Hold," as the forthcoming clinical and financial milestones could either substantiate or debunk the market's current enthusiasm.

Immunovant Q2 Earnings Report

To begin my analysis, looking at Immunovant's most recent earnings report , the company saw a substantial uptick in operating expenses, primarily driven by research and development (R&D) costs, which rose to $50.6M from $28.4M YoY. Acquired in-process R&D also appeared on the ledger at $12.5M, contributing to a net loss of $73.9M for the quarter. This loss, translated to a net loss per share of $0.57, signals an aggressive investment in pipeline development. While escalating expenses may raise eyebrows, it's crucial to understand that R&D investments in the biotech sector often precede potentially lucrative breakthroughs. However, the firm's R&D spend will need to yield demonstrable progress to justify the increased financial outlay.

Financial Health & Liquidity

Turning to Immunovant's balance sheet , the company had $329.96M in 'Cash and cash equivalents' as of June 30, 2023. There are no other liquid assets like marketable securities or investments mentioned. Over the last quarter, the company used $47.37M in operating activities. Extrapolating this to a monthly burn rate, Immunovant incurs approximately $15.79M monthly. Based on these numbers, Immunovant has an estimated cash runway of about 20.9 months. Note that these calculations are based on past data and may not hold in the future.

On the liquidity front, Immunovant is relatively well positioned with no mention of significant debt. However, the cash burn rate does necessitate attention; while the company has a cash runway that is not immediately alarming, ongoing operational expenditures could require further financing. Given the absence of debt and a considerable amount in stockholders' equity ($299.87M), the company has room to secure additional financing if needed, either through equity offerings or debt instruments. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

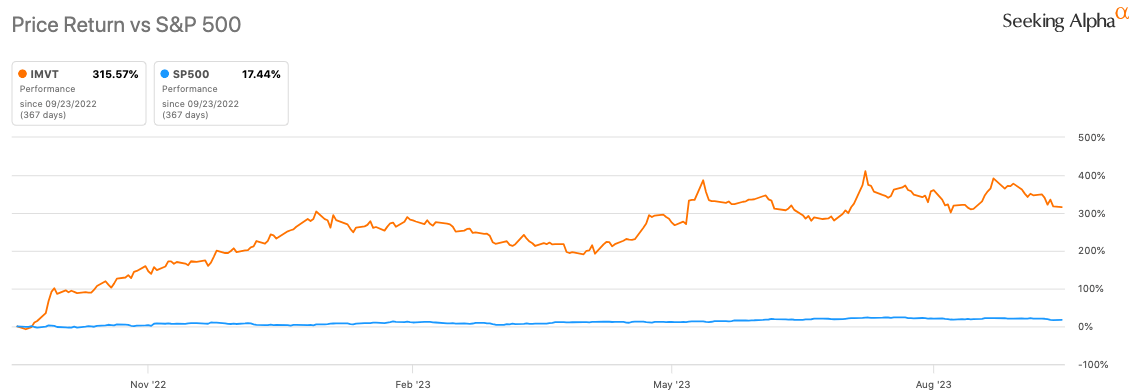

According to Seeking Alpha data, Immunovant's capital structure reveals solid liquidity given its cash holdings and lack of substantial debt, allowing room for leverage. While the market cap, prior to today's news, hovers around $2.65B, the absence of crippling debt balances the cash burn rate. Regarding growth prospects, analyst revenue projections for 2026 show a staggering 393.78% YoY increase, which if realized, could validate the company's heavy R&D investments. However, these are high-risk plays reliant on the success of lead candidates like batoclimab. Stock momentum has outperformed SPY over various timeframes, most notably +315.57% YoY, hinting at investor optimism.

{kind=link}

Ownership primarily lies with public corporations (56.48%), followed by institutions (42.71%), which demonstrates both stakeholder diversity and investment from large financial bodies. Insider trading reveals a pattern of recent sales , indicating caution. Short interest is 8.76%, which is moderately high and could be indicative of market skepticism or potential for a short squeeze.

Immunovant's IMVT-1402: A Promising But Early FcRn Inhibitor

The Phase 1 clinical trial data for Immunovant's IMVT-1402 offers several compelling points but should be approached with caution given the early stage of the data. The drug demonstrated a dose-dependent reduction in IgG levels without adverse impacts on serum albumin or LDL-C. Lowering IgG selectively in healthy individuals is a significant step; it suggests the drug's efficacy in modulating the immune response, vital for autoimmune conditions. However, it's essential to remember that these results are from a small, early-stage trial in healthy adults, and we don't yet know how these findings will translate into broader, more diverse patient populations.

The safety profile of IMVT-1402 is encouraging, with only mild-to-moderate adverse events observed. These favorable safety markers, combined with a robust 63% mean total IgG reduction in the 300 mg cohort, underscore the drug's potential as a best-in-class FcRn inhibitor. But again, these are initial findings and require validation in larger, longer-term studies. The ease of administration, via a 2 mL subcutaneous injection, adds to its potential patient compliance. While the stock's intraday 70% uptick reflects high investor confidence, it's crucial to understand that the clinical pathway ahead is long and fraught with potential challenges.

My Analysis & Recommendation On IMVT Stock

In retrospect, my previous call for a "Strong Sell" on Immunovant seems to have missed the mark, particularly in underestimating the early-stage promise of IMVT-1402. The recent Phase 1 data have reignited interest in the company's drug pipeline, indicating a dose-dependent reduction in IgG levels without significant adverse events. Moreover, the company deserves kudos for the rapid development of IMVT-1402, considering its Investigational New Drug application, or IND, was cleared just months prior. While this positive data has buoyed the stock, it's essential to temper enthusiasm with clinical pragmatism: we're still in the early innings of IMVT-1402's development. Moreover, batoclimab, the company's lead candidate, still needs to traverse a competitive landscape and potential safety concerns.

Investors should closely monitor several factors in the coming months. First, watch for developments around batoclimab's late-stage clinical trials and any comparative data against rivals like argenx's ( ARGX ) efgartigimod. Second, focus on how Immunovant plans to finance its significant monthly cash burn of approximately $15.79M, especially if milestones are missed or delayed. While the company currently has a cash runway of roughly 20.9 months, additional capital may be required to push its drug candidates through costly late-stage trials. Lastly, keep an eye on institutional activity and insider trading patterns. A spike in either could signal shifts in market sentiment that are not immediately apparent in publicly released data.

On balance, given the promising but early-stage data on IMVT-1402 and the ongoing questions surrounding batoclimab, I'm adjusting my investment recommendation to a "Hold." While there's considerable upside potential, the road to commercial viability for both compounds is laden with both scientific and regulatory hurdles. This isn't a time for precipitous action, either to acquire more shares or to liquidate existing holdings. The company's upcoming milestones offer significant catalysts that could either vindicate or invalidate the current market optimism. Until then, cautious optimism should be the order of the day.

For further details see:

Immunovant: Data Sizzles, But The Steak Isn't Done Yet (Rating Upgrade)